Quick Answer

Build your financial identity for nomads as a portable evidence system: a proof packet, a live compliance file, and a resilience setup for cashflow shocks. Keep statements, signed contracts, invoices, and required filings aligned so reviewers can validate income quickly. Track residency and foreign-account reporting checkpoints before filing season, then separate collection, operating, tax, and buffer funds so one interruption does not stall your business.

The Architect of Your Financial Identity: A Blueprint for Global Professionals#

Your financial identity should function as portable proof. It can help you get paid across borders, clear reviews faster, and control risk when your life does not fit the one-address, one-employer, one-country model many institutions still assume.

financial identity for nomads means organized, portable evidence of your income, legitimacy, and financial controls. It can protect cashflow by reducing avoidable payment friction, strengthen credibility by showing where money comes from, and lower operational risk because your records are ready when you are reviewed.

That matters because banks are required in many jurisdictions to verify customer identity through CIP-style procedures and customer due diligence. Self-employed underwriting also often turns on whether income appears stable and likely to continue. In U.S. mortgage underwriting guidance, for example, self-employed borrowers are generally assessed with a two-year prior earnings history.

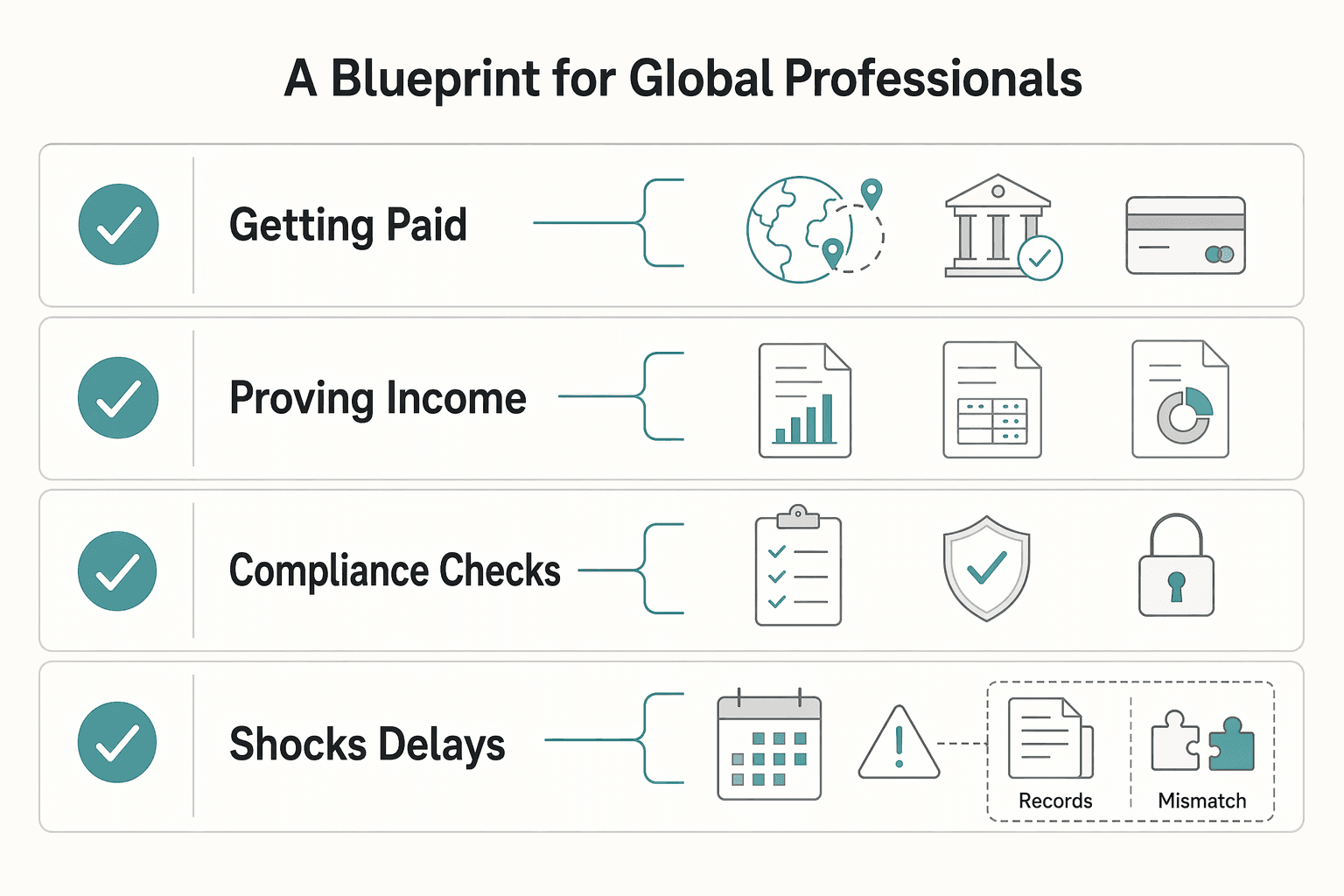

| Area | Reactive money admin | Designed financial identity |

|---|---|---|

| Getting paid | Funds land wherever is convenient | Payment routes are deliberate and easy to explain |

| Proving income | You search across invoices and screenshots | Statements, contracts, and tax records are ready |

| Compliance checks | Requests arrive as urgent disruptions | You respond with current documents and tracked thresholds |

| Shocks and delays | One late payment creates immediate stress | Buffers and account structure absorb volatility |

This friction is structural, not personal. Global standard-setters still describe cross-border payments as too slow, costly, and opaque, and BIS reporting says end-user improvements have been modest so far. World Bank data also reports a 6.49% global average remittance cost, a reminder that moving money across borders is still expensive in many cases.

In practice, many breakdowns are operational. People have scattered accounts, weak records, and no evidence pack ready when a review starts. When you cannot quickly produce clean statements, signed contracts, and filed returns, routine checks turn into avoidable delays. If you are a U.S. person, even baseline reporting thresholds matter. FBAR filing is triggered when aggregate foreign account value exceeds $10,000 at any point in the calendar year.

The rest of this article breaks the work into three pillars: prove income, stay compliant, and absorb volatility. Build those on purpose, and your finances stop looking improvised and start looking verifiable. Related: The Ultimate Guide to Getting a Mortgage as a Freelancer.

Pillar 1: The Legitimacy Engine - Prove You're a Professional, Not a Tourist#

Do not wait for a reviewer to ask for proof. Build a Financial Legitimacy Package now so a reviewer can quickly verify that you are a working professional with stable income, not someone with scattered paperwork. Assume your packet may be evaluated from documents alone, so make it one consistent story that is easy to validate.

Build your packet in purpose-action-proof format#

Start with the documents that establish continuity. You want a reviewer to move cleanly from income source to work performed to money received.

| Document | Proof | Presentation | Risk |

|---|---|---|---|

| Account statements | Recurring income lands in an account you control | Include at least six, preferably twelve, months from your primary business account, plus a short summary or annotations that highlight recurring client payments | Income looks irregular, unverifiable, or one-off |

| Signed contracts | Your income comes from real client relationships with forward visibility | Include active signed agreements with names, dates, scope, and payment terms visible | Reliance on past-work evidence only |

| Invoicing trail | Continuity between work performed and money received | Keep invoices in sequence and make each one traceable to a statement entry | Revenue claims that do not close the loop from client to invoice to payment |

| Official filings (if required) | Reviewer-required declarations are included in the same evidence set | Include any required official filings and align them with your statements and invoices | A packet that looks complete but misses required official documents |

If you are prioritizing, start with the chain the reviewer will care about most: statements show recurring inflows, contracts show forward visibility, invoices connect the work to the payment, and official filings cover any required declarations.

Weak evidence vs strong evidence#

Strong packets are easy to scan and hard to misread. The difference usually is not the amount of paper. It is whether the paper tells one verifiable story.

| Evidence area | Weak evidence | Strong evidence |

|---|---|---|

| Income history | Isolated screenshots or a single statement | At least six, preferably twelve, months from your primary business account, with recurring payments flagged |

| Client relationship | One invoice without context | Signed contract plus related invoices and matched payments |

| Payment proof | Transfers that are hard to interpret | Statement entries that clearly map to invoice details |

| Record quality | Unordered files with inconsistent labels | Ordered files with a clear summary and consistent naming |

| Official validation | Self-prepared summary only | Required official filings aligned with the rest of the packet |

Verify requirements first, then package#

This is where people lose time. Do not assume one institution's document rules apply everywhere. Confirm the current requirements for the exact jurisdiction and institution first, then package to that standard.

Treat the current document lookback window as unresolved until the institution, jurisdiction, or official source record confirms it. If submitting to a U.S. government portal, confirm it is an official .gov site and uses HTTPS. In all cases, share sensitive information only on official, secure websites.

Package for fast review#

A clear packet can reduce back-and-forth. Use one naming pattern across the file set, redact only nonessential sensitive fields, and keep all verification fields visible. Then run one final consistency check before you submit.

Before you submit, run this checklist:

- Can each major income stream be traced from contract to invoice to statement entry?

- Is the required document lookback window verified from official or source records before you match statements to it?

- Are names, dates, and amounts consistent across documents?

- Did you keep verification fields visible while removing only nonessential sensitive data?

- Are you submitting through the institution's official, secure portal?

You might also find this useful: IP Protection for Software Developers: A Deep Dive into Copyright.

Pillar 2: The Compliance Shield - Operate Globally with Zero Anxiety#

Treat compliance as risk control, not admin. If Pillar 1 makes your income legible, this pillar keeps that story defensible across countries, accounts, and contracts.

You need a live file for each country where you spend time, hold accounts, or perform client work. Review it before thresholds or contract terms turn into problems.

Track residency as a live exposure#

Residency is where casual assumptions create expensive mistakes. Do not treat it as a simple day-count rule. Verify the current residency test criteria from the primary rules for that jurisdiction before you rely on the country file.

| Area | Rule | Note |

|---|---|---|

| U.S. Substantial Presence Test | 31 days in the current year and 183 days over a 3-year period | Prior years are weighted at 1/3 and 1/6 |

| U.K. Statutory Residence Test | 183-day trigger | HMRC also evaluates family, accommodation, work, and 90-day ties |

| Treaty tie-breakers | Habitual abode, then nationality if needed | Verify the treaty text before taking a position |

Headline day counts rarely tell the whole story. The U.S. Substantial Presence Test uses 31 days in the current year and 183 days over a 3-year period, with prior years weighted at 1/3 and 1/6. The U.K. Statutory Residence Test includes a 183-day trigger, but HMRC also evaluates ties, including family, accommodation, work, and 90-day ties. So "under 183 days" alone can create false confidence.

If dual residence is possible, verify the treaty text before taking a position. Tie-breakers can look at habitual abode, then nationality if needed. If you take a U.S. treaty-based return position that reduces or overrules U.S. tax, disclosure is generally required on Form 8833.

Where assumptions fail#

Most compliance problems start with a shortcut that sounds reasonable and then collapses under the actual rule. Use the table below to pressure-test your assumptions before they turn into filing or contract problems.

| Common nomad assumption | What authorities or counterparties actually assess |

|---|---|

| "Under 183 days means I cannot be tax resident." | Day count may be only one part of the test. U.K. ties can matter, and U.S. substantial presence uses a 3-year weighted formula. |

| "I only need to worry about one country at a time." | Overlapping residence claims can happen. Treaty tie-breakers may apply, depending on the treaty text. |

| "No single foreign account crossed the limit, so no U.S. report is due." | FBAR uses the aggregate value of foreign financial accounts, not a per-account test. |

| "No local entity means no PE risk." | PE analysis can include fixed place of business activity and whether an agent habitually exercises authority to do business for the company. |

Keep a monthly day log you can reconcile to travel records, calendar entries, and accommodation records. Your memory is not a defensible audit trail.

For U.S. persons, handle foreign-account reporting early#

Do not leave foreign-account reporting until filing season. If you are a U.S. person, check FBAR exposure throughout the year. IRS rules use aggregate foreign-account value and trigger reporting when it exceeds $10,000 at any time during the calendar year. Before relying on any reporting threshold in a workflow, verify the current rule against the official record for the filing year.

| Item | Detail | Timing |

|---|---|---|

| Monthly checkpoint | Update each account's high balance and your combined peak | Monthly |

| FBAR trigger | Aggregate foreign-account value exceeds $10,000 | At any time during the calendar year |

| FBAR due date | April 15 | Annual filing |

| Automatic extension | October 15 | Automatic |

| FBAR record retention | Five years from the due date | After filing |

| General assessment period | 3 years | Return support generally |

Use a monthly checkpoint to update each account's high balance and your combined peak. FBAR is due April 15, with an automatic extension to October 15. Keep FBAR records for five years from the due date.

Your support file should include the filed FBAR, an account inventory, year-end and high-balance statements, and the worksheet used to compute aggregate peak value. For return support generally, retain records through the applicable limitations period. IRS notes a general 3-year assessment period.

Review PE exposure in contracts, not after the fact#

Permanent establishment risk is easier to prevent in the contract than to explain once the work starts. PE generally involves a fixed place of business. Exposure can also arise where an agent habitually exercises authority to do business for the company. HMRC also notes that preparatory activities can fall outside PE, but that must be verified in the relevant jurisdiction and treaty context.

Before signing, review authority, place, and control language. If the terms suggest your workspace functions as the client's place of business, or grant authority to habitually do business on the client's behalf, get that language reviewed before execution. Keep dated copies of the guidance you relied on, since rule application can vary by period, including references to chargeable periods beginning prior to 1 January 2026.

Run a simple compliance cadence#

The goal here is not complexity. It is to stop running compliance from memory.

- Intake: For each new country or client, open a file with residency rules, treaty notes if relevant, account list, and signed contract. Mark unresolved rule-sensitive fields as pending until official or source records confirm them.

- Monthly tracking: Update day counts, ties, and foreign-account peak balances. Save records that support each entry.

- Pre-filing review: Reconcile trackers to return positions, confirm whether FinCEN Form 114 is triggered, and check whether any treaty-based return position needs Form 8833.

- Contract checks: Review new and renewed agreements for PE exposure, including authority, local presence language, and work scope. Retain redlines and final signed versions.

If you do one thing here, keep a dated, jurisdiction-by-jurisdiction evidence file. That is what keeps small issues from turning into expensive ones.

Related: Best Coworking Spaces for Nomads Who Need Reliable Workdays.

Before you file anything, map your travel pattern and residency signals in one place with the Tax Residency Tracker.

Pillar 3: The Resilience Blueprint - Structure Your Business for Volatility#

Resilience is what keeps a delay, review, or payment hiccup from turning into an operating problem. Once your income is provable and your compliance file is current, the next step is to give your money clear roles, keep clean evidence, and avoid single points of failure.

Build local credibility before you need it#

Do not assume your financial history will transfer cleanly across borders; treat portability as uncertain. Traditional finance still leans on fixed-address identity models, so mobile professionals often face extra credibility friction when their records look fragmented.

Use a practical documentation routine each time you enter a new country. Keep your identity and account records organized from day one, and track evidence consistently. Treat that as operating discipline, not a guarantee of approval.

For underwriting readiness, keep a clean proof file. Save at least 6 months, and preferably 12 months, of statements from your primary business account. Keep related account statements and payment records together so the file reads like a stable operating business, not a scattered stack of invoices.

Give each account one job#

A single all-purpose account feels simple, but mixing everything can reduce visibility. A segmented setup is one way to separate collection, spending, tax holdbacks, and short-term shocks.

If your banking access allows it, a role-based setup might look like:

- Collection account for inbound client payments

- Operating account for routine business spending

- Tax account for funds reserved between filings

- Buffer account for delayed payments or temporary disruptions

This will not remove volatility, but defined roles can make day-to-day decisions easier to audit. Use this as a planning template and verify it against your own constraints.

| Architecture | Control | Failure risk | Admin effort |

|---|---|---|---|

| Single-account setup | Can be lower visibility because all flows are mixed | Can be higher concentration risk if one issue affects the account | Can be lower ongoing effort |

| Segmented multi-account system | Can be higher visibility because roles are separated | Can be lower concentration risk when key functions are split | Can be higher ongoing effort |

If part of your inflow depends on opaque crypto transaction paths, treat that as a risk area rather than a core rail. FinCEN has proposed recordkeeping and reporting requirements related to certain CVC-mixing transaction exposure for domestic institutions and agencies. That is a proposal, not final law, but it is still a resilience signal.

Set a reserve policy you can verify#

An unwritten reserve target can fail when you need it most. Leave the reserve target range unresolved until your own records support it.

Then size your reserve against your real operating pattern: income volatility, fixed obligations, tax exposure, and client concentration. Recheck the policy against your last 6 to 12 months of primary business-account statements. Keep the reserve in a dedicated account, and retain monthly balance evidence plus transfer records.

If you want a deeper dive, read Should Your Freelance Business Accept Credit Cards?.

Conclusion: You Are the Architect#

The point is simple: better outcomes come from records that are designed, not improvised. Your financial identity as a nomad is the evidence you can produce quickly, the decisions you document, and the gaps you flag for verification before they become problems.

Your Legitimacy Engine should make readiness clear at a glance. Keep a current proof pack and use one readiness test: if a bank, landlord, or client asks today, can you send a clean packet in one sitting?

Your Compliance Shield should make documentation readiness routine. Keep short notes on what each document proves, and mark every rule-sensitive point as pending until official, financial, government, or source records confirm it.

Your Resilience Blueprint should lower risk by making weak spots visible early. Use a structure you can review quickly, keep a written decision trail, and treat low visibility as the first failure mode to fix.

What to do now:

- Re-run the same checklist from earlier sections on a recurring schedule and before any major application or new client onboarding.

- Refresh your proof pack, archive the prior version, and log what changed.

- Mark each rule-sensitive item as pending until official, financial, government, or source records confirm it before submission.

This is the practical endpoint: a dependable get-paid system that helps you catch delays, avoidable fees, and payment shocks earlier. For a step-by-step walkthrough, see The Future of 'Financial Identity': How AI will help nomads get loans.

When you are ready to turn this checklist into a repeatable get-paid workflow, review Gruv's freelancer payment flow.

Frequently Asked Questions

What is the difference between visa status and tax residency?

Visa status and tax residency do not have one universal legal distinction or test. Treat them as separate requirements to verify under current local rules before you file banking, landlord, visa, or tax paperwork.

Can you use a virtual mail service as your official address for banking?

There is no universal yes-or-no rule. Acceptance depends on the provider and jurisdiction, so confirm what your bank currently accepts before applying. Share sensitive onboarding or KYC data only on official secure websites.

How do you prove income when your earnings swing month to month?

Do not send a random stack of files. Keep a simple, updated proof packet: a short income summary, statements showing where payments land first (income capture account), and organized invoice/receipt history. Required lookback windows vary by provider and jurisdiction, so verify the current window before applying. Refresh your packet on a regular cadence so missed invoices, lost receipts, or unclear income history do not delay applications.

Does your credit history follow you to another country?

There is no universal transfer rule. Ask the target bank or lender what they currently accept, and keep that requirement in writing before you apply.

How much buffer should you keep while building your financial identity for nomads?

Track your runway, meaning how long you can keep operating if income drops. Separate money by purpose instead of using one all-purpose account, fund a tax set-aside from each payment, and automate transfers where possible. As a practical baseline, keep at least one month of fixed bills available and build toward three to six months of core expenses over time; refill your spending account weekly so overspending is visible early.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bis.org/cpmi/cross_border/programme.htmtrusted

- bis.org/publ/bisbull119.htmtrusted

- cityofhomer-ak.gov/sites/default/files/fileattachments/economic...trusted

- drodrik.scholars.harvard.edu/sites/g/files/omnuum7106/files/2025-08/The%2...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- federalreserve.gov/publications/2025-economic-well-being-of-us-...trusted

- fincen.gov/system/files/federal_register_notices/2023-1...trusted

- govinfo.gov/content/pkg/FR-2025-01-03/pdf/FR-2025-01-03.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Should Your Freelance Business Accept Credit Cards?

Offer card payments, but stay in control of how money reaches you. The goal is not a smoother checkout screen. It is predictable cash you can use to run the business.

Getting a Mortgage as a Freelancer Without Guesswork

Start by reconciling your income file before you compare rates. For a **mortgage for freelancers**, the first gate is simple: can an underwriter read your documents cold and see one consistent income story?

IP Protection for Software Developers Using a Copyright-First Plan

Start with a copyright-first baseline, then add other protections where they reduce a specific risk. For small teams doing client work or shipping SaaS features, that makes software IP protection more usable in day-to-day operations.