Quick Answer

Follow a strict three-step sequence: finalize the client file, run invoice QA against that file, then classify lines before any OSS decision. If legal entity details, billing data, VAT ID, or line descriptions do not match, hold the invoice. For mixed engagements, keep custom judgment-led work separate from essentially automated B2C lines, and move only the relevant lines into OSS review.

The US Designer's Playbook for EU VAT: A 3-Stage Framework for Invoicing Clients#

Use a strict go/no-go flow: client file, status validation, invoice QA, then line-level classification for OSS. If any stage is unresolved, do not send the invoice.

That order matters more than most teams expect. A lot of avoidable VAT errors do not start with a hard legal issue. They start with a rushed workflow. The invoice gets drafted before the client file is stable, the billing contact sends a late correction, a template carries over wording from another job, or a bundled engagement gets treated as one thing when it is really two different lanes. Once that happens, the invoice starts driving the conclusion instead of reflecting the evidence you already have. This framework is meant to stop that.

The practical goal is simple: each invoice should be boring to review. By the time you send it, the identity, status, service description, and proposed treatment should all point in one direction. If they do not, your process is telling you to pause, not to improvise.

To keep decisions consistent, lock these working terms first:

- B2B: working label for a business customer record.

- B2C: working label for an end-consumer customer record.

- VAT wording: the invoice wording you plan to use after verification.

- Member State handling: a working note on which Member State path may apply.

- Potentially automated digital line: a working label for lines that may need OSS review.

These are operational labels, not legal conclusions. The goal is to route each invoice into the right review lane and keep matching evidence at every step.

In practice, you are not trying to solve every VAT question from scratch on every project. You are trying to move each job through a controlled sequence:

- identify who the customer actually is,

- confirm whether the status evidence supports the treatment you plan to use,

- make sure the invoice mirrors that file exactly, and

- only then decide whether any line belongs in an OSS review lane.

That sequence cuts two common problems. First, it prevents a billing document from creating a new identity or treatment theory at the last minute. Second, it stops mixed work from being collapsed into a single label just because it was sold together. For designers, that second point is especially important. Many engagements are not purely one thing. They may include custom design work, revision cycles, creative direction, and some digital delivery. If you skip the line-level review, you lose the distinction the file needs.

Use the table below as an operating snapshot. Think of it as your dispatch board: each invoice should move through it cleanly, and any unresolved issue should tell you where to stop.

| Stage | What you check | Evidence required | Next action | When to escalate |

|---|---|---|---|---|

| Step 1 | Customer identity and status | Legal entity name, billing details, claimed VAT ID (if any), service description, contract/order record | Mark go or no-go | Identity mismatch, unclear customer status, conflicting records |

| Step 2 | Invoice mirrors the file | Draft invoice, exact customer fields, line descriptions, VAT wording you plan to use | Send only if every field matches the file | Draft forces a new identity or treatment judgment |

| Step 3 | Mixed scope and OSS gate | Line-level breakdown, delivery method, evidence of human input vs automation, customer type | Separate custom lines, then review only relevant digital lines for OSS | Borderline automated delivery, unclear Member State handling, multi-country complexity |

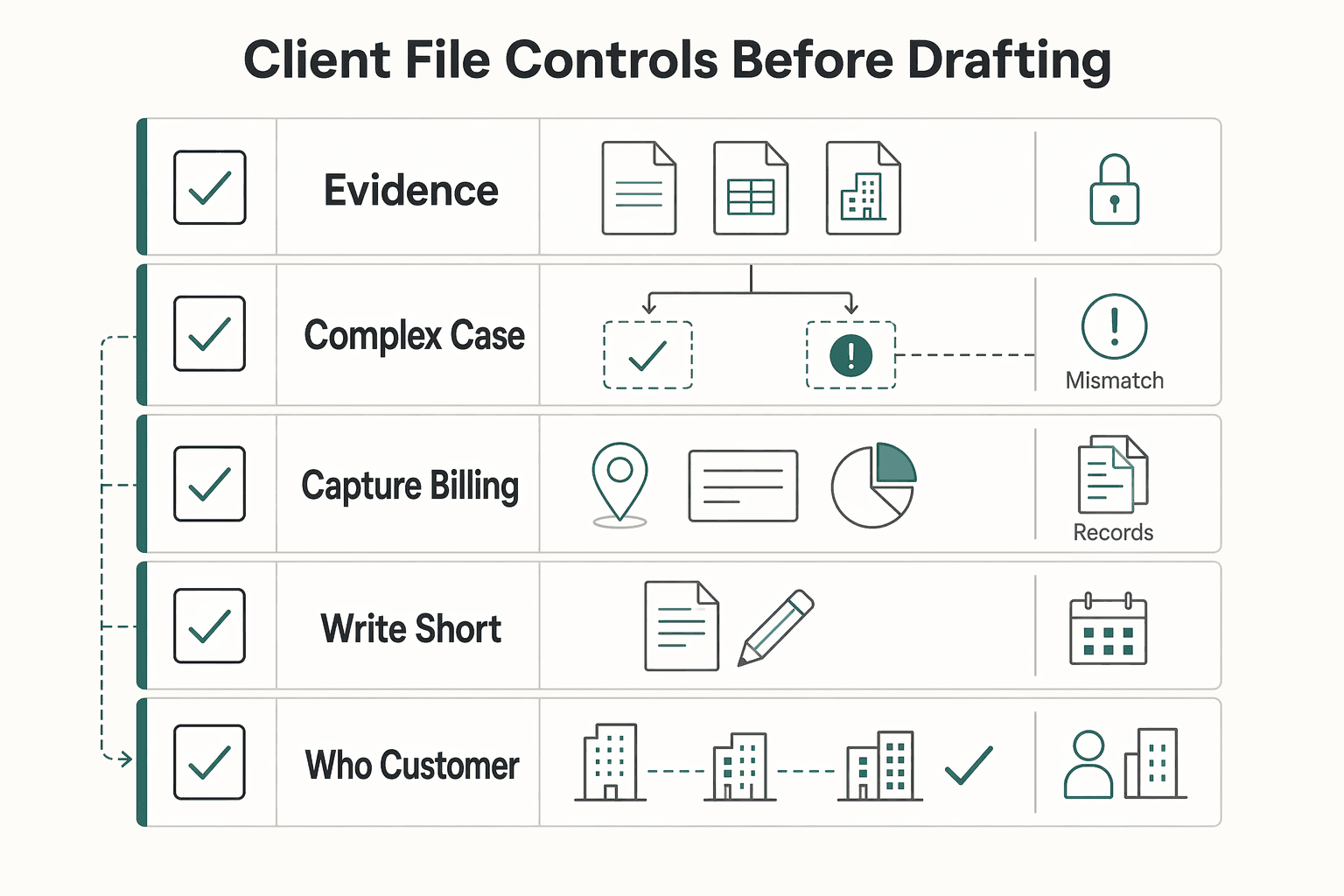

Step 1 Build and validate the client file#

Build one client record before you draft the invoice. Include the exact legal entity, billing address, claimed VAT ID if provided, and a concrete description of what you delivered.

| File item | What to keep | No-go trigger |

|---|---|---|

| Legal entity name | Pull the legal entity name exactly as given in the contract or order record | The contract, billing details, and VAT ID do not align |

| Billing address | Capture the billing address exactly as provided | The source record and the billing system disagree |

| Claimed VAT ID | Record the claimed VAT ID if one was supplied | The VAT ID appears without matching billing details |

| Service description | Write a short service description that reflects what you actually delivered | The service sold is described too vaguely to support later classification |

| Corrected details | Keep both the original and corrected versions so the correction trail stays clear | Corrected details arrive late and replace older ones without a clear trail |

Client File Controls Before Drafting#

Do not treat this as admin cleanup you can do later. The client file is the control point everything else depends on. If the file is weak, you will end up making treatment calls from memory, email fragments, and whatever wording happens to be in the draft invoice. That is the workflow this article is trying to prevent.

Your first decision is straightforward: do all identity details point to the same customer? If the contract, billing details, and VAT ID do not align, treat the file as unresolved and stop there. Build the file in the same sequence every time:

- start with the contract or order record,

- pull the legal entity name exactly as given there,

- capture the billing address exactly as provided,

- record the claimed VAT ID if one was supplied,

- write a short service description that reflects what you actually delivered, not a vague internal label.

That short service description matters more than it seems. If your file says only "design services," you have made later classification harder for no reason. A concrete description helps the next reviewer understand whether the work was custom and judgment-led, whether it included digital delivery, and whether any line may need separate review later. You are not trying to create a legal memo. You are trying to make the file usable.

Match the evidence. A VAT ID on its own is not enough if the legal entity and billing details do not match what you plan to invoice. When VAT status is part of the file, run the same VAT Number Validator check each time so the evidence trail stays consistent. When client details change, keep both the original and corrected versions so the correction trail stays clear.

That correction trail is part of the file, not an afterthought. If a client first sends one entity name and later updates it, do not overwrite the old version without context. Keep the original record, note what changed, and keep the corrected version with the date or sequence clear enough that another person can follow it. The point is not bureaucracy. It is so that, if a question comes up later, you can show how the file moved from unresolved to resolved.

A workable file should let you answer these questions immediately:

- Who is the customer you are invoicing?

- What did you sell?

- Is the customer record stable, or are there unresolved conflicts?

- If a VAT ID is claimed, does it sit in the same record as the legal name and billing details you plan to use?

- Is the service description specific enough to support later line review?

If the answer to any of those is "not really," the file is not done.

A good discipline here is to separate what the client told you from what your invoice system currently contains. Those are not always the same thing. Systems often auto-fill from older records, from a parent company, or from a previous job. If the source record and the billing system disagree, do not guess which one is "close enough." Resolve it in the file first. Let the invoice inherit the answer, not create it.

Typical failure modes at this stage are mundane, but they can block the invoice:

- the contract names one entity, while the billing contact asks for a different one,

- the legal name is shortened for convenience and no longer matches the support file,

- the VAT ID appears without matching billing details,

- the service sold is described too vaguely to support later classification,

- corrected details arrive late and replace older ones without a clear trail.

Every one of those is a no-go until fixed.

It also helps to define what "resolved" means internally. A file is resolved when the identity fields stop moving and when the service description is specific enough that someone other than you can understand the job from the record alone. If the billing contact keeps asking "which entity should this go to?" or if the service line could mean several different things, you are not ready for Step 2.

Verification point: someone else should be able to open the file and identify the customer, the service sold, and whether status is resolved in under a minute.

That one-minute test is worth using literally. Hand the file to a teammate and ask them to answer three questions without asking you for context:

- Who is the customer?

- What was sold?

- Is the record resolved or open?

If they hesitate, the file needs work. Usually the fix is not complicated. Tighten the service description, attach the missing order record, clean up the exact legal name, or separate original details from corrected details. The value is that you catch confusion before it turns into an issued invoice.

One more practical point: keep the file focused. You do not need every email ever sent. You do need the set of records that support the invoice decision. That usually means the contract or order record, the billing details, the claimed VAT ID if any, the service description, and any correction trail needed to explain changes. If a reviewer has to dig through inbox threads to reconstruct the basics, your control is too loose.

The deeper reason Step 1 matters is that every later stage relies on it. VAT wording, customer status, line classification, and OSS review all become riskier when the customer record is unstable. That is why this framework is strict about stopping early. Pausing here is cheaper than correcting a sent invoice later.

Invoice QA as a Fidelity Check#

Step 2 is a strict mirror test: every invoice field must map back to the resolved file before the draft can move forward. If your team needs a process anchor, pair it with the VAT Number Validator and your internal draft controls.

Step 2 QA the invoice against the file#

Once the file is resolved, invoice QA should be mechanical. At this stage, you are checking fidelity, not making a fresh treatment decision.

| Invoice field | Match to file | Stop if |

|---|---|---|

| Customer legal name | Same customer as the file | The draft includes a customer name not found in the resolved file |

| Billing address | Same as the resolved record | The billing address differs from the latest resolved record |

| Claimed VAT ID | Same VAT ID captured in the file | The VAT ID is missing, changed, or attached to a different name than the file supports |

| Line descriptions | Reflect what was actually delivered | The line description is vaguer than the file and makes classification less clear |

| VAT wording | Limited to what the file already supports | The wording implies treatment that the file has not yet supported |

That matters. Run invoice QA as a fidelity check, not as the place to solve ambiguity. If the draft invoice raises a new question, send the issue back to the file instead of improvising on the document itself. The draft should confirm a decision already supported by the record.

Match the legal name, billing details, VAT ID, and line descriptions exactly to the file. If a vague line description makes classification harder, pause and fix the file first.

"Exactly" does a lot of work here. Teams often relax that standard because the differences feel small: an abbreviated entity name, an old address that is still familiar, a service label copied from a proposal, or generic wording used for speed. Those shortcuts are where mismatches start. If your file says one thing and your invoice says another, you are no longer documenting the same customer record.

A useful way to run QA is field by field, in a fixed order:

- customer legal name,

- billing address,

- claimed VAT ID if any,

- line descriptions,

- VAT wording you plan to use.

That order keeps you from polishing the output before confirming the identity. It also makes handoff easier if another person reviews the draft. They do not need to infer your logic. They can trace each field back to the file in the same sequence every time.

Hard rule: if any draft field forces a new judgment, it is a no-go. Common failure modes include template carryover, shortened entity names, stale billing details, and VAT wording reused from another client.

Template carryover deserves special attention because it creates clean-looking errors. A reused invoice template can contain a familiar line description, leftover wording, or an old customer field that looks plausible enough to pass a quick glance. That is why QA should not be "does this look normal?" It should be "can each field be traced to the file?" A polished invoice can still be wrong if it is based on the wrong record.

For any VAT wording, including reverse-charge text, only use text you can already support from the file. If Member State wording is uncertain, hold the draft with Member State handling marked as pending official verification.

That hold rule is practical because it keeps time pressure from turning into guesswork. If the file supports the customer identity and service description but the wording needs verification, hold the draft with a visible internal note. Do not send wording copied from another case. The unresolved note acts as a hard stop. It tells everyone the invoice is not ready, even if the rest of the draft looks complete.

Another useful control is to compare the draft line descriptions to the service description in the file. They should not drift apart. If the file says the work was custom and revision-led, but the invoice line is broad or generic enough to obscure that, you have made later review harder. The invoice does not need to contain every production detail, but it should reflect the file clearly enough that the nature of the work is not distorted.

A strong QA pass should answer these questions:

- Does the draft name the same customer as the file?

- Are the billing details the same as the resolved record?

- If a VAT ID appears, is it the same one captured in the file?

- Do the line descriptions reflect what was actually delivered?

- Is the VAT wording limited to what the file already supports?

- Does any field rely on assumption, habit, or an old template?

If any answer is no, stop and correct the source.

Verification point: every invoice field should trace back to the file without inbox archaeology.

That standard is harder than it sounds, and it is supposed to be. If a reviewer has to search old messages to understand why the draft uses a certain entity name or wording, then the file was not complete enough to support the invoice. The invoice should be the endpoint of the workflow, not the place where hidden logic lives.

One practical way to make this reliable is to treat the invoice draft as a mirror, not a workspace. Build your decisions in the file, then copy them into the draft. When people use the draft itself to "figure out" the treatment, small inconsistencies creep in. The legal name gets shortened for layout reasons. A generic line gets used because it was in the template. A wording block from another job stays in place because it looked familiar. None of that is mechanical QA. It is a fresh decision disguised as formatting.

Watch for these common no-go triggers:

- the draft includes a customer name not found in the resolved file,

- the billing address differs from the latest resolved record,

- the VAT ID is missing, changed, or attached to a different name than the file supports,

- the line description is vaguer than the file and makes classification less clear,

- the wording implies treatment that the file has not yet supported.

When that happens, do not repair it informally by saying "we know what they mean." Fix the file or hold the invoice. Informal fixes are exactly how the document and the support record drift apart.

The practical benefit of a disciplined Step 2 is speed later. Once your team trusts that invoice QA is a fidelity check rather than a new debate, review gets faster. Most invoices should move through this stage quickly because the hard thinking was already done in Step 1. The ones that do not move quickly are telling you something useful: the record remains unstable, or the line descriptions need work before any VAT treatment can be trusted.

Mixed-Scope Classification Before OSS#

Step 3 also runs in a fixed order: split the scope first, classify each line, and only then review OSS fit. For execution discipline, keep the draft format stable with the Free Invoice Generator so line-level distinctions stay visible before approval.

Step 3 Split mixed work before you consider OSS#

Do the line-by-line classification before you assess OSS. Internet delivery by itself does not settle this workflow classification. The practical split here is custom, human-led work versus potentially automated delivery.

| Situation | Path | Note |

|---|---|---|

| No business establishment nor fixed establishment in the EU | Non-Union scheme | May choose any Member State of identification |

| EU establishment or fixed establishment | Union scheme | Member State of identification is tied to where the business is established |

| Specified fixed-establishment cases | Union scheme | Choice is binding for the calendar year plus the next two calendar years |

| Treatment still unclear across participating EU countries | VAT Cross Border Ruling (CBR) | Request it in the participating EU country where you are VAT-registered, following that country's national VAT-ruling conditions |

This is the step where design businesses usually need the most discipline, because the commercial engagement may feel like one project even when the VAT review should not treat it as one undivided line. A client may buy a package, but your review has to ask what each part actually is. If you skip that question and jump straight to OSS, you risk applying scheme logic to a scope that has not been cleaned up first.

If a line is custom, revision-led, and depends on your judgment, keep it in the custom lane unless later review shows otherwise. If a line appears essentially automated and the customer is B2C, consider it for the OSS review lane.

That split is not about how the work was sold on your website or in your proposal. It is about how it was actually delivered. A custom engagement can involve online delivery. A digital file may be part of custom work. Internet delivery by itself is not the answer. What matters is whether the line depends on your ongoing human input and judgment or whether it is essentially automated with minimal human intervention.

A practical way to run the review is line by line, not project by project. For each line, ask:

- What exactly was delivered?

- Was the result dependent on your judgment?

- Was the work custom and revision-led?

- Or was it essentially automated?

- Is the customer B2B or B2C for this file?

Only after that should you ask whether OSS is relevant. That sequence matters because OSS is an output question, not the starting classification question.

The draft already gives you the core distinction in a simple review table:

| Review lane | Indicators from the file | What you do next |

|---|---|---|

| Custom lane | Custom, revision-led, depends on your judgment | Keep separate and do not push into OSS review just because delivery happened online |

| OSS review lane | Essentially automated delivery and the customer is B2C | Review only those lines for possible OSS treatment |

Scheme Selection and Establishment Facts#

That distinction matters because OSS only becomes relevant after the scope is clean. Since 1 July 2021, OSS rules cover cross-border B2C e-commerce activities and include TBE services. If you have neither a business establishment nor a fixed establishment in the EU, the Non-Union scheme is the scheme to evaluate, and you may choose any Member State of identification. That registration issues an OSS VAT ID in EUxxxyyyyyz format. That ID is only for supplies reported under the non-Union scheme.

Those are important facts, but operationally the key point remains sequencing: line split first, scheme review second. If you reverse that order, you will be tempted to treat the whole engagement according to the most visible digital element, even where other lines belong somewhere else.

If you do have an EU establishment or fixed establishment, assess the Union scheme path instead. Its Member State of identification is tied to where the business is established, and in specified fixed-establishment cases the choice is binding for the calendar year plus the next two calendar years. Changing the Member State of identification is restricted unless the fixed establishment is dissolved or moved.

That means establishment facts are not a detail to check casually after the invoice is drafted. They affect which scheme path you evaluate and whether your Member State of identification is freely chosen or tied to where the business is established. If those facts are unclear, that is an escalation issue, not something to smooth over in billing.

The main red flag is a bundled engagement that combines custom design and automated digital delivery. Split the lines first, then decide.

In practice, bundled work causes three common problems.

First, the proposal language is broader than the actual delivery. A package may have been sold under one commercial label, but the file may show that some parts were custom and revision-led while others were delivered in a way that could raise automated-service questions. The commercial bundle is not enough. You need separate line review.

Second, the invoice may compress unlike items into a single broad line because that feels cleaner or more client-friendly. That works against you here. If a mixed job is invoiced as one vague item, you have made it much harder to justify why part of the scope belongs in one lane and part in another.

Third, teams sometimes assume that if any digital asset changed hands, the whole project should be treated as digital. This framework rejects that shortcut. Delivery over the internet does not settle classification.

A better workflow is to break the engagement into invoice lines that reflect how the work was performed. Keep custom, judgment-led work in the custom lane. Isolate only the lines that are potentially essentially automated. Then check whether the customer is B2C. Only those lines move into OSS review.

That does not mean you need to over-fragment every invoice. It means the lines have to be distinct enough that a reviewer can see why you kept some work out of the OSS lane and examined other lines more closely. If the line structure hides the distinction, you have lost a key control.

There is also a support-file point here. For any line that might move into OSS review, keep support showing how the delivery worked and why it was treated as potentially automated or not. For custom lines, keep the elements that show human input, revisions, and judgment. For potentially automated lines, keep the description that supports that characterization. You are not adding new facts. You are preserving the facts already in the job.

When the customer is B2C and the line is essentially automated, the next question is whether the line belongs in the relevant OSS review lane for your business facts. If you have neither a business establishment nor a fixed establishment in the EU, the Non-Union scheme is the scheme to evaluate, and you may choose any Member State of identification. If you do have an EU establishment or fixed establishment, the Union scheme path needs review instead.

That is where some teams rush and get into trouble. They treat OSS as a simple switch they can flip whenever they sell digitally into the EU. The draft is more careful than that. OSS is not a shortcut around classification. It is something you evaluate once the scope is clean and your establishment facts are understood.

A useful internal question at this stage is: if another reviewer looked only at the invoice lines and the support file, would they understand why some lines were kept separate? If the answer is no, your line descriptions may be too broad. Tighten them before you issue anything.

If treatment remains unclear across participating EU countries, evaluate a VAT Cross Border Ruling (CBR) only where the filing preconditions are met. Request it in the participating EU country where you are VAT-registered, following that country's national VAT-ruling conditions.

That is not your first move for ordinary ambiguity. It is an escalation path for cases where the participating-country treatment remains unclear after you have done the file work, the invoice QA, and the line split. The point is not to escalate early because a bundle is messy. The point is to escalate after you have produced a clean fact pattern and cannot resolve the treatment with supportable confidence.

Pre-Send Checklist and Escalation Triggers#

We use a hard release gate before sending: 100% field match, 0 unresolved identity conflicts, and escalation on mixed-scope files above $5,000 when establishment facts are unclear. As an operating target, keep a 95% first-pass QA rate and pause if more than 1% of invoices need reissue.

Use these red flags to decide when Step 3 is not complete:

- the engagement is bundled and the invoice does not separate custom work from potentially automated delivery,

- the service description is too vague to tell which lane a line belongs in,

- the customer type is not yet stable in the file,

- establishment or fixed-establishment facts are unclear,

- the Member State handling is uncertain,

- multiple participating EU countries create unresolved treatment questions.

If any of those remain open, do not use OSS as a shortcut. Hold the invoice or escalate with a complete pack.

Final rule: unresolved file, no invoice. Unresolved draft, no send. Unresolved mixed-scope classification, no OSS shortcut.

That final rule is worth repeating because it keeps the workflow honest. If you cannot identify the customer clearly, stop at Step 1. If the draft does not faithfully mirror the file, stop at Step 2. If the scope is mixed and you have not split the lines, stop at Step 3. Each stop is cheaper than sending a document you cannot support.

If your team needs a repeatable validation drill, adapt How to verify a European VAT number using the VIES system into your internal checklist so invoice QA and status verification stay in sync.

If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Before you issue the invoice, run the client record through the VAT Number Validator so your status check and invoice details stay aligned.

Once your VAT treatment is confirmed, create a clean final draft with the Free Invoice Generator to reduce avoidable reissues.

Frequently Asked Questions

Can you use reverse charge on every EU business invoice?

Not as a blanket rule based on the excerpts used here. They do not define reverse-charge eligibility, required reverse-charge wording, or invoice-level decision criteria. They do confirm that OSS is optional and scheme-specific, so treatment must be handled under the applicable local VAT rules. If the case is still unclear, keep the invoice on hold and use the local escalation path pending advisor or source verification.

What should you do if the VAT number fails in VIES?

The excerpts used here do not define a VIES validation workflow, pass/fail logic, or evidence standard. Use your local VAT-validation process and escalation policy for this case, and keep the invoice on hold until the local escalation path is confirmed and locally verified procedures are applied. If you need the mechanics, see How to verify a European VAT number using the VIES system.

Does invoice currency decide the VAT treatment?

No. These excerpts do not state that invoice currency determines VAT treatment. They focus on OSS/CBR mechanics, including OSS registration and filing obligations. Determine treatment under applicable local rules first, then finalize presentation choices such as currency and formatting.

How should you handle a mixed custom-plus-digital engagement before any OSS decision?

At this level, the confirmed points are high-level: OSS is optional, it has non-Union/Union/import schemes, and if you opt into a scheme you must declare all supplies that fall under that scheme via OSS returns, which are additional to domestic VAT returns. The excerpts do not define line-classification rules for mixed custom-plus-digital engagements, so treat the scheme-fit criteria as unresolved until advisor or source verification is complete and escalate when classification or establishment facts are unclear. Where establishment facts matter, the excerpts confirm that a taxable person with no EU business or fixed establishment may choose any Member State of identification for the non-Union scheme, while certain Union-scheme choices can restrict later changes to the Member State of identification.

When should you escalate to a specialist?

Escalate when the available facts and local rules are not enough to determine the correct OSS scheme, Member State of identification, or filing route. For advance-ruling routes, the excerpts confirm that VAT Cross-border Rulings (CBR) are a mechanism for complex cross-border VAT questions, and that any request must follow national VAT-ruling conditions in the EU country where it is submitted. A clean handoff should state the core transaction facts and the specific decision that remains unresolved, then note that the local escalation path is pending advisor or source verification. Related: The Silent Profit Killer: How to Stop Margin Erosion in Your Freelance Business.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Stop Freelance Profit Margin Erosion Before It Hits Cashflow

Revenue can hold steady while the business underneath it gets weaker. What comes in matters, but what you keep after the work is delivered is the clearer signal of health.

VAT MOSS and Non-Union OSS for UK Freelancers Selling to the EU

If you sell digital services from the UK to EU customers, treat UK VAT MOSS as historical and [Non-Union OSS](https://vat-one-stop-shop.ec.europa.eu/one-stop-shop_en) as the current route to assess. You cannot use UK VAT MOSS for sales made from 1 January 2021 onwards. For UK sellers who are not established and have no fixed establishment in the EU, the relevant OSS branch is the **Non-Union scheme**.