Quick Answer

A calm first year means choosing a simple starting structure you can explain, keeping business records and money separate, and building a repeatable monthly close before you scale. Start with a documented baseline, use the five decision filters to review sole proprietorship versus LLC timing, do not choose a Wyoming LLC by default, and confirm any expat filing position with qualified help before filing.

Start Here and Build a Calm First Year#

Your first year should be compliance-first, not hype-first. Build a clear baseline for your Business-of-One so your structure and recordkeeping decisions are easier to explain, maintain, and revisit later.

In practice, a calm first year usually starts the same way: establish the facts, document them, and track a few simple metrics. For a solo operator, that means getting the basics in place before you chase branding, growth talk, or shortcuts.

Start with a one-page baseline#

Before you choose a legal structure, write a one-page snapshot of how the business works today. A simple 1-Page Solo Strategy is enough. Make it specific enough to use:

- Where you live and work

- How clients find you and pay you

- The name you plan to use on invoices and contracts

- What records you already have

- What still needs legal or tax review

Then run a consistency check across proposals, contracts, invoices, and payment accounts. If names or records do not line up yet, log the gap before you make a structure decision.

What this guide is actually promising#

This guide helps you make an initial structure decision, follow a practical operating sequence, and keep cleaner records through the year. It is not promising rapid growth or a perfect setup.

Running an online business is demanding, and avoidable mistakes create cleanup work. The standard throughout is simple: can you show what you decided, why you decided it, and which documents support that decision?

Keep that standard visible with a short metric list. For example, track invoices sent, payments received as expected, and monthly records filed in one place.

Who this is for and who should slow down#

This guide is for independent professionals who want fewer surprises, cleaner records, and a more defensible first-year paper trail if cross-border filing is part of their reality.

If you already have employees, inventory, or complex ownership, treat this as a starting point, not a complete answer. If your location, client base, or filing facts are hard to explain clearly, pause and get qualified legal or tax advice before you take a firm position.

From here, the guide follows a practical order. First define the terms, then choose a starting structure, then build the habits that make year-end less chaotic.

Define the Terms Before You Choose Anything#

Before you choose a structure, define the terms you are using. When labels blur, unsupported legal or tax assumptions slip in, and those assumptions can drive bad decisions.

Here, entrepreneurship is framed as turning an idea into reality, with a key distinction between risk and uncertainty. Risk covers outcomes you can estimate. Uncertainty covers outcomes you cannot reliably estimate yet.

Many early solo decisions fall into uncertainty. What helps is not confident labeling but taking action, interacting, and reviewing what you learn. In the grounded comparison used here, a solopreneur is better understood as a systems-based lifestyle business model.

Run a quick check. Do you have one standard proposal, one contract version, one invoice format, and one place for supporting records? If not, you are probably still operating ad hoc.

What freelancer means, and why the distinction matters#

One grounded comparison describes a freelancer as primarily doing time-for-money client work, while a solopreneur is positioned more like a systems-based lifestyle business. That is not a value judgment. It matters because these terms often get blended together and then confused with entrepreneurship itself.

Keep legal and tax labels separate from operating model labels. Keep a one-page terminology note that shows which term describes your work style, which describes your current legal path, and which documents use each name.

That is also why the article does not chase generic "Freelance Blueprint" milestones. A short to-do list, clean naming, and consistent documents can help you make better decisions than optics.

Related: The Agency Scaling Blueprint: From Solo Freelancer to Hiring Your First 5 Global Contractors.

Choose Your Legal Starting Point in Week One#

Make a simple week-one choice, document it, and leave yourself room to change it cleanly later. You can start with a Sole Proprietorship while complexity is still low, then reassess an LLC as separation needs become clearer in the work.

Treat entity choice as a strategy, not a permanent identity. The risk runs both ways. You can wait too long to change structure, or take on extra admin before the business really needs it.

Use the same five filters each time you review your setup: income level, stability vs. volatility, risk exposure, growth plans, and exit or lifestyle goals.

Use practical triggers, not identity language#

| Decision filter | Start with Sole Proprietorship when | Move toward LLC when | What to verify this week |

|---|---|---|---|

| Income level | Revenue is still early and uneven | Income is stronger and the structure needs a closer review | Note current income pattern and whether it is changing |

| Stability vs. volatility | Workload and cash flow are still highly variable | Operations are becoming more predictable | Record where volatility is increasing or decreasing |

| Risk exposure | Current work has limited downside | Exposure is increasing and clearer separation matters more | Write one sentence on the likely impact of a bad project outcome |

| Growth plans | Near-term growth is modest | Growth plans add complexity | List the next growth moves and their operational impact |

| Exit or lifestyle goals | Current setup still matches your goals | Goals are changing and your structure may need to follow | Confirm whether your current structure still fits your direction |

If the work itself is starting to call for separation, do not hide behind "keeping it simple." If complexity is still low, a simpler start can be the disciplined choice, as long as you record why. Also keep the labels separate: an LLC is a legal entity, while an S Corp is a tax designation.

Make the choice reversible on purpose#

Do not treat your day-one structure as final. Set recurring checkpoints on a cadence you can actually maintain so the decision stays tied to facts instead of momentum. At each checkpoint, ask:

- Has risk exposure changed?

- Are income and workload becoming more stable or more volatile?

- Have growth plans increased complexity?

- Have exit or lifestyle goals shifted?

- Are records clean enough to support a structure change without reconstruction?

If your answers are shifting toward higher exposure, less predictable operations, or more growth pressure, revisit the LLC decision. If not, keep your current structure and keep the records tight.

Build the evidence pack now#

Whatever you choose, start a small evidence pack in week one so the decision is easy to audit later.

| Record | Sole Proprietorship | LLC |

|---|---|---|

| Starting record | A dated note explaining why you chose a simpler start | Formation and organizational records |

| Five-filter review | Your completed five-filter question sheet | Your completed five-filter question sheet |

| Ongoing checklist | Periodic updates to your entity self-assessment checklist | Periodic updates to your entity self-assessment checklist |

| Core documents | Contracts and invoices signed consistently in your correct legal name | Contracts, invoices, and signature blocks using the same company name consistently |

The main control is consistency across your core records. Weak documentation discipline creates avoidable cleanup later.

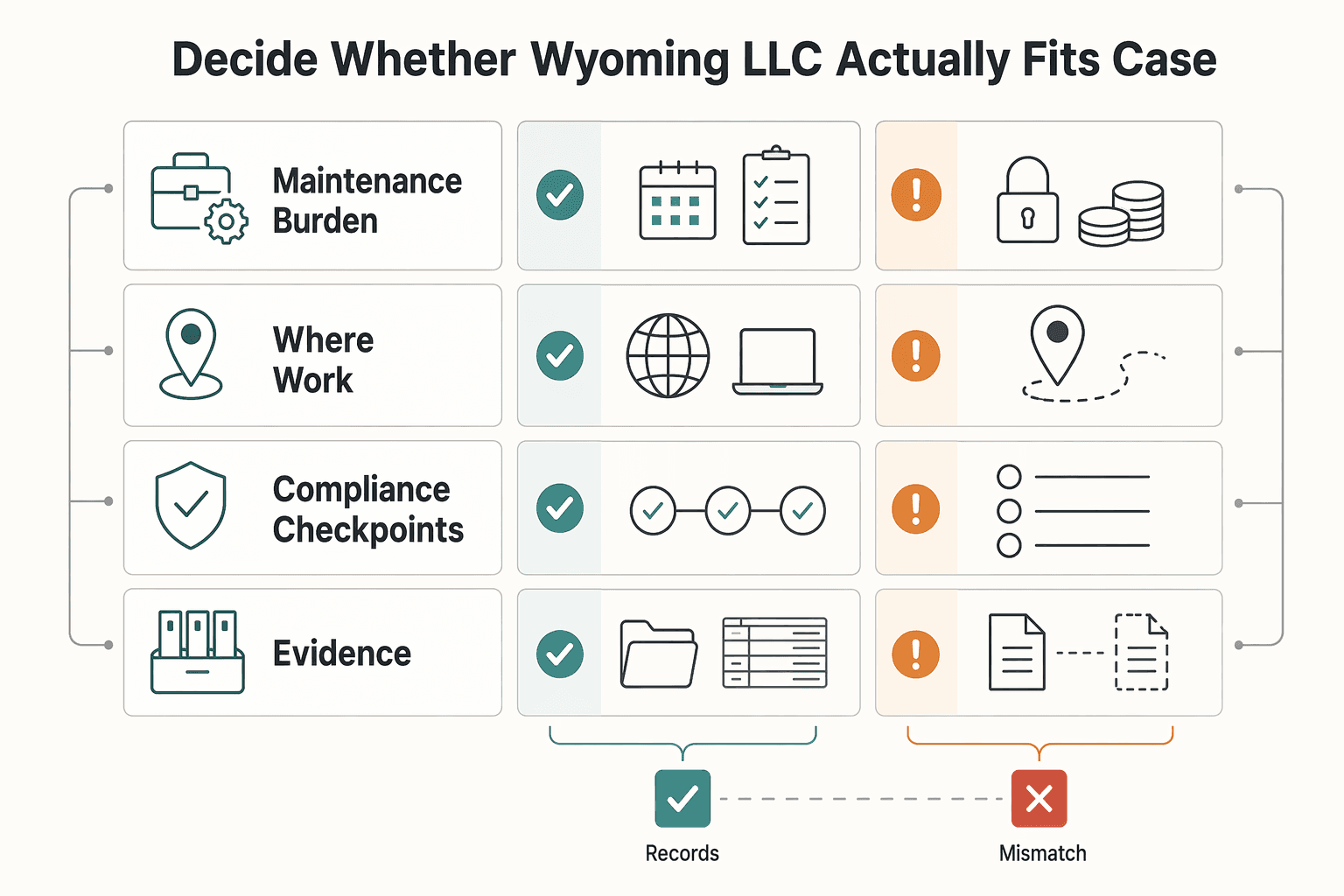

Decide Whether a Wyoming LLC Actually Fits Your Case#

Do not choose a Wyoming LLC by default. Choose it only if it clearly fits how the business actually runs and what you can realistically maintain in year one. State choice should follow operating facts, not reputation.

A quick SWOT can help here because it forces you to compare tradeoffs instead of reacting to branding.

| Decision point | What to check before choosing Wyoming or your home state |

|---|---|

| Maintenance burden | List the recurring admin you will need to keep up, then confirm you can do it consistently. |

| Where work is managed | Write a plain-language summary of where day-to-day decisions and operations happen. |

| Compliance checkpoints | Confirm you reviewed licensing and sales tax considerations. |

| Record discipline | Make sure your setup avoids co-mingling accounts and keeps business records clean. |

If your operating facts are straightforward, prioritize a setup you can run cleanly from day one. If they are complex or changing, slow down and map those facts first so the entity choice does not outrun the operation.

Whichever route you choose, document your reasoning now. First-year mistakes can create long-term cleanup risk, and co-mingling accounts can create avoidable problems later.

Execute the First 90 Days in the Right Order#

Treat your first 90 days as a build phase, not a growth sprint. Stabilize how money and records flow first, then add more client volume.

Even a reasonable structure choice can create cleanup work if setup is rushed. Run this quarter in stages, keep continuity in how you work, and avoid constant context switching while the foundation is still fragile.

Days 1 to 30#

Build the base in order, not all at once. Start with a quick fit check against your current setup decision. Then create the core pieces you will use every week: account access, payment setup, invoice format, bookkeeping home, and one document system for contracts, invoices, receipts, and statements.

Set naming and ownership rules now so the same business details show up across contracts, invoices, banking, and bookkeeping. That is the control that keeps tasks from getting dropped and records from scattering.

Days 31 to 60#

Use month two to prove the setup works under real activity. Run invoicing from one place, route payments to the intended account, and record expenses on a fixed rhythm.

If your process still depends on memory or inbox hunting, fix that before you add complexity. Keep it simple enough that momentum does not get lost to repeated context switching.

Days 61 to 90#

Month three is about repeatability. Run the same close process twice in a row: match invoices to deposits, review uncategorized items, save statements, and file supporting documents. If the close is not repeatable yet, do not scale outreach or onboarding. Make the existing process predictable first.

These are operational checkpoints, not legal or tax filing deadlines.

| Checkpoint | Pass if | Fail if | Corrective action |

|---|---|---|---|

| Day 30 | Core accounts, invoicing, and document system are set up and being used | Money flow or files are still fragmented | Pause new intake briefly and finish setup before expanding work |

| Day 60 | One full reconciliation cycle is complete and traceable | Records are behind, unclear, or memory-dependent | Reduce moving parts, set a fixed review cadence, and backfill gaps |

| Day 90 | Two consistent monthly closes are complete with clean retention habits | Close steps are inconsistent or key records are missing | Stop scaling, assign clear ownership, and clean the prior cycle first |

As you work through this first-year plan, keep travel-rule debates separate from operating discipline. If that topic influenced early decisions, review 183-Day Rule Explained: Stop the Tax Myths Before They Cost You. Keep day-to-day systems decisions grounded in what you can actually run consistently.

Build a Money System That Survives Tax Season#

Build your money setup around one rule: keep business money separate from personal money, and assign each business dollar a clear purpose before you spend it. That is the practical version of a Business-of-One money system, and it helps make tax season manageable instead of reactive.

Whether you are operating as a Sole Proprietorship or an LLC, start with a dedicated business checking account. If possible, add a separate business savings account for taxes so those funds do not get absorbed into day-to-day spending. Keep the setup simple, but keep it clear.

| Money bucket | Practical home | What belongs there | Monthly check |

|---|---|---|---|

| Income | Dedicated business checking account | Client payments and payouts | Can each deposit be matched to an invoice or payout record? |

| Owner pay | Scheduled transfer or clear bookkeeping category | Owner draws or compensation | Are owner transfers clearly labeled and easy to identify? |

| Tax reserve | Separate business savings account | Funds set aside for taxes | Did you move tax money before using operating cash? |

| Operating expenses | Business checking + bookkeeping categories | Business purchases and fees | Is each expense categorized with supporting records? |

The tradeoff is simple: one mixed account may feel faster now, but separation reduces confusion, missed deductions, and tax-time cleanup later. To keep that separation real, run the same monthly checklist every month:

- Review invoice status so sent, paid, and overdue items are visible.

- Reconcile deposits and payouts against your records.

- Capture receipts and payment confirmations while details are still fresh.

- Close the books by categorizing transactions, clearing uncategorized items, and keeping your reports.

For audit readiness, keep records organized and easy to trace across invoices, payment history, receipts, and categorized transactions. These are not automatic legal guarantees, but clear separation and consistent records make questions easier to answer if they come up.

If you use Gruv where supported, invoicing, payout status tracking, and exportable records can help reduce manual matching work. The operating rule stays the same: review monthly, and retain the records you may need later. Use a consistent invoice format now so reconciliation is easier later: Start with the free invoice generator.

Handle Expat Reality Without Falling for Residency Myths#

Treat your filing position as unconfirmed for now. For this part of your first US Expat Tax Return planning, the safest move is to avoid conclusions built on shortcuts until you have qualified review.

Start from what is actually supported#

This material does not give you authoritative expat tax rules. It includes real-estate and business-credit podcast material, which is not enough to support cross-border filing conclusions.

Do not treat a day count as a complete answer#

This material does not support using a day count alone, including references to a 183-Day Rule, to determine your U.S. filing position. If advice starts and ends with a slogan or a single number, treat it as incomplete and verify before filing.

Country and case details still need case-specific review#

This material does not establish country-by-country residency outcomes, treaty treatment, or jurisdiction-specific filing duties. Use it as a reminder to confirm your own facts, not to copy someone else's result.

Confirm safely before claiming any position#

Before you sign with any provider, do your due diligence. Ask direct questions about what facts they need, what could change their view, and what their review will and will not cover. Watch for scam signals, including pressure to pay through informal channels like Zelle or Cash App before basic diligence is complete.

If you keep one rule from this section, keep this one: when your filing position depends on a shortcut, pause and confirm it with qualified help first.

Prepare Year End So Your First Return Is Boring#

Make year end a cleanup phase, not a scramble. For your first return, the goal is to give your preparer a file they can review quickly instead of one they have to reconstruct.

Weak documentation is a common failure point. Waiting can raise cleanup cost, but rushing can create cost too, so use a deliberate review window before filing.

Use a late-year window for cleanup, not discovery#

Treat the final stretch before filing as a practical checkpoint, not a required IRS rule. Run focused reviews:

- Reconcile bookkeeping with your core account activity.

- Verify entity records and key administrative details, including state-level realities.

- Validate how income and expenses are categorized across your records.

- Close documentation gaps while details are still easy to confirm.

This is also a good time to revisit your structure logic. Entity choice is not one-and-done, so if your facts changed, update your reasoning and records. Complete or refresh Tool 1: Entity Self-Assessment Checklist, and keep Tool 6: a one-page entity snapshot with your core entity details for faster review.

Build a return-ready package your preparer can use#

There is no universal legal packet for every case, but you should still prepare a working file before handoff. In many cases, that means organized bookkeeping outputs, supporting records, and short notes that explain unusual transactions or open items.

Fix red flags before filing handoff#

Use prechecks that force correction before filing:

- Documentation is incomplete, unclear, or hard to follow.

- Timing has shifted into last-minute decisions that increase cleanup risk.

- State-level or administrative realities were skipped in earlier setup decisions.

Run a quick test with sample records. If key details do not align or important context is missing, clean that up before handoff.

Set a clean handoff standard#

Give your preparer one organized folder with labeled records, final bookkeeping exports, your entity snapshot, and a short memo of unusual items or open questions. Keep the memo factual, and route tax or legal judgment calls to a qualified independent advisor based on your specific situation. That is the standard you want: fewer assumptions, fewer clarification loops, and a first return process that feels routine.

For a step-by-step walkthrough, see A Guide to Filing Your First Tax Return in France.

Fix the Mistakes That Usually Cost the Most#

Many costly mistakes are process mistakes: locking in the wrong structure too early, ignoring ongoing state and administrative reality, and letting documentation drift.

Across all three, the pattern is the same. An undocumented assumption turns into a filing position. Once that happens, cleanup can become slower and more stressful than making a clear decision earlier.

Wrong entity, wrong timing#

Entity mistakes are often timing mistakes. Entity choice is not one-and-done, and both waiting and rushing can create cost.

If you formed an entity too early, or stayed a Sole Proprietorship too long, run your facts back through the five decision filters and write down the result: income level, stability vs. volatility, risk exposure, growth plans, and exit or lifestyle goals. A written trail helps with later reviews and changes.

Wyoming only works if you respect the admin reality#

A Wyoming LLC is not automatically good or bad. The real question is whether you are maintaining the state and administrative reality consistently.

Check for alignment across your core records and documentation. Keep your entity self-assessment checklist and one-page entity snapshot current. If those are missing, review and filing work can turn into reconstruction.

Weak records create late pain fast#

Weak documentation can compound other mistakes. Use this recovery order:

- Stabilize core records first so documentation is complete and consistent.

- Correct entity and admin records second, including your checklist and one-page entity snapshot.

- Remediate tax filings last, with qualified professional support where needed.

Filing before records are stable can carry the same confusion into formal submissions.

Stop doing this now#

- Stop treating a Wyoming LLC as a one-time setup.

- Stop making structure decisions from memory instead of a documented checklist.

- Stop delaying documentation and record cleanup once gaps are visible.

- Stop ignoring state and administrative reality.

- Stop making entity changes without a written rationale tied to the five decision filters.

- Stop treating general information as individualized legal or tax advice.

If any of these are true today, rebuild the record first, then get qualified tax or legal advice for your specific situation.

Know Exactly When to Bring in a Pro#

Use a DIY path only when your facts are simple and documented. If key details are unclear, get focused professional help before you finalize decisions.

| Area | DIY is usually reasonable when | Bring in a pro when | What to hand over |

|---|---|---|---|

| Sole Proprietorship or Limited Liability Company (LLC) setup | You are choosing between these basic starting structures, operating in one location, and using straightforward contracts | You cannot clearly map liability exposure, growth plans, or local compliance requirements to your structure choice | Business summary, draft contracts, where you operate, and your open compliance questions |

| Local compliance and licensing | You have already confirmed the requirements that apply in each location where you operate | You are unsure which local rules apply, or requirements conflict across locations | Activity description, permit or licensing notes, and the places you sell or deliver work |

| Early market-readiness check | You can identify three to five established operators in your niche and verify local permit activity or supplier signals where relevant | Market or permit signals are unclear and you need help validating assumptions before committing | Competitor notes, permit checks, supplier feedback, and your core assumptions |

The practical trigger is ambiguity. Local compliance can vary a lot by jurisdiction, so a simple plan can become complex once location-specific rules apply.

Keep the scope tight#

Do not start with a broad "full setup" package. Buy the smallest review that unblocks your next decision, then expand only if that review uncovers a second issue.

Before you book help, run a quick reality check: identify three to five established operators in your niche, then verify local permit activity or supplier signals where relevant. If the business case is clear but the compliance path is not, targeted paid support can be the better move.

Take the Next Step This Week#

This week, keep it simple: choose your current structure path, set a basic money map, and start a monthly recordkeeping rhythm you can sustain. For a Business-of-One, that is a practical way to avoid the confusion and wasted effort that usually come from trial and error.

You should leave this article with a short to-do list, not a longer idea list. The goal in seven days is not a perfect back office. It is a setup that is clear, repeatable, and easy to review before small gaps turn into bigger cleanup work.

Make one decision you can explain#

Pick your current operating path and document it in plain English. Write down the setup you are using now, why it is your working choice for this stage, and what you still need to confirm with a qualified professional.

By the end of the week, you should be able to answer three questions clearly: What setup are you using now? How will you handle agreements and payments consistently? What would make you revisit this decision? If you cannot explain those answers cleanly, pause and book a focused review.

Your 7-day checklist#

Use this as a week-one reset, not a full overhaul.

| Day | Focus | Action |

|---|---|---|

| Day 1 | Decision note | Write a one-page decision note with your current setup, the business name you will use publicly, and the open questions you still need answered. |

| Day 2 | Tracking structure | Decide where key business activity and decisions are logged so you can review them in one place. |

| Day 3 | Record home | Create one home for key records and working documents, with file names you will recognize later. |

| Day 4 | Monthly cadence | Add one recurring review block to check what is complete, what is pending, and what needs clarification while details are still fresh. |

| Day 5 | Expert questions | Build a short question list for expert support. Keep it specific so you get direct answers instead of a vague consultation. |

| Day 6 | Retrieval test | Test retrieval. If you cannot quickly find the documents and notes you need, tighten the setup. |

| Day 7 | Outside help | Decide whether you need outside help now. If structure, signing, or recordkeeping is still fuzzy, book the review this week. |

What good looks like by Friday#

Done does not mean fully optimized. Done means next month will be easier than this month: one current setup choice, one place where key activity is tracked, one place where records live, and one calendar slot for review.

That is where simplicity starts to pay off. One clear offer, one understandable setup, and one repeatable admin rhythm usually beat trying to do everything at once. This approach will not remove all legal or tax complexity, but it can help a Business-of-One keep momentum while you verify details.

Related reading: The 'Solo Agency' Blueprint: How to productize your services and manage subcontractors. Before you finalize your filing plan, pressure-test your travel timeline and assumptions with the tax residency tracker.

Frequently Asked Questions

What should a US solopreneur do in the first 90 days?

Use the first 90 days to stabilize how money and records flow before you chase growth. In days 1 to 30, set up core accounts, invoicing, bookkeeping, and one document system. In days 31 to 60, run invoicing and expense capture on a fixed rhythm. By days 61 to 90, complete two repeatable monthly closes before scaling.

Do I need an LLC in year one, or can I stay a sole proprietor?

You can start as a sole proprietorship while complexity is still low and reassess an LLC as separation needs become clearer. Review the same five filters each time: income level, stability versus volatility, risk exposure, growth plans, and exit or lifestyle goals. If the choice is still unclear, get a focused review before filing.

When does a Wyoming LLC make sense for a solo business?

A Wyoming LLC makes sense only if it fits how the business actually runs and what you can realistically maintain in year one. Review maintenance burden, where work is managed, compliance checkpoints, and record discipline before choosing Wyoming or your home state. Do not choose Wyoming by default or because of generic online advice.

If I live abroad, what US tax tasks still apply?

This guide does not establish your exact U.S. filing obligations, forms, deadlines, residency outcome, or treaty treatment. Do not rely on day counts or shortcuts alone. Confirm your facts early with a qualified professional before taking a filing position.

What records should I keep every month to avoid tax-season panic?

Keep one consistent system for invoices, payment history, receipts, statements, categorized transactions, contracts, and bookkeeping records. Each month, review invoice status, reconcile deposits and payouts, capture receipts and confirmations, and clear uncategorized items. Organized records make year end easier to explain and hand off.

How do I know when to hire a tax professional instead of doing it myself?

Hire a professional when key facts are unclear or your filing position depends on assumptions, shortcuts, or location-specific rules. Use a DIY path only when your facts are simple and documented. Start with the smallest targeted review that unblocks your next decision.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 5 external sources outside the trusted-domain allowlist.

- digitalcommons.pepperdine.edu/cgi/viewcontent.cgitrusted

- pressbooks.cuny.edu/introductiontobusiness/chapter/chapter-7-newtrusted

- researchdiscovery.drexel.edu/view/pdfCoverPagetrusted

- calmbusiness.com/foundationexternal

- earlytorise.com/the-adhd-entrepreneurs-guide-to-actually-fol...external

- erikduncan.com/blog/one-person-business-modelexternal

- fulfillment.com/how-it-worksexternal

- instagram.com/p/DWDS3UiCGTNexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

The 'Profit First' Method Part 2: Setting Up Your Bank Accounts

Most freelancers who try Profit First open a few extra bank accounts and call it done. That's the wrong move.