Quick Answer

A UK creative director with a US LLC should sort filing readiness, residency evidence, and LLC classification before trying to optimize tax or take distributions. The article recommends confirming Self Assessment status, UTR and account access, building one evidence pack, using IRS Publication 519 to lock U.S. status and filing logic, and pausing non-routine withdrawals when classification or treaty assumptions remain unresolved.

Start Here if You're a UK Creative Director With a US LLC#

Start with filing readiness, not tax optimisation. This guide is for you if you're using a US LLC and filing, or expecting to file, a UK Self Assessment return. Its purpose is to reduce avoidable filing risk and keep your position defensible. It is not a promise that this structure will lower your total tax bill.

For cross-border treatment, assume uncertainty until you verify it. The safest first move is to get the compliance sequence right.

Before You Start#

| Item | Action | Key detail |

|---|---|---|

| Self Assessment need | Confirm whether you need to complete a UK Self Assessment tax return | Relevant tax year |

| First-time filing | Register for Self Assessment before using HMRC's online filing service | Before first online filing |

| UTR and account status | Make sure you have your Unique Taxpayer Reference (UTR) and check whether your Self Assessment account needs reactivation | HMRC's online service requires a UTR |

| Records | Keep records needed to complete your return correctly | Bank statements or receipts |

| Key dates | Tell HMRC by 5 October; file online on or after 6 April following the end of that tax year; pay by 31 January | Previous tax year / filing cycle |

Work through each row before you start filing.

These are not admin details to skim past. HMRC's online service requires a UTR, and filing without reactivating an existing account can delay your return. If you lived abroad as a non-resident, the standard online route may not apply.

What this guide will and will not do#

This guide helps you work in the right order: facts first, then treatment, then decisions. It is designed to reduce preventable timing and filing errors and make adviser conversations faster when you need them.

It does not resolve complex edge cases on its own. If your facts include dual residency, major cross-border moves in the year, or a disputed view of LLC treatment, treat that as a professional-advice point.

The operating rule for the rest of this article#

Treat uncertainty as compliance risk, not as a tax-saving assumption. Filing earlier can help you know what you owe sooner, but only once your filing setup and records are in order.

If you want a deeper dive, read Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers.

Define the outcome before you optimize anything#

Choose the outcome first, then optimize. If you skip this step, it becomes too easy to justify positions you may not be able to defend later.

Choose one primary objective#

Write down one primary objective: lower compliance stress, lower audit risk, or lower overall tax drag. Pick one and use it as your decision filter.

If your priority is lower compliance stress, start with HMRC filing readiness. Confirm whether you need Self Assessment, whether you must register before first-time online filing, and whether an older account needs reactivation. In HMRC's example for the tax year 6 April 2024 to 5 April 2025, telling HMRC after 5 October 2025 could trigger a penalty. Filing without reactivating an existing account may also delay processing.

Set your risk tolerance in plain language#

Set your risk tolerance in plain language. For example: "I only use positions I can explain with records and filing evidence," or "I accept some uncertainty, but not if it affects payment timing by 31 January."

Keep a one-page checkpoint note with your chosen objective, current filing status, and the records you already have, such as bank statements or receipts. If an adviser cannot understand your position quickly from that note, pause optimization.

Use a hard-stop rule for distributions#

Use one hard-stop rule for distributions: if your structure depends on one untested classification or filing assumption, pause and validate it before you take money out. For limited companies, directors must follow specific rules when taking money out.

The core risk is a mismatch between what you assumed, what you filed, and what your records later show. Until that assumption is validated, treat cash movement as a decision point, not routine admin.

Related reading: A Guide to Portugal's NHR Tax Regime for a US-Based Management Consultant.

Gather your facts and documents before making structural decisions#

Before you change structure, build one evidence pack. If you cannot hand it to an adviser and get a clear, defensible read, you are not ready to optimize.

Set up one evidence folder#

Create one folder with four subfolders: UK residency, LLC formation and elections, prior filings, and reference materials. Use clear file names so the timeline is readable without explanation. That makes it easier to hand the pack over without a separate walkthrough.

| Subfolder | What to include | Use |

|---|---|---|

| UK residency | Dated travel records; a dated timeline of where you lived and worked; records showing when key facts changed during the year | UK residency review |

| LLC formation and elections | Formation documents; operating agreement; EIN confirmation; ownership records; tax election paperwork, including any check-the-box filing if one exists | Answer who owns the LLC, what elections were made, and when they took effect |

| prior filings | UK Self Assessment working papers; submitted returns; prior U.S. individual return drafts or filings; IRS notices or correspondence | Prior filings and current filing signals |

| reference materials | IRS Publication 519 in the 2025 edition; authorities; adviser input you expect to rely on later | Keep source text and notes separate, and date both |

Collect UK residency records#

Collect documents for your UK residency review, including dated travel records, a dated timeline of where you lived and worked, and records showing when key facts changed during the year.

Keep this as evidence gathering, not conclusion forcing. This U.S.-focused checklist does not resolve UK residency status, so if status is still unclear, mark it as unresolved and treat it as a decision gate.

Pull the full U.S. LLC record set#

Pull the full U.S. LLC record set: formation documents, operating agreement, EIN confirmation, ownership records, and tax election paperwork, including any check-the-box filing if one exists.

Your folder should let you answer three basic questions from documents alone: who owns the LLC, what elections were made, and when they took effect.

Assemble prior filings and U.S. filing references#

Assemble prior filings and current filing signals: UK Self Assessment working papers, submitted returns, prior U.S. individual return drafts or filings, and all IRS notices or correspondence.

Keep IRS Publication 519, 2025 edition, in the same pack as your U.S. filing reference. Use its core checkpoints in order: Chapter 1 for the status question, nonresident alien versus resident alien; Chapter 7 for filing guidance on p. 48; and Chapter 9 for treaty discussion on p. 64. This status call matters because resident aliens are generally taxed on worldwide income, while nonresident aliens are taxed only on U.S.-source income.

Remove irrelevant assumptions early. Form 990 is for exempt organizations, not a default individual filing document for this scenario.

Separate authorities from facts#

Create a source folder for authorities and adviser input you expect to rely on later, and keep your adviser notes with dates.

Keep source text and your notes separate, and date both. The goal at the end of this step is simple: one pack of facts, one pack of references, and a short list of missing documents before you touch restructuring or distributions.

Step 1: Confirm residency and control facts that drive the whole analysis#

Lock down your residency evidence and control timeline first. If either is unclear, mark it unresolved and pause conclusions until you have advice. The GOV.UK pages used here do not set out detailed SRT or treaty tie-breaker rules.

Build the residency timeline from dated records#

Build your timeline by UK tax year, not from memory. HMRC's example frame for the previous year is 6 April 2024 to 5 April 2025, so map key dates and work-location changes to clear records before drawing conclusions. If your records do not support a clear answer, mark the position unresolved and escalate. If you need a process refresher, use Understanding the UK's Statutory Residence Test (SRT).

Document who controls day-to-day decisions#

Write down who makes day-to-day decisions and where those decisions happen in practice. GOV.UK flags control-style indicators like deciding how, where and when work is done and who takes responsibility for success or failure. Capture evidence that reflects real conduct, not just formation paperwork.

Split the year when facts changed#

If residence pattern, work location, or decision-making changed mid-year, break the timeline into dated periods. Keep each period factual and separate so later analysis rests on stable facts, not a blended year-end summary.

Check proof before finalizing your position#

If you cannot show who made key day-to-day decisions, where, and when, flag that gap before you finalize your position. Keep supporting records organized, such as bank statements or receipts, so you can complete filing accurately.

Handle HMRC admin timing early as well. Tell HMRC by 5 October if you need to file for the previous year. File online on or after 6 April, and plan for payment by 31 January. If you have an existing but inactive Self Assessment account, reactivate it first to avoid delays, and confirm your UTR is ready for online filing.

Step 2: Classify likely UK treatment of your LLC before planning distributions#

Before you plan withdrawals, write down a provisional UK classification view for the LLC and mark anything unproven. The real risk is not only being wrong. It is acting on a position you cannot evidence later.

Step 2.1 Separate confirmed UK process facts from open LLC classification questions#

Use confirmed UK process facts as guardrails: business structure affects tax and legal responsibilities, and directors must follow rules when taking money out of a limited company. Keep those points as guardrails, but do not treat generic UK structure guidance as proof of how a US LLC is classified for UK tax.

Build a working note in plain English: what is confirmed, what is assumed, what document supports each point, and what is unresolved.

Step 2.2 Treat manual- or case-based conclusions as unconfirmed#

Confirm HMRC International Manual positions on US LLC classification with HMRC directly, and confirm whether Anson applies to your specific facts with a qualified adviser. Treat any transparency-versus-opacity conclusion as open unless you have verified primary material.

A useful check is a short paragraph titled "What is confirmed vs still unproven for my LLC classification." If that paragraph depends on missing documents or assumptions, the position is still open.

Step 2.3 Build a comparison table before any distribution decision#

Use a compact table so you separate confirmed process points from open classification issues. If multiple rows stay unresolved, treat classification as ambiguous.

| Checkpoint | Confirmed UK point | Open question to flag | Evidence weakness to flag |

|---|---|---|---|

| Structure and duties | Business structure affects tax and legal responsibilities | Does this determine your US LLC treatment in UK tax? (not confirmed here) | Assuming an outcome from generic guidance |

| Taking money out | Directors must follow rules when taking money out of a limited company | Which withdrawal rules apply to your facts | Missing dated approvals or payment trail |

| Self Assessment timing | Tell HMRC by 5 October if you need a return for the previous year; returns can be sent after 5 April; tax bill is due by 31 January | How these dates apply to your filing facts | No clear filing calendar |

| Filing readiness | Keep records (for example bank statements or receipts); filing without reactivating an existing account may delay a return | Whether online filing exclusions apply (including non-resident abroad cases) | Weak records or unchecked account status |

| Status uncertainty | HMRC says to contact them if you are not sure whether you are trading | What HMRC guidance says for your situation | No dated note of advice received |

Step 2.4 Escalate ambiguity before large withdrawals#

If key points are still open, pause non-routine withdrawals until you can evidence your position. Keep records tight while the position is open: legal documents, payment records, bank statements, receipts, and a dated note of what you decided and why. If you are unsure whether you are trading, contact HMRC. Related: Tax Implications for a UK Resident Owning a US LLC.

Step 3: Test treaty relief feasibility instead of assuming credits will work#

After Step 2, treat treaty relief as something to validate, not as a cashflow assumption. If your outcome depends on a disputed characterization, mark that assumption as non-bankable until your U.S. filing facts are stable.

Step 3.1 Confirm your U.S. filing facts before treaty analysis#

Start with the U.S. basics: tax residency status, income scope, and filing identity. IRS Publication 519 distinguishes resident and nonresident alien treatment. That changes what income is in scope: worldwide income for resident aliens, and U.S.-source and certain U.S.-connected income for nonresident aliens.

Use a short checkpoint note for the year:

- What U.S. status you are using.

- Why that status is reasonable on your facts.

- Which income is U.S.-source or otherwise in U.S. scope.

- Whether a U.S. federal return is required for your facts.

- Whether you have the required SSN or ITIN for returns and related tax documents.

Only then move to treaty analysis. Publication 519's treaty discussion in Chapter 9 is useful after those inputs are clear.

Step 3.2 Compare mismatch vs alignment before you model relief#

Build a side-by-side table to test whether your positions across jurisdictions are documented consistently. The point here is feasibility discipline, not proving a treaty outcome.

| Test point | Mismatch scenario | More aligned scenario | Failure mode to include |

|---|---|---|---|

| Who is taxed | Your filings identify different taxpayers or treatment layers without a clear reconciliation note | Your filings clearly document how each jurisdiction treats the same income stream | Unresolved characterization gaps can delay filings or change expected relief timing |

| Income in scope | U.S. scope and non-U.S. scope are mapped differently or incompletely | Income mapping is consistent across filings | Scope mapping errors force amendments or change expected offsets |

| Filing mechanics | Missing identifier (SSN/ITIN where required), incomplete withholding trail, or unclear filing position | Filing identity and document trail are complete | Operational gaps weaken any relief position and create cashflow stress |

| Cashflow plan | Spending assumes relief arrives on schedule | Cash reserve covers uncertainty while facts are confirmed | You distribute early, then need to fund tax and cleanup later |

Step 3.3 Use a hard distribution rule while facts are unresolved#

If your plan only works if relief lands exactly as expected, pause non-routine distributions. Keep liquidity based on the higher plausible near-term tax outcome until your U.S. status, income scope, and filing identity are documented and internally consistent.

Also account for timing risk. Special withholding rules can apply in some nonresident cases before final filing positions are settled. Keep a dated memo of assumptions and clearly label contested assumptions as non-bankable.

Step 4: Map required filings and sequence them in the right order#

Turn uncertainty into a clean filing matrix before any non-routine distributions. If the sequence is wrong, you can end up filing against the wrong taxpayer story and fixing it later under cash pressure.

Step 4.1 Build the matrix before you touch distributions#

Use a short matrix with four fields: potential filing or admin track, trigger condition, dependency, and evidence. Keep each row conditional until the underlying assumption is documented.

| Potential track | When to include it | What must be confirmed first | Evidence to attach |

|---|---|---|---|

| Home-jurisdiction income-tax return track | Include as a non-U.S. income-tax workstream to confirm | Local residence position and local characterization of LLC income | Residence note, classification memo, income mapping draft |

| U.S. nonresident filing track | Include if your U.S. status and income scope point to nonresident treatment | U.S. status for the year and whether income is in U.S. scope | U.S. status memo, source or scope note |

| Effectively connected income (ECI) question | Include when U.S. trade or business connection could affect U.S. filing treatment | Whether income is connected with a U.S. trade or business on your facts | Short ECI analysis memo and current conclusion status |

| Other state-level or admin obligations | Include as a separate admin track so it is not lost inside income-tax analysis | Whether activity creates separate state-level indirect-tax or admin follow-up | State issue log and operating-footprint notes |

Keep income-tax positions and indirect-tax or admin checks on separate rows. One does not automatically resolve the other.

Step 4.2 Use the right order of operations#

Use this order and do not skip ahead:

- Confirm U.S. tax status for the year.

- Confirm income scope for that status.

- Test treaty position.

- Finalize filing positions.

- Execute distributions.

For U.S. mechanics, use Publication 519 as the operational anchor: status first, then filing execution. Route forms, timing, and where-to-file questions to Chapter 7. Check Chapter 6 if the year may involve dual-status treatment. Test treaty-dependent positions under Chapter 9 before locking returns.

Step 4.3 Tie every filing position to one assumption#

Each filing row should tie to one named assumption, usually status, income scope, or treaty. If you cannot point to the assumption and its memo, the row is not ready to finalize.

This matters because status changes tax scope. Resident alien and nonresident alien treatment are not interchangeable, and that distinction drives what belongs in the U.S. filing position.

Step 4.4 Watch the common break points#

Two break points create most cleanup work: treating a possible dual-status year as a single-status year, and finishing income-tax analysis while admin obligations remain untracked. If a filing outcome still depends on a disputed assumption, mark it provisional and keep distributions on hold until the filing story is internally consistent.

For another treaty example, see A Deep Dive into the 'Dividend' Article of the US-Germany Tax Treaty for LLC Owners.

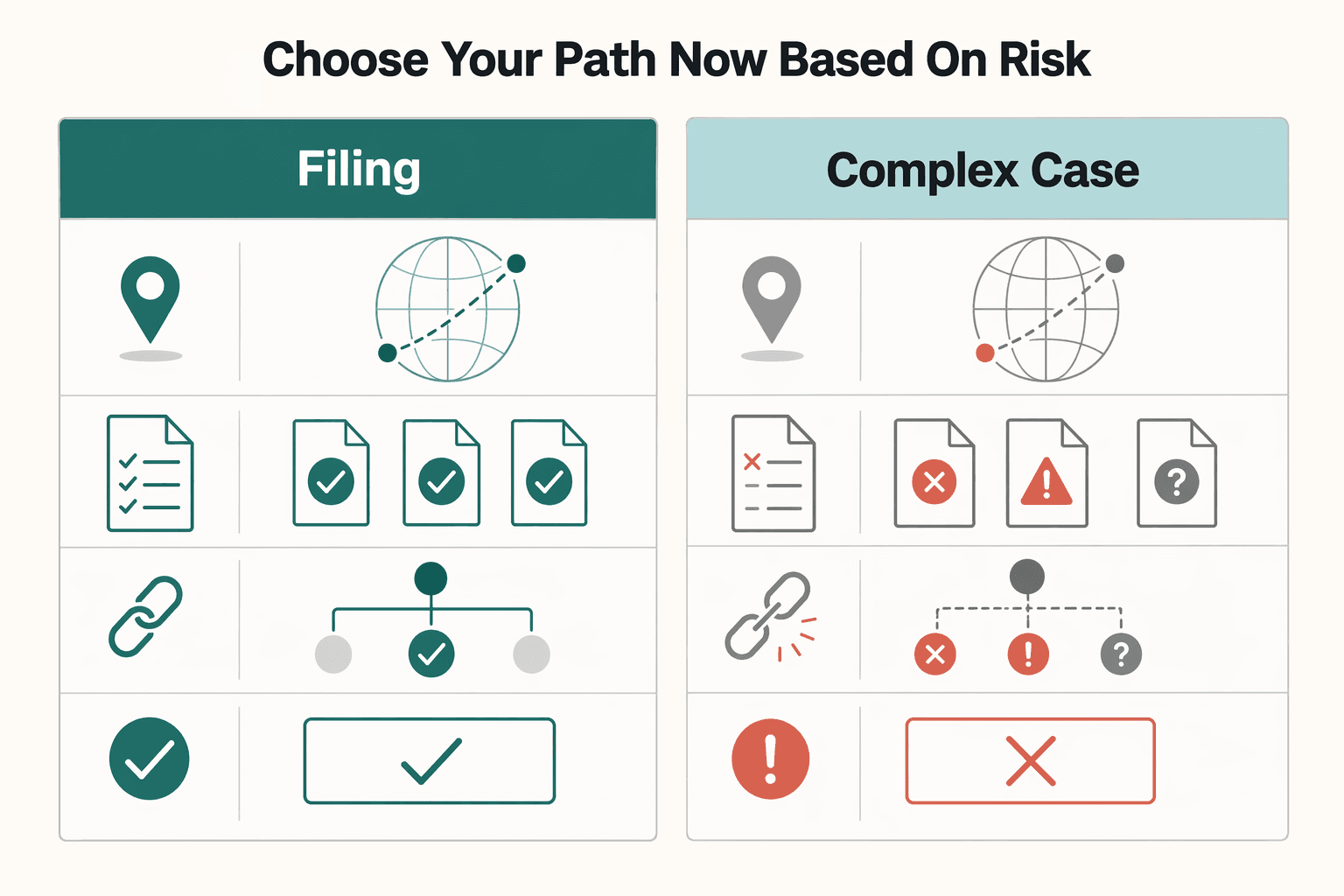

Step 5: Choose your path now based on risk, not hope#

Choose the path that still works if a tax authority asks you to prove each assumption. If key points are still unresolved, take that as a decision signal and keep non-routine distributions on hold. Do not assume a specific UK treatment of a U.S. LLC until that treatment is explicitly confirmed.

| Path | Choose it when | What you should already have | Main downside |

|---|---|---|---|

| Keep the current US Limited Liability Company (LLC) | Your U.S. residency status and filing position are documented and internally consistent | Status memo, filing matrix, SSN or ITIN status, distribution policy note | Harder to defend later if authorities challenge taxpayer alignment or timing |

| Controlled restructure | The risk is structural and core assumptions are still unresolved | Written change plan, year-by-year filing impact draft, adviser review points, hold on non-routine payouts until the change date is clear | Transition-year complexity, including possible dual-status review on the U.S. side |

| Pause distributions pending specialist sign-off | Facts are mixed and your outcome depends on a disputed tax treaty interpretation | Frozen payout decision, cash buffer plan, adviser question list, evidence pack with prior filings and entity records | Slower access to cash and higher near-term advisory cost |

Step 5.1 Keep the LLC only if your filing story is stable#

Keep the current structure only if Step 4 produced a filing position that is no longer provisional. On the U.S. side, determine tax residency status before filing: resident alien and nonresident alien treatment are different, and that changes tax scope. If you are treated as a nonresident artist or athlete with U.S.-source income, U.S. income tax and a federal return are generally required. If status is still open, this is not the low-risk path.

Before you approve distributions, confirm the return can be filed with the right taxpayer story and identifier. SSN or ITIN must be available for tax returns and related tax documents. If the year may be split, resolve that first and review dual-status filing implications.

Step 5.2 Restructure when uncertainty is built into the structure#

If paperwork is not the main problem, a controlled restructure can be safer than ad hoc fixes after cash moves. This is the risk-first option when your position depends on unresolved structural assumptions.

Avoid the common mistake of distributing first and trying to retrofit explanations later. Set a clear change date, map filing effects by tax year, and keep non-routine payouts paused until the new structure is actually in place.

Step 5.3 Pause immediately when treaty interpretation is doing all the work#

If your result only works under one disputed treaty reading, escalate now. Treaty-dependent positions need specialist review before the next payment cycle, especially when taxpayer alignment or entity treatment is still contested.

In mixed-fact years, pause distributions, assemble your evidence pack, and get sign-off before filing positions harden. If your case falls under foreign artist/athlete rules, payments may be subject to special U.S. withholding, and a Central Withholding Agreement can be used to align withholding with net income.

Build an audit-ready record trail from day one#

Build one evidence pack now, before the next payment moves, so you can show exactly how facts became filing numbers. That matters most when deadlines, account status, and filing decisions depend on the same small set of records.

Keep one master evidence pack#

Use one folder for the full filing trail, including prior filing records, account status records, and the core documents behind your return.

Include key UK checkpoints in the same pack:

- If you need to file a UK return, tell HMRC by

5 Octoberfor the previous tax year. - Missing that notification date can lead to a penalty.

- If you had an existing Self Assessment account, keep proof of reactivation where needed, because filing without reactivating can delay the return.

- Keep a dated reminder that Self Assessment tax bills are due by

31 January.

Log your treatment decision and fallback#

Write a short memo that states the facts you relied on, the filing position you took, and the guidance you considered. Then keep a decision log that records:

- Why you took that filing position

- What facts would trigger a re-check

- What your fallback action is if the position is challenged

Reconcile filing totals to underlying records#

Your return totals should tie back to records you can produce. Keep bank statements or receipts, as HMRC advises, along with invoices and payout records used in your reporting process.

Where supported, Gruv exports and traceable payout records can strengthen operational defensibility. Use them as supporting evidence, not as a substitute for your core tax analysis and source documents.

If U.S. information returns apply, save e-filing evidence from the system you used:

- IRIS is available from

January 1, 2026. - Prior-year Forms 1042-S and foreign filer submissions must continue through FIRE until retirement.

- For due dates in this transition period, keep submission receipts and acknowledgment IDs with the rest of your file.

Minimize sensitive data in working files#

Keep only the personal data you need in day-to-day files. Use masked identifiers in working copies where possible, and keep final records in encrypted or access-controlled storage where practical. This keeps the record trail usable for audit while reducing avoidable data exposure.

You might also find this useful: How a UK Creative Director Should Invoice a US Client from their LTD Company to Optimize for Taxes.

Common failure points and how to recover quickly#

When something breaks, fix the assumption first and then the form. Rebuild your logic from records, protect filing deadlines, and document what changed.

- Failure: treating a U.S. entity election as the full UK answer.

Recovery: Re-test your UK position against the facts and records already in your file, and write a short note that maps facts to treatment. If you cannot tie the note to underlying records, treat the position as provisional and rework it.

- Failure: relying on cross-border relief assumptions before your facts are fully aligned.

Recovery: Re-check those assumptions before the next return or payment date, then update your working position immediately. Keep a dated change note so any filing update is traceable.

- Failure: waiting to file because classification is still unresolved.

Recovery: Keep the filing process moving: register for Self Assessment if needed, tell HMRC by 5 October for the previous tax year when required, and plan for payment by 31 January. If you were previously registered, check reactivation status early. If online filing is unavailable, including non-resident cases, switch to commercial software or other forms.

- Failure: mixing unrelated rule sets into a services case.

Recovery: Separate core UK filing checkpoints from side issues, and remove items you cannot support with your current facts. If you are unsure whether your activity counts as trading, get HMRC guidance before locking in treatment.

For a step-by-step walkthrough, see How a German Freelancer Can Handle US Sales Tax with a US LLC.

Your first 30 days with clear decision checkpoints#

Use the first month as a planning cadence to lock U.S. tax status and filing logic before finalizing key tax positions. The goal is to settle the filing approach early so later decisions are easier to adjust if facts change.

Week 1. Lock the U.S. status facts#

Use IRS Publication 519, Chapter 1 to answer the gating question: are you a resident alien or a nonresident alien for U.S. tax purposes?

Your checkpoint is evidence, not intuition: you should be able to show the dates and facts behind that status call. Do not assume one status applies to the full year, because Pub. 519 also allows for a dual-status tax year in Chapter 6.

Week 2. Write a short status-and-assumptions memo#

Tie each conclusion to records you already have, and label unknowns clearly instead of smoothing them over.

If a key point depends on missing documentation or an unverified assumption, flag it as open. That keeps later filing choices traceable and easier to correct.

Week 3. Test treaty feasibility and draft your U.S. filing matrix#

Anchor treaty review to Pub. 519 Chapter 9 and filing prep to Chapter 7, covering what to file and when or where to file.

Keep treaty relief as a tested possibility until your facts are fully aligned. Filing preparation can keep moving while some treaty questions remain open.

Week 4. Choose your path and freeze documentation standards#

If status, dual-status risk, or treaty treatment still depends on one disputed assumption, escalate before you lock the position.

By month-end, keep one dated pack: fact timeline, status memo, open-items list, filing matrix draft, and a decision log for what would trigger a change.

Copy and use this compliance checklist#

Use this as a sign-off sheet. Every line should be either verified with evidence or clearly marked unresolved before you rely on filing positions, distributions, or treaty assumptions.

- Residency position documented, not assumed.

Residency determinations are fact-specific. Keep a dated memo, a fact timeline, and supporting records. If facts are incomplete, keep this open and escalate.

- UK/HMRC classification items explicitly marked

unresolveduntil confirmed.

Do not rely on a U.S. entity label alone for UK treatment. If UK classification depends on HMRC-specific analysis, keep the status unresolved pending specialist review.

- Treaty relief tested only after status alignment is clear.

Use IRS Publication 519, Chapter 9 (page 64) as the treaty checkpoint. Keep relief as provisional unless you can show who is taxed where, on what item, and which assumption that depends on.

- Filing matrix drafted and evidence-linked.

Use IRS Publication 519, Chapter 7 (page 48) for U.S. filing checkpoints. For each potential filing line, track the obligation, status assumption, current evidence, and next action, and mark it verified or unresolved.

- Written escalation trigger in place before filing/distributions.

Define when you must stop and get specialist review: potential dual-residency indicators, unresolved classification, or treaty treatment that depends on a contested assumption. Keep IRS Publication 519, Chapter 6 (page 45) in view for dual-status year risk.

Before you lock filing positions, run your timeline through the Tax Residency Tracker so your residency evidence and decision dates stay consistent.

The bottom line for this structure#

Do not treat projected tax savings as real until your filing position is documented and supportable. The practical sequence is simple: document the facts, lock the UK filing basics, test the cross-border assumptions, then decide on distributions.

Write down what you know and what is still open#

Write down what you know, what you can prove, and what is still unresolved. If your position depends on unsettled points, for example entity classification, treaty alignment, or how a specific case might apply, keep those items explicitly marked as open.

Your checkpoint is simple: every filing position should tie to documents you already hold. Keep an evidence pack with relevant returns, HMRC correspondence, and required records such as bank statements or receipts.

Get UK compliance administration in order first#

Get UK compliance administration in order before optimization decisions. If you are filing for the first time, you must register for Self Assessment before using the online filing service. If you were already registered but did not file last year, you may need to reactivate your account, and HMRC says filing without reactivation may delay your return.

Timing matters:

- Tell HMRC by 5 October 2025 if you needed to complete a return for the previous tax year, 6 April 2024 to 5 April 2025.

- Late notification after that date can lead to a penalty.

- File on or after 6 April.

- Pay your Self Assessment bill by 31 January.

- Keep your UTR ready for online filing.

Test cross-border conclusions separately#

Treat cross-border conclusions as a separate test, not an automatic result. Business structure affects how tax and legal responsibilities are handled, so do not assume one-country treatment automatically carries into the other.

If a key assumption is not yet evidenced, record it as unresolved and avoid building cash-flow plans around it.

Set your filing map before distributions#

Set your filing map before distributions. If facts are still unclear, taking money out early can reduce flexibility and make corrections harder later.

Use a one-page control sheet for each return: the position, the assumption behind it, the supporting evidence, and the fallback action if that assumption fails.

Get specialist review if interpretation points remain open#

If your case still depends on unresolved interpretation points, consider specialist review before the next filing cycle. If your file is fully evidenced, proceed with disciplined filing first, then distributions.

Need the full breakdown? Read A Deep Dive into the 'Royalties' Article of the US-UK Tax Treaty for Authors.

If your case still has opacity or treaty uncertainty, contact Gruv to align your payout flow and record trail setup with your compliance process.

Frequently Asked Questions

Can a UK resident creative director use a US LLC to lower taxes safely?

Possibly, but only if the filing and treaty position are fully documented and defensible. Do not treat projected savings as real when they depend on unresolved assumptions. Start with U.S. tax status in IRS Publication 519, because that changes what income is in scope.

Why can a US pass-through election still be treated differently by HMRC?

Because a U.S. pass-through election answers a U.S. classification question, not necessarily the UK treatment outcome. The article treats UK treatment as a separate analysis that still needs evidence. If your credit or distribution logic depends on unproven assumptions, keep the position unresolved.

Is `Anson` a blanket rule for all `Delaware LLC` cases?

No blanket rule is established in this material for all Delaware LLC cases. The article says to treat each case as fact-specific and map the operating agreement, member rights, and tax facts before relying on any single precedent. If you cannot clearly map those facts, keep the point unresolved before filing or taking distributions.

When does `double tax treaty relief` fail in UK/US LLC structures?

This material does not establish when treaty relief will succeed or fail for your specific facts. Use Chapter 9 of IRS Publication 519 as the treaty checkpoint and document the income item, who is taxed, and the treaty position claimed. If any of that is vague, do not base cash-flow planning on expected relief.

Do I need `Form 1040-NR` if my work is mainly creative services?

Maybe. The type of work alone does not decide it. The answer depends on your U.S. tax status and whether you have U.S.-source income or certain income connected with U.S. business activity, and you should also check for a possible dual-status year.

What are the first documents I should prepare before taking LLC distributions?

Start with a dated residency fact timeline, LLC formation and operating documents, election records, prior filings, and any IRS correspondence. Then prepare a classification memo and a filing matrix that lists each possible return, the assumption behind it, and your evidence. If key items are missing, pause distributions until the position is tested.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- assets.publishing.service.gov.uk/media/5a7f12cb40f0b6230268d458/small_company...trusted

- ftb.ca.gov/file/personal/residency-status/part-year-and...trusted

- ftb.ca.gov/forms/2024/2024-1031-publication.pdftrusted

- irs.gov/pub/irs-pdf/p519.pdftrusted

- irs.gov/individuals/international-taxpayers/taxation...trusted

- sec.gov/Archives/edgar/data/1500412/0001193125260172...trusted

- taxpayeradvocate.irs.gov/wp-content/uploads/2024/12/ARC24_MSP.pdftrusted

- un.org/esa/ffd/wp-content/uploads/2014/08/UN_Handbo...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

Understanding the UK's Statutory Residence Test (SRT)

Treat SRT like ops, not folklore. You want a repeatable workflow you can run monthly so your tax-year answer is boring, documented, and easy to defend.

Tax Implications for a UK Resident Owning a US LLC

When people search **uk resident owning us llc tax**, they often start with the wrong question. You do not win by chasing a clever position. You win by running a compliant system that can handle the way the US and UK classify LLC income differently, with records you can defend.