Quick Answer

For most families, a 529 is usually the better choice if the goal is education savings with family-level flexibility. A UTMA fits better when you want an irrevocable gift to one child and broader spending options for that child's benefit. The key factors are control, tax treatment, financial aid treatment, and any cross-border reporting or school-eligibility issues.

UTMA vs. 529: A Strategic Framework for the Global Professional#

If you are mainly saving for education and want to preserve family-level flexibility, a 529 is usually the default. A UTMA can still make sense when you intentionally want an irrevocable gift to one child and want spending flexibility beyond education. Use this decision lens: control, tax treatment, financial aid treatment, and cross-border compliance friction.

| Decision point | UTMA / UGMA custodial account | 529 plan |

|---|---|---|

| Ownership and control transfer | A valid UTMA transfer is irrevocable, and legal title vests in the minor. You act only as custodian until the state-defined handoff. | Beneficiary-change flexibility is explicit: you can change the beneficiary to another family member without tax consequences, and federal law treats that change as not a distribution. |

| Allowed uses | Broad, as long as spending is for the minor's benefit. | Tax advantages depend on qualified education expenses. |

| Beneficiary flexibility | Assets are a gift to that child, with no practical reassign option. | You can change the beneficiary to another family member without tax consequences. Federal law treats that change as not a distribution. |

| Tax handling | Does not carry the same qualified-education tax treatment as a 529, and kiddie tax rules can apply to unearned income. | Earnings are federally tax-free, and generally state-tax-free, when used for qualified education expenses. |

| Financial aid treatment | Older federal formula text applied a 20% student-asset multiplier. Verify current-year FAFSA treatment before planning. | FAFSA includes 529 plans under qualified education benefits. Confirm current aid treatment for your filing year. |

| Cross-border reporting friction | Can be higher when accounts are foreign-held. FBAR can apply if aggregate foreign financial accounts exceed $10,000 at any time in the year. | Verify reporting obligations and local-country tax treatment case by case. |

Control is the real dividing line#

The real tradeoff here is not abstract flexibility. It is whether you are willing to give up control permanently.

With a UTMA, that tradeoff has two parts:

- The contribution is irrevocable.

- The child has legal ownership even before they can liquidate, and full control later follows state law timing.

Those two points drive most downstream consequences. Once you fund a UTMA, you should think of the money as no longer available for a family-level course correction. If one child gets a scholarship, delays school, studies abroad, or simply has a different plan than you expected, the UTMA does not give you much room to redirect assets to a sibling. The account is still that child's property. Your role is administrative, not ultimate.

That is why the control question should come first, before you compare tax features or aid effects. If you know you want family-level flexibility, especially beneficiary-change flexibility within the family, a 529 starts from the stronger position under the rules described here. If you know you want to make a completed gift to one child and you are comfortable with the handoff that comes later, a UTMA can fit on purpose rather than by accident.

In practice, the split is simple:

- If your goal is flexible, family-level education funding across multiple possible beneficiaries, a UTMA is usually a poor fit.

- If your goal is a final gift to one child, and you accept the control handoff timeline, a UTMA can be appropriate.

A 529 is built for the opposite profile. You can reassign the beneficiary within the family if plans change, without tax consequences.

Ask yourself three practical questions before opening anything:

- If your child's education path changes, do you want to decide what happens next, or do you want that decision to be constrained by an earlier gift?

- Are you funding for one named child only, or are you really building a family education pool?

- Will you still be comfortable with the structure when the child reaches the state-law control point, even if your views on spending differ by then?

If your honest answer keeps coming back to family-level flexibility, the 529 is usually doing the job you actually want. If your answer is that the money is meant to belong to that child no matter what, the UTMA may be the cleaner expression of that intent.

Tax and aid are operational, not secondary#

Tax treatment and aid treatment should shape the decision early, not after the account is open. A 529's tax advantage is conditional: qualified use gets federally tax-free earnings and generally state-tax-free qualified withdrawals. A UTMA does not provide that same education-specific shelter, and kiddie tax rules can apply.

That means your first planning step is not just picking an account. It is mapping expected use. If you expect the funds to be used for education and want the account structure to reinforce that goal, a 529 is aligned with the intended use. If there is a real possibility the money may be used for the child's benefit outside education, the broader UTMA use rules matter more, but you are also accepting the different tax profile.

Aid treatment also needs a current-year check. FAFSA guidance includes 529 plans in qualified education benefits, and Federal Student Aid announced 2026-27 FAFSA changes, posted August 15, 2025 and implemented with the 2026-27 launch by October 1, 2025. Treat older formulas, including the 20% student-asset reference, as context only until you verify treatment for your filing year.

That step is easy to postpone and expensive to skip. If aid treatment is part of your decision, do not rely on a blog post you read last year or an old planning memo. Confirm the filing-year treatment that will actually apply when your family reports assets. If you are comparing different ownership and reporting categories, treatment can differ, and those categories should be checked against current instructions rather than memory.

Before you fund either account, gather a small decision file:

- your expected use case for the money

- who needs to control the account over time

- whether aid sensitivity is a real concern for your family

- whether the account will be U.S.-based or foreign-held

- what documents you will need later to support qualified use or ownership treatment

That same confirm-first approach matters even more once you add a non-U.S. residence or foreign-held accounts. For expat families, tax and aid are rarely separate from account administration. The choice of account can affect what you need to track each year, what you may need to report, and which assumptions have to be checked country by country. A structure that looks straightforward in a domestic-only setup can get much less straightforward once account location, local tax treatment, and school eligibility all enter the picture.

Expat compliance checklist#

Before opening either account, run this quick check:

| Check | What to confirm | Record or timing |

|---|---|---|

| Account location | Whether the account is U.S.-based or foreign-held | Save the plan or account opening materials that show where the account is held. |

| Reporting exposure | FBAR filing risk if aggregate foreign financial accounts exceed $10,000 at any point in the year | Review all relevant foreign accounts together, not one balance snapshot. |

| Local-country tax treatment | Local treatment instead of assuming U.S. tax outcomes carry over | Write down the exact issue; if you use an adviser, give them the account type, account location, owner or custodian details, and expected use. |

| School eligibility | Whether a foreign school is an eligible educational institution and participates in a U.S. Department of Education aid program | Verify before the withdrawal and keep the result with your records. |

For most global professionals, that checklist works best as a short document pack rather than a mental note.

For account location, save the plan or account opening materials that show where the account is actually held. That becomes useful later if you are trying to sort out whether the account is foreign-held or simply connected to a child or parent living abroad. Do not assume residence and account location are the same thing.

For reporting exposure, review your full account picture rather than testing one account in isolation. FBAR exposure is tied to aggregate foreign financial accounts, so review all relevant foreign accounts together and check whether the threshold was exceeded at any time during the year. If you wait until year-end and only look at one balance snapshot, you can miss the question you were supposed to be asking.

For local-country tax treatment, write down the exact issue you need to confirm. The point is not to ask whether a 529 or UTMA is "good" abroad in general. The point is to ask how that account is treated where you live. If you use an adviser, give them the account type, account location, owner or custodian details, and expected use. That usually gets you a better answer than a broad, abstract tax question.

For school eligibility, verify before the withdrawal, not after. If you are relying on 529 qualified treatment for a foreign institution, confirm the school's status before you move money. Keep the result with your records so you are not trying to reconstruct the basis for the withdrawal later.

A simple expat workflow looks like this:

- decide which account type fits your control goal

- confirm where the account will be held

- check whether foreign-account reporting could be triggered

- verify local-country treatment

- confirm school eligibility before any 529 withdrawal tied to a foreign institution

That sequence keeps the decision practical. It also helps you avoid choosing an account for one reason and then discovering a reporting or eligibility issue after the money is already in place.

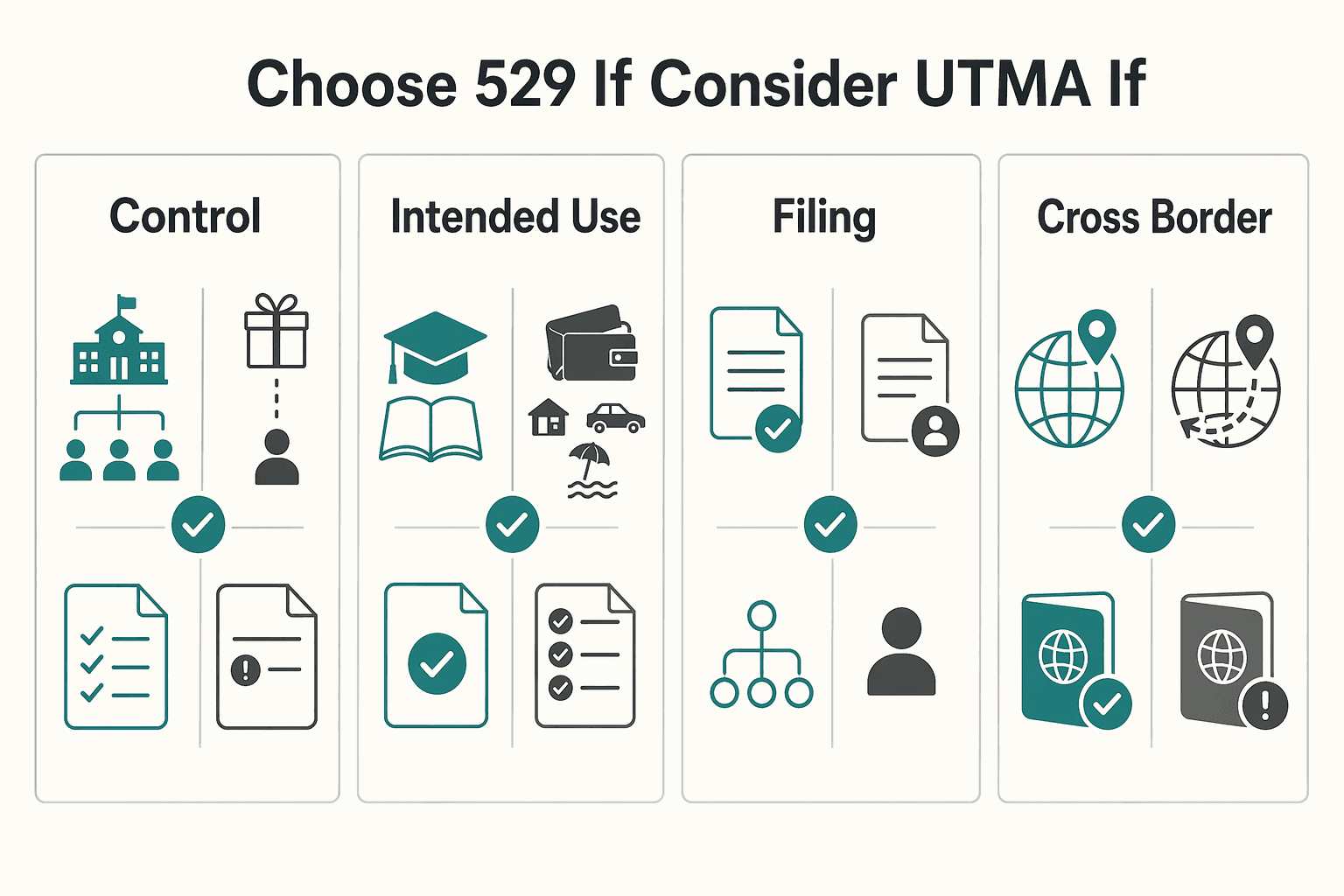

Choose 529 if... / Consider UTMA if...#

For most families, the decision comes down to whether you need family-level flexibility or broad-use flexibility. Choose a 529 if you want education-specific tax efficiency and beneficiary flexibility within the family. Consider a UTMA if you want a true gift to one child, want broad non-education use, and accept irrevocability plus eventual control transfer.

| Step | Focus | What to check |

|---|---|---|

| 1 | Control | Whether you want family-level flexibility or to make an irrevocable gift |

| 2 | Intended use | Mostly education, or potentially broader child-benefit spending |

| 3 | Tax and aid | Aid and tax treatment for the filing year and expected use case |

| 4 | Cross-border | Whether you live abroad or may use foreign institutions |

If you are stuck between the two, do not ask which account is more flexible in the abstract. Ask which one is more forgiving of the way real family plans change. A 529 is usually more forgiving when uncertainty is about who will use the funds or whether one child's plans will differ from another's. A UTMA is more flexible only in the sense that the child's funds can be used more broadly for that child's benefit.

That distinction matters. Families often say they want "flexibility" when they really mean one of two different things:

- flexibility for the parent or family to adapt the plan later

- flexibility for the child's funds to be spent on more than education

Those are not the same. The first points toward a 529. The second points toward a UTMA.

One practical way to decide is to follow this order:

- Start with control: do you want family-level flexibility or to make an irrevocable gift?

- Then test intended use: mostly education, or potentially broader child-benefit spending?

- Then check aid and tax treatment for the filing year and expected use case.

- Then run the cross-border checklist if you live abroad or may use foreign institutions.

In most cases, the practical verdict is simple: if future plans may change, beneficiary flexibility usually matters more than spending flexibility.

If you want a deeper dive, read A Guide to 529 Plans for US Expats.

Before you finalize UTMA vs. 529, test your foreign account reporting risk with the FBAR calculator.

If your savings plan is cross-border, the Gruv tools hub can help you build a next-step checklist before you act.

Frequently Asked Questions

What is the main risk of a UTMA account?

The main risk is loss of control. A UTMA is irrevocable, the child has legal ownership, and full control arrives at adulthood under state law, commonly 18 or 21, but it varies by state. If you want the money to remain part of a parent-directed education plan, that structure may not fit your goal.

Can you open or contribute to a 529 while living abroad?

Treat this as a confirm-first question. The article does not give a universal yes or no for living abroad. Before contributing, check plan enrollment rules, U.S. federal treatment, and local-country tax treatment.

Can you use 529 money at an international university?

Possibly, but this article does not list the eligibility rules for international schools. For a 529, confirm the school's eligibility under current rules before taking a qualified withdrawal. Keep a record of what you checked and when.

Does a UTMA trigger FBAR reporting?

Potentially. FBAR risk can apply when aggregate foreign financial accounts exceed $10,000 at any point in the year. If any accounts are held outside the U.S., review all relevant accounts together and confirm current-year reporting requirements before year-end.

Which is usually better for estate and gift planning?

If your goal is education funding with retained control, a 529 is usually the stronger fit. It lets you keep control and may have high state plan limits plus a potential five-year front-loading strategy. Verify current thresholds before acting.

What happens if your child does not go to college?

With a UTMA, the money remains that child's asset and can still be used for that child's benefit. With a 529, first consider changing the beneficiary to another family member, then verify current tax treatment before taking a non-qualified withdrawal. This is where a 529's family-level flexibility often matters most.

How does the kiddie tax affect a UTMA?

The article does not provide kiddie tax thresholds or mechanics. It does say a UTMA does not offer the same education-specific tax treatment as a 529, and kiddie tax rules can apply to unearned income. For projections, verify current tax rules first.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaefiling.fincen.gov/docs/FinCENFBARHelp.pdftrusted

- fsapartners.ed.gov/knowledge-center/library/electronic-announce...trusted

- fsapartners.ed.gov/knowledge-center/fsa-handbook/2025-2026/appl...trusted

- irs.gov/newsroom/529-plans-questions-and-answerstrusted

- irs.gov/credits-deductions/individuals/eligible-educ...trusted

- legacy.pli.edu/product_files/Titles/123/%2350518_Blattmachr...trusted

- nrc.gov/docs/ML1211/ML121160136.pdftrusted

- secure.ssa.gov/poms.nsf/lnx/0501120205DALtrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

A Guide to 529 Plans for US Expats

**Run a risk-first workflow that protects liquidity, clarifies control, and prices in tax uncertainty before you fund a 529 account.** The goal is simple: choose a safe default you can defend later, and avoid "helpful" moves that create admin chaos when your situation changes.

Custodial Accounts for U.S. Expats: UTMA/UGMA, FBAR, and 529 vs. Trust

Standard financial advice on custodial accounts is a compliance trap for the global professional. Guides written for a domestic audience - with a U.S. address and a financial life contained within 50 states - are not just incomplete for you; they are a direct threat to your financial autonomy. They fail to warn you that many U.S. brokerages may refuse to open an account for a client with a foreign address, or worse, freeze your assets if they discover you've moved abroad. They omit the most critical compliance tripwire of all: the Report of Foreign Bank and Financial Accounts (FBAR).

Create a Freelance Hire Me Page That Qualifies Better Clients

More inquiries are not the goal. You want better inquiries, routed through terms you can actually deliver on. A strong hire me page does two jobs at once: it helps the right buyer raise a hand, and it prevents loose intake, payment confusion, and overpromising once they do. Keep this model in mind: