Quick Answer

Use Ramp when your remote US agency primarily needs tighter spend controls, corporate cards, expense management, travel, accounts payable, and clearer finance-operations visibility, not hiring, payroll, or EOR services. Then support it with a staged operating model: track possible FBAR exposure, document worker-classification and contract-authority controls, and centralize policy, approvals, and monthly reviews so spending, delivery, and hiring stay aligned.

What Does 'Ramping' a Remote Agency Really Mean?#

For a remote US agency, "ramping" starts with a tool-category decision. Pick the wrong category and you create avoidable finance and operations risk. Use this quick matrix to match the product to the job you actually need done:

| Product | What it is actually for | Best fit for a remote US agency | Not a fit when you need |

|---|---|---|---|

| Ramp | Finance operations: corporate cards, expenses, travel, and accounts payable | You need tighter spend controls and clearer finance-operations visibility | Recruiting, employer of record (EOR), payroll, or talent sourcing |

| Remote (Remote.com) | Global HR: contractor management, payroll, and EOR services | You need to hire or pay people across borders with HR workflows | Corporate card and expense controls as your primary problem |

| Remote Ramp (remoteramp.co) | A separate remote workforce solutions site | You are evaluating remote workforce support options and want to compare positioning | A corporate card platform or a staffing-agency marketplace |

| RAMP.Global | Staffing-agency hiring, matching, and management platform | You hire through staffing agencies and want broad agency-network coverage | Internal expense management or company card issuance |

Start with a quick self-check. If your pain is "who spent what, where," start with Ramp. If your pain is "how do we hire or pay this person across borders," start with Remote's global HR stack, with listed pricing separated by Contractor Management, Payroll, and EOR. If your pain is "we need agency partners to fill roles," start with RAMP.Global.

Before you adopt any platform, read the overview and pricing pages and confirm that the core language on the page matches your problem: spend, employment, or staffing-agency matching. That simple check helps you avoid patching core gaps with manual work later. Choose for risk exposure first, then cashflow visibility, then operational scale.

Related: The Best Business Credit Cards for Freelancers.

Stage 1: Build a Bulletproof Financial Foundation#

Work this stage in order. First confirm whether FBAR reporting may apply, then track account values during the year, then verify deadline exceptions before filing.

Follow the sequence in order#

| Step | Action | Key detail |

|---|---|---|

| 1 | Confirm whether FBAR may be required | Check whether a single foreign account maximum value or aggregate maximum value across accounts can exceed $10,000 during the calendar year. |

| 2 | Track account values as the year progresses | Record each foreign account's maximum value as a reasonable approximation of its highest value. |

| 3 | Standardize currency conversion for reporting | Convert balances to USD using the Treasury year-end rate. If no Treasury rate is available, use another verifiable rate and document the source. |

| 4 | Validate filing details before submission | Review FinCEN notices for event-based extensions and filer-type differences. If you have fewer than 25 accounts and cannot determine whether aggregate maximum value exceeds the filing trigger, complete the appropriate per-account FBAR sections. |

Keep that sequence intact. Ongoing value tracking supports threshold checks, and a final deadline check reduces avoidable filing errors.

Treat FBAR as a live control#

If FBAR may apply, track it throughout the year and verify current filing thresholds before filing. Use this process:

- Track each foreign account's maximum value during the year as a reasonable approximation of its highest value.

- Use periodic account statements when they fairly reflect that maximum, and keep the records you relied on.

- Convert non-U.S.-currency balances to USD using the Treasury year-end rate, which is the last day of the calendar year. If no Treasury rate is available, use another verifiable rate and document the source.

- Review aggregate exposure across accounts, not just one account at a time.

- If you have fewer than 25 accounts and cannot determine whether aggregate maximum value exceeds the filing trigger, complete the appropriate per-account FBAR sections.

- Check FinCEN notices before filing because event-based extensions can apply, and deadlines can differ by filer type, including certain signature-authority-only cases.

Check deadline exceptions before you file#

Do a final timing check before submission instead of assuming one universal due date. FinCEN can publish event-based extensions, and certain signature-authority-only individuals may have an extended due date while other FBAR filers keep the standard due date.

Stage 2: Scale Your Team, Not Your Compliance Risk#

Once Stage 1 is stable, hiring drift becomes the next scaling risk. Treat each new role as a worker-classification and tax-presence decision before you treat it as a recruiting decision.

Start with misclassification, not headcount#

For US federal employment tax purposes, the IRS uses a common-law analysis grouped into three categories: behavioral control, financial control, and the relationship of the parties. It is not a single-factor test, and contract wording alone is not determinative.

Use a practical screen: are you buying a defined outcome from an independent business, or are you directing the work in a way that looks like employment? Keep current US labor framing in view. The DOL 2024 final rule took effect on March 11, 2024, rescinding the 2021 rule. A new NPRM announced on February 26, 2026 is not final law.

| Control factor | Lower-risk contractor indicator | Higher-risk indicator |

|---|---|---|

| Behavioral control | You define outcomes and timelines; the contractor controls how work is done | You direct how work is done day to day |

| Financial control | The contractor operates like an independent business in pricing and delivery | The arrangement is managed more like an employee relationship |

| Relationship of the parties | The engagement is clearly scoped and independent in nature | The relationship is open-ended and treated like an internal seat |

| Integration into your business | Work is clearly bounded from your core regular business | Services are a key aspect of your regular business |

Recheck the classification when scope, duration, or management intensity changes. If US federal status is genuinely unclear, Form SS-8 is the IRS path for a worker-status determination.

Watch the dependent-agent PE trigger#

Classification is only the first layer. Dependent-agent PE risk can arise when someone habitually concludes contracts, or habitually plays the principal role leading to contracts your company routinely concludes without material modification. For client-facing roles, set hard authority guardrails:

- Reserve contract authority, pricing approvals, discounts, renewals, scope changes, and termination concessions to named internal approvers.

- Require written internal approval before any client commitment is treated as binding.

- Keep an approval trail showing who reviewed and approved each exception.

The treaty summary here includes an independent-agent exception, but treaty outcomes still vary by jurisdiction pair and covered-agreement notifications. Keep country-specific rules in your rollout checklist and verify them against current official sources before assigning authority or signing workflows.

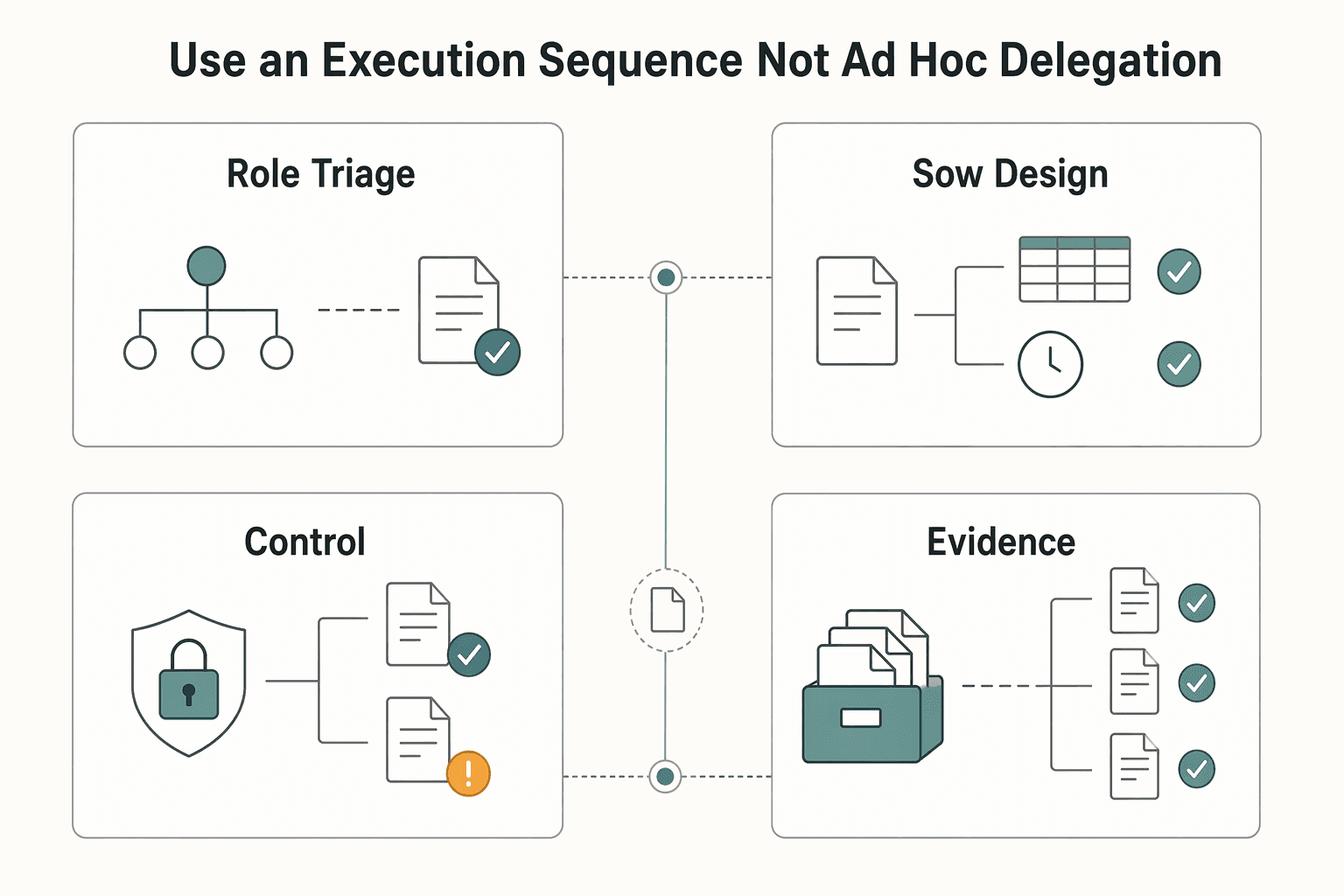

Use an execution sequence, not ad hoc delegation#

Ad hoc delegation is where classification files start to fall apart. Decide the model first, then document it in the same order every time.

| Step | Details |

|---|---|

| Role triage | Decide up front whether the role is project-based or an ongoing operating seat, whether it is core to delivery, and whether it is client-facing. |

| SOW design | Define outcomes, acceptance criteria, timeline, and payment terms. Avoid prescribing how work is performed when you are using a contractor model. |

| Contractor agreement controls | Include independent-contractor status, tax-responsibility language, confidentiality/IP terms, and no-authority-to-bind language. |

| Documentation habits | Keep the triage memo, SOW, agreement, invoices, and approval records together for audit readiness. |

Use the same order every time so your classification file stays readable.

If you use Ramp, condition-based approval chains and action logs can support that documentation trail as control evidence. They do not determine legal compliance on their own.

Contractor vs EOR: when to escalate#

The practical question is not which label you prefer. It's when the facts have moved far enough toward employment that you should escalate to an EOR structure.

| Criteria | Contractor lane | EOR lane |

|---|---|---|

| Work pattern | Scoped, outcome-based engagement | Ongoing role that functions like employment |

| Management model | Limited direction focused on deliverables | Day-to-day managerial direction by your team |

| Business criticality | Non-core or bounded support work | Core delivery role with sustained operational dependency |

| Client-facing authority risk | No effective authority over binding terms | Elevated authority/commitment risk that needs tighter employment structure |

| Employment administration need | Not the primary requirement | Need payroll and regulatory administration through a legal employer |

| Jurisdiction check | Verify local contractor-classification rules against current official sources before using this lane. | Verify local employment and EOR requirements against current official sources before using this lane. |

An EOR is a third-party legal employer that handles employment administration while you keep managerial control. Use it as an escalation path when the facts increasingly match employment reality.

For a step-by-step walkthrough, see Best Corporate Debit Cards for Global Spending in Small Teams. Before you onboard another contractor, pressure-test your classification assumptions with this W-2 vs 1099 calculator.

Stage 3: Integrate Operations into a Single Growth Engine#

By this stage, fragmented execution becomes the bottleneck. Spending, delivery, and hiring should operate as one loop. If they stay disconnected, decisions turn reactive, and reactive fixes do not scale.

Spend controls should show where delivery is straining. Delivery signals should show whether a cost protects quality or only patches a process gap. Hiring decisions should come from that combined evidence.

Put policy in one controlled place#

If policy lives across chat threads and scattered docs, consistency drops fast. Keep it in one searchable place with clear ownership and versioning.

| Spend category | Control method | Owner | Enforcement action |

|---|---|---|---|

| Software subscriptions | Preapproved vendor list, named card or reimbursement path, and an internal policy limit defined before rollout. | Finance owner plus tool owner | Pause renewal, reject new vendor request, require owner review before reactivation |

| Client project costs | Project code required, receipt or invoice attached, and an internal policy limit defined before rollout. | Delivery lead | Hold reimbursement or charge review until project tag and client allocation are corrected |

| Contractor services | Approved SOW or agreement on file, project or department tag, and an internal policy limit defined before rollout. | Hiring manager plus finance | Block payment until scope, approver, and classification records are complete |

| Marketing and business development | Campaign or channel tag required, with an internal policy limit defined before rollout. | Growth lead | Route to exception review if uncoded or outside current campaign approval |

| Travel and team spend | Preapproval and business purpose required, with an internal policy limit defined before rollout. | Department manager | Reimburse only after missing approvals or documentation are cured |

Standardize the core rules, owners, and version history, then let functions or client accounts add supplemental guidance inside that shared structure. Recurring outsourced work can be an early hiring signal, so review it deliberately.

Let spending trigger hiring decisions#

Review recurring outsourced work in three passes:

- Detect recurrence. Flag repeat vendors, repeat reimbursement types, or repeat project spend tied to the same work.

- Validate operating effect. Check whether the spend protects delivery quality or mostly patches a process gap, using project notes, rework volume, delays, and QA signals. If quality varies widely, fragmented execution may be part of the problem.

- Choose a response. Automate repetitive low-judgment work, expand contractor coverage for variable specialized demand, or create a role when work is recurring, core, and needs daily coordination.

Before any new hire, contractor expansion, or internal transfer touches live delivery, add a lightweight certification gate so readiness is defined before the work starts.

Build the minimum architecture and run a monthly cadence#

You do not need a sprawling stack here, but you do need a minimum operating setup: a policy hub plus the core systems used for spending, delivery, and staffing. Keep shared identifiers such as vendor or payee, worker or owner, client or project code, spend category, and policy version consistent so exceptions stay traceable.

| Monthly check | Review focus |

|---|---|

| Spend review | Review spend by category, client or project, and worker type. |

| Exceptions | Inspect exceptions, uncoded transactions, and repeat manual fixes. |

| Delivery linkage | Compare outsourced categories against delays, QA notes, and rework pressure. |

| Policy updates | Update the policy hub, then broadcast updates and capture acknowledgment. |

| Structured intake and QA | Route unusual requests through a structured intake and QA loop, and keep request, approver, rationale, and effective date together. |

Run that review monthly.

If updates are not centralized and auditable, you lose traceability on who saw what and which rule was in effect. Then fixes arrive only after cost and delivery impact are already real.

You might also find this useful: The Best Expense Management Software for a Remote Team.

Your Next Move: Scale with Confidence, Not Anxiety#

Use the same three-stage framework this week, but make it concrete: one owner per stage, one action per stage, and a named owner for every legal or tax question that still needs verification.

For financial setup, lock one policy path your team can follow consistently. For hiring risk controls, treat guidance as informational, not binding on its own, and verify applicable statutes, regulations, and current effective dates before you standardize decisions. For system integration, treat your spend and expense tooling as part of your operating process, not as a substitute for legal or tax review. The material here does not support Ramp-specific product or compliance claims, so verify vendor scope in official documentation before you rely on it.

This week, do three things:

- Stage 1: Publish your spend-policy baseline: owner, approval flow, documentation requirements, and exception path. Record any reporting trigger that still needs confirmation from current official sources.

- Stage 2: Open a pre-offer risk note for each cross-border role: open classification questions, potential local-presence questions, and payment or tax ownership follow-up. Record any reporting trigger that still needs confirmation from current official sources.

- Stage 3: Connect spend review to month-end close, and block approvals when required transaction evidence is incomplete.

Stay in optimization mode when the problem is operational execution. Escalate to specialist legal or tax review when cross-border hiring may affect worker status, local-presence risk, or reporting obligations and you cannot confirm the answer in current official sources.

We covered this in detail in How to Use Brex for a Venture-Backed Startup with a Remote Team. If you want to replace fragmented payment workflows with a simpler operating stack, review Merchant of Record options.

Frequently Asked Questions

How should you tell a spend tool apart from a hiring or EOR service?

Tell them apart by matching the product's official documentation to the problem you need solved, such as spend control, employment administration, or staffing-agency support. The FAQ says scope assumptions for Ramp, Remote, and EOR-style support should be treated as unverified until current official terms confirm them.

What should you lock down before you issue cards or approve reimbursements?

This article does not verify a universal checklist for cards or reimbursements. Define the controls in your internal policy, including owner, approval flow, documentation requirements, and an exception path, then verify any legal requirements in current official sources.

Who should own receipt capture, policy enforcement, and month-end review?

This article does not verify one ownership model for receipt capture, policy enforcement, and month-end review. Assign clear owners in policy, keep versioning and accountability visible, and confirm legal responsibilities against current source regulations.

What is the fastest compliance checklist for cross-border hiring?

Use a counsel-reviewed checklist, because this article does not verify jurisdiction-specific cross-border hiring rules. At minimum, review worker classification, local-presence questions, and payment or tax ownership before onboarding. Track any filing triggers that still need confirmation from current official sources.

How do you verify legal references before updating policy?

Start with official sources. For US items, confirm you are on a .gov domain with a lock icon or https:// before relying on the page. Check effective dates every time, because applicability can change over time.

Does software remove your legal obligations if you automate approvals and receipts?

No. The article says automation supports process and documentation, but it does not change your legal obligations or determine legal compliance by itself. Verify legal rights and responsibilities in current source regulations before relying on policy updates or automated workflows.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ada.gov/law-and-regs/design-standards/1991-design-st...trusted

- azdot.gov/sites/default/files/2019/06/adotsystemwidera...trusted

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- courts.ca.gov/documents/cfac-20230627-materials.pdftrusted

- ddot.dc.gov/sites/default/files/dc/sites/ddot/CTR%20Guid...trusted

- dol.gov/agencies/whd/flsa/misclassification/rulemakingtrusted

- federalregister.gov/documents/2024/01/10/2024-00067/employee-or-...trusted

- fincen.gov/reporting-maximum-account-valuetrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

The Best Business Credit Cards for Freelancers

Pick for reliability first. For a freelancer, the right business card is usually the one that keeps recurring bills moving, keeps records clean, and avoids extra costs when income swings from month to month. Rewards still matter, but they sit on top of those basics. They do not replace them.

The Best Expense Management Software for a Remote Team

If you are choosing the **best expense management software for a remote team**, treat it as an operating decision, not just a receipt-tool purchase. You need a setup that shows money in, money out, approvals, reconciliation status, and potential risk signals early enough to act.