Quick Answer

IRS penalty abatement is relief that can reduce or remove certain IRS penalties when you qualify under the right path. The practical process is to classify the penalty, screen First-Time Abatement first, test reasonable cause with evidence, and apply exclusion checks early. Follow your notice instructions, use Form 843 if needed, and move to Appeals quickly after a denial instead of resubmitting the same story.

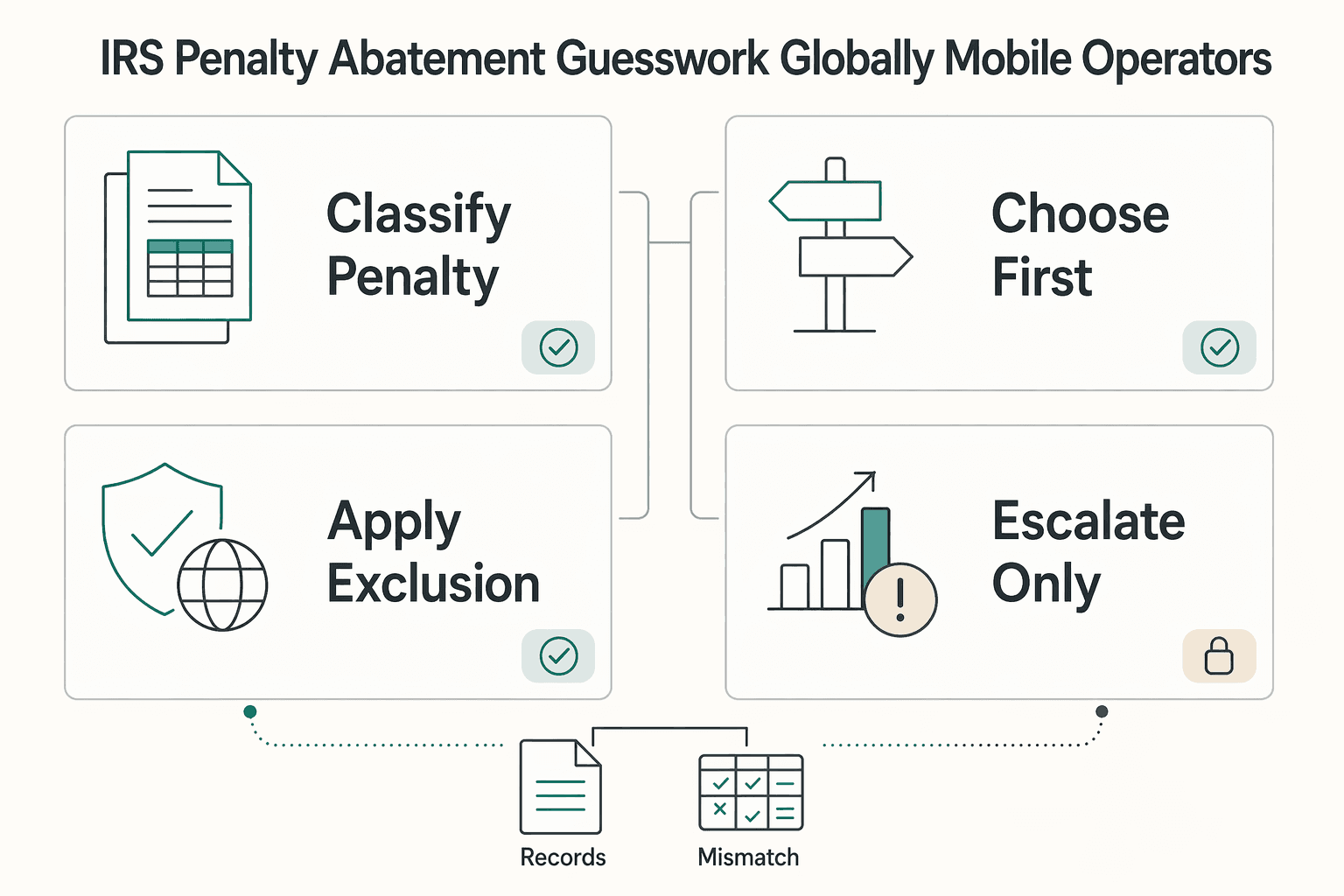

IRS penalty abatement without guesswork for globally mobile operators#

Treat IRS penalty abatement as a risk-control workflow: protect compliance first, then pursue relief.

| Workflow step | What to do | Expected outcome |

|---|---|---|

| Classify the penalty | Identify the exact penalty shown on your notice, and keep each penalty stream separate | You know which rules apply and avoid mixing unrelated arguments |

| Choose the first eligible path | Screen First-Time Abatement first. If FTA does not fit, test reasonable cause | You pick a relief path with a defensible eligibility basis |

| Apply exclusion checks early | Confirm your chosen path is valid for that penalty category | You drop claims the IRS is likely to reject on scope alone |

| Escalate only when needed | Start with intake and request review. If phone approval does not happen, move to a written request with Form 843 | You keep momentum while preserving an audit-ready record |

If you run a business of one, you want to reduce a tax penalty without creating a second problem. That second problem usually shows up when claims are weak, penalty types get mixed, or the submission path is wrong. This guide gives you safe defaults within the Internal Revenue Service framework so you can move in order instead of improvising.

Start with one operating rule: penalty abatement is not automatic. Relief is case by case, especially under reasonable cause. Standards can also differ by penalty type and Internal Revenue Code authority. That is why aggressive, one-size templates can fail.

Use the same sequence in practice:

- Classify the penalty. Identify the exact penalty shown on your notice, and keep each penalty stream separate.

Expected outcome: You know which rules apply and avoid mixing unrelated arguments.

- Choose the first eligible path. Screen First-Time Abatement first, since it is a common administrative waiver and depends on good compliance history. That includes filing the same return type for the prior 3 tax years when required. If FTA does not fit, test reasonable cause.

Expected outcome: You pick a relief path with a defensible eligibility basis.

- Apply exclusion checks early. Confirm your chosen path is valid for that penalty category. Reasonable cause does not cover certain penalties, including estimated tax penalties.

Expected outcome: You drop claims the IRS is likely to reject on scope alone.

- Escalate only when needed. Start with intake and request review. If phone approval does not happen, move to a written request with Form 843. If the IRS denies relief, move to the appeal-eligibility step instead of resubmitting the same story.

Expected outcome: You keep momentum while preserving an audit-ready record.

Picture a consultant managing cross-border travel who gets a penalty notice during a filing-season crunch. In most cases, the safe move is to run this sequence, document each decision, and escalate only after each gate fails. For broader operating guardrails, keep your compliance system aligned with The Ultimate Digital Nomad Tax Survival Guide for 2026.

What to prepare before you request penalty abatement#

Prepare a penalty-specific evidence file before you request relief, so your facts are clear and your request is easier to route correctly.

You're not writing yet. You're building the file that makes your request verifiable.

Before you start

- Work from the IRS notice first, not memory. * Pull only the return family tied to the penalty at issue, such as the Form 1040 series, Form 1065, or Form 1120. * Create one working folder per penalty item.

- Step 1. Gather the base record set. Collect the IRS notice or letter, your filing and payment history, and the underlying return documents for the account in question. This set supports First-Time Abatement screening and reasonable-cause review.

Verification point: You can identify the exact penalty you want relieved and the exact return context that produced it.

- Step 2. Build a chronological reasonable-cause timeline. Write what happened, when it happened, how it blocked filing or payment, and what compliance attempts you made anyway. Pair each event with a supporting record so your narrative stays factual under IRS review.

Verification point: Every sentence in your timeline maps to a date, an action, and a document.

- Step 3. Split evidence by penalty type. Keep separate mini-packets for Failure to File, Failure to Pay, and Failure to Deposit penalties because eligibility treatment differs by penalty type.

| Penalty type | What to include first | Why this separation helps |

|---|---|---|

| Failure to File | Filing timeline and filing-attempt records | Supports filing-fact analysis |

| Failure to Pay | Payment history and payment-attempt records | Supports payment-fact analysis |

| Failure to Deposit | Deposit-related account records | Keeps deposit facts distinct |

- Step 4. Add a rules-check page. Flag exclusions up front, including that reasonable cause does not apply to certain penalties such as the estimated tax penalty. Add a quick check for First-Time Abatement history, including whether you filed the same return type for the prior 3 tax years when required. Note where Internal Revenue Code treatment can differ by penalty type.

Verification point: Your rules-check page shows clear go or no-go decisions before submission.

Which IRS relief path should you choose first?#

Choose this sequence: check First-Time Abate first, test reasonable cause second, then review administrative waivers or statutory exceptions, and escalate only after a denial.

Once your evidence is organized, choose the path before you draft the request. The order matters because it keeps your case tight, reduces avoidable rejections, and prevents over-claiming.

| Relief path | Use it when | Verification check |

|---|---|---|

| First-Time Abate (FTA) | Your penalty type falls in scope and your compliance history supports it | Confirm the same return type was filed for the prior 3 tax years when required |

| Reasonable cause | You exercised ordinary care and prudence but still could not file or pay on time | Match your timeline to proof of what happened, when it happened, and what you tried |

| Administrative waivers or statutory exceptions | FTA and reasonable cause do not fit, but the penalty may qualify under another IRS channel | Tie the penalty to the specific legal or administrative basis before you submit |

- Step 1. Run the First-Time Abate screen first. Start here because FTA is a common administrative waiver path. If your records touch payroll accounts, keep Form 940, Form 941, Form 944, and Form 945 context clear so you evaluate the right account history rather than a mixed file.

Expected outcome: You confirm whether FTA fits before you spend time building a longer reasonable cause argument.

- Step 2. Test reasonable cause with strict evidence rules. Use this path only when facts show ordinary care and prudence plus an actual inability to comply on time. Keep each argument penalty-specific, and do not claim reasonable cause for estimated tax penalty categories.

Expected outcome: You keep a defensible, case-by-case narrative the IRS can verify.

- Step 3. Check administrative waivers and statutory exceptions if Step 1 and Step 2 fail. Do not recycle a weak reasonable cause claim. Route to the relief channel that matches the penalty rules instead of forcing one template across every case.

Expected outcome: You preserve credibility and avoid duplicate denials.

- Step 4. Escalate with structure when the IRS says no. If phone review does not resolve your request, move to a written submission with Form 843. If the IRS denies relief, request an IRS Independent Office of Appeals conference or hearing. Treat the rejection letter date as an operations deadline because you generally have 30 days to file an appeal request.

Expected outcome: You move forward on a formal track instead of repeating unsupported requests.

If you are juggling multiple notices in the same season, this sequence helps you split cases and choose the right path for each penalty. It also helps you protect your compliance posture while you pursue relief.

How do you validate your penalty type and eligibility fast?#

Validate notice language first, then map each line to a penalty category before you submit a request.

Before you draft anything, run a fast triage so you do not force the wrong rule onto the wrong penalty. This step is about clean classification and scope control.

- Step 1. Map the notice to a named penalty category. Read the IRS notice line by line and label each charge as Accuracy-related penalty, Information return penalties, Failure to pay penalty, or another explicit category. IRS notices state the reason for the charge and the next action, so use that text as your primary classification input.

Verification point: You can point to one notice sentence that supports each category label.

- Step 2. Run a scope check for higher-risk form contexts. Treat Form W-2 and Form 1099 issues as information-return workflows, not generic late-filing stories. Treat Form 3520 and Form 5471 as international reporting tracks where eligibility can narrow, and not all international information-reporting penalties qualify for reasonable cause.

Verification point: Your worksheet flags category-specific constraints before you draft a narrative.

| Context | Fast eligibility check | Why it matters |

|---|---|---|

| Form W-2 and Form 1099 information returns | Check notice instructions and response window. For Notice 972CG, respond in 45 days, or 60 days if you are a foreign filer | IRS instructs you to respond before assessment, so deadline control is part of eligibility triage |

| Form 3520 and Form 5471 international reporting | Confirm penalty-specific relief rules first, then test reasonable cause availability | These penalties can follow narrower relief rules than standard failure-to-file or failure-to-pay cases |

| Form 5471 failure | Mark base exposure at $10,000 per failure before strategy selection | Knowing the base exposure helps you triage faster and decide whether to escalate |

-

Step 3. Add a rules-variance box to your packet. Separate IRS baseline guidance from Internal Revenue Manual (IRM 20.1.1) operational guidance. Use IRS baseline rules to decide eligibility, then use IRM detail to shape workflow and documentation order. Do not treat IRM language as a substitute for statute.

-

Step 4. Insert an automation verification note. If NATP 2026 summaries suggest automatic First-Time Abatement, treat that claim as unverified until current IRS language confirms it.

Verification point: Your file shows a dated confirmation step before you rely on automation.

If you receive both a failure-to-pay notice and an information-return notice, split validation into two tracks. You will move faster, and you will keep each penalty tied to the right rule set.

Build your audit-ready request packet that survives scrutiny#

Build your packet so every claim maps to one document and one rule before you submit.

| Packet item | What to include | Why it helps |

|---|---|---|

| Cover letter | Name the relief path, the exact penalty, the tax period, and the account context | A reviewer can understand what you want removed, why, and where the proof sits |

| Fact matrix | Event, proof, penalty impact | It forces precision and keeps your case factual instead of emotional |

| Document index and version log | Number exhibits, lock file names, and track each edit date | You preserve consistency if your request needs follow-up |

| Final scrutiny check | Confirm your chronology, confirm your compliance attempts, and remove any claim that lacks evidence | It protects credibility |

Once the penalty type and relief path are clear, build a reviewer-ready file. The goal is not a long narrative. It is a packet that lets the IRS confirm facts quickly and see a clear path to the relief you requested.

- Step 1. Draft a tight cover letter. Name the relief path you want, such as reasonable cause or another relief path where supported. State the exact penalty, tax period, and account context. If you move to a written request, align the letter with Form 843 requirements and include the applicable IRC section for assessed-penalty abatement requests.

Expected outcome: A reviewer can read one page and understand what you want removed, why, and where the proof sits.

- Step 2. Build a fact matrix that controls your narrative. Use three columns only: event, proof, penalty impact. This format is optional, but it forces precision and keeps your case factual instead of emotional.

| Event | Proof | Penalty impact |

|---|---|---|

| What happened and when | Notice excerpt, filing record, payment record, or other support | Shows how the event triggered or affected the tax penalty |

| Compliance attempt you made | Submission receipt, payment attempt, account note, or correspondence | Supports your reasonable cause position with action, not opinion |

| Follow-up action after notice | Response draft, corrected filing, or payment plan record | Shows ongoing good-faith behavior during relief review |

- Step 3. Add a document index and version log. Number exhibits, lock file names, and track each edit date. If clarification is requested, you can respond with the same structure instead of rewriting your story under pressure.

Expected outcome: You preserve consistency if your request needs follow-up.

- Step 4. Run a final scrutiny check before sending. Confirm your chronology, confirm your compliance attempts, and remove any claim that lacks evidence. Do not route estimated tax penalty arguments through reasonable cause. As U.S. tax resolution attorney Lance Drury puts it, "After explaining your situation, presenting the facts, and providing the documentation, there are still no guarantees." Treat that as practical perspective, not IRS authority.

What if IRS says no and you need to escalate?#

Escalate a denied penalty-relief request with a deadline-driven appeal built on facts, not frustration.

A denial is your cue to tighten the case. Control timing, trim weak arguments, and submit an Appeals-ready record.

- Step 1. Confirm appeal eligibility before you draft anything. Read the rejection letter and confirm you meet the prerequisites for an IRS Independent Office of Appeals conference or hearing. Do not assume every denied penalty request qualifies automatically. Use Publication 4576 as your process anchor so you follow the Appeals sequence from the start.

Expected outcome: You make a clear go or no-go decision on escalation.

- Step 2. Build a deadline control block from the rejection letter. Treat the letter date and filing deadline as hard operational gates. You generally get 30 days to request an appeal, but your letter controls the specific deadline. Assign an owner, lock a submission date, and add an internal buffer so routine delays do not kill your case.

| Control item | What to record | Why it matters |

|---|---|---|

| Rejection letter date | Date shown on letter | Starts your appeals clock |

| Appeal deadline | Exact date listed in letter | Overrides assumptions |

| Internal submit date | Your target date before deadline | Creates execution margin |

| Packet owner | Name and role | Prevents handoff gaps |

- Step 3. Reframe the case for independent review. Appeals reviews facts and law independently, so cut weak claims and keep only supported arguments. Center documented facts for your path, whether reasonable cause, statutory exceptions, or administrative waivers. Align each argument to the penalty category and the facts in your file so reviewers can validate quickly.

Expected outcome: You produce a shorter, stronger narrative that survives scrutiny.

- Step 4. Submit a clean appeals packet and control new evidence. Include the denial letter, your core evidence set, and your updated argument map. If you add new documentation, expect possible referral back to Compliance review, so submit only material that directly strengthens your position. Cut noise and provide as much relevant supporting documentation as possible.

Common mistakes and recovery actions for freelancers and consultants#

The safest move is one penalty type, one relief path, and one return context per request.

Most failed requests do not fail on effort. They fail on classification, scope, and mixed narratives. Use this section as a pre-flight check before you submit. Before you start, pull the IRS notice, your draft narrative, and the return package tied to the penalty in question.

| Common mistake | Why it breaks | Recovery action |

|---|---|---|

| One vague request for multiple penalties | Relief is penalty-specific, so mixed claims create routing and logic conflicts | Split into separate tracks for each penalty category, with its own evidence set |

| Over-claiming Reasonable cause | Reasonable cause is case by case and does not apply to certain categories, including Estimated tax penalty | Route excluded categories to the IRS path identified for that penalty instead of forcing a reasonable-cause argument |

| Treating third-party summaries as policy | Secondary summaries can lag or overstate changes | Treat NATP-style updates as secondary and confirm current IRS language before operational decisions |

| Missing return-type detail | Reviewers cannot map history and eligibility without return-type context | State the exact return type in your narrative and keep supporting records aligned to that same return type |

- Step 1. Split your request by penalty label. Build separate narratives and attachments for each penalty category. Hypothetical: you combine a payment issue and a deposit issue in one letter, and the IRS cannot match the facts to one abatement path.

Expected outcome: Each file maps cleanly to one relief decision.

- Step 2. Route excluded penalties immediately. If the issue is estimated tax, do not force a reasonable cause argument. Move to the appropriate alternative track early so you do not burn time on a non-qualifying request.

Expected outcome: You stop preventable denials caused by ineligible framing.

- Step 3. Verify policy claims before you execute. Keep First-Time Abatement checks tied to current IRS language, then validate the same return-type compliance history across the past three tax years when relevant. Do not operationalize automation claims until the IRS confirms them.

Expected outcome: Your workflow stays current and audit-defensible.

- Step 4. Lock return-context precision into the narrative. Name the return type up front and keep supporting records aligned to that return type. If records are incomplete for business filings such as Form 1065 or Form 1120-S, correct the package before resubmission so the reviewer can process your relief request without guesswork.

Expected outcome: Faster reviewer comprehension and fewer clarification loops.

Run this safe-default checklist and decide your next move#

Use this checklist to run the process like an operator, with one clear path, one clean packet, and one escalation plan.

| Step | Action | Key point |

|---|---|---|

| 1 | Label the exact penalty from your notice, then choose the matching route | Check FTA eligibility against the same return-type filing history for the past 3 tax years |

| 2 | Create a packet that includes your notice copy, a dated timeline, and a penalty-specific narrative for each penalty item | If you claim reasonable cause, state what happened, when it happened, and attach supporting records |

| 3 | Follow the instructions in your IRS notice first | If your notice route includes phone contact, request relief there, then submit Form 843 in writing if phone approval does not happen |

| 4 | Move immediately to penalty-appeal eligibility and prepare your appeal package if the IRS denies relief | Use Publication 4576 for a process overview. Your rejection letter gives the controlling deadline |

| 5 | Use this playbook first, then bring in a qualified tax professional when facts get complex or records stay incomplete | Review the broader operations baseline if you need it |

Use this as your execution layer. Copy it into your workflow tool, and do not submit until every line is checked.

- Step 1. Classify the tax penalty and lock one relief path.

Start by labeling the exact penalty from your notice. Then choose the matching route: First-Time Abate (FTA), reasonable cause, administrative waiver, or statutory exception. Check FTA eligibility against the same return-type filing history for the past 3 tax years. Expected outcome: You choose one defensible relief path instead of mixing arguments.

- Step 2. Build a penalty-specific packet before contact.

Create a packet that includes your notice copy, a dated timeline, and a penalty-specific narrative for each penalty item. If you claim reasonable cause, state what happened, when it happened, and attach supporting records. Expected outcome: Your relief request reads as facts first, not opinions.

- Step 3. Submit through the IRS channel in order.

Follow the instructions in your IRS notice first. If your notice route includes phone contact, request relief there, then submit Form 843 in writing if phone approval does not happen. If you ask for reasonable cause but qualify for First-Time Abate, the IRS can apply FTA. Expected outcome: You use the documented workflow without guessing.

- Step 4. Pre-build your denial response path.

If the IRS denies relief, move immediately to penalty-appeal eligibility and prepare your appeal package. Use Publication 4576 for a process overview. You generally have 30 days from the date of the rejection letter, and your rejection letter gives the controlling deadline. Expected outcome: You protect appeal rights and avoid deadline misses.

- Step 5. Choose the next move with a safe default.

Hypothetical: you run a solo consulting business and your records span multiple countries with inconsistent backups. Use this playbook first, then bring in a qualified tax professional when facts get complex or records stay incomplete. If you need a broader operations baseline, review The Ultimate Digital Nomad Tax Survival Guide for 2025.

Frequently Asked Questions

What is IRS penalty abatement?

IRS penalty abatement is IRS relief that reduces or removes a tax penalty when you qualify under an approved path. For most operators, that means First-Time Abatement, reasonable cause, or a statutory exception. Use the path that matches your notice and penalty category, not the path you prefer.

Who qualifies for reasonable cause relief?

You qualify for reasonable cause when your facts show you tried to comply but circumstances outside your control blocked timely compliance. The IRS reviews this claim case by case, so your timeline and records drive the decision. Lead with verifiable events, then map each event to the penalty impact.

Does reasonable cause apply to estimated tax penalties?

No. The IRS excludes the estimated tax penalty from standard reasonable cause treatment. If your notice points to estimated tax, move to the specific relief track for that penalty instead of forcing a reasonable cause argument.

Which penalties are most commonly abated?

IRS guidance identifies penalties that may qualify for relief, including failure-to-file and failure-to-pay categories, plus estimated tax underpayment contexts under separate rules. It does not provide a ranked list of the most commonly abated penalties in this guidance set. Your safe move is to classify the exact penalty on your notice, then choose the matching relief route.

How do I request relief after an IRS notice?

Follow the instructions in the notice first. Then call the number on the notice to request relief, since the IRS can confirm approval status during that call in some cases. If phone resolution does not happen, submit a written request using Form 843 with a clean, penalty-specific narrative and your supporting records.

How long do I have to appeal a denied request?

Do not assume a universal deadline. The IRS directs denied requests to penalty appeal eligibility guidance, and your letter controls your next steps. Treat the deadline in your rejection letter as the operational date, then prepare your appeal materials immediately.

Is First-Time Abatement automatic in 2026?

Treat full automation claims as unconfirmed until current IRS language explicitly confirms them. Current IRS administrative guidance still describes active request workflows, including phone and written requests. Run First-Time Abatement as an eligibility check, including compliance history for the past three tax years, and keep a manual submission plan ready.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

The Best Digital Nomad Cities for Entrepreneurs and Startups

Choosing a nomad base for your company is an execution decision first. Lifestyle matters, but it belongs in the second round. The costly mistakes usually show up after the city-ranking stage, when a place that looks great online turns into a slow or expensive setup once you start invoicing, signing contracts, and working against real deadlines.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.