Quick Answer

No. The carried interest loophole generally concerns fund profit shares, not standard freelance invoices. For most consultants, the safer move is to classify each payment by its real economics, run S-corp compensation in the correct order with wages before non-wage distributions, and treat IRC §1061 as relevant only when an applicable partnership interest is actually present. If your contract references waterfalls, hurdles, or clawbacks, get structure-specific advice before assuming long-term capital-gain treatment.

The Carried Interest Debate: A Primer for the Modern Executive#

What many call the carried interest loophole is a dispute about tax character: whether a fund manager's profit share should be taxed like a return on capital or like payment for services. For you, this is more a decision lens than a tactic to copy.

Carried interest is a profit-sharing right for a fund's general partner. That is separate from a management fee, which is usually based on fund asset size and taxed as ordinary income. The core question is simple: is this income really investment return, or compensation for managing money?

| Item | What it is | Typical recipient | Usual tax character | Where treatment diverges |

|---|---|---|---|---|

| Carried interest | Share of fund profits tied to performance | Fund general partner or manager | Generally capital-gain treatment when requirements are met | Section 1061 can recharacterize certain API-related long-term gains as short-term gains |

| Management fee | Fee based on fund asset size | Fund manager | Ordinary income | Treated as compensation for services |

| Return on own invested capital | Profit tied to the manager's own capital contribution | Partner who personally invested capital | Return on capital | Reform framing often separates this from service compensation |

Where the policy split comes from#

Critics argue this income often functions like compensation and should be taxed more like other pay, warning that lighter treatment can create fairness and efficiency distortions. Supporters argue that higher taxes on carried interest could reduce investment and growth. Critics counter that the benefit is concentrated among fund managers and may have limited investment impact.

For your own planning, this matters because similar economics can be framed in different ways, and weak framing is where trouble starts.

The technical rule that changes outcomes#

The key term is applicable partnership interest (API). Under Section 1061, certain net long-term capital gains tied to an API can be recharacterized as short-term capital gains. IRS guidance states Section 1061 applies for taxable years beginning after December 31, 2017, and final regulations were published on January 19, 2021.

The practical checkpoint is holding period. In the IRS Section 1061 FAQ context, more than three years is a relevant threshold for some API-related gain to retain long-term treatment. So the idea that "it is all capital gains" is usually too simplistic.

What this means for you now#

Treat this as context, not a DIY filing strategy. If someone presents a simple "convert fees into gains" story, pressure-test the documents and the economics. A fee for services, a profit share, and a return on your own contributed capital are not the same thing.

The policy debate remains active, with repeated proposals to tax some or all carried interest as ordinary income, and estimates tied to reform proposals are material, for example about $13 billion over ten years in one estimate. The next sections turn that debate into practical choices with tighter guardrails.

You might also find this useful: A Guide to Schedule B (Interest and Ordinary Dividends) for US Expats.

The Billion-Dollar Lesson: Why the Tax Code Favors Capital Over Labor#

Your first call is classification: is this payment for your work, or for owning something that produced a return? That answer drives your planning, documentation, and how defensible your position is.

The carried-interest debate is a high-profile example of this capital-versus-labor split in fund-manager contexts. The preference debate persisted through late July 2022, when a provision described as limiting the preference during Inflation Reduction Act negotiations was reported as scrapped.

Classify the income before you plan#

Start with the economics and legal rights, not the tax outcome you want.

| Income character | What it reflects | Typical treatment to validate | Main planning lever | Challenge note |

|---|---|---|---|---|

| Payment for services | You were paid to perform work | Often service-income treatment (validate current-year rules) | Clear scope, fee terms, invoices, delivery records | Risk increases if service payments are relabeled as investment return |

| Return on owned capital/assets | You earned from ownership or asset appreciation | Capital-gain treatment may apply when legal requirements are met (validate current-year rules) | Ownership proof, acquisition records, basis, disposition records | Weak ownership or timing records can undermine the position |

| Profit share tied to ownership rights | You share upside through actual ownership rights | Fact-specific based on governing documents and economics | Agreement terms, ownership records, distribution mechanics | High challenge risk when upside resembles compensation without real ownership economics |

You do not get capital treatment by calling it capital treatment. You get it when the facts, rights, and records line up.

Use the two hats test#

Ask which hat you were wearing when the money was earned.

| Bucket | Indicators | Records or implication |

|---|---|---|

| Labor hat | delivery work, advisory work, revisions, client management | Keep service agreements, SOWs, invoices, and related work records |

| Owner hat | capital at risk, ownership rights, transferable assets, retained value | Keep formation and ownership records, approvals, and records showing you owned the relevant asset before payout |

| Red flag | the story is only "I worked hard and got paid more" | Usually still in the labor bucket |

That is the bridge from policy to practice. Tax expenditures can function like spending programs, and testimony has estimated annual forgone revenue above $1 trillion. For you, the narrower takeaway is that tax treatment can differ by income character, so structure and documentation matter.

That sets up the next sections on entity structure and compensation design. The goal is not to force service income into a capital label. It is to separate labor earnings from owner returns where the facts support it. Outcomes depend on your facts, jurisdiction, and professional advice in edge cases. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

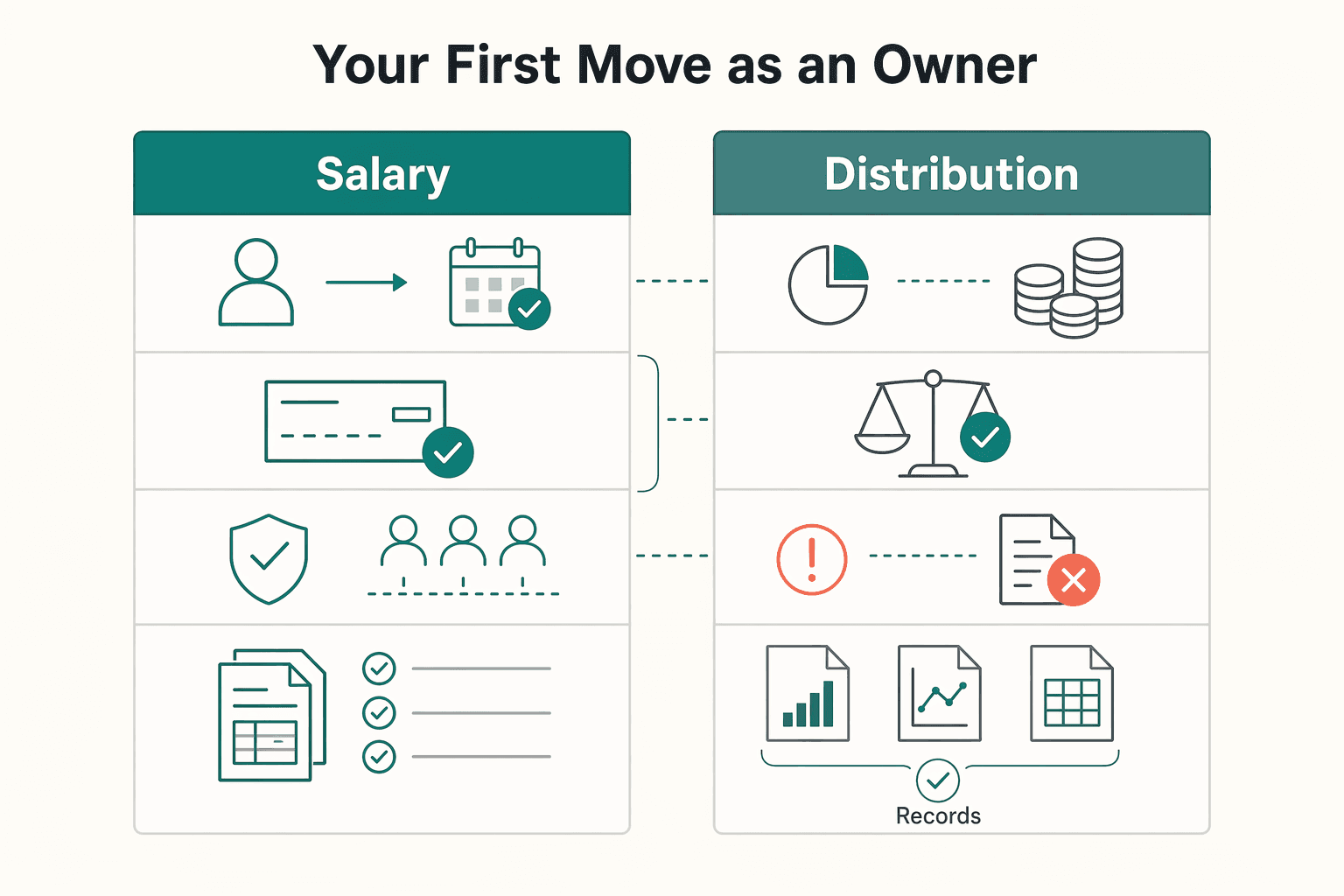

The S-Corp Strategy: Your First Move as an Owner#

If you use an S corporation, get the order right. Pay wages first for the services you actually perform, then treat later payments as non-wage distributions only after that wage decision is supportable. The IRS position is clear on this order for shareholder-employees, and it can reclassify distributions as wages when compensation is understated.

This is separate from Section 1061. That rule addresses certain partnership interests. S-corp compensation is an officer-wages and payroll-compliance issue.

| Payment type | Tax character | Payroll treatment | Cash flow impact | Documentation burden |

|---|---|---|---|---|

| Salary | Payment for services you perform as a shareholder-employee/officer | Treated as wages for officer services; withholding and employment-tax compliance apply | Cash moves through payroll as earned | High: payroll setup, wage records, withholding filings, and support for reasonable compensation |

| Distribution | Non-wage owner payment after reasonable compensation is addressed | Not subject to employment taxes as a non-wage distribution, but can be reclassified if wages were understated | More timing flexibility after wage decisions are set | Medium to high: distribution records, ownership records, and support that reasonable wages were paid first |

Build your wage number from the work you actually do#

Do not start with a target percentage. Start with the work. There is no fixed IRS formula for reasonable compensation, so your file should show how you reached the number based on what you actually did for the company.

Use four inputs, and keep the evidence simple:

- role duties and responsibilities you actually perform

- comparable pay for similar services

- time and effort you devote to delivery, sales, management, and admin

- records that show this was your actual operating pattern

Role notes, benchmark notes, time summaries, payroll reports, and other internal records can help support your position.

Red flags that trigger challenges#

The problem is not distributions by themselves. It is using distributions or loans while treating meaningful labor as something other than wages. Watch for:

- paying yourself only through draws or shareholder loans

- using a token salary with no comparable support

- ignoring your real time and effort in the business

- lacking records that support duties, time, and comparable pay

For globally mobile consultants, take a conservative approach. Confirm S-corp eligibility before filing Form 2553, which must be signed by all shareholders. Do not push salary to the floor when residency or ownership facts are changing. S-corp eligibility rules include restrictions such as no non-resident alien shareholders.

Your execution checklist#

Once the wage logic is sound, execution is mostly recordkeeping and payroll discipline. Use this checklist:

- Confirm S-corp eligibility and file Form 2553 with all required shareholder signatures.

- Run payroll before treating cash movements as non-wage distributions.

- Keep employment-tax records for at least four years after filing the fourth quarter for the year.

- Consider keeping a short compensation memo in your records to document your wage logic.

- Revisit compensation when duties, time, pricing, or profit profile materially changes.

- Escalate to a qualified tax professional for cross-border moves, uncertain eligibility, mixed ownership, or any compensation position that is hard to defend plainly.

We covered this in detail in A Deep Dive into Australia's 'Temporary Resident' Tax Rules.

Before you change entity or compensation structure, map your travel pattern and filing footprint in the Tax Residency Tracker. That keeps your decisions documented and easier to defend.

The Partnership Play: Structuring Fees as 'Profits Interest'#

Use a profits-interest component when you are intentionally trading guaranteed cash for future upside. If you need predictable near-term pay, keep the core fee in cash.

The contract distinction matters. A profits interest is generally a right to future partnership profits, not a fixed fee for current services. You are negotiating for future performance, not just invoicing for value that already exists. That is why the structure matters as much as the headline economics.

Partnership allocations are treated by income character at the partnership level, which is central to the carried-interest debate. So before you negotiate percentages, make sure the legal documents clearly define what is being allocated, when, and under what conditions.

| Structure | Payout timing | Tax character | Risk transfer | Control rights | Documentation complexity |

|---|---|---|---|---|---|

| Cash fee | Fixed or milestone-based, usually near term | Typically distinct from partnership profit allocations | Low; payment is not tied to future profits | None unless separately granted | Low to medium |

| Profits interest | Delayed and contingent on future profits/distributions | Depends on partnership allocations and current law; not the same as a fixed fee | Higher dependence on future performance and distributions | Not automatic; only what governing documents grant | High |

| Blended structure | Cash now plus contingent upside later | Mixed by component (cash vs profit allocation) | Medium | Depends on governing documents | High |

When this can fit your work model#

This works best when your contribution is tied to long-run value creation rather than one-off delivery. If your role is ongoing and performance-linked, future-profit participation may make commercial sense.

It can also fit when the partnership economics are transparent enough to evaluate, including who gets paid first, how distributions flow, and whether a preferred return or hurdle exists.

When it likely does not#

This usually does not fit when your engagement is short, your deliverable is discrete, or your priority is reliable cash collection. In those cases, a standard cash contract is usually the cleaner choice.

Treat opaque economics as a stop sign. If the client will not clearly share waterfall logic and payout order, you cannot evaluate the upside with confidence.

A practical default is to use a blended structure only when the cash portion fully works on its own. The upside should be optional upside, not the part that makes the engagement viable.

Execution guardrails (practical checklist)#

The common failure mode here is document mismatch. Service terms, upside terms, and the operating agreement need to tell the same story.

| Guardrail | Article detail |

|---|---|

| Grant terms | Define what interest you receive, effective date, eligible profit pool, and any hurdle or preferred return mechanics [verify current legal/tax treatment with counsel] |

| Vesting and forfeiture | Define earning conditions, what happens at early termination, and treatment of unvested amounts [verify enforceability with counsel] |

| Waterfall and clawback | Document payout order and whether over-distributions can be clawed back |

| Economic support | Keep contemporaneous documentation showing baseline economics at grant and how future-profit participation is intended to work |

| Operating agreement alignment | Service terms, side terms, and governing partnership terms must not conflict on allocations, transfer limits, or rights |

| Records | Retain signed agreements, approvals, allocation schedules, and a dated deal memo capturing shared intent at signing |

A simple control test is to trace how one dollar of future profit would flow through the waterfall to you. If you cannot do that clearly, pause before signing.

Talk to a pro before you DIY this#

Some facts make this too risky to handle casually. Get tax and legal advice before signing if any of these apply:

- You cannot clearly model the waterfall, payout order, or preferred return/hurdle.

- Vesting, forfeiture, or clawback terms are unclear or internally inconsistent.

- Service agreements and partnership documents use conflicting allocation language.

- The economic value of the upside cannot be explained in plain terms at signing.

This structure can align you with future value, but only when the documents clearly grant future-profit participation rather than a relabeled fee.

Related: How to Use a 'Cost-Plus' Model for Transfer Pricing.

The Endgame: Building a Salable Enterprise#

The real endgame is not clever characterization. It is building something a buyer can run without buying your personal labor. If revenue stops when you step away, you mostly have income. If revenue continues through transferable assets, contracts, and documented operations, you may have enterprise value.

That is the practical lesson for owners planning an eventual transfer: move from labor-dependent work toward an asset a buyer can actually underwrite.

| Dimension | Owner-dependent practice | Salable enterprise |

|---|---|---|

| Transferability | Buyer is effectively hiring you | Buyer can acquire assets, contracts, and operating know-how |

| Revenue durability | Revenue depends on founder relationships and hours | Revenue is supported by recurring agreements, repeatable delivery, and established customers |

| Documentation quality | Key knowledge sits in inboxes and memory | SOPs, contract files, client records, and handoff materials are organized |

| Buyer risk | High key-person and continuity risk | Lower continuity risk because responsibilities, processes, and expenses are defined |

What buyer-ready looks like in practice#

Buyer-readiness is not abstract. It shows up in diligence. The pillars are still IP, brand, recurring revenue, and documented operations, but each one has to hold up under review.

| Area | What to keep ready |

|---|---|

| IP | Keep ownership and usage rights clear in business records |

| Brand | Keep site access and customer information under business control, not personal accounts |

| Recurring revenue | Keep signed agreements, renewal terms, and concentration visibility so durability is testable |

| Operations | Document onboarding, delivery, billing, and quality control so a trained operator can execute without you |

In practice, the point is simple: keep these items in business-controlled records so a buyer can test them quickly.

This is also consistent with SBA guidance. Intangible value can include brand, intellectual property, customer information, and projected future revenue, while existing-business strength can include established customers, defined expenses, and trained employees.

Treat exit tax as transaction-specific#

Do not assume a sale is taxed entirely as long-term capital gain. The IRS states a business sale is usually not a one-asset sale, and assets are treated separately. In the same transaction, inventory can produce ordinary income or loss while capital assets can produce capital gain or loss.

Structure matters too. A transaction may be an asset sale or a stock sale, and outcomes can differ. In qualifying asset deals, if goodwill or going-concern value attaches, Form 8594 may apply. The IRS requires the residual method for transfers of a group of assets that constitutes a trade or business. Acquired Section 197 intangibles are generally amortized over 15 years.

Even with favorable gain treatment, other rules may still apply. NIIT may apply at 3.8% above statutory thresholds ($250,000 MFJ, $125,000 MFS, $200,000 single/head of household). Where an applicable partnership interest is involved, Section 1061 can also recharacterize certain gains, with a more-than-three-years holding-period framework in that context.

Sale-readiness checklist#

The cleaner your records are before a deal starts, the more credible your enterprise value usually is. Use this checklist:

- Document ownership of IP, brand assets, customer records, and key contracts in the business entity.

- Standardize delivery with current SOPs for onboarding, production, QA, billing, and offboarding.

- Reduce key-person dependency by moving client communications, access, and approvals into business-controlled systems.

- Organize revenue evidence: signed agreements, renewal dates, client concentration, and clean revenue history.

- Prepare diligence files: financial records, operating-expense records, and legal documents you may need at sale.

- Confirm exit structure and gain characterization with a qualified tax advisor and attorney before acting.

This pairs well with our guide on A Guide to Conflict of Interest for Independent Consultants.

Your Takeaway: Stop Thinking Like a Freelancer, Start Acting Like an Investor#

The practical takeaway from the carried-interest debate is simple: do not relabel service income. Build a transferable business and document it so the structure, tax treatment, and eventual exit can be defended.

If most of your income still comes from invoices tied to your personal output, you are operating labor-first. The shift is to make each decision increase transferability: recurring revenue, clearer ownership, stronger records, and less dependency on you.

| Dimension | Time-for-money operator | Enterprise builder |

|---|---|---|

| Revenue model | Hourly/project work, custom scope each time | Repeatable offers, retainers, recurring revenue, reusable IP |

| Documentation | Key terms and delivery details live in inboxes and memory | Signed agreements, entity records, transaction summaries, and supporting documents kept systematically |

| Dependency risk | Delivery and client trust depend on you personally | Work can be handed off, monitored, and repeated |

| Exit optionality | Hard to transfer without your ongoing involvement | More credible path to sale, partner buy-in, or managed handoff |

Use that table as a filter for pricing, delivery, and structure choices. Ask yourself: does this decision only buy more of your time, or does it build an asset the business can keep using?

If you use an S corporation, treat payroll setup as a hard compliance checkpoint. Shareholder-employees must receive reasonable compensation before non-wage distributions, and the IRS can reclassify distributions as wages. If you use a partnership or profits-interest model, verify whether you actually have an applicable partnership interest under IRC §1061. Section 1061 can recharacterize certain API-related gains and generally requires a holding period of more than three years for long-term treatment.

What to implement now#

The point is not to chase a tax label. It is to make the business more transferable, then verify the tax treatment that follows from real facts.

- Convert at least one service into a repeatable offer with defined scope, pricing logic, and documented delivery steps.

- Maintain a recordkeeping baseline that summarizes transactions and preserves supporting documents for books and tax return entries.

- Tighten ownership documentation: signed client agreements, relevant IP assignment language, entity records, and current revenue visibility by client and renewal timing.

- Reduce key-person risk by documenting handoffs, approvals, and where critical files, credentials, and client history are stored.

- Before modeling any tax upside, have a qualified advisor verify entity setup, income characterization, and likely exit treatment for your specific facts and jurisdiction.

A common failure mode is strong revenue paired with weak characterization and records. That can surface at audit or sale, especially if the transaction is treated as a qualifying asset sale of a trade or business. In that case, both buyer and seller generally must file Form 8594. Even when capital-gain treatment applies, results still depend on taxable income. The 3.8 percent NIIT can apply above IRS thresholds, including $200,000 for single filers and $250,000 for married filing jointly. Build for transfer first. Optimize second, after the facts and documentation are real.

For a step-by-step walkthrough, see Tax Implications of Receiving Stock Options as a Freelancer.

If you are shifting from solo billable work to a more structured operating model, review Gruv for freelancers to simplify invoicing, payouts, and recordkeeping where supported.

Frequently Asked Questions

What is the carried interest loophole, in plain English?

The carried interest loophole is favorable tax treatment for certain compensation tied to private equity, venture capital, and hedge-fund managers. In that setup, a manager is paid through a share of fund profits (carried interest), not a typical service invoice. These arrangements are often built around terms like hurdle rates, waterfalls, and clawbacks.

Does this apply to you if you are a freelancer or consultant?

Usually not in the direct Wall Street sense. If you are paid through invoices under a services agreement, this material does not establish that income as carried interest. The practical takeaway is to avoid relabeling ordinary client fees as carry without structure-specific advice.

How should you distinguish fees, distributions, profits interests, and sale proceeds?

As a narrow concept check, carried interest here means a share of fund profits for private fund managers, often with terms like hurdle rates, waterfalls, and clawbacks. Beyond that, outcomes are structure- and fact-specific.

What should you document if you want “build a salable enterprise” to be real?

Starting with clear agreement language and economics lets carry terms be evaluated. For documentation checklists or legal requirements, get transaction-specific advice.

What if your arrangement actually looks like carried interest?

Start with the agreement language and economics. Check whether it grants a share of profits and whether it references terms like hurdle rates, waterfalls, clawbacks, or a holding-period framework, including the cited "more than three years" context. If you are mainly paid through invoices, treat it as service compensation unless a qualified advisor says otherwise.

Should you plan around policy changes now?

If you are in a true carry structure, monitor policy risk closely. There was active political pressure to end this tax break, but implementation details were still described as unclear, including timing and grandfathering. Do not make major decisions from headlines alone.

When should you talk to a pro?

Talk to a qualified tax professional whenever your structure or timing is unclear, or before major decisions tied to carry treatment. Ask for your current-year treatment to be checked against your exact agreement terms, timeline, and holding-period considerations. This is where generic guidance stops and case-specific advice starts.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cbo.gov/budget-options/60946trusted

- congress.gov/crs-product/R46447trusted

- federalregister.gov/documents/2021/01/19/2021-00427/guidance-und...trusted

- irs.gov/businesses/partnerships/section-1061-reporti...trusted

- irs.gov/businesses/small-businesses-self-employed/s-...trusted

- sba.gov/business-guide/manage-your-business/close-or...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

How to Use a 'Cost-Plus' Model for Transfer Pricing

Before you use this playbook, note the evidence limit for this section: the grounding available here does not establish technical rules for cost-base construction, arm’s-length legal tests, comparables screening, defensible markup ranges, or jurisdiction-specific thresholds. Treat the steps below as an internal execution checklist, and escalate technical transfer-pricing positions to a qualified advisor.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.