Quick Answer

Use EBITDA as a screening metric, then verify it before trusting it for payment decisions. What is ebitda in this context: earnings before interest, taxes, depreciation, and amortization, rebuilt from traceable lines or a clean bridge from GAAP results. After that, compare it with operating cash flow and debt exposure before agreeing to flexible billing. If reconciliation is weak or cash conversion is poor, shorten billing cycles, tighten milestones, or require partial prepayment.

The Executive Briefing: What You Actually Need to Know About EBITDA in 5 Minutes#

Use EBITDA as a fast screening signal, not as proof that a client can pay you on time. It shows earnings before interest, taxes, depreciation, and amortization. Then validate that signal with cash-based checks before you agree to flexible payment terms.

EBITDA stands for earnings before interest, taxes, depreciation, and amortization. For invoice risk, each add-back can help, but each one also removes part of the cash reality you still need to test. Depending on the statements you have, use the method that matches the line items you can actually trace.

- Interest: helps you compare operations without financing-structure noise, but it does not show cash available for payments.

- Taxes: are added back in EBITDA, but tax payments still reduce cash.

- Depreciation and amortization: are added back in EBITDA; if D&A is not shown separately on the income statement, pull it from the cash flow statement.

| Approach | Calculation path | Required line items | Best used when | Common mistake to avoid |

|---|---|---|---|---|

| Bottom-up | Net income + interest + taxes + depreciation + amortization | Net income, interest expense, tax expense, D&A | You have a full income statement and want to rebuild the number directly | Missing D&A when it is not shown separately. Pull it from the cash flow statement |

| Top-down | Operating profit + depreciation + amortization | Operating profit (operating income), D&A | Operating profit is clearly shown and you need a fast check | Adding interest or taxes again and double-counting exclusions already outside operating profit |

| Company-reported EBITDA or Adjusted EBITDA | Start with management's figure only after reconciliation to the closest GAAP measure | Reported EBITDA, comparable GAAP measure, reconciliation bridge | You receive a deck, summary, or lender pack instead of raw statements | Accepting add-backs that remove normal, recurring cash operating expenses |

If you cannot trace EBITDA to named line items, do not treat it as reliable. It is a non-GAAP measure, and there is no single universal formula, so definitions can vary. Before you rely on it, run this operator checklist.

- Compare EBITDA to operating cash flow (cash flow from operations) to see whether reported operating earnings are turning into cash.

- Watch working-capital signals such as receivables, payables, and inventory, which can make EBITDA look solid while cash is tight.

- Ask for a clear reconciliation from GAAP results to EBITDA. For public disclosures, Regulation G requires the comparable GAAP measure and a quantitative reconciliation for historical periods.

- Remember that operating cash flow still excludes capital expenditures, so it is not full free cash flow.

The practical takeaway is simple: use EBITDA to screen, then confirm with cash evidence before you lock payment terms. Next, request the income statement, cash flow statement, and any EBITDA reconciliation. Compare operating profit with operating cash flow, and flag anything you cannot tie back to source lines.

You might also find this useful: What is 'Deferred Revenue' and How to Account for It.

Your Three-Step Playbook for Vetting Any Private Company Client#

Use this three-step flow to set payment risk before you sign: ask for usable financial context, test whether the story holds together, then set terms based on the risk you actually see. EBITDA can help you screen a client, but it should not decide the deal by itself.

Step 1 Ask early and professionally#

Start the ask before the contract is final. Frame it as routine due diligence for payment structure, and use a request like this:

| Request item | When | Key check |

|---|---|---|

| Core reporting package the company already relies on internally | Request first | Clear line-item traceability |

| EBITDA bridge or reconciliation | If they cite EBITDA or adjusted EBITDA | Reconciliation when adjusted figures are used |

| Condensed management summary covering earnings and cash movement for the same period | If access is limited | Same reporting period |

| Short note on who approves invoices and releases payments | If access is limited | Who approves invoices and releases payments |

"Before we finalize scope and billing, please share the latest financial reporting package your team uses for planning and lender/investor updates, including any EBITDA or adjusted EBITDA reconciliation. We use this only to set delivery and payment structure, and we treat shared information as confidential."

In practice, ask first for:

- The core reporting package they already rely on internally.

- The EBITDA bridge or reconciliation if they cite EBITDA or adjusted EBITDA.

If access is limited, request:

- A condensed management summary covering earnings and cash movement for the same period.

- A short note on who approves invoices and releases payments.

Your minimum standard is consistency: the same reporting period, clear line-item traceability, and a reconciliation when adjusted figures are used. If that is missing, pause and ask follow-up questions before you extend flexible terms.

If the company is in an acquisition or integration phase, add one more check. Ask who currently owns approval and payment decisions. Execution risk is real, and transitions can blur decision rights and operating priorities, especially in the first 100 days post-acquisition.

Step 2 Compare EBITDA to cash-side signals and operating reality#

What you want here is coherence, not perfection. A single metric will not tell you enough. The question is whether the earnings story, the cash story, and the operating setup point in the same direction.

| Pattern you see | What it may mean | What you should do next |

|---|---|---|

| EBITDA trend and cash-flow trend do not move together | The operating story may be incomplete, or timing effects need clarification | Ask for a short bridge explaining the gap and keep terms tighter until the explanation is clear |

| EBITDA is presented, but supporting diligence detail is thin or unavailable | You cannot test how the headline metric connects to operating reality | Ask for a concise management snapshot for the same period and keep terms tighter until clarity improves |

| EBITDA looks strong, but approval ownership is unclear during ownership or org changes | Execution complexity can blur decision rights even when headline metrics look fine | Confirm approver names, approval path, and escalation contact before kickoff |

| Adjusted EBITDA includes multiple add-backs without a clean bridge | The figure may depend heavily on assumptions | Recalculate from disclosed lines where possible. If that is not possible, treat it as a caution flag |

A mismatch is not an automatic failure. It is a signal to tighten controls until the financial and operational story is defensible.

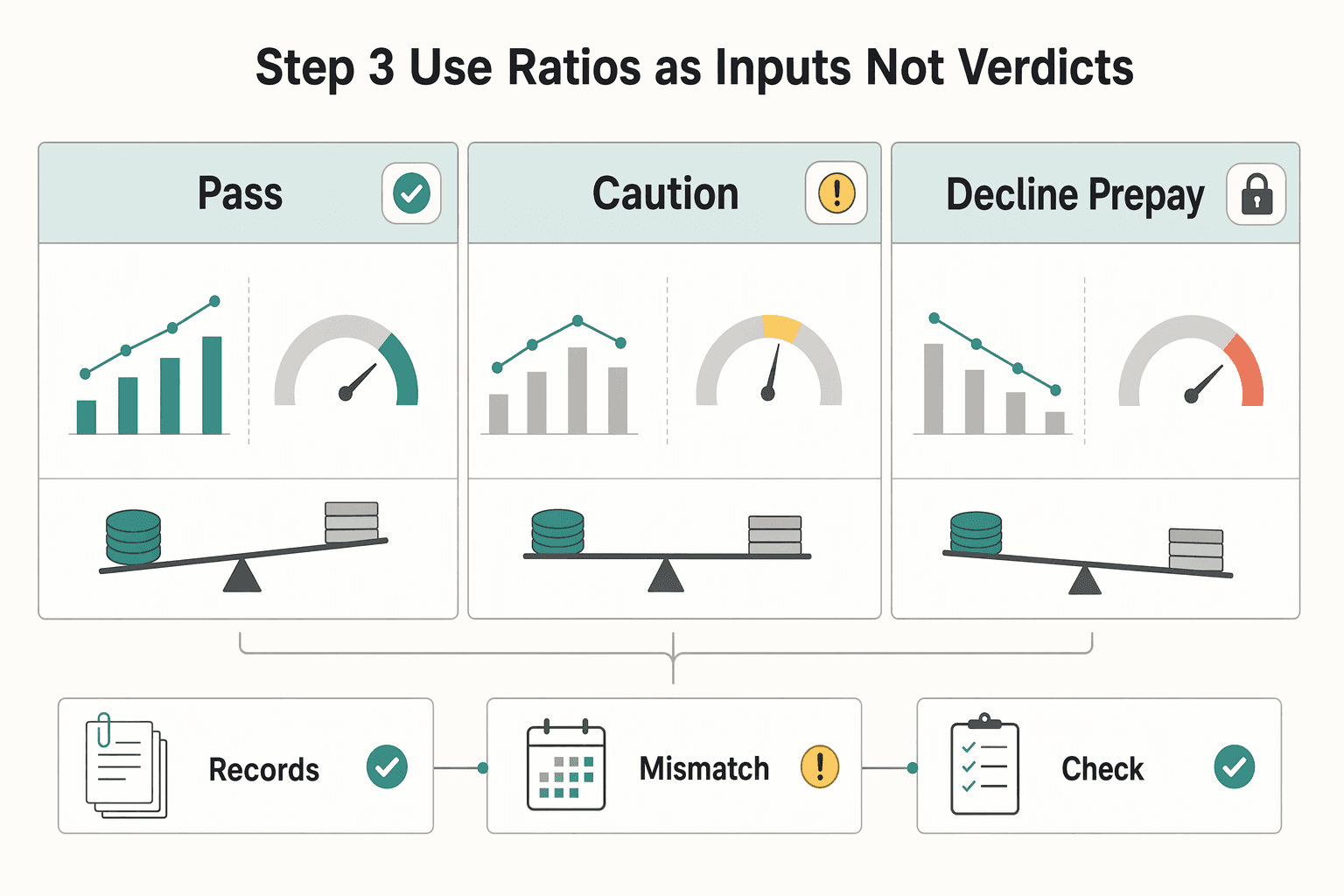

Step 3 Use ratios as inputs, not verdicts#

Ratios can sharpen your view, but only if the underlying definitions and periods are consistent. Use EBITDA margin and debt-to-EBITDA to inform your terms, not to approve a client on their own.

| Posture | What it means | Terms |

|---|---|---|

| Pass | Financial story is coherent, reconciliation is clear, and approval ownership is clear | Standard deposit and milestone terms |

| Caution | Partial visibility, unresolved mismatches, or transition-phase execution risk | Higher deposit, shorter billing cadence, and tighter scope/change controls |

| Decline or prepay only | Basic diligence is refused or key numbers cannot be reconciled | Prepayment or walking away |

Keep the ratio check disciplined:

- Match reporting periods across revenue, EBITDA, and debt.

- Confirm what "debt" includes in their reporting.

- If adjusted EBITDA is used, compare ratios using both reported and reconstructed figures.

For cutoffs, keep each value unresolved until relevant comparables are verified:

- EBITDA margin reference: Current margin reference pending industry/source-record verification.

- Debt-to-EBITDA alert level: Current threshold pending finance/source-record verification.

If you want a mechanics refresher, see A Guide to Financial Ratios for Business Health. Then use the posture above to set terms that match the risk you actually see.

If you want a deeper dive, read Hiring Your First Subcontractor: Legal and Financial Steps. After you compare a prospect's EBITDA to cash flow and debt, pressure-test what you actually keep per invoice with the Payment Fee Comparison.

Turning the Lens Inward: Your Business-of-One#

The same discipline applies to your own business. If you want a clearer read on operating performance, separate core operations from owner-specific choices.

Step 1 Choose the right earnings lens#

Pick one primary lens and label it clearly every time you use it. EBITDA isolates operating performance before interest, taxes, depreciation, and amortization, and it is not a standardized GAAP/IFRS metric. A common build starts with net income and adds those items back.

For an owner-operated business, SDE (Seller's Discretionary Earnings) is often the more relevant cash-flow lens because it is meant to reflect the owner's full financial benefit. The key difference is simple: SDE adjusts owner compensation, while EBITDA does not.

Whatever you choose, use one definition consistently and keep a simple reconciliation from net income to your adjusted number each period. That discipline prevents drift and makes your decisions easier to trust.

Step 2 Sort add-backs before you count them#

This is where self-assessment usually goes wrong. Do not treat every painful expense as an add-back. Classify each item first, then decide.

| Adjustment category | Why it may be adjusted | Common mistake that overstates performance |

|---|---|---|

| Recurring operating costs | Usually not adjusted because they are part of normal delivery and operations | Adding back normal, recurring cash operating expenses needed to run the business |

| Owner-discretionary items | Adjusted in SDE to remove owner-specific compensation or spending choices | Assuming every owner-related cost is discretionary when part of it is operational |

| One-off adjustments | Adjusted to normalize a period when a cost is genuinely non-recurring | Labeling repeated "special" costs as one-time every year |

If an item is borderline, verify the treatment with your accountant before you adjust it. Keep the support tight: where the item appears in your books and a short reason it is discretionary or non-recurring.

Step 3 Track consistently, then act on direction#

A single headline number matters less than a clean trend. Track the metric the same way each month or quarter, then use the direction of that trend to inform decisions on pricing and cost management.

| File item | What the file should show |

|---|---|

| Metric definition | A consistent metric definition |

| Net income | A reconciliation to net income by period |

| Material adjustments | Support for each material adjustment |

Turn that trend into action:

- If earnings trend up, you may have a stronger case for pricing changes, capacity investment, or financing discussions.

- If earnings flatten or fall, tighten scope, reduce underpriced work, and slow fixed-cost commitments until performance stabilizes.

These same records also support exit and financing conversations. Adjustment choices can materially change value when SDE multiples are used, so your file should always show the same three things: a consistent metric definition, a reconciliation to net income by period, and support for each material adjustment.

Related: How to Perform a Business Valuation for a Small Agency.

The Gruv Bottom Line: From Metric to Mindset#

Once you understand EBITDA, the practical shift is simple: stop making client-risk calls on instinct alone and start using a repeatable screen. EBITDA is one operating signal. The real decision comes from checking that signal against cash flow, debt load, and the terms you are about to sign.

Step 1#

Start with the number, then verify how it was built. EBITDA is a non-GAAP measure. It is not standardized under GAAP or IFRS, so definitions can vary and the reconciliation matters more than the headline. In public-company disclosures, that means showing the most directly comparable GAAP metric and reconciling to it. Ask for the bridge to EBITDA, and confirm that the same definition is used across periods.

A common failure mode is easy to miss: the definition changes over time, or an adjusted figure strips out normal recurring cash operating expenses and makes performance look cleaner than it is.

Step 2#

Use EBITDA to shape payment-risk decisions, not replace them. It can be a rough cash-flow proxy, but it is not a full cash metric. Compare profitability with cash from operating activities. If EBITDA looks strong but operating cash flow is weak, tighten terms before work starts. That may mean shorter billing cycles, milestone billing, or partial prepayment.

If debt is material, calculate debt-to-EBITDA as total debt divided by EBITDA. Do not force a universal cutoff. Even commonly cited ranges like 2.5 to 4 are context-dependent by industry and company goals.

In practice, the difference usually looks like this:

- Hope-based: accepts one EBITDA figure, uses standard terms by default, and watches only top-line results.

- Risk-managed: requests the income statement plus an EBITDA reconciliation, tightens milestones when cash evidence is weak, and tracks one consistent definition over time.

Step 3#

Apply the same discipline to your own business. Track operating profitability consistently and keep the supporting statements organized so your pricing, hiring, and planning decisions are grounded in operating reality, not guesswork.

Reuse this checklist on every client. For the next layer, use ratio analysis to combine profitability, cash, and debt in one view: A Guide to Financial Ratios for Business Health. For a step-by-step walkthrough, see What is a Merchant of Record (MoR) and How Does It Work?.

When you are ready to apply this risk-first approach in your day-to-day payment workflow, see how Gruv for freelancers is structured.

Frequently Asked Questions

How much should you trust an EBITDA margin?

Trust the consistency behind the margin more than the headline percentage. Do not use a universal “good margin” number here; any margin benchmark needs industry and company-type source-record verification before use. Next, request consecutive income statements and a clear reconciliation from net profit or operating profit (EBIT) to EBITDA.

How do you screen a startup client with limited history?

Start by testing whether the client defines core terms consistently, because mixed definitions can distort the numbers and reduce trust. If they cannot clearly separate bookings, revenue, and EBITDA, treat the metric as weak for payment-risk decisions. Request current management reporting, confirm their definitions in writing, and use tighter terms, such as shorter cycles or upfront partial payment, until reporting is consistent.

Can a company have positive EBITDA and still report a net loss?

Yes. EBITDA is calculated by adding interest, taxes, depreciation, and amortization back to net income or operating income, so EBITDA can be positive while net profit remains negative. Ask for the bridge from net profit to EBITDA. Then confirm whether they are using one of the two common calculation paths: net profit plus add-backs, or operating profit (EBIT) plus depreciation and amortization.

What trend should worry you most?

A major concern is deterioration under the same definition, not a single period that happens to look fine. If EBITDA or margin keeps weakening, or the formula changes between periods, your payment-risk visibility can get worse. Compare multiple periods using one consistent method, and move to staged billing, tighter milestones, or partial prepayment if trend quality declines.

Why is EBITDA criticized so often?

It is criticized because it excludes capital-related items, so it should not be used alone. That can make the operating picture look stronger than the company’s full financial strain. Pair EBITDA with cash evidence and keep contract protections active, including milestone billing and a clear stop-work clause.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- ecfr.gov/current/title-17/chapter-II/part-244trusted

- law.cornell.edu/uscode/text/26/162trusted

- people.stern.nyu.edu/adamodar/pdfiles/acf3E/book/ch5thru8.pdftrusted

- sec.gov/rules-regulations/staff-guidance/corporation...trusted

- sec.gov/rules-regulations/2003/03/conditions-use-non...trusted

- bain.com/insights/private-equity-buy-and-build-how-to...external

- bizbuysell.com/learning-center/article/sellers-discretionar...external

- british-business-bank.co.uk/business-guidance/guidance-articles/finance/...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Hiring a Subcontractor for the First Time Without Costly Surprises

**Start with a risk-control sequence, not an ad hoc handoff.** As the Contractor, your goal is simple: deliver cleanly, control scope, and release payment only when the work and file are complete.

How to Perform a Business Valuation for a Small Agency

---

Financial Metrics That Matter for a Business-of-One

Before you build a better financial command center, separate what ratio analysis can do from what it cannot. Ratio analysis can extract useful insight from financial statements, and in some study contexts, financial ratios have distinguished failed and non-failed companies several years before failure. But the method has clear limits. If you ignore benchmark fit, historical inputs, or inflation effects, the conclusion can point you in the wrong direction.