Quick Answer

Vietnam tax for expats starts with one decision: are you a Vietnam tax resident or non-resident based on facts you can prove. Residents face Vietnam PIT on worldwide income, while non-residents are generally taxed only on Vietnam-sourced/Vietnam-related income, such as work performed in Vietnam. Treat 183 days and long leases as high-signal triggers, and build an evidence pack (day logs, entry/exit records, contracts, invoices, and payment trails) to support your position.

You don't need a rates dump-you need a residency + evidence playbook you can run in 10 minutes#

If you get one thing right, get your residency posture and your evidence stack aligned. That single decision drives almost every other tax decision you make in Vietnam because it sets scope. Scope comes from two inputs: residency and sourcing.

Most people do this backwards. They burn time hunting for a perfect rates table before they have decided what income Vietnam can even see. Rates are downstream. Scope is upstream.

Read this as an operator playbook, not theory. Your goal is to make your filing position boring, coherent, and easy to defend using documents you already have. Pick a defensible default, document it immediately, then have a licensed advisor pressure-test edge cases.

Step 1: Pick a residency posture you can prove#

Under Vietnam rules, a tax resident can face worldwide taxation under the Vietnam tax system. A non-resident can still face Vietnam tax on Vietnam-related income. A Double Taxation Agreement (DTA) can affect outcomes in some cases, but treaty positions still depend on facts and paperwork.

Do not aim for the cleverest posture. Aim for the posture you can prove quickly without improvising. If your facts sit close to residency thresholds, use a defensive default until you confirm the final position.

If you cannot prove tax residence in another country, treat time-in-country and accommodation signals as high risk. A lease term of 183 days or more in a Vietnam tax year is a signal you should not ignore.

Your practical objective is not to win arguments. It is to maintain a position you can support on demand with clean records.

Step 2: Classify income into "Vietnam-related" vs not#

Once residency is framed, the next job is turning messy real life into a ledger you can audit. Classify each inflow by what created it and where the work was done. Do not classify based on where money landed.

Think in terms of a mapping pass you run for every payment. You are not trying to write a legal memo. You are building a reviewable trail that ties the commercial story to the money.

Use this mapping for each inflow:

- What work was delivered?

- During which period?

- Where was that work performed?

- What did the client actually buy: output, support, or both?

The moment you can answer those questions from your own files, tax anxiety drops. You stop guessing and start checking.

Step 3: Understand what PIT is (without getting lost)#

Personal Income Tax (PIT) is Vietnam individual income tax. Keep the model simple: decide what income is in scope, then apply the right label and treatment to each inflow.

| Your posture | What Vietnam may tax | Your 10-minute goal |

|---|---|---|

| Tax resident | Vietnamese-sourced plus foreign-sourced income under a worldwide concept | Prove residency basis and list all income streams |

| Non-resident | Vietnam-related work income | Prove non-residency and document Vietnam-related scope |

If a DTA could apply, treat it as a structured override after domestic analysis, not as your first move.

The 10-minute residency decision tree (the only "first step" that matters)#

Decide resident versus non-resident from facts first, then gather the documents that support those facts. Run this check monthly. It keeps your tax position aligned with travel, leases, and work patterns before contradictions build up.

Step 1 - Build your residency fact pattern (don't guess)#

Start with two buckets: physical presence and accommodation. You are building a fact pattern you can show, not a vibe.

- Physical presence: keep a day count for time spent in Vietnam.

- Accommodation: flag any rented housing with a lease term of 183 days or more in a tax year.

If you cannot establish residence elsewhere, these signals become more important. The best time to organize residency records is while the year is happening, not after.

Step 2 - Use a safe default near thresholds#

When your pattern sits near 183 days or your housing file is strong enough to raise residency questions, adopt a defensive default. Act as if resident-level documentation may be needed, even before your final classification is confirmed.

In practice, that means you start capturing worldwide income records now: contracts, invoices, payout reports, and bank inflows tied to service periods. You can later confirm non-resident treatment if facts support it. You cannot reliably recreate clean records months later without gaps and contradictions.

Step 3 - Separate tax from immigration, but keep your story consistent#

Tax status and immigration status are different systems. A work permit is an immigration and labor issue. Tax status depends on residency and income facts.

Those systems are separate, but your timeline must still be coherent across both. If your visa, permit, or exemption timeline says one thing and your day-count file says another, you create avoidable risk. Build one timeline and reuse it everywhere.

Step 4 - Pick a planning branch (not legal certainty)#

You are not declaring final legal truth in this step. You are choosing the planning lane that reduces avoidable mistakes.

| Branch | Working assumption | Planning focus |

|---|---|---|

| A | Likely tax resident | Map all income streams and prepare worldwide-scope records |

| B | Likely non-resident | Isolate Vietnam-connected work and document service location clearly |

Both branches can change after professional review. The point is to keep records good enough for either branch, so you do not get trapped by missing evidence later.

Step 5 - Confirm safely#

Vietnam has signed DTAs with more than 80 countries and territories. Cross-border relief may require supporting documents and formal steps. If you are US-connected, remember the US and Vietnam do not currently have a complete income tax treaty in force.

Use this sequence: build your domestic posture first, then test any treaty logic, then confirm with a Vietnam-licensed advisor for the current year.

"If I work remotely in Vietnam, do I owe Vietnam tax?"-a sourcing model you can actually use#

Potentially yes. If services are performed while you are physically in Vietnam, treat that period as Vietnam-sourced income risk until your facts are confirmed. This is where freelancers get burned by focusing on client location, payment currency, or bank destination instead of where work happened.

You do not need to become a tax technician to get this right. You need a sourcing model you can run consistently, plus an evidence stack that makes your model believable.

Two questions that prevent bad decisions#

Every remote-work case starts with two questions. Keep them separate, because mixing them is how people misclassify income.

- Residency question: how wide is your tax net?

- Sourcing question: which inflows fall inside Vietnam's net?

Residency usually determines breadth. Sourcing determines line-item inclusion. Decide each one cleanly, then connect them in your ledger with a simple note that a reviewer can follow.

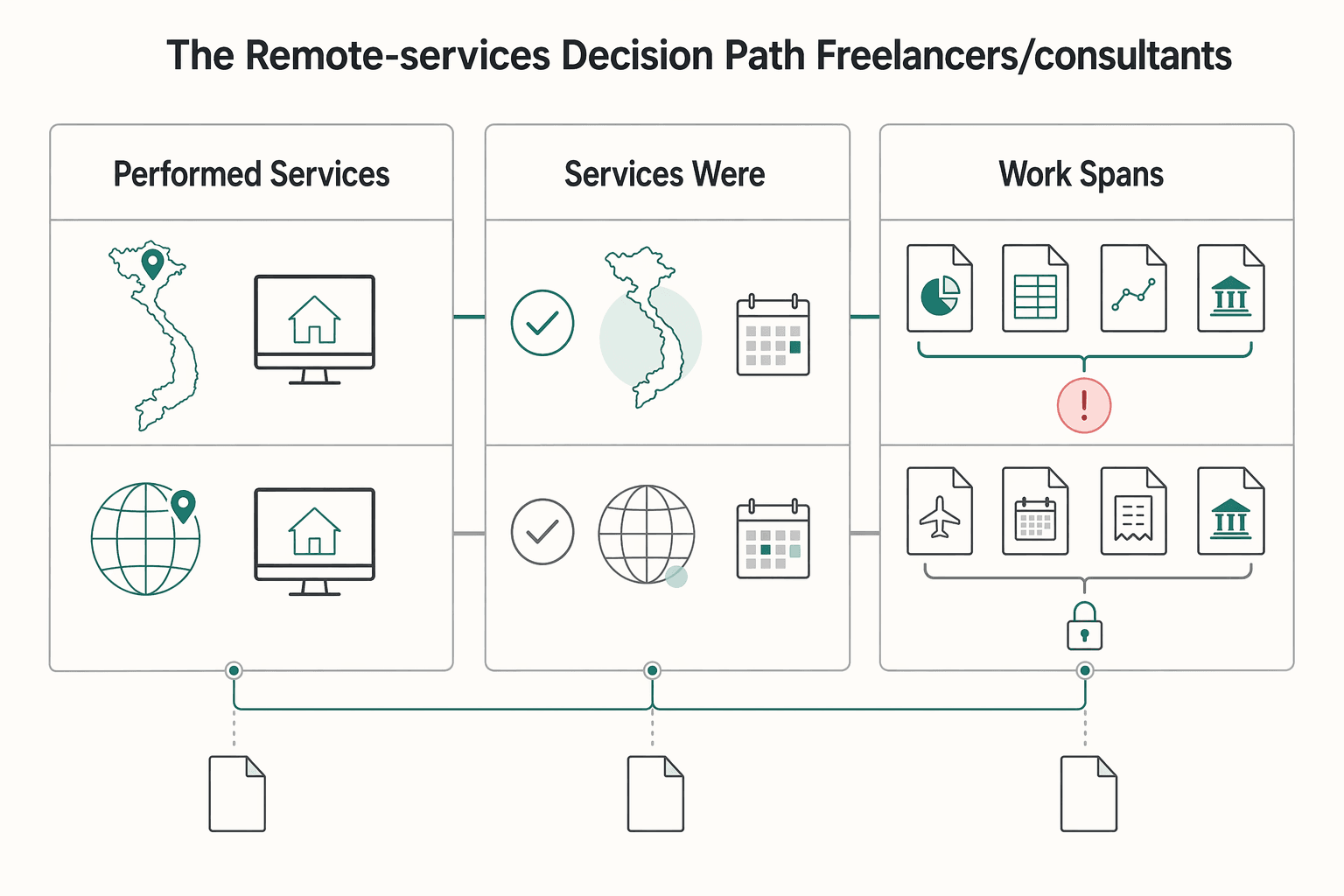

The remote-services decision path (freelancers/consultants)#

Run a simple operating rule until you receive fact-specific advice.

| Service pattern | Working treatment | Record action |

|---|---|---|

| Performed the services while in Vietnam | Classify that service period as Vietnam-sourced risk | Keep evidence for that period |

| Services were performed outside Vietnam | Ring-fence that period | Keep matching documents |

| Work spans multiple locations across one invoice | Tie the invoice to a service period record that shows how you split the work windows | Do not let the invoice become a single ambiguous blob |

If you performed the services while in Vietnam, classify that service period as Vietnam-sourced risk and keep evidence for that period. If services were performed outside Vietnam, ring-fence that period and keep matching documents. This avoids one of the most common errors: treating payment location as if it controls sourcing.

A payment sent from abroad can still relate to work performed in Vietnam. Your file should show what was delivered, when it was delivered, and where the services were performed.

If your work spans multiple locations across one invoice, do not let the invoice become a single ambiguous blob. Instead, tie the invoice to a service period record (even a simple note) that shows how you split the work windows. The goal is not to argue in the abstract. The goal is to keep your own records internally consistent.

Evidence that makes "where the work happened" coherent#

You do not need perfect surveillance of your life. You need a coherent record set that tells one story from contract to payment.

Start with the core four, then add supporting detail only if it improves clarity:

- Contract and SOW: scope, client, deliverables, timing.

- Invoice and service period: revenue tied to specific work windows.

- Time logs and calendar exports: workload by date.

- Travel records: presence by period.

| Evidence type | What it proves well | What it does not prove alone |

|---|---|---|

| Contract plus SOW | Scope and obligations | Exact day-by-day work location |

| Invoice plus service period | Revenue-to-period mapping | Tax treatment by itself |

| Time log plus calendar | Work cadence and dates | Income classification by itself |

| Travel records | Physical presence windows | Client benefit or income type |

Store this as an evidence stack, not isolated documents spread across tools. When a question comes up, you want to click one folder and see the entire story in sequence.

Where rules vary (and how to confirm)#

Non-resident scope is often described as including income received from working in Vietnam or Vietnam-related income. Treatment can also depend on applicable DTA provisions. That is exactly why you run this as a process, not a one-time guess.

Confirm the final classification with a Vietnam-licensed advisor, but do not wait for that meeting to build your records. The record system is what protects you before advice, and it is what makes that advice usable.

Personal Income Tax (PIT) in Vietnam: the parts that matter (and the rates you actually need)#

PIT planning is a two-step job: decide scope, then apply the right income label. Once those two steps are clean, rates become manageable and filing choices get less stressful.

A clean scope decision also keeps you from overpaying out of caution or underpaying out of optimism. Both outcomes usually come from the same root cause: unclear classification.

Start with scope (it changes the whole game)#

Under Vietnam rules, tax residents are generally taxed on worldwide income, while tax non-residents are generally taxed on Vietnam-sourced income only. This switch determines what your ledger must contain.

Resident posture usually means global inflow visibility. Non-resident posture usually means disciplined isolation of Vietnam-sourced items, with notes on why other inflows sit outside scope. If a DTA applies, treaty analysis sits on top of this domestic base.

If you want a quick self-check: look at your ledger and ask whether a reviewer could tell, just from your rows and links, what is in scope and why. If the answer is no, you are not ready to optimize. You are still in cleanup mode.

Employment income: the only headline rates most people need#

Most people only need two headline anchors for employment-style income:

- Residents: progressive rates from 5% to 35%.

- Non-residents: Vietnam-sourced employment income commonly described at a flat 20%.

| Status | Scope anchor | Headline employment takeaway |

|---|---|---|

| Tax resident | Worldwide concept | Progressive 5% to 35% |

| Non-resident | Vietnam-sourced employment | Flat 20% |

Use these as orientation points. The operator move is not memorizing brackets. It is making sure your employment compensation, benefits, and reimbursements are documented well enough that the right treatment can actually be applied.

Non-employment income: don't memorize-label correctly#

Non-employment income can be taxed at different rates depending on income nature. Most errors here are classification errors, not math errors.

Instead of trying to memorize categories, set up an inflow ledger that forces you to label consistently. Keep one row per payment and make these columns mandatory:

- income type label

- contract or invoice link

- service period

- your working sourcing view

- one-sentence reason note for the sourcing tag

This makes your position reviewable. It also makes it easier to work with an advisor because you are giving them a structured input, not a pile of PDFs.

Fringe benefits & reimbursements: where expats can lose favorable treatment to "paperwork failure"#

Benefits are often lost on documentation quality, not on underlying eligibility. If your paperwork is weak, favorable treatment becomes hard to defend even when facts are reasonable.

Treat benefits like a controlled process, not a monthly scramble. You are building repeatable evidence that matches your employer policy, your contract language, and the payment trail.

The "receipt + policy + contract" triad (build once, reuse forever)#

Treat each recurring benefit as a controlled packet with three required artifacts.

| Piece | What it proves | Safe default to store |

|---|---|---|

| Receipt | Amount and payor trail | Invoice, lease, ticket, and payment proof in the correct name |

| Policy | Rule and conditions | Written employer policy or contract clause |

| Contract | Entitlement basis | Agreement language that shows coverage |

Build this once per benefit type, then reuse the same file structure monthly. That is how you avoid re-litigating the same benefit every time you file.

Common benefits: structure matters#

Start with consistency, not creativity. The structure that usually holds up is the one where the written policy, payment route, and your claim all match. When those three disagree, you force the reviewer to guess what happened.

Home-leave flights and education fees are good examples because they often look clean on paper until you inspect the payment trail. If your intended treatment depends on direct employer payment, keep proof of that payment route and keep the supporting condition coherent in your documents. The rule is simple: do not let your file tell two different stories.

If you are reimbursed, keep the approval chain and attach it to the receipt packet. If the employer pays directly, keep the direct-payment proof with the same packet. Either way, your goal is one folder that explains the benefit end-to-end without extra narration.

Housing: don't let your lease contradict your residency narrative#

Housing files do double duty. They affect benefit treatment and can influence residency analysis. Keep lease agreements, payment records, reimbursement approvals, and employer housing documents in one connected folder.

If your lease term reaches 183 days or more, be extra careful that your housing documentation does not contradict your residency posture. Your tax narrative should match your lease narrative without forcing explanations later.

Confirm safely#

Treat favorable benefit outcomes as item-specific and document-dependent. Final treatment should be checked with a Vietnam tax advisor based on your current facts.

The "audit-ready evidence layer" for freelancers: what documents prove what (and what's weak)#

A defensible tax position is an evidence problem before it is a technical problem. Pair each claim with contemporaneous records you can produce quickly.

The practical test is simple. If your proof sits in scattered chats and screenshots, your confidence drops the moment someone asks for reconstruction. If your proof lives in a structured folder with clear naming and links back to your ledger, questions become routine.

Build a "claim → evidence" map (and be honest about what's weak)#

Create a claim map that forces evidence quality checks. Do not aim for perfect. Aim for honest.

| Claim | Stronger evidence | Weaker evidence |

|---|---|---|

| Residency posture | Organized timeline supported by third-party records | Memory-based travel notes |

| Non-Vietnam sourcing position | Contract scope plus dated delivery records | Generic calendar blocks |

| Reimbursement treatment | Written policy plus receipts plus approval chain | Verbal internal norms |

This table is more than a template. It is a weekly decision tool. When you notice you are leaning on weak evidence, you can fix it while time is fresh instead of trying to patch it later.

Create a reconciliation trail (single source of truth)#

Your ledger is the hub. Everything else should link back to it.

Keep one reconciliation chain for every inflow. The chain should tie revenue recognition, payment proof, and banking evidence without gaps.

Minimum chain:

- Invoice

- Contract or SOW that matches invoice scope

- Payment confirmation from platform or client

- Bank statement entry

- FX conversion note when currencies change

Audits usually reward contemporaneous and verifiable records. This chain gives you both. It also makes it easier to answer your own questions when you are doing year-end totals.

Multi-rail payments: control the ambiguity you create#

Using multiple platforms and bank accounts is not automatically a compliance problem. Ambiguity appears when those rails are not reconciled in one view.

Run one ledger that maps each inflow from invoice ID to provider reference to bank credit. Use consistent filenames with date and amount tags so any reviewer can follow the trail in minutes.

If you want this to stay low-maintenance, standardize two habits:

- Every invoice gets a stable ID you never reuse. 2) Every payout record is saved with the invoice ID in the filename (or in the same folder).

You are reducing cognitive load. You are also preventing the most common freelancer failure mode: money arrives, the work is real, but the chain is not provable quickly.

Retention safe default#

Maintain a year folder per jurisdiction and a separate residency folder. If you are treated as a Vietnam PIT resident and rely on mechanisms such as foreign tax credits, supporting documents are required.

Treat treaty and credit mechanics as paperwork-dependent. Relief is earned through coherent documents, not assumptions.

Tax treaties & double taxation: the safe-default playbook (not wishful thinking)#

Treaty planning is useful only after your Vietnam domestic position is coherent. If you need the cross-border framework first, start with How to Legally Avoid Double Taxation: A Freelancer's Guide to Tax Treaties. Use treaties as optimization, not as a substitute for core compliance.

A Double Taxation Agreement (DTA) aims to reduce the chance of the same income being taxed twice. Vietnam has signed treaties with more than 80 countries and territories. That is helpful context, but it does not remove filing and evidence requirements.

The operator default: lock Vietnam first, then test treaty fit#

Start with domestic analysis every time, even if you are confident a treaty exists.

- Determine your Vietnam residency treatment from facts.

- Determine what income is in scope under domestic rules.

- Only then test whether treaty provisions change the outcome.

This sequence prevents premature treaty assumptions that fall apart once documentation is requested.

A practical treaty workflow you can run in one sitting#

This is a tight workflow you can run without turning your week into a research project. Keep it in order:

- Step 1: confirm the treaty exists for the country pair.

- Step 2: match income to the right treaty category.

- Step 3: resolve dual-residence issues using tie-breaker rules when relevant.

- Step 4: prepare claim documentation before filing.

| Goal | What makes it defensible |

|---|---|

| Treaty relief claim | Treaty application, coherent residency narrative, and supporting records |

| Foreign tax credit relief where relevant | Complete supporting documents and matching calculations |

Treaty benefits are not automatic. The filing process and your documentation do most of the work.

Permanent Establishment (PE): the quiet risk freelancers miss#

Permanent Establishment (PE) is commonly described as a fixed place of business through which business is carried on. Depending on your client structure and facts, PE questions can surface even when you think you are only providing remote services.

If a key relationship has long duration, local dependency, or operational substance in one place, escalate for professional review before you lock your filing position. Do not wait until filing season to discover your story is incomplete.

Confirm safely#

Treaty outcomes are fact-specific and process-dependent. If you plan to rely on treaty positions for Vietnam tax treatment, get qualified advice and keep one consistent narrative across all forms.

If you're also dealing with the IRS: a two-country compliance checklist that won't contradict itself#

If you are a US person, run Vietnam and US compliance in parallel. Do not treat one system as a replacement for the other. The goal is one fact pattern expressed consistently in both jurisdictions.

The IRS generally taxes US citizens and resident aliens on worldwide income. Vietnam may also impose tax and reporting obligations depending on your facts.

The "no-contradictions" framework#

Build one master file and reuse it for all filings. When you do this, most cross-border stress turns into routine administration.

- Location timeline: where you lived and worked, by date.

- Work narrative: what services you performed, where, and for whom.

- Account inventory: accounts you own or control.

When those three files disagree across forms, risk increases quickly. When they match, even complex situations become explainable.

US items to flag early (common landmines)#

| Item | What to remember |

|---|---|

| FEIE | Rules-based. Qualification depends on meeting specific requirements. |

| FTC | Credit or deduction may be available, but you cannot claim FTC on income you exclude. |

| FBAR (FinCEN Form 114) | Filed with FinCEN, not with the IRS. |

| FATCA (Form 8938) | Filing Form 8938 does not replace FBAR when FBAR is required. |

| Schedule SE | If net earnings are $400 or more, reporting on Schedule SE is required. |

For employees, US Social Security and Medicare taxes generally continue to apply to wages for services performed outside the US.

Fix-it guardrail#

If prior-year foreign asset reporting was missed, do not improvise a patchwork response. Discuss the IRS Streamlined Filing Compliance Procedures with a qualified advisor. Eligibility is fact-specific and includes non-willful certification requirements.

The compliant workflow: what to do this week (and what to automate so it stays low-stress)#

Consistency beats intensity. A light weekly workflow prevents year-end reconstruction and keeps your position defensible with minimal stress.

The key is that you are not doing taxes every week. You are maintaining the evidence layer that makes tax work straightforward later.

1) Your weekly compliance block (keep it boring)#

Treat this like paying yourself first. One recurring block each week, same outputs every time.

| Output | What to do |

|---|---|

| Presence log stays current | Update your day log for Vietnam presence and keep entry-exit support with it |

| Inflows get labeled immediately | Classify each new inflow by income type while the context is fresh |

| Sourcing gets one reason note | Tag sourcing and add a one-sentence reason so the decision is reviewable later |

Output 1: presence log stays current. Update your day log for Vietnam presence and keep entry-exit support with it. Output 2: inflows get labeled immediately. Classify each new inflow by income type while the context is fresh. Output 3: sourcing gets one reason note. Tag sourcing and add a one-sentence reason so the decision is reviewable later.

Day counts can rely on immigration certification shown in your passport, so keep those records clean and easy to retrieve.

2) An "audit pack" you never rebuild#

Maintain two standing folders and update both weekly. The goal is that you can answer most questions by sharing a structured folder, not by writing explanations.

- Residency folder: day log, passport or immigration entry-exit records, and supporting residence artifacts.

- Income folder: contracts, SOWs, invoices, payment confirmations, bank records, and FX support.

If you approach 183 days in a calendar year or in a 12 consecutive months window, tighten controls immediately. If resident treatment applies, worldwide-income documentation pressure rises fast, and you want that work done before it becomes urgent.

3) Make payments traceable (without changing your whole stack)#

Do not rebuild your banking setup just to be compliant. Most of the value comes from making your existing rails traceable.

Use consistent invoice IDs and standardized payment references across all rails. If your providers offer structured payout references, use them for reconciliation clarity.

Keep one reconciliation sheet with these fields:

- invoice ID

- provider reference

- bank credit

- file link

This can be a simple spreadsheet if it stays current. If it is not current, it turns into another abandoned system and you lose the benefit.

Micro-checklist (printable)#

- Day log updated

- Contracts and invoices stored

- Payments matched to invoices

- FX conversion support saved

- Supporting documents filed with clear naming

When to stop DIY and bring in a pro (and how to keep your bill down)#

DIY works until complexity shifts from organization to judgment. Once residency, sourcing, or treaty exposure becomes ambiguous, professional review becomes a risk-control decision.

The goal is not to outsource responsibility. The goal is to buy judgment where your own rules start to break.

Escalate if any of these are true#

Use this as a hard trigger list.

- You are likely a Vietnam tax resident and also handling meaningful offshore income or mixed income types.

- You want DTA relief or are testing tie-breaker concepts.

- Compensation includes unusual items such as equity, large one-time payments, or benefit-heavy structures.

- You have multi-country physical presence with no clear primary base.

- You suspect PE exposure in a key client relationship.

- You are a US person with FBAR, Form 8938, FTC decisions, streamlined procedures, or late-filing cleanup.

For FBAR context, the IRS describes a filing trigger when aggregate foreign financial account value exceeds $10,000 at any time in the calendar year.

Bring a prep packet (so you pay for judgment, not fact-finding)#

Bring complete inputs before the call so advisor time is spent on decisions.

| Packet section | Include |

|---|---|

| Residency proof | day-count export, entry-exit records, visa artifacts where relevant |

| Income proof | contracts, SOWs, representative invoices, payment evidence, bank records, full-year totals |

| Benefits file | receipts, lease records, policies, approvals |

| One-page narrative | where you lived, where you worked, where clients were, written to match documents |

A clean packet changes the economics of professional help. You stop paying someone to reconstruct your year and start paying them to pressure-test your position.

Safe-default instruction#

Ask this question: What filing position is defensible with my current evidence, and what documents are missing?

That framing produces better outcomes than chasing a lowest-tax answer you cannot support.

The bottom line: pick a defensible residency posture, then run the evidence system every week#

The winning move is operational control. Decide your posture, classify inflows consistently, and maintain evidence every week. That is how you keep tax decisions stable when facts get messy.

This is not about perfection. It is about making your position explainable from your own files without heroic effort.

Your safe-default playbook#

Use this table as your weekly anchor.

| Your posture | Typical scope anchor | What to optimize |

|---|---|---|

| Tax resident | Worldwide taxable income under Vietnam PIT concepts | Clean classification, complete records, and one cross-border narrative |

| Non-resident | Vietnam-sourced income | Tight sourcing notes and clear Vietnam-related evidence |

If your day count is near 183 days, tighten records before you hit thresholds. The paperwork is easier when it is routine.

Treat treaties as secondary, paperwork-dependent#

Treaties can help in the right fact pattern, but treaty logic should come after domestic analysis and only with full documentation. If you cannot support a treaty position with records, do not build your filing plan on it.

Keep one reconciliation chain (invoice → payment → any calculation records you used)#

Traceability beats complexity. Keep each inflow linked from invoice to payment to banking evidence, and keep any calculation records used for reported amounts in the same folder path.

Organized records reduce filing friction and make follow-up questions easier to answer because you are showing, not explaining.

Suggested next reads#

Read in this order based on your bottleneck:

- Residency and day-count hygiene if your location pattern is changing.

- Sourcing documentation if remote services are your main income.

- Double-tax mechanics only after residency and sourcing files are clean.

Light-touch CTA#

If your real issue is broken invoice-to-payment traceability, fix that first. Standardize invoice IDs, payment references, and reconciliation naming so your tax file and cash file tell the same story.

Frequently Asked Questions

How do I know if I'm a tax resident in Vietnam?

Start with the 183-day test. If you're physically present in Vietnam for 183 days or more in a calendar year, you likely fall into Vietnam's tax-resident bucket. The test can also apply within any rolling 12-month period. Vietnam's rules can also treat you as resident if you have a rented house in Vietnam with a lease term of 183 days or more in a tax year.

Do expats pay tax on worldwide income in Vietnam?

If you qualify as a Vietnam tax resident, Vietnam can tax you on worldwide income under its Personal Income Tax (PIT) framework. In plain terms: residency can pull offshore income into scope. That can include income paid from outside Vietnam.

What is the personal income tax rate in Vietnam for foreigners?

For resident employment income, summaries often describe progressive rates ranging from 5% to 35%. For non-residents, some guides summarize a 20% flat rate on Vietnam-sourced income. Rate treatment can vary by income type, so confirm the rate that matches your income category.

If I work remotely in Vietnam for a foreign company or offshore clients, do I pay Vietnam tax?

Don't start with your client's location. Start with Vietnam tax residency. Guidance aimed at remote workers frames obligations as primarily determined by residency status, and it can also turn on whether the income is treated as Vietnam-related. If your facts sit in a gray zone, document where you performed the work and get local advice before you file.

What income is considered Vietnam-sourced income?

Use a practical working definition: Vietnam-sourced income generally connects to income received as a result of working in Vietnam or other Vietnam-related income in the tax year. Beyond that, you need official guidance and your exact fact pattern to draw clean lines. When in doubt, keep a one-sentence "why" note for each inflow and ask a pro to sanity-check the classification.

Do I need a work permit to pay tax in Vietnam (or vice versa)?

Don't treat immigration status and tax status as interchangeable. Your tax obligations can hinge on residency and income facts. Work permits follow immigration and labor rules.

What records should expats keep for Vietnam taxes-and how long should I keep them?

Keep what proves days, income type, and payment trail: a day log, entry/exit evidence, contracts/SOWs, invoices, payment confirmations, bank statements, and FX conversion evidence. Audits often come down to documentation quality. For retention length, follow current Vietnam guidance or your advisor's policy for your situation instead of guessing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Vietnam's 90-Day E-Visa: A Guide for Long-Term Travelers

Treat this like relocation operations, not a quick form fill. Decide your constraints first, then submit. That one sequence removes most avoidable mistakes and keeps your timeline stable.

Ho Chi Minh City Digital Nomad Guide for a 30-Day Move (2026)

Ho Chi Minh City is a strong base if your priority is keeping work momentum while relocating. You get density, plenty of places to work from, and a social scene that can help you settle quickly. It is a weaker fit if your best days depend on calm streets, easy walking, and long stretches of quiet. In practice, Saigon tends to reward people who want convenience and activity more than retreat pace.

How Freelancers Can Legally Avoid Double Taxation With Tax Treaties

Classify the tax problem before you touch a return. If your income is mostly personal service fees across borders, this guide fits. If your issue is C corporation profits and shareholder dividends, you are solving a different problem.