Quick Answer

A settlor creates the trust and sets its terms, while the trustee holds legal title to trust property and administers it for the beneficiaries under those terms. The main difference is design versus execution: the settlor decides what authority exists, and the trustee decides how to carry it out in good faith. In some trusts, one person can serve in both roles, but successor planning still matters.

A trust works best when you treat it as an operating structure, not just a stack of legal documents. The first decision is role design: who writes the rules, who carries them out, who benefits, and who steps in if the first trustee cannot serve? Once you frame it that way, the settlor-trustee split becomes much easier to evaluate.

Meet Your Personal Board of Directors#

At the core is role clarity. You set the trust terms. The trustee holds legal title and manages trust property under those terms. The beneficiary receives the beneficial enjoyment. A successor trustee keeps administration moving if the original trustee dies, becomes incapacitated, or otherwise cannot serve.

The settlor, grantor, and trustor refer to the same role: the person who creates the trust relationship and sets its terms. The trustee is the person, or people, who holds legal title to trust property and administers it under the trust terms. The beneficiary holds the beneficial interest in that property. The successor trustee is the replacement person or institution who takes over if the current trustee dies, becomes incapacitated, or cannot serve.

| Role | Who this can be | Primary authority | Primary duty | Main risk if chosen poorly |

|---|---|---|---|---|

| Settlor / Grantor / Trustor | The person creating the trust | Sets trust terms and structure | Give clear, lawful instructions | Ambiguous terms that create later administration problems |

| Trustee | You or another person, including co-trustees | Holds legal title and manages trust assets, subject to trust terms and applicable law | Administer the trust for beneficiaries | Conflicts, poor administration, or inadequate records |

| Beneficiary | Person(s) named in the trust | Beneficial enjoyment of trust property | Receive benefits under trust terms | Misalignment between your intent and trust language |

| Successor trustee | Person or institution | Steps in when the current trustee cannot serve | Maintain continuity of trust administration | Delay, refusal to serve, or inability to prove authority |

In some trusts, one person can hold more than one role. For example, one person may be settlor, trustee, and beneficiary. Even then, the split between trustee control and beneficiary enjoyment still matters, especially when a successor needs to prove authority to a bank or another third party.

Fiduciary duty is the real operating standard, not just a label. Core fiduciary duties include care, loyalty, and good faith. In practice, a trustee should follow lawful trust instructions, act for the beneficiaries' benefit, avoid personal use of trust property or trustee powers unless authorized, and keep adequate records.

When naming a successor trustee, confirm these four points now:

- Fit: they have the competence and time for the role.

- Willingness: they have agreed to serve, since a designated trustee can reject the trusteeship.

- Access: they can access the trust and proof-of-authority documents needed to act.

- Continuity: they understand the handoff if the current trustee dies or becomes incapacitated.

For a step-by-step walkthrough, see How to Choose a Trustee for Your Trust.

The Core Dilemma: Maximizing for Control or for Protection?#

The next decision is how much authority you want to keep. If you want to amend terms, revoke the trust, and direct decisions closely, you are usually looking at revocable trust territory. If you want stronger separation between yourself and the assets, you are usually evaluating irrevocable structures with more independent trustee administration.

Revocability is not a nationwide default. In some UTC-style statutes, revocability is the default unless the trust says it is irrevocable, as in Florida Statutes 736.0602. Other statutes require express revocability language, as in 760 ILCS 3/602 in Illinois. So your first check is always the signed trust instrument and the governing law, not the label on the cover.

A revocable trust usually gives you high control and high flexibility, but weaker protection. Under 760 ILCS 3/603, while a trust is revocable, beneficiary rights are subject to settlor control and trustee duties are owed exclusively to the settlor. Under 760 ILCS 3/505, revocable trust property is subject to settlor-creditor claims during life.

An irrevocable trust shifts that balance. You usually get less flexibility to change terms and less day-to-day control, which can improve creditor-shielding posture, but not automatically. Florida Statutes 736.0505 states that a settlor's creditor may still reach the maximum amount distributable for the settlor's benefit. If you retain benefit or distribution access, the shield can weaken materially.

| Selection factor | Revocable trust | Irrevocable trust |

|---|---|---|

| Control rights | Usually high if terms and law allow amendment or revocation | Usually reduced once funded |

| Creditor-shielding posture | Generally weak during settlor's life | Often stronger, but can be limited if settlor-benefit distributions remain possible |

| Trustee independence | Often limited where settlor direction controls outcomes | Usually more important when protection is the goal |

| Change flexibility | High, if trust terms and governing law permit | Low to moderate, depending on terms and jurisdiction |

| Administration burden | Varies by terms and tax posture | Varies by terms and tax posture; fiduciary administration may include Form 1041 filing obligations |

Tax treatment also follows retained control more than the trust label. IRS guidance on grantor-trust treatment focuses on retained economic interest and control, and fiduciary administration may include Form 1041 filing. Calendar-year estates and trusts generally file by April 15 of the following year.

Use this quick fit check to pressure-test your direction. If you are thinking about broader planning, see A Guide to Estate Planning for Digital Nomads.

- If your risk profile is ordinary and flexibility is the priority, revocable is often the cleaner fit.

- If asset separation is the priority and you can accept real delegation, evaluate irrevocable options under your governing jurisdiction.

- If you want flexibility now and tighter lock-in later, focus on which powers and benefits you retain, because retained control can preserve creditor and tax reach.

- If you are considering self-settled or domestic asset-protection structures, treat this as jurisdiction-sensitive: availability and creditor or tax reach vary by state and court treatment.

The Trustee Selection Matrix: A Framework for Your Most Critical Appointment#

Once you decide how much control to keep, trustee selection becomes the main execution risk. The right choice is the person or institution that can administer your actual assets, stay loyal to the beneficiaries, keep trust property and records clean, and keep the trust functioning over time. The exact fiduciary rules and procedures are state-law specific, but these selection checks are broadly useful.

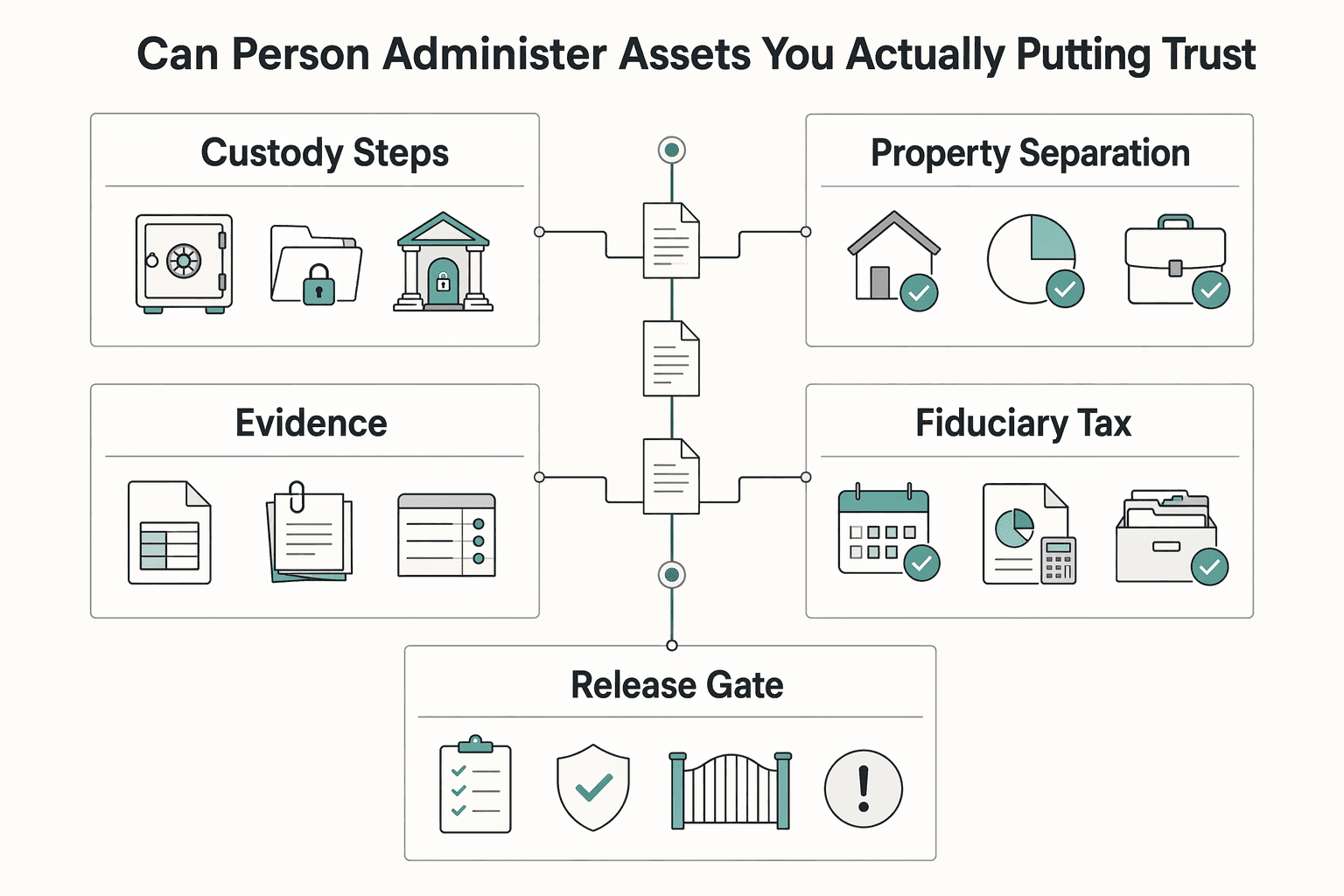

Can this person administer the assets you are actually putting in the trust?#

Start with your asset mix, not family dynamics. Ask the candidate to walk through how they would handle your specific assets, records, valuations, tax coordination, and distributions. This matters even more if the trust will hold business interests, real estate, digital assets, or cross-border accounts.

| Plan component | What to confirm |

|---|---|

| Custody steps | A concrete administration plan covers custody steps for your specific assets |

| Property separation | The plan covers separation of trust property from personal property |

| Recordkeeping setup | The plan covers recordkeeping setup |

| Fiduciary tax workflow | The plan covers fiduciary tax workflow, including Form 1041 when required |

| Delegated work supervision | If key tasks are outsourced, confirm how delegated work will be supervised |

If you chose this trustee for claimed expertise, that expertise should show up early in administration. A useful test is a concrete administration plan. It should cover custody steps, separation of trust property from personal property, recordkeeping setup, and fiduciary tax workflow, including Form 1041 when required. If the plan is to outsource key tasks, confirm how delegated work will be supervised instead of treating delegation as a full handoff.

Can this person stay loyal to the beneficiaries and out of self-interest?#

This is the baseline test. The trustee acts for beneficiaries, not for personal convenience. If personal and fiduciary interests collide, the transaction can be challenged by affected beneficiaries.

In practice, that means no treating trust funds like shared family money, no role blurring because someone is also family, and no using personal accounts for trust transactions. You should expect disciplined recordkeeping and clear separation between trust property and the trustee's own property.

Can the trust keep operating if this trustee gets sick, quits, or stalls out?#

Continuity planning is not optional. A capable solo trustee can still create fragility if the trust is long term or operationally active.

A co-trustee structure can help keep decisions moving and reduce single-person failure risk. Remaining co-trustees may keep acting if one seat becomes vacant. But co-trusteeship only helps when cooperation is realistic. Unresolved conflict can materially impair administration and become its own removal risk. Under many state trust statutes, if no trustee remains, the vacancy must be filled.

Will this trustee follow the document, keep records, and answer for decisions?#

You want document-first administration, not improvisation. Once trusteeship is accepted, the trustee is expected to administer in good faith according to the trust's terms and purposes.

| Checkpoint | What to confirm |

|---|---|

| Role acceptance | Get explicit role acceptance before any asset transfer; acceptance can also be inferred from conduct such as taking trust property or exercising trustee powers |

| Asset-mix ability | Confirm the ability to administer your real asset mix, not just generic investments |

| Backup coverage | Confirm successor naming, co-trustee mechanics, and resignation handling, including any required notice period such as 30 days where applicable |

| Fee terms | Set fee terms clearly, or define how reasonableness will be assessed if compensation is not set in the trust |

| Communication cadence | Confirm communication cadence for reporting, beneficiary questions, and tax-season deliverables |

Get explicit role acceptance before any transfer. Acceptance can also be inferred from conduct, such as taking trust property or exercising trustee powers. Set accountability terms early: reporting cadence, response expectations for beneficiary information requests, and fee clarity. If compensation is not set in the trust, reasonableness becomes the default standard, so it helps to define the framework in advance.

| Trustee type | Operational capacity | Conflict risk | Continuity | Documentation and accountability | Best fit when | Warning signs |

|---|---|---|---|---|---|---|

| Family member or friend | Strong when assets and admin demands are simple and the person has real time capacity | Higher when personal relationships or beneficiary overlap are active | More exposed to illness, burnout, resignation, or death | Can be uneven without strong discipline | Your trust is straightforward and this person is organized, available, and trusted by all key parties | Informal money habits, weak records, reluctance to share information, unclear boundaries |

| Corporate or institutional trustee | Can be stronger for complex assets, long duration, and formal administration | Can reduce some personal conflict risk, depending on structure and incentives | Often offers structural continuity beyond any one individual | Often uses formal process, reporting, and controls | You need durability, impartiality, and consistent administration standards | Unclear fee model, weak diligence responsiveness, limited fit with your asset profile |

| Co-trustee or family-plus-professional support | Can combine personal context with technical administration | Can improve balance, but only if authority lines are clear | Better resilience if one decision-maker is unavailable | Often strongest when reporting ownership is explicit | You want family judgment plus professional rigor | Overlapping authority, unresolved disagreements, no clear owner for records or deadlines |

Use the lightest structure that can still meet fiduciary duties without strain. If your assets or administration demands are complex, a corporate trustee or a family-plus-professional model may be safer than relying on a solo relative.

Your Contingency Plan: The Critical Role of the Successor Trustee#

A trust handoff can fail even if the primary trustee choice was sound. Name and prepare your successor trustee now, because once authority shifts, that person may need to handle records, trust tax filing, and beneficiary accounting.

One rule matters above all: before a triggering event, the successor has no authority to act. So the plan has to do more than name a backup. It has to make the transition clear enough that institutions, advisors, beneficiaries, and the successor all know when authority begins and what happens next.

Define the trigger with operational detail#

The triggering event is what turns successor authority on. Your trust should define qualifying events and the required process, because transition rules vary by jurisdiction and by trust terms.

| Triggering event | When successor authority begins | What you should define now | Main failure point |

|---|---|---|---|

| Death of the original trustee | After death, the successor assumes management under trust terms | Who is notified first, where core documents are stored, and which institutions or advisors are contacted first | No document access and no contact path to key institutions |

| Incapacity | Only after the trust's incapacity trigger is met | How incapacity is addressed and how transfer of authority is documented under the trust and governing law | Vague incapacity language that causes delay or dispute |

| Unwillingness or inability to continue (if the trust allows it) | After the trust's stated process is completed | How refusal, resignation, or unavailability is confirmed, and who controls handoff records | Successor is unreachable or never accepted the role |

Apply the same selection test you used for the primary trustee#

Do not treat this as a courtesy appointment. Use the same criteria you used for the primary trustee: time capacity, organizational skill, expertise, judgment, and willingness to serve.

A practical test helps here too. Can this person or institution realistically handle the time, organization, expertise, and judgment the role may require? If administration could involve family conflict, tax complexity, or personal liability, confirm fit directly. Confirm it in writing, and make sure they can be reached quickly in an emergency.

Build a short activation checklist#

A named successor who cannot activate quickly is not ready. Keep this package current:

| Checklist item | What to keep current |

|---|---|

| Trust document package | Location of the trust document, amendments, and related instructions |

| Professional contacts | Current contacts for your lawyer, accountant, financial advisor, and other key professionals |

| Account and asset inventory | Current account and asset inventory, including where records are maintained |

| Communication protocol | Communication protocol for beneficiaries and advisors after the trigger |

| Acceptance confirmation | Written confirmation that the successor accepts the role and remains reachable |

Readiness is not early control. Before a trigger, the successor should know where instructions live and who to contact, not act on trust property.

Risk-prevention callout: Failure points include unclear trigger language, an unprepared successor, and missing access instructions. You can prevent a lot of that by drafting trigger terms clearly, confirming acceptance in writing, and keeping documents and contact details current.

You might also find this useful: A Guide to Setting Up a Trust for Asset Protection.

Conclusion: From Legal Document to Lasting Enterprise#

The basic split is straightforward under state-law trust frameworks. Your job as settlor is to design the trust terms. The trustee's job is to carry them out under fiduciary duty. You create the trust relationship and set the instructions; the trustee holds legal title and administers the assets for the beneficiaries.

That boundary lives in the trust instrument. It determines what authority you keep, what authority you delegate, and where the limits sit. It is also the standard the trustee must follow in good faith, based on the trust's terms, purposes, and beneficiary interests.

| Point of comparison | You as settlor / grantor | Trustee |

|---|---|---|

| Core function | Create the trust and set its terms | Hold legal title and administer trust assets |

| Main source of control | Trust terms and valid amendments | Powers granted by trust terms and governing law |

| Duty standard | Define purpose, beneficiaries, and distribution provisions | Act as a fiduciary for beneficiaries |

| Practical boundary | You decide what authority exists | Trustee decides how to execute within that authority |

A strong setup is specific. Your trust terms should clearly state governing law, trustee rights, duties and powers, distribution provisions, successor trustee designations, and who the beneficiaries are, including present or future interests. That clarity can help reduce inconsistent administration and handoff problems if the current trustee cannot serve.

Before signing, run this checklist and confirm:

- Review the trust terms for clear powers, distribution rules, beneficiary definitions, and governing-law language.

- Confirm the trustee's rights, duties, and powers are explicit in the trust instrument.

- Confirm successor coverage and activation details so authority can transfer cleanly.

- Get jurisdiction-specific legal review, since trust governance is state-law based.

We covered this in detail in How to Use a Trust to Avoid Probate.

Frequently Asked Questions

What is the difference between a settlor, grantor, and trustor?

Settlor, grantor, and trustor usually refer to the same person: the person who creates the trust and sets its terms. The key issue is not the label but whether the document clearly identifies that person and states how the trust operates. Check the party definitions, operating terms, and governing-law clause.

Who has more power, the settlor or the trustee?

Usually, the settlor controls the trust design in the document, while the trustee controls day-to-day administration within those terms. In practice, the settlor decides what authority exists, and the trustee decides how to execute within that authority. Check trustee powers, any stated settlor rights, and the governing-law clause.

Can you be both the settlor and the trustee?

Often yes, including in many revocable trusts while you are alive. One person can sometimes hold more than one role in the same trust. If you use that structure, make sure the successor trustee and the handoff trigger, such as incapacity or death, are clearly stated.

Can you remove or replace the trustee?

Sometimes, but not automatically in every trust or jurisdiction. Treat removal flexibility as a drafting issue, not an assumption. Check what the trust says about removal and replacement, and whether court process may apply under governing law.

Can a trustee also be a beneficiary?

Sometimes one person can hold more than one role in a trust, including trustee and beneficiary. But there is no universal rule stated here, so treat trustee-beneficiary overlap as drafting-dependent and jurisdiction-dependent. Verify it directly in the trust terms and governing law.

What happens if the trustee does not follow the trust terms?

That becomes an enforcement issue under the trust terms and applicable law. A trustee is expected to administer the trust in good faith according to its terms and purposes, and affected beneficiaries can challenge conflicted transactions. Strong drafting on duties, powers, remedies, and any removal or replacement mechanism can reduce later disputes.

Does governing law really matter if you or your assets are in more than one place?

Yes. Trust governance is jurisdiction-dependent and trust law is state-based, with possible federal overlay for some institutional fiduciaries. If your setup crosses state lines, the governing-law clause matters even more before signing. Also check whether a bank or savings association trustee may be operating under additional fiduciary rules.

If court oversight comes up, will it always be required?

No. Whether court process is needed depends on the trust terms and governing law. Check whether the trust states a trustee-removal path and successor appointment process.

What if you signed the trust but did not transfer assets into it?

That is a real failure point. If funding is not completed, the trust may not operate as intended. Funding is part of setup, not a cleanup task after signing, so confirm that transfer records are in place for the relevant assets.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- codes.ohio.gov/ohio-revised-code/section-5808.10trusted

- flhouse.gov/Statutes/2025/0736.0602trusted

- flhouse.gov/Statutes/2025/0736.0505trusted

- ilga.gov/documents/legislation/ilcs/documents/0760000...trusted

- ilga.gov/documents/legislation/ilcs/documents/0760000...trusted

- irs.gov/businesses/small-businesses-self-employed/ab...trusted

- irs.gov/individuals/file-an-estate-tax-income-tax-re...trusted

- law.cornell.edu/wex/successor_trusteetrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Germany Freelance Visa Application Path for Freiberufler and Gewerbe

Choose your track before you collect documents. That first decision determines what your file needs to prove and which label should appear everywhere: `Freiberufler` for liberal-profession services, or `Selbständiger/Gewerbetreibender` for business and trade activity.

Estate Planning for Digital Nomads: Legal Intent and Cashflow Continuity

Treat estate planning for digital nomads as a two-part continuity system: legal intent plus operational execution, so your business keeps moving when you cannot. The common trap is thinking, "I have a will, so I'm covered." If you run a business-of-one, cashflow, logins, and process often live in your head until you deliberately externalize them.

When a Trust for Asset Protection Makes Sense for Your Business

Use a trust only after your core liability setup is solid. A trust for asset protection is an escalation layer, not a substitute for entity separation, insurance, or clean operations.