Quick Answer

Yes, many freelancers should evaluate cyber liability insurance when they handle client data, depend on cloud tools, process payments, or accept cyber-heavy contract terms. The article’s core advice is to decide with a workflow-based framework, not price alone: map exposure, validate first-party and third-party coverage boundaries, normalize quote terms, and confirm unclear language in writing before binding.

Build a Cyber Risk System Before You Buy a Policy#

Treat cyber coverage as part of your system, not a checkout decision.

| Step | What to capture |

|---|---|

| Map exposure first | Client data you touch, where you store it, and which tools your delivery depends on |

| Split loss paths | Direct business recovery costs and potential claims from clients or third parties |

| Check your current stack | Whether general liability and other standard policies leave cyber gaps |

| Define your incident record routine | Logs, timeline notes, and client updates |

| Use a strict buying rule | If language stays unclear, treat it as uncovered until you get written clarification |

When you handle delivery, payments, and data alone, a single data breach or ransomware event is not just a technical problem. It forces you to pause client work, run recovery, and manage client communication at the same time.

It is easy to turn cyber coverage into a pricing exercise. For a business-of-one, that is backwards. Your revenue depends on staying available, and you do not have room for long decision loops when something breaks. Small businesses attract cyber criminals, and solo operators often have limited security capacity. Practical risk management starts before you request quotes.

This guide gives you a framework and a purchase checklist. Use it to choose cyber liability and data breach coverage with fewer surprises than a fast quote flow.

Example: you click a convincing phishing message, lose access to a core account, and miss deliverables while you recover files and credentials. The immediate issue looks technical, but the business impact hits operations and cash flow first. That is why cybersecurity planning and policy design have to work together.

Set expectations early: cyber policy terms and claims handling vary by insurer, and legal duties vary by jurisdiction. In the United States, breach notification laws apply across all states and multiple territories, but definitions and notice mechanics still differ. If you run a technical practice, pair this with Liability Insurance for Freelance IT Consultants: Do You Need It?.

What Is Cyber Liability Insurance and What Is It Not?#

Cyber liability insurance covers cyber incident losses, while general and professional liability policies cover different risk lanes.

Once you have your exposure mapped, get the boundaries right before you shop. A quote only looks good if it protects the failure modes you actually face each week.

Cyber Liability Insurance addresses cyber events such as Phishing, Malware, ransomware, and unauthorized data exposure. Phishing tricks people into opening harmful links, files, or messages. Malware can give attackers unauthorized access to systems. That is why cyber liability sits in a different lane than general and professional liability.

Use a simple coverage map#

| Policy type | What it usually addresses | What it usually does not replace |

|---|---|---|

| Cyber Liability Insurance | Cyber event response, including first-party and third-party cyber tracks | Broad bodily injury or physical property claims |

| General Liability Insurance | Bodily injury, property damage, and personal or advertising injury exposures | Dedicated cyber response for a data breach or ransomware event |

| Professional Liability Insurance / Tech E&O | Claims tied to professional mistakes or omissions | A full cyber package unless the policy explicitly adds cyber components |

Keep your model simple and strict. Separate first-party response from third-party claims, and treat bundled language cautiously.

- First-Party Cyber Coverage handles your direct loss response after an incident. Depending on wording, it can include forensic investigations and other breach response costs.

- Third-Party Cyber Coverage handles claims from clients or other outside parties. It can include Legal Defense Costs and Settlements.

- Some products can include breach litigation and regulatory defense expense components, but terms vary by carrier and form.

A common solo-operator scenario looks like this. An account gets compromised through phishing, client data is exposed, and you have to restore operations while also managing external claims. That is why you want first-party and third-party clarity before you bind.

From here forward, keep one rule. If policy language blurs boundaries between cyber, general liability, and E&O, treat the gap as uncovered until you get written clarification.

Do You Actually Need Cyber Liability Insurance as a Freelancer?#

If you handle client data, depend on cloud tools, process payments, or accept cyber-heavy contract terms, you should evaluate cyber coverage.

With the boundaries clear, move from definitions to a decision. This is a triage exercise based on workflow exposure, not fear or headline pricing.

Run a four trigger triage before you shop#

| Trigger | Why it raises risk | What to verify now |

|---|---|---|

| Sensitive client data | Unauthorized access can create direct response work and client-facing liability after a data breach | What data you store, where it lives, and who can access it |

| Payment flow complexity | Accepting card payments can increase breach and operational exposure | Which payment tools you rely on and where failure blocks cash flow |

| Cloud tool dependence | Cyber events that impair systems can stop delivery and drive Business Interruption losses | Which tools are mission critical and how long you can operate without them |

| Contract risk transfer | Client agreements can push cyber responsibility to your business | Indemnity, notice, and insurance clauses that require specific cyber treatment |

You do not need a rigid scoring formula. If several triggers apply, treat your baseline exposure as meaningful and evaluate this coverage as core risk management. Size does not shield you from cyber incidents.

Match coverage priority to your actual work#

Your coverage priorities depend on what you touch.

If your work involves credentials, integrations, or client infrastructure, you should review Third-Party Cyber Coverage more closely. Client impact can lead to legal defense costs, settlements, and judgments. If your work is less tied to client systems, client-side liability exposure may be lower, but first-party disruption risk can still matter if a cyber incident blocks delivery.

Example: you lose access to a project platform during a live client sprint after a cyber incident. Work stops, invoices slip, and the client asks who covers downstream harm. In that moment, Cyber Extortion, Business Interruption, and third-party terms matter more than a cheap premium.

One safe rule: if a client contract shifts cyber liability to you, do not assume General Liability Insurance closes the gap. Confirm cyber terms in writing before you bind.

Which Coverage Components Matter Most for Solo Operators?#

Prioritize First-Party Cyber Coverage, Third-Party Cyber Coverage, and Business Interruption terms before you compare price.

You have already decided whether you have meaningful exposure. Now make sure the policy components match how incidents actually hit a one-person business.

A useful framing is simple: first-party is your costs to recover, and third-party is other people's claims against you. Keep that in mind when you read quotes. One incident can hit both lanes, so you need to pressure-test both before you buy.

Map incidents to coverage lanes#

| Incident pattern | Coverage lane to inspect first | Why it matters for a solo operator |

|---|---|---|

| Ransomware or data breach in your own systems | First-Party Cyber Coverage | This lane often handles direct response expenses tied to breach or hack containment |

| Client claims your work failed to prevent cyber harm | Third-Party Cyber Coverage | This lane addresses lawsuit-driven exposure, including Legal Defense Costs and possible Settlements |

| Malware or denial-of-service event pauses delivery | Business Interruption terms | This language can determine whether lost revenue and recovery expenses get support while systems stay impaired |

| Threat actor demands payment to stop harm | Cyber Extortion component | Some cyber products include this explicitly, so confirm wording instead of assuming it is standard |

Professional Liability Insurance and Tech E&O still matter, but they do not automatically replace dedicated cyber coverage. E&O focuses on negligence, errors, and omissions claims. Dedicated cyber coverage focuses on cyber events and related response and liability paths. Some carriers bundle them, but bundled does not mean identical.

If a term is unclear, treat it as uncovered until you get written clarification. That rule saves you from buying a policy you cannot actually use under pressure.

How Do You Compare Quotes Without Getting Tricked by Starting Prices?#

Normalize coverage terms across carriers before you compare premium, or the cheapest quote will often be the weakest risk transfer.

| Market mention | Article note | Stated takeaway |

|---|---|---|

| ERGO NEXT | Markets cyber liability insurance with low starting prices | Headline price does not equal comparable protection because prices change based on bundle context |

| GEICO | May route cyber through a partner | What matters is the form you are buying, not the logo on the quote |

| Liberty Mutual | Uses product structures such as Liberty Cyber Resolution and Liberty Tech Resolution | What matters is the form you are buying, not the logo on the quote |

Once you know what you need, the quote process becomes a documentation and wording exercise. Your goal is a claim path you can execute quickly, not a checkout flow that feels convenient.

Treat teaser pricing as a lead, not a decision. ERGO NEXT markets cyber liability insurance with low starting prices. Those prices can change based on bundle context, such as adding coverage to General Liability Insurance or Professional Liability Insurance. The takeaway is simple: headline price does not equal comparable protection.

Build one comparison worksheet and force every quote into it#

| Field to normalize | Why it changes claim outcomes | What to ask for in writing |

|---|---|---|

| Coverage structure | Carriers package cyber differently, including blended Tech E&O forms | Whether the quote uses standalone cyber liability insurance or a blended form |

| First-party and third-party scope | Coverage can split direct incident costs, business interruption, and third-party liability or regulatory costs | Exact limits for each major coverage component |

| Waiting periods and retentions | Time-based retention can reduce Business Interruption recovery | The waiting period trigger and how retention applies |

| Exclusions | Exclusions can remove common cyber loss paths | Plain language explanation of each exclusion |

| Claims reporting rules | Reporting mechanics control eligibility for support | Reporting window, channel, and required documentation |

Use market names like GEICO, Hiscox, and Liberty Mutual only as context. GEICO may route cyber through a partner, and Liberty uses product structures such as Liberty Cyber Resolution and Liberty Tech Resolution. What matters is the form you are buying, not the logo on the quote.

Your hard gate stays the same. If a term reads unclear, treat it as uncovered, ask for written clarification from the carrier or broker, and save that clarification with your worksheet so you can use it during claims handling.

What Should You Do in the First 72 Hours After a Suspected Incident?#

Execute containment, insurer notice, evidence logging, and client communication in parallel during the first 72 hours.

Buying coverage is only half the job. The other half is having a response routine that protects operations and preserves coverage options when time is tight.

When you detect suspected phishing or malware, activate your incident playbook immediately. Isolate affected systems, secure accounts, and fix exposed weaknesses to limit additional loss. Pull in legal and communications support early, not only technical help, because early decisions shape coverage options and client trust.

Use a time-boxed incident checklist#

| Window | Operational priority | Coverage and legal priority | Communication priority |

|---|---|---|---|

| Immediate | Isolate affected devices, revoke risky access, preserve system state | Open an incident file and pull your policy wording | Tell internal responders what is known and unknown |

| Early investigation | Preserve and centralize logs, record a timestamped timeline, retain key artifacts | Review notice requirements and coverage triggers, then notify the insurer through the required channel | Prepare plain language updates for affected clients |

| Active response | Continue containment and recovery while tracking every action | Coordinate with insurer-approved legal, forensic, and recovery vendors when required | Share factual status updates without speculation |

| Stabilization | Validate restored systems and monitor for repeat compromise | Organize records that may support coverage review and claim handling | Communicate next steps and support channels clearly |

Example: you see suspicious mailbox rules, then files become inaccessible across a client project workspace. Log actions as you go. Notify the carrier promptly so you can access response resources and preserve coverage options. Send factual client updates. That combination protects both recovery speed and your claim position.

Keep one compliance note in view: some jurisdictions set strict reporting clocks. Under UK GDPR, you must report a notifiable personal data breach without undue delay and no later than 72 hours after awareness, but you must verify rules for your own jurisdiction and program. This is not paperwork. It is how coverage and response planning deliver value under pressure.

Where Cross Border Rules and Program Requirements Change Your Safe Default#

Treat every cyber incident as jurisdiction specific and program specific, then verify obligations in writing before you act.

| Area | Rule change | Article detail |

|---|---|---|

| EU cross-border processing | Regulator target | One incident can affect people in multiple member states, and you notify the lead supervisory authority |

| U.S. | Breach-notification laws | All 50 states plus DC, Guam, Puerto Rico, and the Virgin Islands have breach-notification laws |

| UK practice | Breach reporting timing | You report qualifying personal-data breaches without undue delay, and if you notify after 72 hours under GDPR, you provide reasons for delay |

| PIPEDA / Canada regulations | Breach records | You keep breach records, provide them when the Commissioner requests them, and retain those records for 24 months |

If you work across borders, you cannot run incident response on autopilot. The same event can trigger different notice duties, client program requirements, and policy conditions depending on where the affected people, systems, and clients sit.

Compliance and claims obligations can change across markets. In EU cross-border processing, one incident can affect people in multiple member states, and you notify the lead supervisory authority. In the U.S., all 50 states plus DC, Guam, Puerto Rico, and the Virgin Islands have breach-notification laws. In UK practice, you report qualifying personal-data breaches without undue delay, and if you notify after 72 hours under GDPR, you provide reasons for delay. Under PIPEDA, you keep breach records, provide them when the Commissioner requests them, and Canada regulations require you to retain those records for 24 months.

| Area | What changes | Safe default |

|---|---|---|

| Notification | Deadlines, regulator target, and trigger definitions differ by jurisdiction and program | Build a per-country notice map and assign one owner before incidents happen |

| Documentation | Authorities and insurers may ask for different evidence depth | Keep a living incident log with facts, effects, and remedial actions from day one |

| Investigation | Policy requirements and legal workflows can vary by policy and jurisdiction | Confirm approved vendors and reporting channels in your policy forms before you engage |

Tie your cyber coverage to the controls you already run in your stack. Keep traceable access logs, ticket history, change approvals, and client communication records so your cybersecurity posture can support cyber insurance decisions and claims handling.

For payments-heavy workflows, keep structured transaction histories and exports to support chronology and reconciliation. Do not treat exports alone as sufficient legal proof everywhere. Example: a solo operator handling cross-border subscriptions matches payment events to incident timestamps, then shares a clean timeline with counsel and the carrier to reduce dispute risk.

Use a written verification script every time#

- Pull insurer policy forms first, then confirm cyber obligations in writing.

- Get licensed legal advice for each affected jurisdiction, and work with a licensed insurance producer for policy interpretation and placement.

- Use broad explainers from Paychex as orientation only, not as final authority.

- Use conservative wording in client and internal notes: coverage varies by market and program.

- When your service mix overlaps consulting and implementation risk, cross-check your stack with Liability Insurance for Freelance IT Consultants: Do You Need It?.

The Purchase Checklist You Can Use This Week#

Use a written, side-by-side checklist to buy the policy you can defend at claim time, not the policy with the lowest headline premium.

You now have the workflow map, the quote worksheet, and a response routine. This checklist turns that into a binding decision that aligns coverage, controls, and reporting mechanics before anything goes wrong.

Run this purchase checklist before binding#

| Checklist item | What to verify in writing | Why it matters |

|---|---|---|

| Baseline stack | Current General Liability Insurance, Professional Liability Insurance (or Tech E&O), and any cyber endorsement on your COI and policy forms | General liability focuses on third-party bodily injury and property damage, so you need clear separation from service-error and cyber exposure |

| Core cyber scope | Explicit treatment of Data Breach, Business Interruption, third-party litigation exposure, and response costs such as forensics, legal, regulatory, crisis, and extortion events | This coverage only works when the covered incident types match your real operating risk |

| Claims mechanics | Exact reporting channel, timing, and required first notice details for known or suspected incidents | Some carriers instruct immediate filing after a known or suspected cyber event, so process clarity protects eligibility |

| Exclusions and sublimits | Every exclusion, waiting period, and sublimit that could narrow recovery | Policies differ, and vague language creates disputes when you need fast payment and legal support |

| Limit selection | Contract-driven limits and any client insurance requirements | Your contracts should drive limits, not quote-page defaults |

Treat marketing pages and marketplace summaries as orientation, not authority. Policy forms govern coverage terms and conditions. Keep conservative language in your notes, including this phrase when uncertainty remains: coverage varies by market and program.

If you are choosing between two quotes, do not let lower price override operability. A quote with vague reporting steps and narrow business interruption terms can cost you more when you need it. The defensible pick is the one with clear written triggers, reporting steps, and coverage boundaries.

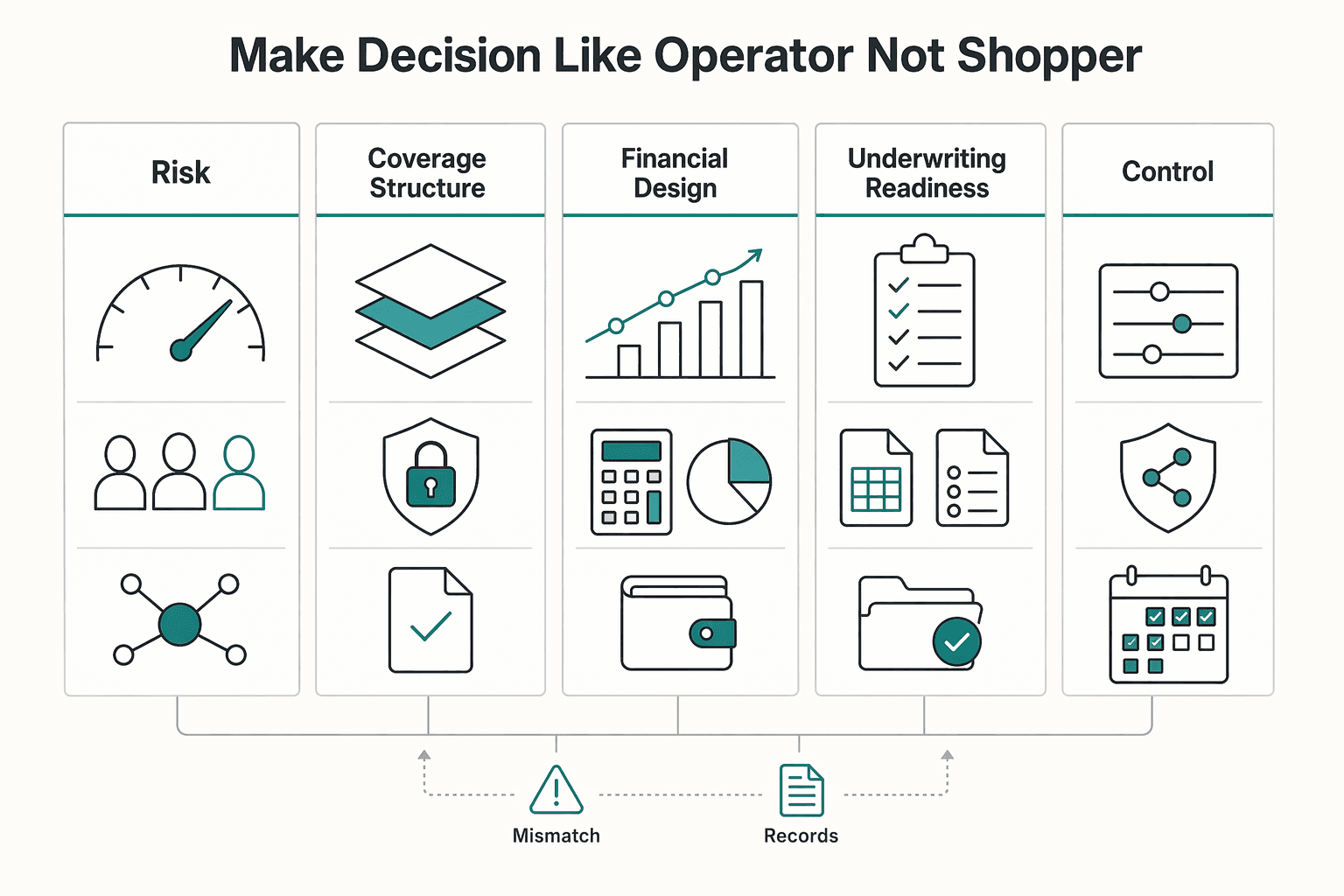

Make the Decision Like an Operator Not a Shopper#

Pick the policy that matches your real workflow risk and gives you the clearest claim path, even when a cheaper quote looks tempting.

At this point, you have what you need to decide like an operator. Use the framework and checklist as a control in your risk system, not as a shortcut to just "get something in place."

The sequence matters. Fit the coverage mechanics to your work model first. Then compare limits, deductibles, and price. Then lock your documentation so you can execute under pressure. First-party and third-party coverage handle different failure modes, so confirm both against your real exposure before you bind.

| Decision lens | What to verify now | Operator standard |

|---|---|---|

| Workflow risk fit | Client data sensitivity, admin access, payment and delivery dependencies | Match coverage to your actual cybersecurity and service workflow, not a generic profile |

| Coverage structure | First-party events, third-party events, exclusions | Treat unclear language as a gap until you get written clarification |

| Financial design | Premium, deductible, and limit options (for example, lower limits versus higher limits) | Choose the level you can defend at claim time, not the lowest monthly cost |

| Underwriting readiness | Backup strategy, access controls, firewall hygiene, incident response plan | Keep reusable evidence ready because carrier and industry criteria vary |

| Policy wording control | Core terms and exclusions | Do not assume blanket coverage for every expense |

Close the decision loop before binding#

- Gather your current insurance and cyber policy forms.

- Run the checklist across final quotes and log your choice criteria in plain language.

- Request written clarification on every vague term, especially exclusions and unclear conditions.

- Save the decision record, then revalidate coverage whenever your client mix, tooling, or data handling model changes.

That is operator-grade risk management for cyber coverage: clear fit, clear wording, and a claim path you can use under pressure. Want to confirm what is supported for your specific country or program with Gruv? Talk to Gruv.

Frequently Asked Questions

What is cyber liability insurance for freelancers?

Cyber liability insurance for freelancers helps cover financial losses after cyber incidents like data breaches and cyberattacks. It often combines first-party coverage for your direct response costs and third-party coverage for claims from clients or other affected parties. In practice, it supports breach response and legal defense for a one-person business.

Do freelancers need cyber liability insurance if they already have general liability coverage?

Usually, yes. General Liability Insurance often does not include core data breach costs unless you add specific cyber coverage. If you handle client data, treat cyber liability insurance as a separate decision with its own terms and claims mechanics.

What does cyber liability insurance typically cover for a solo business?

Many policies include breach response costs such as customer notification, legal fees, and certain fines, along with cybersecurity incident response costs. Third-Party Cyber Coverage can also help with legal fees, settlements, and judgments if a client sues after an incident. Coverage varies by policy, so verify the exact terms in the policy form.

What does cyber liability insurance usually not cover?

Policies can exclude specific events, so read exclusions and sub-limits line by line. Some policy language excludes data loss caused by a power outage. Do not assume every policy handles ransomware, business interruption, or cyber extortion the same way.

How much can cyber liability insurance cost for freelancers and what changes the price?

Price depends on your risk profile, especially how much sensitive information you handle and which limits you select. One small-business benchmark reports an average premium of $134 per month ($1,609 annually), with annual premiums ranging from $400 to over $8,000. Use these numbers as context, not as a guaranteed quote.

What coverage limits should a freelancer prioritize first?

Start with limits that match contract requirements, client expectations, and realistic incident costs. Many cyber policies show limits in a $1 million to $5 million range, and deductible size changes your out-of-pocket exposure. Compare limits, sub-limits, and deductibles together before you bind coverage.

What documents should I gather before requesting cyber insurance quotes?

Collect a short summary of your data handling workflow and operational controls before you apply. Underwriters may ask whether you run a backup strategy, how often you back up, and where you store backups. If your work blends consulting and implementation, use Liability Insurance for Freelance IT Consultants: Do You Need It? to tighten your quote packet.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cisa.gov/news-events/cybersecurity-advisories/aa25-266atrusted

- edpb.europa.eu/system/files/2023-04/edpb_guidelines_202209_...trusted

- ftc.gov/business-guidance/small-businesses/cybersecu...trusted

- ftc.gov/business-guidance/resources/data-breach-resp...trusted

- sba.gov/business-guide/manage-your-business/strength...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Canada Digital Nomad Visa Planning for Visitor Status and Work Permits

The phrase `canada digital nomad visa` is useful for search, but misleading if you treat it like a legal category. It is shorthand for existing Canadian status options, mainly visitor status and work permit rules, not a standalone visa stream with its own fixed process. That difference is not just technical. It changes how you should plan the trip, describe your purpose at entry, and organize your records before you leave.

Liability Insurance for Freelance IT Consultants: Do You Need It?

**Treat your insurance decision like risk management, not online shopping.** As an independent IT consultant, you can face a negligence allegation, a client financial-loss claim, and legal defense costs even when you delivered in good faith. One bad dispute can drain time, focus, and cash before anyone proves fault. If you run solo, you are the CEO of a business-of-one, and risk decisions are part of the job.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.