Quick Answer

Use HMRC's order for the tax year: automatic overseas tests first, automatic UK tests second, and sufficient ties only if status is still unresolved. Being under 183 days is not a safe conclusion by itself, because midnight presence, UK workdays, and prior residence history can still change the outcome. Keep same-day travel and work logs with tickets and boarding records so your position is supportable if HMRC asks for evidence.

Why the SRT is a Critical Risk to Your "Business-of-One"#

If you get your residence status wrong, it is not a technical footnote. It can change whether the UK taxes only your UK income or normally taxes income from both the UK and abroad for that tax year.

For a solo consultant, contractor, or freelancer, the UK statutory residence test is an operating risk, not just a tax concept. The practical questions are straightforward: what triggers UK residence, what happens next, and what evidence will you need if HMRC asks you to support your position?

Use the risk model that fits the SRT#

The first control point is the tax year. The test is applied year by year, using 6 April to 5 April. It is not a single rule. HMRC works through automatic overseas tests, automatic UK tests, and then the sufficient ties test if the automatic tests do not settle your status.

| Boundary | Fact | Note |

|---|---|---|

| 6 April to 5 April | The SRT is applied year by year | The first control point is the tax year |

| 183 days or more in the UK | Makes you resident under an automatic UK test | This is one boundary, not the whole analysis |

| Below 183 days in the UK | Does not end the analysis | Automatic overseas tests, automatic UK tests, and, if needed, the ties test may still matter |

| Fewer than 16 days | Automatic overseas treatment can apply for some people | Prior UK residence history matters |

| 46 days | Automatic overseas treatment can apply for some people | Prior UK residence history matters |

| Sufficient ties test | Used if the automatic tests do not settle your status | The number of ties that matters changes with UK day count and prior residence history |

That is why the usual shortcut fails. Spending 183 days or more in the UK makes you resident under an automatic UK test, but being below 183 days does not end the analysis.

Use this rule instead. If your plan is "stay under 183 days," replace it with "verify my actual threshold first, then manage ties against that threshold." For some people, automatic overseas treatment can apply at fewer than 16 days or 46 days, depending on prior UK residence history. For others, ties decide the outcome, and the number of ties that matters changes with both UK day count and prior residence history.

What HMRC is really checking#

| Common assumption | What HMRC actually tests | Safer default action |

|---|---|---|

| "Under 183 days means I'm fine." | Under 183 days can still require the rest of the SRT analysis (automatic overseas tests, automatic UK tests, and, if needed, the ties test). | Treat 183 as one boundary, not your planning rule. |

| "A UK day is any day I land there." | A UK day is generally based on being in the UK at midnight, subject to specific exceptions. | Track arrivals, departures, and where you are at midnight. |

| "A few client calls from London do not matter." | A work tie can arise if you work more than 3 hours in the UK on at least 40 days in the year. | Log UK workdays separately and do not rely on memory. |

| "One document proves where I live." | HMRC expects records and documents, and one piece of evidence is usually not enough to prove a UK or overseas home position. | Keep a consistent evidence pack across travel and accommodation records. |

The evidence burden is part of the cost#

If you are taking a non-resident position, a confident spreadsheet is not enough. HMRC expects records and documents to support the statements you make for the test. In practice, that means keeping tickets and boarding cards, including etickets, plus a day log showing where you were at midnight. If home or accommodation is relevant, build an evidence pack rather than a one-document story, because HMRC looks at evidence cumulatively.

Use this checkpoint: could you reconstruct your UK days and accommodation position for the full tax year without guessing? If not, your risk is already higher than it looks. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

What goes wrong in practice#

A common failure sequence is simple and expensive: status error, then return correction, then cash-flow pressure, then admin drag. HMRC gives a 12 month window after the Self Assessment deadline to correct a filed return. If that correction increases tax, you can face extra tax due, interest, and potentially penalties.

| Issue | Timing or amount | Detail |

|---|---|---|

| Return correction | 12 month window after the Self Assessment deadline | HMRC gives this window to correct a filed return |

| Late filing | £100 | Late filing can start at this level |

| Additional late filing | £10 per day up to £900 | Further charges can follow later |

| Late payment | 5% penalties at 30 days, 6 months, and 12 months | Interest can also apply |

| Inaccuracy | Potential penalties | May apply if the return is inaccurate and tax was understated |

Then comes the admin burden. You may need to rebuild a full year of facts from travel records, calendars, and messages. If deadlines were missed, late filing can start at £100, then £10 per day up to £900, with further charges later. Late payment can add 5% penalties at 30 days, 6 months, and 12 months, plus interest. If HMRC considers the return inaccurate and tax was understated, inaccuracy penalties may also apply.

So the job is not just to count fewer days. It is to manage the ties that can turn routine UK presence into a residence issue. That is the next step.

Your Control Panel: Managing the Five Sufficient Ties#

Once you are in the ties stage, treat this as a practical control-panel problem. the exact tie triggers, tie thresholds, and tie-to-risk-zone mechanics are not verified, so confirm the current rules before you plan travel, UK work blocks, or accommodation around them.

Use this operating rule: run verified filing controls in parallel with tie verification.

| Tie | Verification status | Common mistake | Best preventive action |

|---|---|---|---|

| Family | Trigger criteria are not verified here. | Treating this tie as confirmed without checking current rules. | Verify current criteria before relying on this tie in your plan. |

| Accommodation | Trigger criteria are not verified here. | Treating this tie as confirmed without checking current rules. | Verify current criteria before relying on this tie in your plan. |

| Work | Trigger criteria are not verified here. | Treating this tie as confirmed without checking current rules. | Verify current criteria before relying on this tie in your plan. |

| 90-day | Lookback criteria are not verified here. | Treating this tie as confirmed without checking current rules. | Verify current criteria before relying on this tie in your plan. |

| Country | Country-comparison criteria are not verified here. | Treating this tie as confirmed without checking current rules. | Verify current criteria before relying on this tie in your plan. |

The five ties in practical terms#

This section works best if you separate tie analysis from filing operations. The tie mechanics still need current-rule verification, but these compliance controls are clear:

| Filing control | What the article says | Detail |

|---|---|---|

| Self Assessment registration | Register if you need to file for the previous tax year | For 6 April 2024 to 5 April 2025, the deadline shown here is 5 October 2025 |

| Account reactivation | Check whether an existing Self Assessment account needs reactivation before filing | Filing without reactivation may delay the return |

| Record keeping | Keep records to support your return | Examples given are bank statements or receipts |

| Filing route | Confirm early whether the online filing service can be used | It cannot be used in some cases if you lived abroad as a non-resident |

| Payment date | Plan for the Self Assessment tax bill date | The date shown here is 31 January |

- Tell HMRC by registering for Self Assessment if you need to file for the previous tax year. For 6 April 2024 to 5 April 2025, the deadline shown here is 5 October 2025.

- If you already have a Self Assessment account, check whether it needs reactivation before filing, because filing without reactivation may delay the return.

- Keep records to support your return, including bank statements or receipts.

- Confirm your filing route early if you lived abroad as a non-resident, because the online filing service cannot be used in some cases.

- Plan for payment timing: the Self Assessment tax bill date shown here is 31 January.

Tie mapping is still useful, but do not treat unverified tie mechanics as settled until you confirm the current rules. You might also find this useful: A Guide to the Best No-Code Tools for Freelancers.

The Hard Boundaries: Automatic UK and Overseas Tests#

The order matters here. Check automatic overseas tests first, then automatic UK tests, and use sufficient ties only if neither stage gives a conclusive answer.

If you meet an automatic overseas test, stop there for that tax year. If you do not, move to the automatic UK tests. Only when both stages are inconclusive should you go on to ties.

Run the sequence in this order#

Start by confirming your residence history for the prior three tax years, where relevant, and your UK day count using the midnight method. Then check whether deeming-rule days must be added after the first 30 qualifying days.

If no automatic overseas test is met, move to the automatic UK tests, including the 183-day test, the UK home test, and the UK full-time work test.

| Automatic test | What it asks | What records you need | Common failure mode |

|---|---|---|---|

| Automatic overseas tests | Do you qualify as conclusively non-resident based on residence history, UK days, and, where relevant, work pattern? | Prior-year residence position, travel ledger, tickets and boarding records, UK work log with dates and hours | Skipping status-history checks or undercounting UK workdays and day-count details |

| Automatic UK day-count test | Did you spend 183 days or more in the UK in the tax year? | Midnight-based day log, travel records, supporting movement evidence | Counting trips loosely instead of applying midnight and deeming rules |

| Automatic UK home test | Did you meet the UK home conditions for at least one 91-day consecutive period (with at least 30 days in-year) and, if relevant, spend fewer than 30 days in each overseas home? | Lease or ownership records, occupancy timeline, overseas-home evidence, calendars | Treating any available place as a "home," or relying on one document as proof |

| Automatic UK full-time work test | Did you meet the full-time UK work conditions over the required period? | Contracts, timesheets, diaries, invoices, meeting logs, payment records | Reconstructing work patterns late instead of keeping same-day records |

Keep the UK home test and accommodation tie separate#

Do not merge these rules. The automatic UK home test sits in the automatic-residence stage. The accommodation tie sits in the ties stage and can apply even when you do not have a UK home.

In practice, accommodation can be more transient than a home. A short-term UK base can still matter later as a tie, even if it does not meet the home test now.

A practical checklist before you move to ties#

Before you move to ties, make sure you have four things pinned down:

- your residence history for the required prior period

- your UK day-count method, including the midnight rule and any deeming-rule exposure

- your home and work evidence pack, dated, consistent, and complete

- whether the facts are mixed or borderline enough to justify specialist review

If your outcome turns on close thresholds, overlapping home facts, or incomplete travel or work logs, consider qualified advice before finalizing your position. Related: Understanding the UK's Statutory Residence Test (SRT).

Strategic Scenarios: The Framework in Action#

If your residency position is unclear, the real job is to control the facts early and keep filing readiness in step. Even then, weak records or filing-access issues can still create avoidable risk.

| Profile state | Likely pressure points | Primary risk if unmanaged | Practical control move |

|---|---|---|---|

| You live abroad but return to the UK for recurring client work | Recurring UK workdays, overnight stays, frequent returns | You cannot show where work happened or how UK presence built over time | Keep a same-day travel and work ledger, and separate UK workdays from pure travel days |

| You live abroad and make frequent family visits to the UK | Frequent UK visits, accommodation use, overnight presence | Personal trips are under-documented and later look like broader UK presence | Track each UK midnight and keep booking, payment, and visit-purpose records |

| You are considering moving back after a period abroad | Changing accommodation, changing work locations, timing of return plans | You plan the move but miss account reactivation, registration, or filing-route constraints | Build a filing checklist before arrival and confirm whether the standard online route fits your case |

Scenario A#

Situation: You are mostly based outside the UK, but you return for in-person client work in short bursts. Risk trigger: Repeated trips can stack UK work and UK presence at the same time, and rough notes are not reliable when the facts are close. Safer default: Keep a same-day ledger showing your midnight location, whether UK work happened, and the supporting proof.

If the year may end up being UK-reportable, set up filing early. First-time filers must register for Self Assessment before using the online service, and registration requires a National Insurance number. Evidence to retain: Contracts, invoices, meeting logs, tickets, accommodation confirmations, bank statements, and receipts. Your records should line up without late reconstruction. Escalation rule: Escalate when your position depends on close day tracking, mixed travel and work days, or unclear treatment of repeated UK stays. Also escalate early if you lived abroad as a non-resident. Some cases cannot use the standard online filing service and may need commercial software or other forms.

Scenario B#

Situation: You work abroad full time, but family reasons bring you to the UK regularly. Risk trigger: The problem is usually not the travel itself. It is poor documentation of overnight presence, stay patterns, and supporting records. Safer default: Treat personal UK visits with the same discipline as business travel. Log arrivals, departures, and where you stayed, so your year file is usable if a return is needed.

Evidence to retain: Booking emails, travel confirmations, calendar entries, bank statements, and receipts with clear dates and locations. Escalation rule: Escalate when your records conflict, or when family access to UK accommodation is informal, shared, or open-ended enough that the facts are no longer clear.

Scenario C#

Situation: You are testing a return to the UK after time abroad, with changing work and living arrangements. Risk trigger: This creates two risks at once: a finely balanced residency assessment and filing-access failures when deadlines get close. Safer default: Run a dual track from day one. Keep travel, accommodation, and work records as you go, and verify filing status early.

If you registered before but did not file last year, you may need to reactivate your Self Assessment account, and filing without reactivation may delay your return. Online filing opens on or after 6 April following tax year end, and the tax bill is due by 31 January. Evidence to retain: Lease or accommodation records, invoices, receipts, bank statements, and HMRC registration or reactivation messages. If you operate as a sole trader, remember this is handled through Self Assessment registration. The GOV.UK example for the 2024 to 2025 tax year used 5 October 2025 as the notification date, so verify the current-year date before relying on it. Escalation rule: Escalate when the year includes a move back, overlapping work locations, or an outcome that turns on finely balanced facts.

We covered this in detail in A Deep Dive into the 'Habitual Residence' Test in the UK. Want to test your plan before booking travel? Use the tax residency tracker to keep your day-count and trip notes in one place.

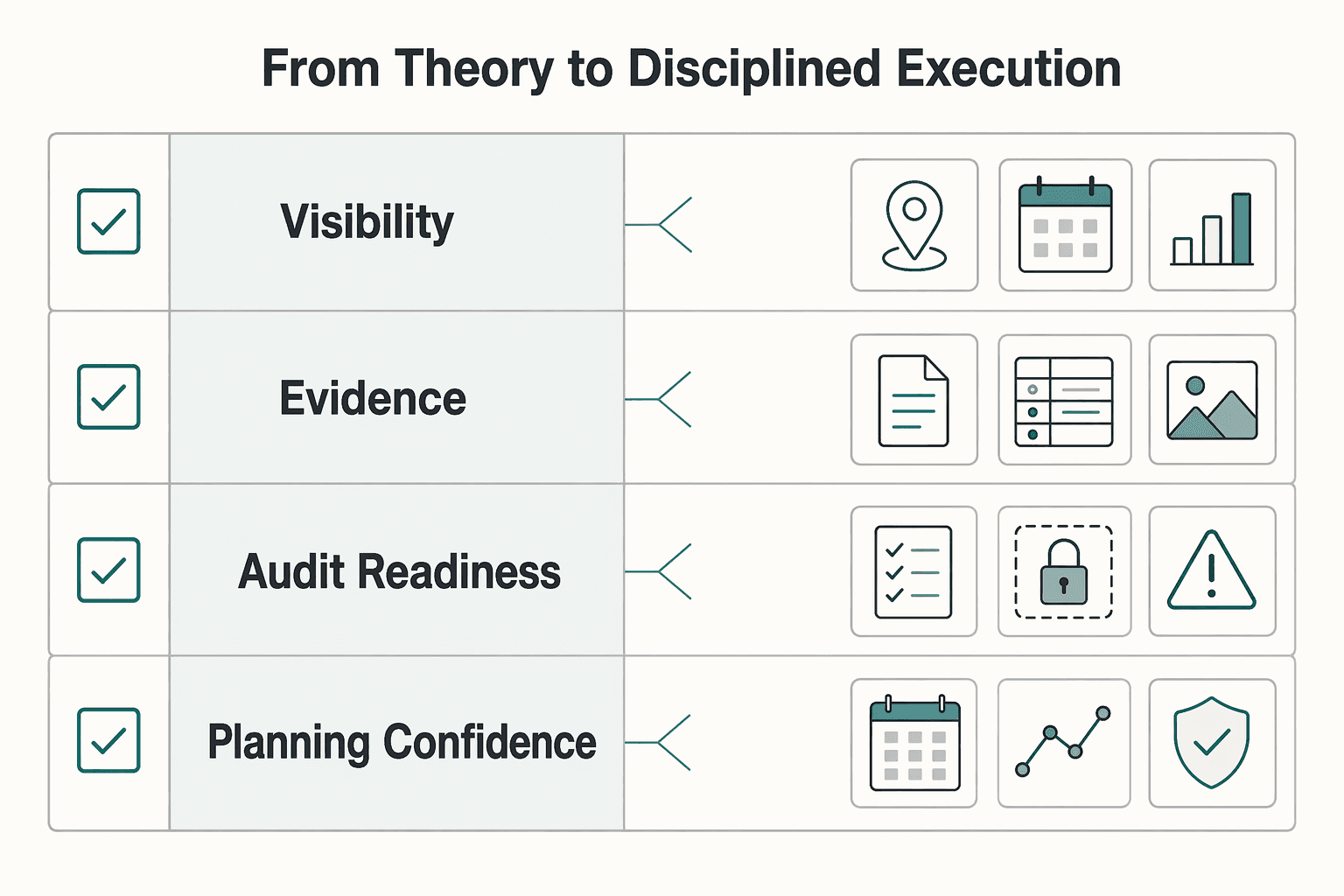

Your Action Plan: From Theory to Disciplined Execution#

For the SRT, execution beats theory. File from records you can explain and support, not from memory.

Treat your residency file as part of your tax return process. If this is your first Self Assessment return, register before using the online filing service. In HMRC's current example window, you must tell HMRC by 5 October 2025 for the tax year 6 April 2024 to 5 April 2025. You can file on or after 6 April after year end, and payment is due by 31 January. Confirm that you have your National Insurance number for registration and UTR for filing. Also check whether an older account needs reactivation, since filing without reactivation may delay your return.

| Area | Ad-hoc tracking | Disciplined system |

|---|---|---|

| Visibility | You rebuild dates from memory, inboxes, and scattered apps. | You track key dates and tax-year cutoffs in one place. |

| Evidence quality | Records are incomplete or inconsistent. | Bank statements, receipts, and tax records are organized and consistent. |

| Audit readiness | Questions trigger a scramble for documents. | Your core evidence pack is already organized. |

| Planning confidence | Trips get added without checking downstream impact. | You review potential tax implications before confirming travel. |

To make that system real, keep this checklist current:

- Travel log (if relevant): entry and exit dates, tickets, boarding passes, and calendar cross-checks

- Accommodation/work notes (if relevant): key records that support where you stayed and worked

- Self Assessment access checks: registration complete, National Insurance number and UTR available, and account reactivated if needed

- Filing-route check: confirm whether you can use HMRC's online service or need commercial software or other forms

- Document storage routine: one folder per tax year for bank statements, receipts, filing confirmations, and HMRC messages

Run one filing-route check early. HMRC says the online service is not available in some situations, including living abroad as a non-resident, and directs you to commercial software or other forms instead.

If your records conflict or your residency position is unclear, pause self-assessment and move to professional review before filing.

For a step-by-step walkthrough, see The Bona Fide Residence Test: A Deep Dive for US Expats.

If you want invoicing, payouts, and audit-ready records in one cross-border workflow where supported, review Gruv for freelancers.

Frequently Asked Questions

Do I need to register for Self Assessment?

If you need to complete a tax return, you must tell HMRC by 5 October. If you are filing for the first time, register for Self Assessment before using the online filing service. Telling HMRC late can lead to a penalty.

I was registered before but did not file last year. What now?

You may need to reactivate your Self Assessment account. If you file without reactivating an existing account, your return may be delayed.

What do I need to file online?

You need your Unique Taxpayer Reference (UTR) to sign in and file online. Keep records such as bank statements or receipts so your return is complete.

What if I cannot use HMRC’s online filing service?

HMRC lists cases where the online service is not available, including if you lived abroad as a non-resident. In those cases, use commercial software or download/request other forms instead.

When is payment due?

You can file your return any time on or after 6 April after the tax year ends. You’ll need to pay your tax bill by 31 January.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Understanding the UK's Statutory Residence Test (SRT)

Treat SRT like ops, not folklore. You want a repeatable workflow you can run monthly so your tax-year answer is boring, documented, and easy to defend.

Best No-Code Tools for Freelancers Who Need Clean Handoffs

Choose for maintainability first. If you do repeat client work, the right no-code tools are the ones you can still explain, hand off, and troubleshoot a year later. A strong demo matters far less once real client data, deadlines, and day-to-day edits show up.