Quick Answer

Start by locking one consecutive 12-month period, then choose the residency route your records can actually prove. For UAE filings, the 183-day path is usually cleaner, while the 90-day path requires extra status and UAE-tie evidence for the same period. Count days from passport and entry-exit records, including part-days, before you open EmaraTax. Treat the AED 50 TRC submission fee as a final step, because the Federal Tax Authority reviews applications and can reject them.

Tax Residency in the UAE Without Guesswork#

Choose your route before you collect documents. For UAE tax residency, this is a compliance decision, not a paperwork task: one route, one consecutive 12-month period, and one fact pattern you can prove. Use these terms as controls:

- Legal anchor: the exact basis you are claiming under UAE tax law, not a document set that could support multiple stories.

- Assessment period: the consecutive 12-month window you are testing. Day counting happens inside that window, and presence days do not need to be consecutive.

- Evidence consistency: records complete enough to count every day or part-day of UAE presence without gaps.

- Escalation trigger: the point where your file becomes interpretive instead of factual. If wording is borderline or texts conflict, escalate for technical review because the Arabic text prevails.

| What you lock first | Why it matters | What to check before moving on |

|---|---|---|

| Legal anchor | Prevents mixed-route files | Verify the current legal reference and threshold from official FTA/source guidance, then confirm one route fits all facts |

| Assessment period | Day tests only work inside a fixed window | Pick one consecutive 12-month period and reconcile every trip against it |

| TRC purpose lane | Domestic and DTA requests are different filing lanes | Confirm whether you are applying as a UAE tax resident under UAE law or for DTA use |

| Evidence map | The FTA reviews applications and issues only if approved | Check passport stamps, entry/exit logs, address records, and status documents for date alignment |

Before you open EmaraTax, create a one-page period note and run this pass/fail check:

- Pass: your claimed route, tested period, and proof list fit on one page with no contradictions.

- Pass: every UAE entry and exit can be matched and counted by day or part-day.

- Fail: your core facts, such as address availability, permit or status, or work story, change across documents.

- Fail: you need two different explanations for the same period. That is your escalation trigger.

Portal access shows process readiness, not approval. TRC issuance is reviewed and not automatic. If you want broader cross-border context before filing, read the digital nomad tax survival guide. Related: Hungary Tax Residency for Nomads and the White Card.

Start With the Terms That Actually Decide the Outcome#

Keep legal classification separate from filing mechanics. Whether you are treated as a UAE tax resident is determined under the legal tests. The TRC application is an administrative filing step that comes after your analysis is consistent. Use these four terms as controls in your notes:

| Term | What it means in practice | Common mistake if misunderstood |

|---|---|---|

| Residency route | Choose one legal condition set and build the file around it | Blending multiple routes because each seems partly available |

| Assessment period | Lock one relevant consecutive 12-month period before testing days | Changing the period mid-process or counting across mismatched windows |

| Evidence pack | Keep records that support the chosen route for the same period, including physical presence by day or part-day | Submitting many documents that do not prove one consistent fact pattern |

| Administrative filing step | Use the FTA service after route and period are settled | Assuming portal access, payment, or submission establishes residency |

When wording is unclear, use Cabinet Resolution No. 85 of 2022 and Ministerial Decision No. 27 of 2023 as your authority baseline. That is where you confirm the consecutive 12-month period, that presence days do not need to be consecutive, and that a day or part-day can count.

Keep process details in their lane. The FTA service workflow, including the AED 50 submission fee, is an operational step. It does not replace a sound classification analysis.

Before you proceed, write one line for your route, one for your 12-month period, and one for the records supporting both. If any line conflicts with the others, pause and escalate for technical review. For a cross-border comparison, see our guide on Costa Rica Tax Residency for Pura Vida Nomads.

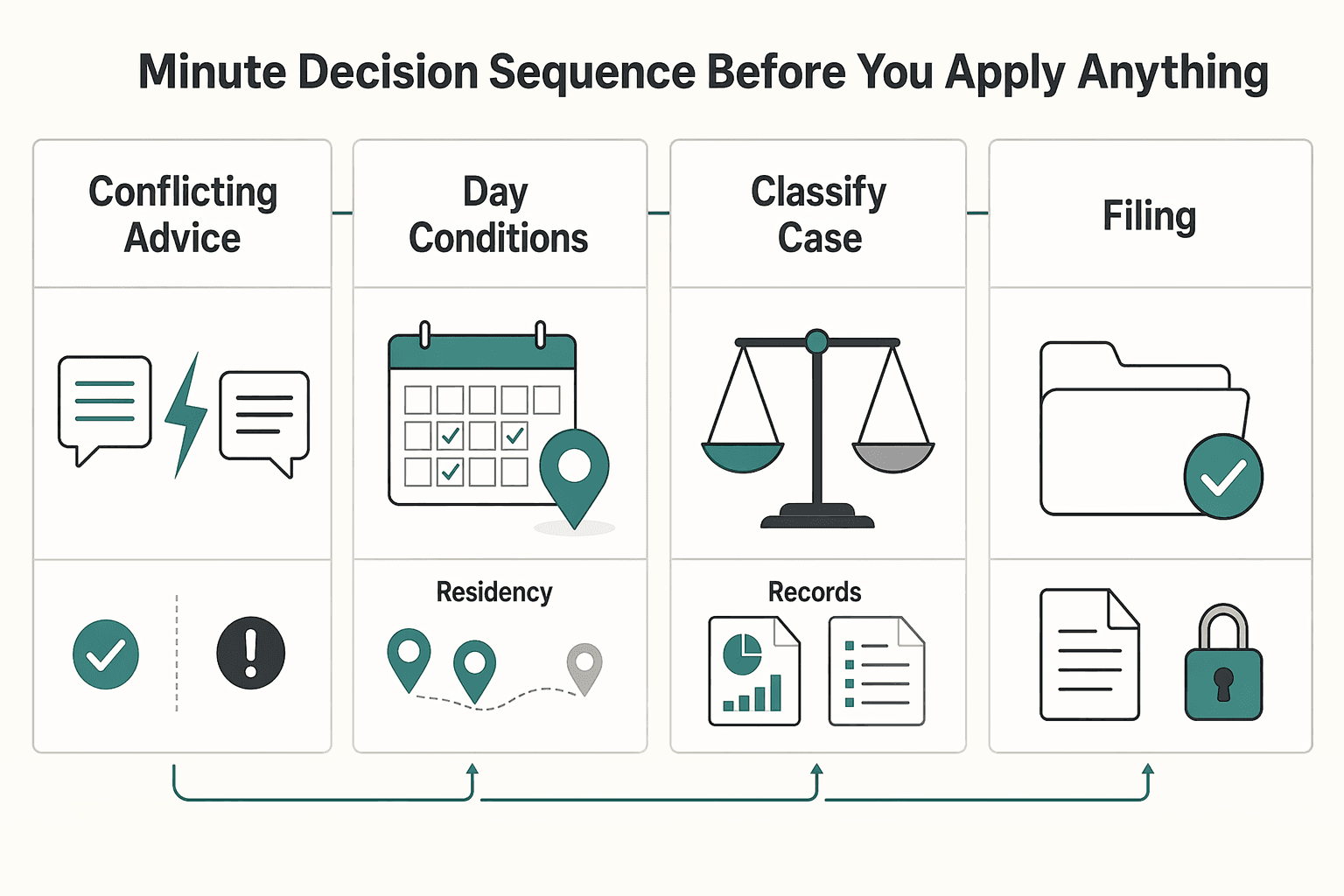

Use This 15 Minute Decision Sequence Before You Apply for Anything#

Classify first, submit later. If your travel record, legal route, and application setup do not point to one consistent outcome, pause before you pay the AED 50 submission fee. That fee is not refundable if the application is rejected.

| Step | Pass | Fix | Escalate |

|---|---|---|---|

| Map days and resolve conflicts | Day total is clear and supported for the full period | Dates or movement records conflict but can be reconciled | Result depends on exceptional-circumstance days being disregarded, or remains borderline after reconciliation |

| Check 90-day conditions | Day count, status condition, and UAE tie align for the same 12-month period | Fact pattern may qualify, but evidence for status or ties is weak | File depends on combining partial facts that do not fit one route cleanly |

| Classify the case | Domestic route is clear and no competing claim is obvious | Wording or facts need alignment across jurisdictions | Competing residency treatment is plausible and needs technical review |

| Run the filing-readiness gate | Access works, application type matches your case, and the application period matches your tested period | Profile, access, or application selection is incomplete | Selected portal track does not match your legal classification |

Run this sequence in one sitting: map days, check ties if needed, classify the case, then confirm filing readiness.

Step 1 map days and resolve conflicts first#

Start with physical presence, because both the 183-day and 90-day routes depend on it. Lock one relevant consecutive 12-month period, count each day or part-day physically present in the UAE, and remember that the days do not need to be consecutive.

If records conflict, treat that as a stop point until you resolve it. It is not stated as a statutory filing ban, but unresolved conflicts make your route decision unreliable.

Pass: your day total is clear and supported for the full period. Fix: dates or movement records conflict but can be reconciled. Escalate: the result depends on exceptional-circumstance days being disregarded, or remains borderline after reconciliation.

Step 2 check 90-day conditions only when relevant#

If you are at 183+ days, assess under that route. If you are using the 90+ day route, test the extra conditions directly.

On the 90-day route, you also need a qualifying status condition. That can be UAE nationality, a valid UAE residence permit, or GCC nationality. You also need at least one listed tie, such as a permanent place of residence in the UAE. Use the legal definitions: a residence permit does not include a temporary entry permit, and a permanent place of residence is available to you at all times.

Pass: day count, status condition, and UAE tie align for the same 12-month period. Fix: the fact pattern may qualify, but evidence for status or ties is weak. Escalate: your file depends on combining partial facts that do not fit one route cleanly.

Step 3 classify the case before portal steps#

Keep three lanes separate: domestic residency assessment, treaty-risk screening, and portal process. First, determine whether you meet UAE domestic residency tests. Then screen whether another country could also claim residency for the same period. The FTA service distinguishes UAE tax resident under UAE legislation from UAE tax resident under DTA application, so keep one consistent fact pattern across both lanes.

Pass: domestic route is clear and no competing claim is obvious. Fix: wording or facts need alignment across jurisdictions. Escalate: competing residency treatment is plausible and needs technical review. See A Freelancer's Guide to the US-Germany Tax Treaty.

Step 4 run the filing-readiness gate#

Only after classification should you complete filing setup. Portal readiness is not eligibility: you still need EmaraTax profile readiness, UAE PASS access for FTA services, and the correct application track, whether DTA or non-DTA.

Pass: access works, application type matches your case, and the application period matches your tested period. Fix: profile, access, or application selection is incomplete. Escalate: the portal track you selected does not match your legal classification.

Use the Tax Residency Tracker as an optional aid while you review day counts and records. It does not replace legal classification.

You might also find this useful: Tax Residency in Croatia: A Guide for Nomads on the Adriatic.

Understand the 183 Day Route and Where People Misread It#

If you are using the higher day-count route, treat it as an evidence test, not just a math exercise. This route is only clean when you can support physical presence across one relevant consecutive 12-month period.

Under the UAE rules, a natural person can be a Tax Resident if they are physically present in the State for 183 days or more in that period. The days do not need to be consecutive, and days or parts of days count. In practice, counting alone is not enough if you cannot support the days claimed.

Residency status is not the same thing as certificate processing#

Keep this distinction clear: legal tax residency comes from meeting the legal tests, while a Tax Residence Certificate is issued by the FTA after application review and approval. Filing a TRC application does not create eligibility.

That matters because TRC issuance is a review process subject to requirements and conditions. The FTA also states, in at least one FAQ context, that no amendments are possible under TRC, so pre-filing accuracy matters.

Pre-filing control checks for this route#

| What to verify | What breaks review |

|---|---|

| One locked consecutive 12-month period for day counting | Changing the period to patch weak day totals |

| Counted days can be supported if reviewed | Day totals that cannot be clearly supported |

| Application details are final before submission | Post-submission changes may not be possible in at least one TRC FAQ context |

In your internal filing note, leave the certificate-threshold line unresolved until current FTA wording confirms the exact certificate purpose and threshold.

Use a travel ledger, then apply one hard gate#

Build a travel ledger for the claimed 12-month window: date, movement, supporting evidence, and whether the day is counted. The goal is simple: every counted day should be traceable.

Apply one hard gate before submission: if any movement cannot be tied to supporting evidence, pause and resolve it first. If your total only works when exceptional-circumstance days are disregarded by the Authority, treat that as an escalation point, not a routine filing.

Lock the period, prove the movements, then move to the certificate step. Need the full breakdown? Read Indonesia Tax Residency for Bali Digital Nomads.

Understand the 90 Day Route and the Extra Ties You Must Prove#

Treat the 90-day route as a strict pass/fail test, not a lighter fallback from 183 days. Your file must prove three things for the same claimed period: presence, qualifying status, and an additional UAE tie.

Cabinet Resolution No. 85 of 2022 sets the natural-person tests, and Ministerial Decision No. 27 of 2023 clarifies day counting, including parts of days and no requirement that counted days be consecutive, within a relevant 12 consecutive month period. Before you finalize a filing position, verify the latest Ministry of Finance (MoF) and FTA wording for the 90-day condition set. Use official publications, and remember the Arabic text prevails if English wording conflicts.

Check fit, status, ties, and consistency in that order#

Start with route fit: can you prove physical presence in the UAE for 90 days or more in one relevant 12 consecutive month period? If not, stop.

Then test status for that same period: can you prove UAE nationality, a valid UAE residence permit, or GCC nationality? Day count alone is not enough.

Then test extra ties: can you prove your UAE connection for the same period? Official wording explicitly includes a permanent place of residence in the UAE, and MoF guidance says it does not need to be owned, but it must be continuously available. Published technical summaries also describe UAE employment or business as an alternative tie. If that is your path, confirm current official wording before filing.

Finally, run a consistency check across all records. Strong proof on one condition does not cure a gap in another. Evidence expectations can vary by case, so treat the table below as a readiness check, not a fixed FTA document checklist.

| Condition | Strong evidence examples | Weak evidence patterns | Corrective action before filing |

|---|---|---|---|

| 90+ days in one 12-month period | Records that reconcile physical presence day by day, for example travel logs and passport movement history | Counted days without movement support, patched periods, totals that depend on assumptions | Lock one period and remove unsupported counted days |

| Qualifying status during the claim period | Valid UAE residence permit covering relevant months, or applicable nationality documents | Permit starts too late, expired status, coverage gaps | Narrow the period or wait until status is supportable across the full window |

| Additional UAE tie during the same period | Records showing continuously available residence; where relevant, employment or business records for the same months | Short-stay bookings, residence gaps, activity records without clear UAE linkage in that window | Build month-by-month tie coverage and close unsupported months |

| Cross-document consistency | Matching name format, ID details, address history, and dates across records | Name spelling differences, conflicting addresses, mismatched start dates | Resolve conflicts before submission |

Apply only when your period map is clean#

Process readiness is not eligibility. UAE Pass, portal access, or opening the TRC flow does not prove you qualify. The FTA reviews and issues only if approved.

Use one hard guardrail: submit only when your 12-month map is clean, with no unsupported months and no mismatched records. If any month has presence without status proof, or status without tie proof, pause and fix it first.

Use the Residence and Personal Interests Tests Only With Strong Facts#

Use this path only when your file shows one clear UAE centre of life for one exact claim period. If your facts already support the 183-day or 90-day route, use that first. This test is evidence-heavy and most defensible when your records align without gaps, timing drift, or competing country narratives.

For screening, keep definitions strict. Your usual or primary place of residence is where you habitually or normally reside, and where you spend most of your time compared with any other jurisdiction. Your centre of financial and personal interests is where your personal and economic interests are closest or most significant. This turns on occupation, family and social relations, cultural activities, place of business, property administration, and other relevant facts. If the result depends on explaining why another country is equally central, pause and reassess.

Before you rely on this route, verify current primary sources: Cabinet Decision No. 85 of 2022, Ministerial Decision No. 27 of 2023, and current FTA certificate guidance. For close calls, do not rely on summaries alone, and treat Arabic text as controlling where wording conflicts.

Test the evidence, not the story#

| Evidence area | What strong looks like | Common weak pattern | What to fix before relying on this test |

|---|---|---|---|

| Usual or primary residence | Lease, occupancy, utility, or similar records show UAE residence was continuously available and actually used through the claim period | Hotel-heavy stays, late lease start, or residence proof for only part of the period | Build a month-by-month residence map and remove unsupported months |

| Personal and economic interests | UAE work, client activity, invoicing, company records, or other economic activity align with the same months as residence evidence | Strong UAE business evidence but weak residence continuity, or the reverse | Align activity and residence records to one claim window |

| Personal ties | Family, social, cultural, and day-to-day life facts point to the UAE more strongly than any other jurisdiction | Another country appears equally central on practical living factors | Do not use this route until the comparative picture is clearly one-sided |

| Identity and timing consistency | Name format, passport details, Emirates ID or permit details, address history, and dates reconcile across records | Spelling mismatches, conflicting addresses, overlapping country narratives, or timing drift | Normalize identity data and reconcile all records to one period |

Two red flags commonly cause failures: partial-picture files and timing drift. A lease alone does not prove centre of interests, and a UAE contract alone does not prove habitual residence. More documents do not help if they describe different periods or different narratives.

Use a hard decision gate#

Use residence and personal-interests analysis only when residence, activity, and identity records line up over the same claim period without exception-heavy explanations. If your day map cleanly meets a day-count route, use that route first.

If you have real dual-country exposure, review treaty conflict handling before assuming a UAE certificate resolves the cross-border outcome. See A Freelancer's Guide to the US-Germany Tax Treaty.

Operator checkpoint#

- You can state one exact claim period, and all key documents support that same period.

- Your residence evidence supports habitual living, not just access to a place.

- Your personal and economic ties point more strongly to the UAE than to any other jurisdiction.

- A reviewer can reconcile your travel, address, activity, and identity records without repeated exceptions.

If you want a deeper dive, read How to Manage Your Time Effectively as a Freelancer.

Apply for a TRC at the Right Time and for the Right Period#

Apply for a TRC only after you have confirmed your residency route and locked a claim period your file can support. A Tax Residence Certificate proves UAE tax-resident status, so the status analysis comes first and the application comes second.

The FTA service is for people who are UAE tax resident under UAE tax law or under a double tax agreement. Do not use the portal to figure out your route. If your day count or legal-person position still needs interpretation, pause and finalize that first. If needed, rerun your logic from the 15-minute decision sequence.

Lock one applicant path before you open the form#

Choose one path: Natural Person or Juridical Person. Stay on that path for the full filing. FTA wording separates application types by applicant category, with distinct natural-person and legal-person tracks. Public FTA search snippets also indicate that core fields, including request basis, Natural or Legal classification, and TRN details, may not be amendable, and one snippet states no amendments are possible under TRC. Treat classification as a hard gate, not a formality.

Use a verified timing checklist#

File for a period that has already started and that your records already support. For natural-person day-count routes, the test is tied to a relevant 12 consecutive months, so your selected period and your records must match.

| Case | Timing note | Check |

|---|---|---|

| Any filing | File for a period that has already started and that your records already support | Verify current FTA filing guidance on the live TRC service page |

| Natural person | For natural-person day-count routes, the test is tied to a relevant 12 consecutive months | Selected period and records must match |

| Legal person | Secondary guidance has described filing after 3 months from the start of the relevant tax period | Confirm the current FTA position before relying on it |

| Newly incorporated company without a return | Secondary guidance has described, in some cases, 12 months of establishment | Confirm the current FTA position before relying on it |

Before submission, run this checklist:

- Verify current FTA filing guidance on the live TRC service page.

- Confirm period lock by writing the exact claim period and matching each core document to it.

- Verify the filing window before use: confirm the current earliest filing point from official FTA guidance before relying on it.

For legal persons, treat timing rules as verify-before-filing items. Secondary guidance has described points such as filing after 3 months from the start of the relevant tax period and, in some cases, 12 months of establishment for newly incorporated companies without a return. Confirm the current FTA position before relying on either.

Run one pass/fail check before submission#

| Check | Pass standard | Fail signal | Action |

|---|---|---|---|

| Period coverage | All core documents support one selected period | Months do not reconcile, or period is not properly started | Stop and rebuild one supportable period |

| Applicant type | File is clearly Natural Person or clearly Juridical Person | You need mixed personal + company logic to make it work | Stop and reclassify before filing |

| Document consistency | Name, IDs, TRN details if relevant, addresses, and dates align | Mismatches, conflicting identifiers, address drift, or timing gaps | Normalize records, then recheck |

If any portal field forces interpretation, especially classification, request basis, or period selection, do not submit that day. Capture the prompt, verify classification against current FTA guidance, and continue only when the answer is unambiguous.

Public material also conflicts on items like bank-statement requirements and review timelines. Some references say 3 working days, others say within 5 working days. Avoid fixed-SLA assumptions and reused checklists without a live check.

For a step-by-step walkthrough, see Tax Residency in Colombia for Digital Nomads and Expats.

Build an Evidence Pack You Can Reuse Every Year#

Build one submission-ready pack for one claim period. If it does not support one route, one consecutive 12-month window, and one consistent identity story, hold submission.

Here, submission-ready means you can reopen the folder later and still see exactly what you claimed, which period it covers, and how weak points were already explained. Keep the pack focused: the FTA TRC service supports treaty and non-treaty purposes, and required evidence can differ by route and purpose.

Anchor the pack to the live legal position#

Use the current UAE residency framework as your legal anchor, not last year's checklist. For non-DTA natural-person TRC requests, public FTA guidance points to Cabinet Decision No. 85 of 2022 read with Ministerial Decision No. 27 of 2023 for the relevant 12-month period. Confirm current instrument naming on live FTA and legislation pages before filing.

That anchor drives your evidence logic: day tests run over a consecutive 12-month period, days do not need to be consecutive, and part-days physically present in the UAE can count. If you rely on the 90-day route, your pack must also prove the extra status and UAE-ties conditions.

Use a practical evidence map#

This is not an official universal checklist. It is a working map to keep your file coherent.

| Evidence group | What it proves | Required period alignment | Common mismatch to fix before filing |

|---|---|---|---|

| Identity and movement records | Your identity and how UAE presence days were counted, for example Emirates ID and residence visa, or passport with an entry-exit report, where relevant | All records reconcile to the same selected consecutive 12-month period | Name or passport details conflict across records, or entry-exit data does not match your day log |

| Status and route-support records | Why you qualify for the route claimed. For 90-day cases, this includes status plus UAE-ties support | Status evidence must exist within the claimed period | Status document dates fall outside the period you are claiming |

| Residence tie records | Support for permanent place of residence in the UAE where your route requires it | Dates overlap the same claim period | Housing records start too late, end too early, or conflict with other address records |

| Employment or business records | Support for UAE employment or business activity where your route requires it | Activity evidence sits inside the same 12-month period | Only setup documents are provided, with no support for activity during the claim period |

| Gap and exception notes | Explanation of missing months, ID changes, unusual travel, or exceptional-circumstance days | Notes reference exact dates and linked records | Known gaps exist but no written explanation is included |

Keep one reusable folder structure#

Use a period-based template, not a calendar-year habit:

<tax-period>-TRC/01-identity-movement<tax-period>-TRC/02-status-ties<tax-period>-TRC/03-work-business<tax-period>-TRC/99-submission-notes

Apply one naming rule to every file: YYYY-MM-DD_document-type_covered-period_version.ext Example: 2026-03-31_entry-exit-report_2025-04-to-2026-03_v01.pdf

This naming pattern is an internal control, not a legal requirement. It helps you prevent duplicates and untraceable files.

Hold submission if one check fails#

Run these pass/fail checks before filing. If any one fails, hold submission.

- Period match: Core files align to one selected consecutive 12-month period.

- Identity match: Name and identifiers are consistent, or documented with supporting records where changes exist.

- Route fit: Evidence matches the exact route claimed, including extra 90-day conditions when relevant.

- Documented gap treatment: Missing months or anomalies are explained and linked to available substitute evidence.

Then maintain the pack monthly: add new travel, status, residence, and work records, update your day log, and note unresolved gaps in 99-submission-notes. This keeps your file aligned with the TRC timing section.

Related reading: Malta Tax Residency Decisions for Digital Nomads.

Handle Treaty Situations and Conflicting Signals Carefully#

In treaty-conflict cases, lock one fact pattern for one review period, then run both countries' domestic residency tests before you interpret any treaty.

Start there. Under UAE domestic law, residency analysis comes first, including the 183-day route and the 90-day route with extra conditions. UAE day counts can be built from non-consecutive days within the relevant 12-month period.

Treaty tie-breaker rules apply only if both countries can still treat you as resident under domestic law, and those tests run in sequence. Some treaties start with permanent home, but wording and order can differ by treaty, so do not assume one template fits all.

Use primary texts first#

Keep your authority stack strict:

| Source | Role |

|---|---|

| Primary legal and tax authority text for each country's domestic residency rules | Start with domestic residency analysis for each country |

| Exact in-force DTA text for the treaty partner | Use the treaty text that actually applies |

| Competent-authority or MAP guidance | Use when interpretation or application is disputed |

| Secondary explainers | Use only for orientation, never as decision authority |

Before you finalize anything, confirm both country analyses use the same movement, address, and work facts for the same review period. If a source says a specific legal text controls, for example Arabic text or authentic treaty texts, treat summaries as convenience copies, not controlling law.

Keep a compact conflict file#

A practical conflict file can include:

| File | What it can contain | Owner | Action |

|---|---|---|---|

| Domestic position memo | One memo per country stating resident or not resident for the same period, with the applied domestic rules | You or local adviser | Complete before treaty interpretation |

| Treaty clause memo | Relevant treaty clauses in sequence, with your facts mapped to each step | Technical reviewer | Draft only if both domestic analyses indicate residence |

| Contradiction log | Facts that weaken your preferred outcome, with linked records or explanation notes | You | Update before any filing |

| Cross-filing consistency check | Position alignment across TRC requests, returns, disclosures, and adviser letters | You | Sign off last |

If both countries can still reasonably claim residence after memo review, consider pausing filings as an internal risk-control step and get technical advice before submission. Do not reshape facts to fit an outcome. If facts change, update the core fact set first, then rerun domestic analysis and treaty analysis in order.

For a worked treaty example, see A Freelancer's Guide to the US-Germany Tax Treaty. We covered similar issues in Tax Residency in Italy for Freelancers and Nomads.

Avoid the Mistakes That Cause Delays and Rework#

Most delays come from assumptions you cannot prove, not from complex analysis. Use one rule from start to finish: if a claim is not tied to verified authority text and period-matched records, treat it as unproven.

Anchor your file to current UAE natural-person residency guidance and the FTA TRC service criteria for the relevant consecutive 12-month period. For local-purpose natural-person TRCs, the FTA service page references Cabinet Decision No. 85 of 2022 and Ministerial Decision No. 27 of 2023 for the relevant 12-month period. If interpretation is sensitive, do not rely on English wording alone; the UAE legislation portal states that Arabic text prevails in case of conflict.

| Mistake | Consequence | Fix |

|---|---|---|

| You assume meeting a headline test means a TRC will issue automatically | TRC issuance is review-based: the FTA issues only if approved, and rejected applications are not refundable | Treat submission as a review process, not an entitlement. Complete legal and evidence checks before paying and filing |

| You rely on broad summaries, old notes, or mixed guidance | You can apply the wrong test, wording, or period support | Recheck against current UAE natural-person residency guidance and confirm controlling instruments for your period before submission |

| You count days from memory or with the wrong method | Totals can be wrong even when your travel pattern looks right. Current rules count all days or parts of a day, and days do not need to be consecutive within the relevant 12-month period | Rebuild from dated travel records. Spot-check arrivals and departures and isolate any exceptional-circumstance days instead of silently excluding them |

| You mix periods across domestic analysis, treaty notes, and the application | Contradictions trigger follow-ups or rework. A clean 183-day or 90-day day-count can still break if supporting evidence is from a different period | Use one consecutive 12-month period everywhere, with matching applicant language, address history, and tie statements |

| You jump from residency status to broad tax conclusions | You overstate outcomes. Residency status does not by itself prove every later tax consequence | Draw a hard boundary: establish residency first, then run a separate tax-consequence analysis |

| You expect to fix errors after submission | FTA search-listed FAQ signals indicate some TRC cases are not amendable, and approved changes may require a new application | Do a final scrub before submission and assume drift in names, dates, or facts may force a fresh application |

Before you submit, run this pass/fail check:

- Day-count evidence: every counted day is supported by dated records.

- Same-period alignment: day count, residence facts, and any treaty notes all use the same consecutive 12-month period.

- Consistent applicant language: status and narrative stay consistent across forms, statements, and supporting files.

- Unsupported statements removed: anything not tied to authority text or records is deleted, generalized, or stated as uncertainty.

Two late-stage failures cause repeated rework: copying prior-period assumptions without retesting the new period, and overloading the file with documents that do not prove your position. If your file still depends on interpretation-heavy explanations after this check, stop, hold submission, and escalate before paying and filing.

Know Exactly When to Bring in a Professional#

Stop self-service when your outcome depends on interpretation rather than clean, consistent records. If your conclusion only works because you are explaining around gaps, escalate.

Before you act, validate the current UAE tax-residency legal framework, current guidance for natural persons, and current FTA TRC service criteria for your filing period. If wording conflicts across versions, rely on the controlling legal text; the Arabic text prevails over translations.

| You can proceed yourself | Escalate now |

|---|---|

| Your 12 consecutive months are locked, and every counted UAE day is tied to dated records | Your day map is incomplete, memory-based, or hard to reconcile across nonconsecutive travel and part-days |

| You fit the 183-day route without stretching facts | Your result depends on the usual or main residence and center of financial and personal interests test |

| Your 90-day route is supported by status plus an additional UAE tie, with consistent documents | You have the days but weak proof of status or ties, or your documents point in different directions |

| You are not relying on treaty residence, or the treaty result is clear from the agreement text | Your position depends on treaty interpretation, dual residence, or tie-breaker sequencing |

| Your TRC file is internally consistent before payment | Names, dates, addresses, or route descriptions conflict across forms and evidence |

Run one stress test before filing: remove your two strongest documents. If your conclusion collapses, or shifts from clear to arguable, pause and get technical review.

When you brief an adviser, send a one-page intake with:

- Claimed route

- Tested 12-month period

- Evidence map (fact -> supporting document)

- Known contradictions

- Open questions that could change the outcome

If two professionals disagree, require both to use the same fact set and the same period. Ask each to identify the exact fact that changes the result, the document needed to confirm it, and whether the disagreement is about domestic residence, treaty residence, or TRC filing risk. This helps show whether the real issue is legal interpretation, evidence quality, or file consistency.

Make the Decision Early and Document It Like an Operator#

Choose your route first, then build documents to match it. The strongest file is one legal basis, one clearly defined analysis period, and one evidence set that stays internally consistent.

The routes are not equally document-heavy. The 183-day route is mostly a day-count exercise if records reconcile. The 90-day route needs more than presence. You need 90+ days in a consecutive 12-month period, a status link such as UAE nationality or a valid UAE residence permit, and a UAE tie such as a permanent place of residence, UAE employment, or UAE business activity. The usual or primary residence plus centre of financial and personal interests route is valid, but it is interpretation-heavy and needs stronger facts.

| Route | When to choose it | Verify first | Common failure mode |

|---|---|---|---|

| 183 days or more in a consecutive 12-month period | Your travel history is complete and reconcilable | Count physical-presence days correctly, including partial days; do not use a calendar-year shortcut | Claimed days conflict with passport, entry-exit, or travel records |

| 90 days or more plus status and UAE ties | You can prove the lower-day test and the extra conditions | Confirm status, for example a valid residence permit, and map each UAE tie to evidence | 90+ days are shown, but tie evidence is weak or inconsistent |

| Usual or primary residence plus centre of financial and personal interests | Your facts show your life is centered in the UAE | Check for cross-border fact conflicts before filing | File depends on interpretation because facts point in different directions |

Follow the sequence in order#

- Lock your analysis period first.

For the 183-day and 90-day routes, use a consecutive 12-month period and build a day map. Count all days or parts of a day physically present in the UAE; presence days do not need to be consecutive. If passport stamps, travel records, and your log do not match, reconcile them before filing work starts.

- Run the route-specific check.

For 183 days, prove presence cleanly. For 90 days, treat presence as only the first gate and confirm status plus UAE ties.

- Build a period-aligned evidence pack.

Keep every document aligned to the same analysis period. Use a one-page tracker: fact claimed, proving document, period covered.

- Stress-test before submission.

Remove your strongest document and see whether the position still holds. If it collapses, the file is not ready.

- Run a final consistency control.

Names, passport numbers, dates, addresses, and period references must match across all records. Filing should be execution, not diagnosis.

Keep the scope tight#

This close-out process is for natural persons. UAE rules define "Person" to include natural and juridical persons, but the tests are not interchangeable. For juridical persons, one route is UAE incorporation, formation, or recognition, and a branch of a foreign juridical person is excluded from that incorporation-based test. Keep corporate-tax "Resident Person" language separate from UAE "Tax Resident" analysis.

Close the loop after filing#

A Tax Residency Certificate is reviewed by the Federal Tax Authority and is not automatic. Keep a short post-submission note with the route used, the analysis period, final day count where relevant, tie documents relied on, and any review questions raised. Use that note as next year's baseline.

If your outcome still depends on interpretation, especially centre-of-interests analysis or treaty interaction, escalate to professional support at that point.

If your final residency position still depends on interpretation instead of clean records, get a second set of eyes before filing through Gruv support.

Frequently Asked Questions

What are the individual residency routes for UAE tax purposes?

Treat route definitions as unconfirmed and verify current official guidance before choosing a route or filing.

Is spending 183 days in the UAE mandatory?

The provided material does not confirm whether 183 days is mandatory. Verify current threshold language for your filing period before relying on any path, and pause if your decision depends on memory, old screenshots, or secondary summaries.

How does the 90-day route differ from the 183-day route in practice?

The criteria for comparing the 90-day and 183-day routes require verification against full official guidance before submitting, as legal details can differ from summary descriptions.

Can you apply for a Tax Residency Certificate before the tax period ends?

The excerpts do not establish TRC timing rules. Treat timing as a live procedural check and confirm current official guidance for your exact period and profile before filing.

Does UAE tax residency automatically mean you owe UAE personal income tax?

Keep residency determination and liability analysis separate, and get professional review if your position depends on cross-border or treaty interpretation.

What documents should you prepare first for a TRC application?

The provided material does not include a reliable TRC checklist. Confirm the current official document requirements first, then map each claimed fact to supporting records; do not rely on extracts that are mostly metadata, navigation text, or cookie language.

How do you know whether a source is reliable enough to answer a residency question?

If an extract is mostly metadata, navigation text, or cookie-consent language, do not use it for legal answers. A common failure mode is truncated extraction, where operative rule text is missing but the summary still sounds complete. Confirm you have full article body text or official guidance, and escalate if your conclusion changes after removing weak sources.

What should you do if UAE domestic tests and treaty residence seem to conflict?

The provided excerpts are not sufficient to resolve domestic-versus-treaty conflicts. Keep one consistent fact set, verify current treaty text and tie-breaker logic before filing, and stop self-service when the outcome depends on interpretation or sequencing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- assets.publishing.service.gov.uk/media/5da850dce5274a5ca94bb5cc/2016_UK-UAE_D...trusted

- foreign.senate.gov/download/transcript092221trusted

- ftb.ca.gov/tax-pros/procedures/waters-edge-manual/chapt...trusted

- mof.gov.ae/wp-content/uploads/2023/03/Ministerial-Decis...trusted

- mof.gov.ae/en/news/following-cabinet-decision-85-of-2022trusted

- sec.gov/Archives/edgar/data/1794350/0000950170220061...trusted

- tax.gov.ae/en/services/issuance.of.tax.certificates.aspxtrusted

- tax.gov.ae/en/content/tax.resident.and.tax.residency.ce...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

How to Manage Your Time Effectively as a Freelancer

Most freelancers struggle not because they work too few hours, but because they misallocate the hours they have—treating time as an infinite resource rather than a finite business asset with a real cost per unit. The solution is a three-layer operating system: a Time Budget Framework that commits hours to four categories before any client work is booked, a Weekly Operating Template that assigns those categories to specific calendar windows, and a monthly Admin Audit Checklist that reconciles invoicing, bookkeeping, and compliance records. Multi-client orchestration requires a WIP limit, dedicated client windows, and a capacity decision rule run before accepting new engagements. Together, these systems replace reactive decision-making with a repeatable structure that keeps delivery quality consistent, records audit-ready, and the freelance practice operationally durable.

A Freelancer's Guide to the US-Germany Tax Treaty

---