Quick Answer

Start by assigning one named owner per control and treating evidence retrieval as a release gate. In this usa patriot act fintech context, account opening should stay blocked until the Section 326 CIP decision is complete and logged, and any Section 314(b) exchange should show Treasury notice status, purpose, scope, and approval path. Keep SAR and EDD handling in a fixed order, then test live cases to confirm decisions, timestamps, and access history can be pulled without cleanup.

How USA PATRIOT Act Duties Are Divided in a Bank Partnership Model#

The tension is straightforward: you need fast onboarding and payments growth, but your controls still have to hold up under review. In that setting, weak controls are not just a back-office problem. They can shape day-one product choices such as what data you collect, when activity is paused, and how escalations are documented.

Section 314(b) is one example of formal coordination in this area. It permits financial institutions that provide notice to Treasury to share information with one another to identify and report activity that may involve money laundering or terrorist activity. A concrete participation checkpoint is submitting notice through the Section 314(b) Certification process with the required information.

Policy attention on bank-fintech partnerships is visible too. A House Financial Services field hearing on July 12, 2024 focused on these third-party relationships. Public comments on bank-fintech arrangements argue that compliance risk can increase when third parties handle significant lending activities. Operational resilience matters as well. Payment processor outages can leave merchants unable to accept electronic payments.

This article gives you a practical path. You should:

- Decide where responsibilities and applicable obligations sit across your entity and partner-bank relationships before adding features that increase compliance load.

- Assign clear ownership for core controls and information-sharing decisions.

- Keep audit-ready records from day one so reviews rely on evidence, not memory.

This is an operational explainer, not legal advice. Exact obligations can vary by market, regulator, and partner program, so confirm scope with legal counsel and compliance partners before launch.

For a step-by-step walkthrough, see A Deep Dive into Florida's Money Transmitter License Rules.

Start With the Terms That Drive Real Decisions#

Start by narrowing the term map, not widening it. If a term does not point to a specific legal source, a named owner, and one retrievable evidence artifact, it is too vague to support a launch decision.

Start with the exact PATRIOT Act term in scope#

The first term to isolate is Section 314(b), not the entire statute used as a catchall. FinCEN describes Section 314(b) as permitting financial institutions, after notifying Treasury, to share information to identify and report activity that may involve money laundering or terrorist activity.

That moves the discussion from abstract policy to proof. A concrete checkpoint is whether someone can show that notice was submitted through the Section 314(b) Certification process with the required information, and retrieve that record on demand. Also verify document status before relying on older procedures, because FinCEN's 314(b) resource page includes materials marked "Rescinded December 2020."

Put BSA and FBAR in the right box#

Once you separate the PATRIOT Act term, put BSA and FBAR in the right lane. In the cited materials, FinCEN frames the Bank Secrecy Act as the statutory basis for FBAR requirements, which is different from 314(b) information sharing.

| Scenario | Instruction |

|---|---|

| Certain signature-authority-only individuals whose FBAR deadlines were previously extended | Due date: April 15, 2027 |

| All other individuals with an FBAR filing obligation | Due date remains April 15, 2026 |

| Maximum account value | Record in U.S. dollars and round up to the next whole dollar |

| Computed value is negative | Enter 0 in Item 15 |

| Filer has fewer than 25 accounts and cannot determine whether aggregate maxima exceeded $10,000 | Item 15a ("amount unknown") is the checkpoint to document |

If you want a cleaner ownership model for recordkeeping and repeatable evidence handling, see Bank Secrecy Act fintech decisions. The discipline is simple: each recurring term maps to one operational owner and one artifact you can actually retrieve.

For execution, keep these BSA-linked FBAR mechanics explicit:

- Certain signature-authority-only individuals whose FBAR deadlines were previously extended have a due date of April 15, 2027.

- For all other individuals with an FBAR filing obligation, the due date remains April 15, 2026.

- Maximum account value is recorded in U.S. dollars and rounded up to the next whole dollar (for example, $15,265.25 becomes $15,266).

- If a computed value is negative, enter

0in Item 15. - If a filer has fewer than 25 accounts and cannot determine whether aggregate maxima exceeded $10,000, Item 15a ("amount unknown") is the checkpoint to document.

Operationally, when a control depends on a FinCEN instruction, your evidence pack should include the exact document and the specific field or step your team followed.

Teams often miss this. FinCEN's FBAR e-filing guidance states a submission can be rejected when a required element is not recorded, so weak evidence quality becomes an execution failure. One scope boundary matters. This section does not define or test CIP, KYC, AML, SAR, or EDD, so do not pull those terms in here without separate approved grounding.

Treat this as a launch gate. If your team cannot name the owner for a term and produce the supporting artifact immediately, pause release. A named owner plus a retrievable evidence artifact is the minimum standard.

Decide Your Regulatory Position Before You Add Features#

Decide feature ownership before build starts, because unclear ownership at launch can become a control failure, not just a paperwork issue. Set the operating position first and treat implementation as downstream.

Use one working label per feature, such as direct entity, bank-program fintech, or hybrid split model. Keep labels as internal decision tools, then validate with counsel and partner compliance teams. A practical checkpoint is retrieval. Can you pull the current owner, approval trail, and governing agreement reference immediately?

Keep the decision record in three distinct internal layers so oversight and execution stay separate:

- Key regulators and oversight

- Current regulatory framework assumptions

- Day-to-day AML/CFT and sanctions control execution

The middle layer is where teams can drift. If the FTC Safeguards Rule may apply, state that assumption clearly and confirm it against the rule text before launch. The FTC describes the rule as applying to financial institutions under FTC jurisdiction, notes the rule text as the primary reference point, and outlines key compliance questions for obligations review. It took effect in 2003, was amended in 2021, and was further amended in 2023 to require reporting of certain breaches and security incidents, with notification requirements effective in May 2024.

Keep the decision log checklist intact:

- Feature or product surface and selected model label

- Legal-entity roles and partner roles

- Named owners for control execution and escalation

- Governing contract artifact and version

- Open perimeter questions for counsel with target decision dates

- Latest sign-off record and timestamp

For each line item, include retrieval handles: named owner, approval record, and contract or governing document reference. This helps make the log audit-ready evidence rather than a planning note.

If responsibility is marked "to be finalized" while work continues, stop release until ownership is current. A missing current responsibility log is a launch gate failure. For adjacent process-discipline examples, see Taxes in Germany for Freelancers and Expats, How to Automate Your Freelance Tax Preparation, and What Is FinCEN for Freelancers and FinTech Users.

Map PATRIOT Act Sections to Your Product Surfaces#

Use this map as a release gate, not a research note. If a feature is tagged to one of these sections and you cannot retrieve verified legal text, a named owner, and a live escalation path, treat the mapping as unvalidated and do not ship that change.

Your model decision from the prior section tells you who owns the question, not whether the section mapping is validated. Keep this table provisional until legal sources are verified.

Use current evidence status, not stale confidence#

Current evidence status is the core issue here. Verified substantive legal text for Sections 311, 312, 314(b), 326, and 359 requires review of the official statutory text and counsel-confirmed interpretation. Implementation topics like "case review procedures" or AML software planning should be grounded in verified legal text rather than product-feature overviews.

So keep the mapping visible, keep it provisional, and require verification before release. A section label without source validation should be treated as a control risk.

Keep each row operational#

Each row should work like a repeatable operating instruction: trigger, accountable owner, required artifact, escalation path. Clear role assignments can make retrieval and handoffs easier across product, legal, and partner teams. For accountability discipline, see The Role of the BSA/AML Compliance Officer in a U.S. FinTech Company.

| Section | Operational trigger | Owner | Required evidence | Escalation point |

|---|---|---|---|---|

| Section 326 | Any feature, rule, or compliance decision your team maps to this section, with scope pending legal confirmation | Product lead plus compliance lead | Verified official legal text, counsel interpretation note, approved control spec version | Counsel and partner compliance reviewer |

| Section 314(b) | Any feature, rule, or compliance decision your team maps to this section, with scope pending legal confirmation | Compliance lead plus data-governance owner | Verified official legal text, purpose memo, approved decision record | Privacy counsel and executive risk owner |

| Section 311 | Any feature, rule, or compliance decision your team maps to this section, with scope pending legal confirmation | Risk lead plus business owner | Verified official legal text, risk memo, dated sign-off record | Compliance committee or equivalent |

| Section 312 | Any feature, rule, or compliance decision your team maps to this section, with scope pending legal confirmation | Partner manager plus compliance lead | Verified official legal text, due-diligence packet, approval record | Partner compliance and counsel |

| Section 359 | Any feature, rule, or compliance decision your team maps to this section, with scope pending legal confirmation | Legal owner plus product owner | Verified official legal text, decision memo, release approval log | General counsel and release approver |

The practical test is retrieval speed. Can you open the exact artifact, confirm the current version, and identify who owns the next decision? If not, the row is decorative. A screenshot, an old slide, or "per counsel" without a dated memo is not release-grade evidence.

Common failure modes to watch for: section tags spread through tickets before evidence is validated, and ownership gets assigned to team labels instead of named people. Both patterns can slow escalation, including partner-bank review cycles.

Run the pre-release checkpoint the same way every time#

Before each release cut, run one checkpoint: every row must include document ID, version date, accountable owner, and latest approval timestamp. That is the minimum for a current, attributable, reviewable section map.

Keep implementation material separate from legal authority. Secondary materials can support case-review design and operational handoffs, but they should not be the only basis for section mapping decisions.

Under delivery pressure, teams may defer missing fields to "next sprint." Treat that as a release failure. Missing document IDs, generic owners, stale version dates, or unretrievable approval timestamps are launch blockers and evidence-quality gaps.

Build a Defensible Account Opening Checkpoint#

A defensible account-opening checkpoint can be defined as one where no account opens until the Customer Identification Program decision is complete and logged. The legal anchor is specific to covered broker-dealers. The CIP rule implementing Section 326 of the USA PATRIOT Act requires reasonable procedures to verify the identity of a person seeking to open an account, maintain records of the information used to verify identity, and check government-provided terrorist lists. The cited final rule also excludes brokers or dealers registered solely because they effect transactions in securities futures products.

Keep product design choices separate from legal claims. Define required onboarding and verification inputs in your program policy, and tie compliance controls to documented identity-verification, recordkeeping, and list-check decision logic.

Use explicit decision states#

Ambiguity here can create audit risk, so use clear states and avoid soft-approved language in product copy and ops notes.

| Decision state | Definition |

|---|---|

| Approved | Program-required data is present, required verification checks are complete, and the decision record is written. |

| Pending evidence | Account request exists, but required input or verification evidence is missing. |

| Rejected | Checkpoint failed under policy and cannot proceed without a new submission. |

| Manual review | Data is present, but a human decision is still required before approval. |

Bind each state to product permissions. Pending evidence and manual review should not allow activation steps that depend on completed identification.

Capture evidence like you will defend it later#

Do not store only the final status. Keep an evidence packet that shows why the status exists and when it should be revisited under your policy.

- What was collected: information used for identity verification.

- What was checked: identity-verification and list-check steps, execution time, and result.

- What was decided: decision owner, timestamp, and approval method, automated or human.

- When to recheck: policy-based trigger for refreshing time-bound evidence.

In your control review cadence, sample recent approvals and confirm each record contains these elements. Missing metadata is a control gap because you cannot reconstruct why the account was opened.

When conversion pressure rises, keep one tradeoff rule in writing: do not remove CIP controls to move faster. Improve user guidance, tighten form error handling, and staff manual review queues instead. Treat proposed rules as proposed, and verify legal-research conclusions against an official Federal Register edition when legal certainty is required.

Set SAR and EDD Escalation Rules Early#

Set SAR and EDD escalation rules before alert volume spikes, or case handling will drift and your audit trail will weaken. Name decision owners early, define required case-file artifacts, and keep the process consistent when speed pressure rises.

Keep the policy framing anchored to current FinCEN guidance, and update it when guidance changes. The operational goal is consistency: same fact pattern, same escalation path, same documentation standard.

Tie SAR to observable behavior#

Escalate from observed activity and documented facts, not instinct or shorthand labels. For workflow ownership, keep identity-and-expected-use records distinct from monitoring-and-escalation records when activity no longer aligns with the baseline.

Keep ownership explicit in every escalated case: one accountable owner, one backup, and a file that records what was seen, when, by whom, and why the case was escalated or closed. At minimum, capture the alert or case ID, timestamp, owner, records reviewed, and rationale. If a second reviewer cannot reconstruct the decision later, the file is incomplete.

Avoid broad labels like "unusual" or "high risk" without tied evidence. Those labels do not show what contradicted expected activity or why the case moved forward, and they make threshold tuning harder under queue pressure.

If a case may require inter-institution information sharing, require a 314(b) checkpoint before anything is sent. Section 314(b) permits participating financial institutions to share information to help identify and report activity that may involve money laundering or terrorist activity. Participation also includes notice to Treasury through the 314(b) certification process. Your file should show whether 314(b) was considered, whether notice or certification was in place, and the purpose of the proposed exchange.

Start EDD with a documented handoff process#

Start EDD with a documented handoff, not chat fragments or memory. Keep the checklist simple. Common case-file items include:

- Risk question associated with the escalation

- Additional evidence requested and what was received

- Remaining contradictions or gaps

- Final decision and next review condition if the account stays active

The risk question can define scope. Evidence tracking should show both what was requested and what was actually received, including partial, stale, or missing responses. Contradictions and gaps should be stated directly, with clear treatment in the disposition.

If you need a repeatable operating model for higher volume, Enhanced Due Diligence in FinTech That Holds Up Under Real Case Volume goes deeper on evidence design and staffing tradeoffs.

Also recheck older 314(b) references before relying on them. FinCEN's current 314(b) materials explicitly note rescission of at least one prior administrative ruling (December 2020), so stale templates or analyst notes are a governance risk.

Keep escalation order fixed and review it on a recurring cadence#

Use one fixed sequence: alert triage, analyst review, escalation decision, record retention, then post-incident tuning. A fixed order keeps cases evidence-led and makes queue pressure easier to manage without changing standards.

Run recurring internal quality reviews to confirm similar fact patterns are handled consistently and closed files include required artifacts. When queues grow, do not weaken escalation gates. Increase reviewer capacity, improve triage quality, and reduce alert noise.

Sample recently closed files and confirm a consistent minimum record every time: case ID, owner, rationale, evidence log, disposition, retention location, and any 314(b) checkpoint used for external sharing. If you cannot verify that an external exchange was covered by Treasury notice or certification and tied to the permitted purpose, pause that sharing path until the gap is fixed.

That same documentation discipline matters in other compliance workflows. For a related onboarding and escalation topic, read What Is a Politically Exposed Person and How to Decide Next Steps.

Use Section 314(b) Without Creating Privacy Exposure#

Treat Section 314(b) as a narrow coordination lane, not a blanket reason to circulate customer data. In practice, define the AML or counterterrorism purpose first, then share only what that purpose requires through controlled internal processes.

This is a control choice to make now, not after policy changes. Bank-fintech data-transfer arrangements can be governed by different legal frameworks, and rule changes can create confusion or conflicting incentives. Your process should work under current conditions without assuming future expansion.

Set internal gates before sharing#

Before any exchange, require a short internal check so scope stays tight:

| Gate | Required action |

|---|---|

| AML/counterterrorism objective | State the specific AML/counterterrorism objective and tie it to a case record. |

| Minimum data elements | Identify the minimum data elements needed for that objective. |

| Decision owner and approval | Assign a decision owner and approval step before transmission. |

| Channel control | Use approved channels and avoid informal workarounds. |

| Internal record | Record what was shared and why as an internal control. |

| Scope expansion | If scope starts expanding mid-case, pause and reapprove rather than adding fields ad hoc. |

Keep financial-crimes and privacy review in the same decision#

Do not separate financial-crimes urgency from privacy review. Bank-fintech data-transfer arrangements are often subject to different regulatory requirements, and banks remain responsible for both AML and data-privacy compliance in partnerships. Treat that as an operating signal: review both in one decision path.

Practical exposure can include nonpublic personal information. Core identity data collected for CIP includes name, date of birth, address, and TIN or SSN. Keep sharing tightly bounded to the stated purpose so speed in financial-crimes response does not create avoidable privacy risk.

Related reading: Use the Three-Act Structure to Improve Proposals and Pitches.

Handle Cross-Border and Partner-Bank Risk Edges#

Treat higher-risk cross-border corridors as launch-gated programs, not speed-driven rollouts. If product, compliance, and partner-bank owners cannot document exposure labels, decision ownership, and escalation paths, pause launch.

This caution is operational, not theoretical. Bank customer identification controls must be risk-based and should match each bank's business model, and CIP alone does not satisfy a bank's broader BSA obligations. Regulatory posture can also tighten partner-bank access in some higher-risk sectors (for example, crypto-related activity), so do not assume one reusable template across every country or partner program.

Map exposure labels to real product paths#

Start with a product-flow map, then test where higher-risk partner-bank exposure could appear across onboarding and account-opening points. For lending flows, treat account opening as the point where an enforceable loan agreement is in place, and do not treat denied applicants as CIP customers. Use these labels as internal triage only, and confirm program-specific treatment with partner banks and qualified counsel.

| Product path | Exposure label to test | Why this path needs extra review |

|---|---|---|

| Corridor with multiple institutions touching funds flow through partner rails | Candidate label (confirm classification) | Multi-party handoffs can make ownership and escalation less clear. |

| Model where another party may route activity through your bank relationship | Candidate label (confirm classification) | Oversight can become harder to evidence across parties and controls. |

| High-touch cross-border client servicing model | Candidate label (confirm classification) | Relationship complexity can require tighter escalation and review. |

Compare domestic and cross-border launch burden#

Domestic, lower-complexity onboarding may be simpler to coordinate. In practice, cross-border corridors can need more partner alignment, more review steps, and tighter escalation handling before and after go-live.

For higher-risk corridors, set one internal go-live gate as an operating control, not a legal standard:

- Documented controls by corridor and partner role, with named owners.

- Staffed escalation coverage, including backup decision owners.

- Tested incident-response process with written outcomes.

- Launch memo listing open legal or policy questions and closure owners.

Run a pre-launch verification and an early post-launch review. If pressure rises, add review capacity or narrow rollout scope instead of weakening the gate.

Translate Controls Into Product and Ops Controls#

If a control does not change product behavior or leave a durable record, it can break down when pressure rises. Turn each compliance decision into a product state change with an audit trail to reduce the risk of funds moving while status is still unclear.

| Field | Description |

|---|---|

| request_id | Reused across records |

| provider_reference | From a screening or verification provider |

| decision_state_before | Decision state before |

| decision_state_after | Decision state after |

| decision_reason_code | Plus analyst note for manual actions |

| decision_actor | Person, rule, or service account |

| ledger_posting_id | When funds are booked |

| reconciliation_export_id | When records are exported |

Map sanctions obligations to explicit decision states, then bind each state to allowed actions, for example: pending, approved, restricted, rejected, escalated. When an account is restricted, keep release actions blocked until a documented approval moves it to a releasable state. This aligns product behavior with OFAC transaction controls and asset-freeze expectations under U.S. jurisdiction.

Build a traceable chain from intake through reporting so you can demonstrate the adequacy of the compliance program during review. Example internal fields can include:

request_idreused across recordsprovider_referencefrom a screening or verification providerdecision_state_beforeanddecision_state_afterdecision_reason_codeplus analyst note for manual actionsdecision_actoras person, rule, or service accountledger_posting_idwhen funds are bookedreconciliation_export_idwhen records are exported

Consider protecting the chain during retries and callbacks by preventing duplicate actions and preserving the final approved state after closure.

Before release, use a risk-based checkpoint: assess controls against your products, services, customers, entities, transactions, and geographic locations, and document gaps.

Treat enforcement exposure as a governance trigger. OFAC's Economic Sanctions Enforcement Guidelines (final rule issued November 9, 2009) state that enforcement outcomes consider factors including the adequacy of the compliance program. Civil penalties for apparent violations may be as much as $250,000 per violation or twice the transaction amount, whichever is greater.

Account for current fintech conditions in control design: lower entry costs can come with higher legal-risk exposure, including liability, cybercrime, and taxation risk. If those risks rise alongside sanctions-control weaknesses, consider pausing affected flows, reconciling the decision chain, and restarting only after written sign-off.

Related: Money Transmission Modernization Act and State Licensing Decisions.

Keep an Audit-Ready Evidence Pack From Day One#

An audit-ready evidence pack turns your event trail into records your team can retrieve quickly and trust under pressure. If you cannot assemble a complete case file quickly, treat that as a control gap.

| Evidence type | Minimum contents |

|---|---|

| Customer identification and due-diligence records | Minimum customer-identification data collected before account opening, tied to a stable case trail with decision history and reviewer identity. |

| Escalation decision logs | Timestamps, rationale, escalation path, and final disposition. |

| Policy versions | Effective date, approver, and change summary. |

| Training acknowledgments | By role and completion status. |

| Exception approvals | Scope, expiry, and approver. |

| Access history | Records of who accessed nonpublic personal information (NPI), when, and why. |

Define one minimum pack and use it consistently. Assign an owner for each evidence type and set internal retrieval targets your team can actually meet.

For Section 314(a) requests, document who receives FinCEN's bi-weekly notifications, who runs searches, and who submits positive-match responses within the two-week window.

Capture each 314(a) request's posting date, identifying details, and search scope. That scope covers the preceding 12 months for accounts and the past 6 months for covered non-account transactions. Record whether a response was filed or no reply was required after a no-match search.

Treat Section 314(a) output as investigative lead information only, and document any subpoena or other legal-process follow-up separately.

Run retrieval drills on one recent case and one older case, verify chain completeness from intake through final reporting, and log retrieval time.

Consider a recurring attestation signed by ops and compliance leads confirming controls are active, not just documented. Missing logs are a red flag, and missing sign-off should trigger follow-up.

Keep a known-unknowns register for perimeter questions and pending legal interpretations. Track owner, next decision date, interim control, and impact if interpretation changes.

Use one operating rule: when uncertainty rises, increase evidence discipline early instead of waiting for a crisis.

Execute a 30/60/90 Day Buildout for a Lean Team#

Treat this 30/60/90 plan as an internal execution cadence, not a statutory timer. Do not advance a phase until controls are validated in practice and evidence is retrievable without cleanup.

If you need a lightweight way to make manual back-office steps repeatable, the same discipline used in automating routine operations applies here. Assign an owner, define the record, and verify the output before you scale it.

Exact obligations can vary by market, regulator, and partner program, so confirm scope before launch and tie each term to one accountable owner and one retrievable record. In practice, anchor onboarding to Section 326 CIP requirements, including TIN handling before approval, and keep Section 314(a) search-response records and Section 314(b) sharing decisions tightly scoped and logged.

| Phase | Build focus | Launch checkpoint |

|---|---|---|

| Days 1-30 | Finalize scope decisions, assign control ownership, baseline Section 326 CIP onboarding controls, and define evidence capture in your internal plan | Verify onboarding cases are traceable from decision to one retrievable record |

| Days 31-60 | Operationalize escalation and information-sharing procedures in your internal plan | Run a test scenario and confirm sharing and escalation decisions are tightly scoped and logged |

| Days 61-90 | Automate evidence-pack assembly, run a mock review, and close priority control gaps | Complete a mock request with records that are already retrievable |

The table only works if your gates are strict. In the first 30 days, test whether a reviewer can pull an onboarding case and see the decision and retrievable record tied to it. By day 60, your sample scenario should show that Section 314(a) search-response records and Section 314(b) sharing decisions are logged end to end. By day 90, the mock request should confirm your evidence pack is usable without cleanup.

Keep each phase gate lightweight but strict: record pass or fail, owner, and retrievable evidence for the sampled case. If your team cannot immediately name the owner and evidence artifact for a compliance label, treat that gap as a launch blocker. If that packet is not ready during the review meeting, the phase is not complete.

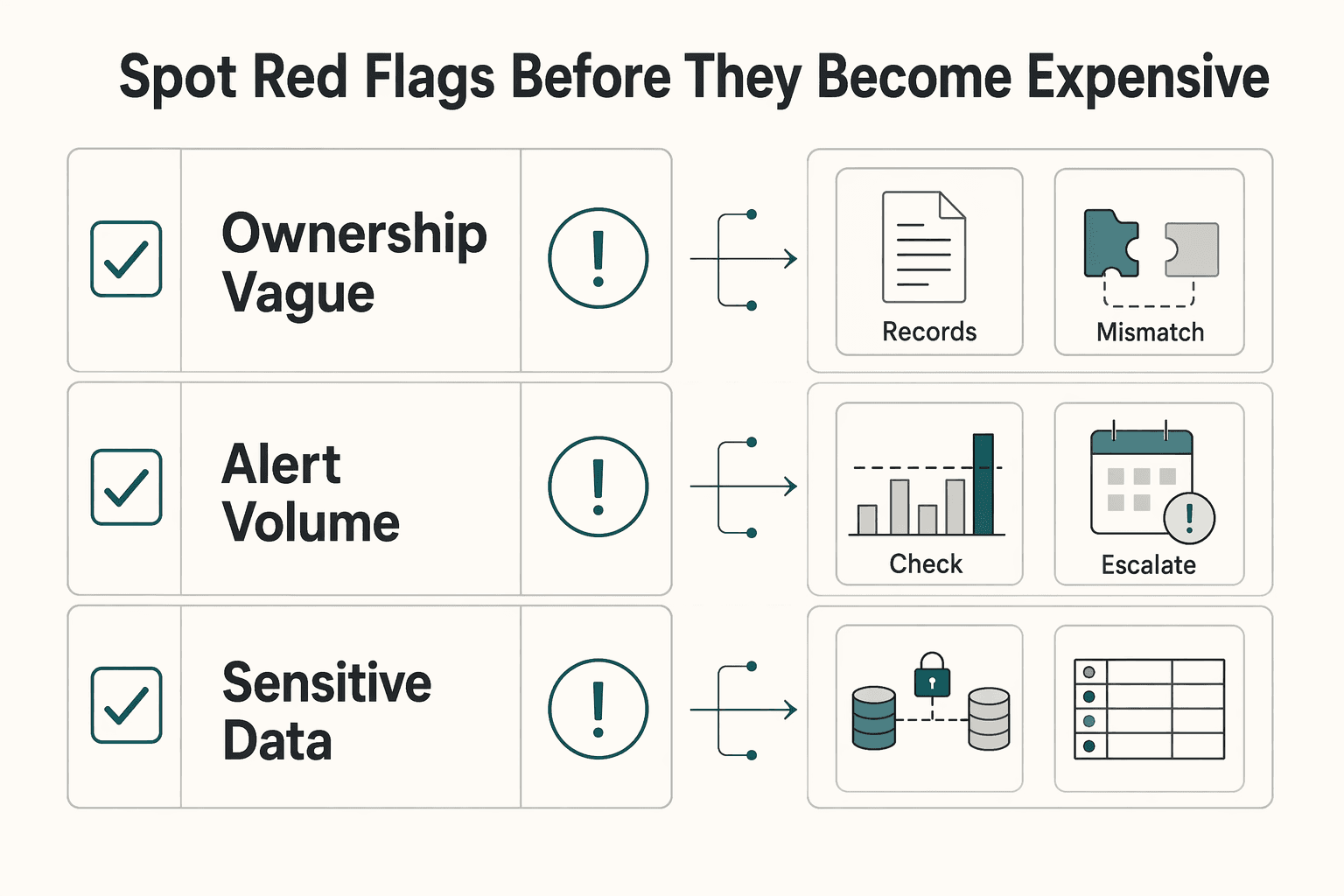

Spot Red Flags Before They Become Expensive#

Costs can rise quickly when ownership is unclear, alerts keep aging, and sensitive data moves without a clean record. Treat those as immediate operating risks, not minor process issues. If you cannot name the owner and retrieve the evidence quickly, treat the control as not ready.

| Red flag | Immediate response | Proof check |

|---|---|---|

| Ownership is vague between teams | Use an owner register for each key control: primary owner, backup owner, partner contact, and required evidence artifact | Pull one live case and confirm who owns the alert, who can approve the disposition, and where the supporting record lives |

| Alert volume rises while closure quality drops | Set a SAR triage path with clear case states and required notes at each decision point | Sample a case and confirm what triggered review, which transactions were examined, who made the call, and when the decision was recorded |

| Sensitive data is shared outside approved channels | Restrict sharing to approved channels and keep access logging complete, including who accessed what and when | Make sure the case points to the exact location of the shared material and the approver tied to that action |

AML work in practice often includes customer checks, transaction monitoring, and suspicious activity reporting. Monitoring is a continuous review of transfers, deposits, withdrawals, and payments, but it can break down in familiar ways: outdated tools, excessive false positives, fragmented data, compliance-culture gaps, and conflicting requirements. If your product touches Convertible Virtual Currency activity, FinCEN has warned that risk can be harder to assess because of the global reach, distributed structure, limited transparency, and speed of widely used virtual currency systems. That is not a reason to overreact to every case. It is a reason to make sure your monitoring scope, escalation path, and evidence pack are tight enough to show how a decision was made.

Red flag 1#

Ownership is vague between teams. Fix it with an owner register for each key control: primary owner, backup owner, partner contact, and required evidence artifact. If ownership is shared but not explicit, treat it as unowned and escalate. A quick verification check is simple: pull one live case and confirm the reviewer can identify who owns the alert, who can approve the disposition, and where the supporting record lives without asking around in chat.

A common failure mode is that work sits in limbo, handoffs become verbal, and nobody can prove whether a review was completed or just discussed. In a bank partnership model, that can become expensive remediation because the issue is not only the alert itself, but the missing trail behind it.

Red flag 2#

Alert volume rises while closure quality drops. Set a SAR triage path with clear case states and required notes at each decision point. Prioritize timely, documented resolution over queue-clearing speed. The same operational automation discipline matters here, because faster handling only helps if case states, reviewer notes, and outputs stay consistent. Your checkpoint is whether a sampled case shows what triggered review, which transactions were examined, who made the call, and when that decision was recorded.

This is where weak monitoring quietly hurts you. False positives can swamp the team, and disposition quality can slip while teams try to move faster. FinCEN's advisory on CVC exploitation specifically emphasizes red flags and the SAR information most useful to law enforcement, regulators, and national security agencies. If a case file cannot show why the activity mattered, what context was considered, and how the conclusion was reached, you are accumulating rework, not reducing risk.

Red flag 3#

Sensitive data is shared outside approved channels. Restrict sharing to approved channels and keep access logging complete, including who accessed what and when. Unlogged sharing is difficult to evidence during review, and it gets worse when teams start sending screenshots, exported files, or customer details outside the case record. If you rely on approved channels, make sure the case points to the exact location of the shared material and the approver tied to that action.

This matters even more where source-of-funds or counterparty questions are already hard to assess. FinCEN notes that without sufficient controls, institutions cannot reasonably assess and mitigate those risks. If you cannot prove the path sensitive information took, you also cannot prove the review stayed within your approved controls.

Use a regular proof check, not a status check: sample real cases end to end and confirm ownership, disposition notes, monitored transaction context, and access history line up. Keep one concrete signal in view. One secondary-source report cites 6,830 SARs linked to money laundering between January and March 2025, which is directionally useful because it reinforces the point that suspicious-activity volume is not theoretical. The practical test is whether your team can pull a case under time pressure and show a clean record without backfilling anything.

We covered this in detail in California Money Transmitter License Requirements for First-Time Filers.

Conclusion#

Durable compliance here comes from clear scope decisions and repeatable, risk-based execution, not one-time setup.

Start with ownership and scope, then run applicable CIP and AML controls and related procedures consistently. For account opening, make sure the CIP minimum identity data is collected, including name, date of birth, address, and TIN or SSN, and keep decisions and evidence traceable under pressure.

The practical upside can be fewer surprises, cleaner partner-bank conversations, and faster audit response. In bank-fintech partnerships, role clarity matters because banks remain accountable for compliance with applicable banking laws.

Policy expectations can move, so build for reviewability. For Section 314(a), treat results as investigative leads routed through designated institution contacts, report positive matches within two weeks, do not respond when no match is found, and remember 314(a) is not a substitute for subpoena or other legal process.

Before scaling into a new country, partner-bank program, or higher-risk segment, validate your controls against official legal and regulatory texts and current partner requirements. Confirm your partner agreements still match operational reality and close any scope gaps with qualified counsel.

Frequently Asked Questions

Does the USA PATRIOT Act apply directly to fintech companies, or only to banks?

Based on these materials, CIP obligations are directed at covered financial institutions, and fintech firms are not explicitly covered in the same way. Scope depends on the entity’s role and partner-bank relationships.

What customer information is typically required under CIP at account opening?

The materials identify core CIP data elements: customer name, date of birth, address (for an individual), and TIN or Social Security Number. Exact collection and verification steps should follow the covered institution’s CIP program.

What is Section 314(b) in plain English, and when should a fintech use it?

Section 314(b) is voluntary information sharing among financial institutions to deter money laundering and terrorist activity. Use it when sharing with another financial institution is needed for that purpose, and keep it within Section 314 procedures.

Which PATRIOT Act sections matter most for a fintech handling cross-border payments?

Two anchors are clear: CIP requirements and Section 314 information-sharing mechanisms (314(a) and 314(b)); there is no ranked list of other cross-border priority sections.

How do responsibilities change when a fintech operates through a partner bank?

These materials indicate fintech role boundaries are not always explicit under CIP and can create confusion or conflicting incentives in partnerships. They do not define one universal responsibility split, so ownership and escalation paths should be documented by agreement.

What are the minimum controls a small fintech should implement first to reduce compliance risk?

Start with controls these materials support directly: CIP controls for account-opening identity data, SAR handling aligned to current FinCEN clarification, and controlled Section 314 information-sharing procedures.

How should teams balance AML monitoring with privacy obligations when sharing data?

Use Section 314 procedures to keep sharing tied to AML or terrorist-activity deterrence. Where bank obligations apply, protect nonpublic personal information while sharing only what is needed for that AML purpose.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/manual/AssessingComplianceWithBSARegulatoryR...trusted

- bsaaml.ffiec.gov/manual/OfficeOfForeignAssetsControl/01trusted

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- congress.gov/crs_external_products/IF/PDF/IF13168/IF13168...trusted

- congress.gov/event/118th-congress/house-event/LC75317/texttrusted

- federalregister.gov/documents/2022/09/30/2022-21020/beneficial-o...trusted

- federalreserve.gov/econres/notes/feds-notes/offline-payments-im...trusted

- federalreserve.gov/SECRS/2024/November/20241101/OP-1836/OP-1836...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Taxes in Germany for Freelancers and Expats

Low-stress compliance in Germany comes from decision order, not tax tricks. Use this sequence: confirm core facts, apply conservative temporary assumptions, verify the few points that can break invoices or filings, and keep one evidence file that explains each decision.

How to Automate Your Freelance Tax Preparation

**To automate freelance taxes safely, automate the boring mechanics and keep human approval for the decisions that create real compliance risk.** You are the CEO of a business-of-one. Your job is to run a system that stays resilient while your clients, tools, and countries change.

PFIC Rules for US Expats Investing Abroad

Start with compliance, not optimization. Screen PFIC risk before you buy, rebalance, or add cash. A common costly mistake is buying a familiar local fund first and checking PFIC classification later.