Quick Answer

A digital nomad stipend is usually taxable unless it is set up as a compliant reimbursement arrangement under an accountable plan. To stay out of wages, the payment must have a business connection, each expense must be substantiated, and any excess amount must be returned. If it is a flat allowance with no receipts or reconciliation, treat it as taxable wages.

The Global Professional's Playbook for a Tax-Proof Digital Nomad Stipend#

Start by classifying the payment before you try to optimize its tax treatment. A stipend is a fixed periodic payment for services or to defray expenses. Taxable compensation is pay for employee services unless a specific exception applies. A reimbursement gets different treatment only when the arrangement has a business connection, you substantiate the expense, and you return any excess amount.

| Requirement | Article detail |

|---|---|

| Receipts or electronic records | Include the date, amount, merchant name, and merchant location |

| Business-purpose note | Keep a short business-purpose note for each expense |

| Advance safe harbor | 30 days |

| Substantiation safe harbor | 60 days |

| Return-of-excess safe harbor | 120 days |

The label alone does not control the result. Calling a payment a "stipend," "allowance," or "remote work benefit" does not change how it is taxed. If the structure is unclear, use the default position and treat it as taxable until it is formally set up as a compliant reimbursement arrangement. A common failure mode is a flat monthly allowance with no receipts, no business-purpose record, and no process to return unused funds.

To do this correctly, you need clear policy or contract language, proof for each expense, and timing discipline. Keep receipts or electronic records with the date, amount, merchant name, and merchant location, plus a short business-purpose note. If funds are advanced, follow the fixed-date safe harbors: 30 days for advances, 60 days to substantiate expenses, and 120 days to return excess amounts.

One final guardrail matters throughout: if your facts involve cross-border income or unclear worker classification, get professional review early. Worker classification is a facts-and-circumstances determination, and for U.S. citizens and resident aliens abroad, worldwide income remains in scope.

If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2026.

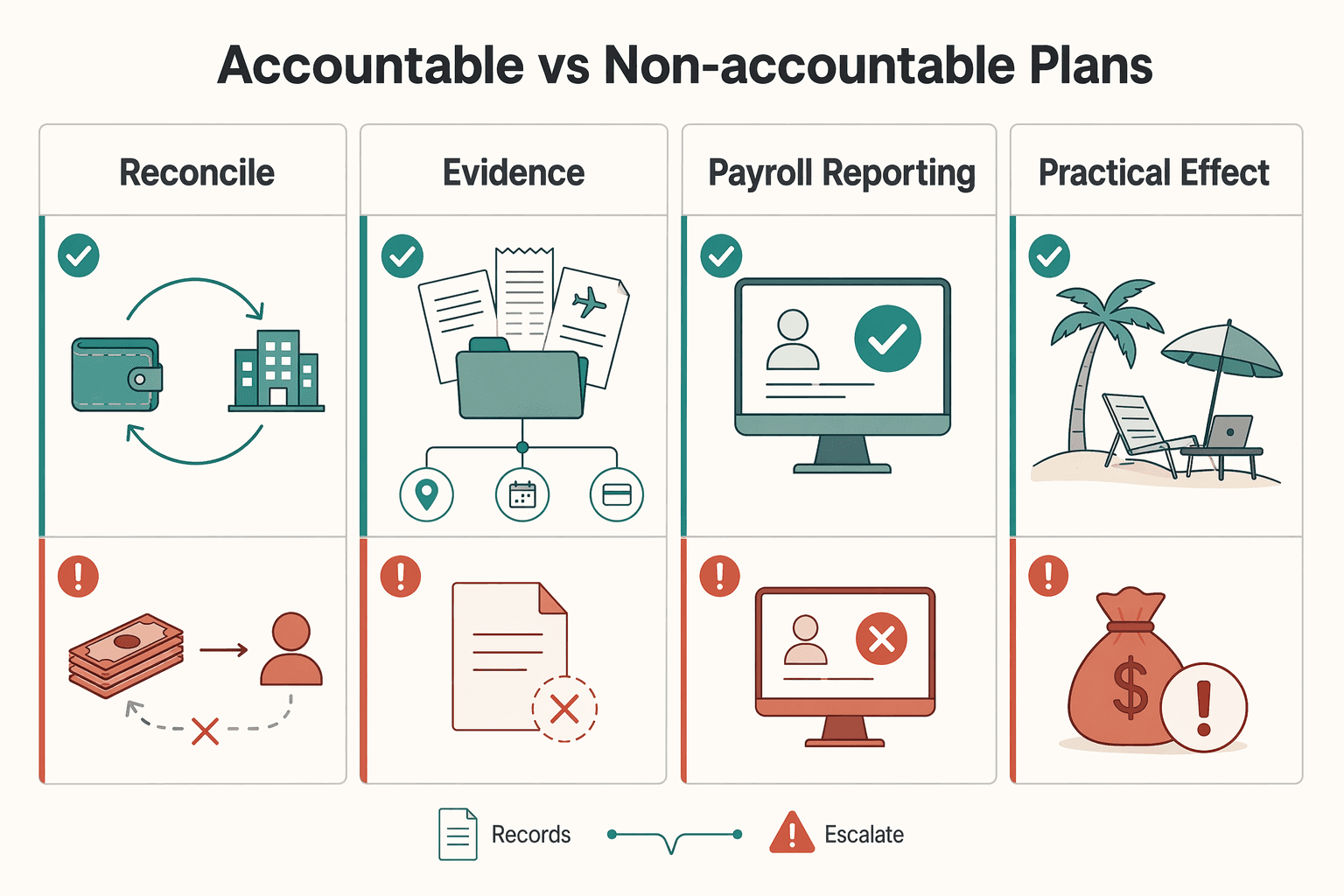

The Critical IRS Distinction: Accountable vs. Non-Accountable Plans#

If your payment is a flat allowance without a real substantiation-and-return process, treat it as taxable until your employer documents a compliant reimbursement arrangement.

An accountable plan is a reimbursement or allowance arrangement that meets all three requirements: business connection, substantiation, and return of excess amounts. A nonaccountable plan misses one or more of those requirements, including arrangements where substantiation is not required or excess amounts can be kept. For payroll purposes, wages means remuneration for employee services unless a specific exception applies. A reimbursement is generally excluded from wages only when it satisfies accountable-plan rules.

That is the key distinction for the rest of this guide: "stipend" or "allowance" is just a label. The actual process determines the tax treatment.

| Decision point | Accountable plan | Nonaccountable plan |

|---|---|---|

| Payment method | Reimbursement of actual business expenses, or advances tied to expected business expenses and later reconciled | Allowance or advance paid without reconciliation to substantiated business expenses |

| Documentation standard | You substantiate each expense and return excess amounts | Limited or no substantiation, and/or no return-of-excess step |

| Payroll reporting | Excluded from gross income and not reported as wages on Form W-2 | Included in gross income and reported as wages on Form W-2 |

| Practical effect on your net pay | Not subject to employment-tax withholding/payment on reimbursed amounts | Subject to withholding and employment taxes, reducing take-home value |

Quick self-check#

- Payment is for work-related expenses, not extra pay for services.

- You submit substantiation for each expense.

- Any advance is reconciled to actual expense amounts, not treated as fixed extra pay.

- Excess advances must be returned.

- Payroll confirms accountable-plan treatment instead of W-2 wage treatment.

If any of the last three boxes are unchecked, fix that process gap first. If most are unchecked, treat the amount as taxable wages until the process changes.

One planning point is easy to miss: nonaccountable-plan amounts flow into gross income and W-2 wages, which can increase AGI. That can affect FEIE planning for globally mobile workers, and claiming FEIE requires attaching Form 2555 and qualifying under the bona fide residence or physical presence test. Before you act, verify the filing year because FEIE limits change (for example, $130,000 for 2025 and $132,900 for 2026).

This pairs well with our guide on Italy Digital Nomad Visa Tax Playbook for Remote Professionals.

The "Accountable Plan" SOP: Your Blueprint for a Non-Taxable Stipend#

Use this rule first: your arrangement is accountable only if all three requirements are met: business connection, substantiation, and return of excess. If any one fails, treat the payment as taxable until the process is fixed.

Start with the right definitions#

Classify each transaction using these four terms:

- Ordinary and necessary business expense: a cost that is common and accepted in your industry and helpful or appropriate for your work.

- Substantiation: proof of the amount, time/date, place, and business purpose.

- Expense advance: money paid before final expense accounting.

- Excess reimbursement: any amount paid above what you substantiated as a business expense.

If your workflow is a flat allowance with no real expense report and no return-of-excess step, treat it as taxable pay, not accountable-plan reimbursement.

Pillar 1: prove the business connection#

Start with a simple judgment call: is the expense tied to doing your work, or is it mostly a personal living cost? If that answer is fuzzy, slow down before you submit it.

- Qualifies: work-related costs that meet the ordinary-and-necessary standard.

- Does not qualify: primarily personal or lifestyle spending.

- Keep: a short business-purpose explanation plus supporting records.

- If not met: do not submit it as accountable-plan reimbursement.

| Expense category | May be supportable when business-connected and substantiated | Usually not supportable | What to keep |

|---|---|---|---|

| Coworking membership | May be supportable if used for work and tied to your role | Leisure club access presented as workspace | Invoice, dates, business purpose |

| Software subscription | May be supportable if needed for client or employer work | Personal entertainment app | Vendor invoice, subscription details, work-use note |

| Home internet | Business-use portion may be supportable | Full household bill with no business allocation | Bill, allocation method, work explanation |

| Airfare for required team offsite | May be supportable when travel is primarily for business | Personal side trip added to the same travel | Itinerary, meeting purpose, receipts |

| Apartment rent | Usually a personal living cost; only a clearly documented business-use portion may be arguable | Full monthly housing cost submitted as business expense | Lease plus clear allocation if any business-use claim |

| Groceries, sightseeing, gym | Generally personal costs | Personal costs | Do not submit |

If a cost is mixed personal and business, such as internet, housing, or blended travel, treat that as a tax-pro review trigger before you assume tax-free reimbursement.

Pillar 2: substantiate every item#

A total amount is not enough. Your report needs to show the core facts for each expense so payroll or accounting can follow the trail without guessing.

- Qualifies: entries with amount, date/time, place when relevant, and business purpose.

- Does not qualify: missing core facts or no expense report.

- Keep: receipt or invoice plus a clear business-purpose note.

- If not met: treat the amount as taxable until documentation is corrected.

Do not assume one universal substantiation deadline. IRS per-diem guidance includes a 60-day example for filing an expense report, but your policy should use the rule that applies to your setup.

Pillar 3: return excess amounts#

This is where many arrangements fail in practice. If you receive an advance, reconcile it to substantiated expenses and return any leftover amount.

- Qualifies: the advance is fully accounted for, and excess is returned.

- Does not qualify: you keep amounts above substantiated business expenses.

- Keep: the advance record, matching expense report, and return or reconciliation record.

- If not met: the amount can become wage-reportable and subject to withholding.

Do not assume one universal excess-return deadline. Publication 505 includes a 120-day periodic-statement example for resolving outstanding advances; confirm the rule that applies to your plan. In cross-border payroll structures, accountable-plan failures can also trigger W-2 or 1042-S reporting and withholding issues, which is another clear point to bring in a tax pro.

For a step-by-step walkthrough, see Digital Nomad Tax Residency in Thailand for 2026.

Before you lock your reimbursement process, map your travel pattern and documentation trail in the Tax Residency Tracker.

How to Take Control: Scripts for Employees (Direct Hire & EOR)#

Ask for a documented reimbursement process, not a generic stipend. If the payment is meant to cover business expenses, it needs an accountable-plan workflow with business connection, substantiation, and return of excess, or it will be treated as taxable wages.

Map the stakeholder chain before you ask#

Before you raise the issue, confirm who actually owns each step. In reimbursement arrangements, the payor can be the employer, an agent, or a third party, so you need all four owners identified up front: policy owner, payroll coding owner, substantiation channel, and approval chain.

| Path | Policy owner | Payroll execution | Where you submit substantiation | Common failure point |

|---|---|---|---|---|

| Direct hire | Employer, usually HR, finance, or payroll policy | Internal payroll or payroll processor | The documented expense workflow payroll uses | Manager approves informally, but payroll still codes it as wages |

| EOR / multi-entity setup | Your company and/or employing entity per contract | EOR, local employer, or third-party payroll operator | Only the written reimbursement path tied to payroll coding | You open a support ticket, but no one updates policy and payroll treatment |

If no one can clearly name all four, treat the amount as taxable until they can.

Talk track: Direct hire employee#

Use this structure in your own words:

- Intent: "I want work expenses reimbursed through a documented process, not paid as a flat allowance."

- Compliance rationale: "I need the workflow to support business connection, substantiation, and return of excess so qualifying reimbursements are not handled as taxable wages."

- Process asks: "Who owns the policy, where do I submit receipts, who reviews first, and how do we reconcile and return any excess advance?"

- Close: "If this process is not in place yet, please treat current payments as taxable until it is."

If the answer is "just send receipts to your manager," that is not enough on its own.

Talk track: EOR (or other outsourced payroll setup)#

In an EOR setup, platform labels like "allowance" or "benefit" do not by themselves determine tax treatment. In outsourced payroll setups, federal tax responsibility does not automatically transfer away from the employer, and responsibility can shift only in limited structures (such as certain CPEO arrangements).

Use this structure:

- Intent: "Please route this as formal reimbursement for business expenses, not a flat taxable stipend."

- Compliance rationale: "I need confirmation that the setup supports business connection, substantiation, and return of excess."

- Process asks: "Who owns policy terms, who controls payroll coding, what submission channel is recognized, and what is the approval chain before payroll cutoff?"

- Scope check: "If the setup only supports a flat monthly amount with no substantiation or excess-return step, I will treat it as taxable wages."

Keep your own records, including receipts, approvals, and reimbursement logs, even if the platform stores them.

Employer-cost discussion: use formulas, not fixed savings claims#

When you discuss this internally, use formulas until your team verifies the current setup details:

| Payroll item | Rate or wage base | Article note |

|---|---|---|

| Social Security | 6.2% up to $184,500 of wages for 2026 | If wages are already above the Social Security base, extra taxable wages may not add this marginal cost |

| Medicare | 1.45% | If wages are already above the Social Security base and above the FUTA wage base, this may remain in the marginal employer cost |

| FUTA | 6.0% on the first $7,000; can be 0.6% if the maximum credit applies | Use formulas until your team verifies the current setup details |

| Additional Medicare | 0.9% | Do not include it in employer match math; there is no employer match |

Use the verified stipend amount with the applicable Social Security, Medicare, and FUTA employer-cost assumptions before turning the example into a fixed savings claim.

For 2026, Social Security applies up to $184,500 of wages. FUTA is 6.0% on the first $7,000 and can be 0.6% if the maximum credit applies. If wages are already above the Social Security base (and therefore above the FUTA wage base), the marginal employer cost on extra taxable wages may narrow to:

If Social Security and FUTA do not apply at the margin, recalculate using the verified stipend amount and the applicable Medicare employer-cost assumption.

Do not include the 0.9% Additional Medicare withholding in employer match math. There is no employer match for that amount.

Escalate fast when ownership is unclear#

When the setup is muddy, escalate by function instead of waiting for a generic answer:

| Function | What to confirm |

|---|---|

| Payroll | Pay code, wage versus reimbursement treatment, and W-2 handling |

| HR/Finance | Written policy owner, submission workflow, and approval chain |

| Legal/contract owner | Responsibility splits in PEO, CPEO, EOR, or joint-employment structures, especially where liability may be shared or shifted |

| Tax professional | Cross-border rules, mixed personal and business expenses, or conflicting local payroll treatment create uncertainty |

If ownership or the documentation path is unclear, default to taxable treatment until the process is explicit.

You might also find this useful: How to Handle Taxes for a Side Hustle.

The Business-of-One Strategy: Structuring Reimbursements in Client Contracts#

If you work client to client, separating your service fee from client-paid costs can make internal tracking clearer. It does not, by itself, determine tax treatment.

Use consistent working labels in your own paperwork:

- Service fee: payment for your work.

- Client-paid cost: an expense you plan to bill back to the client.

- At-cost reimbursement: billed back without markup.

- Pre-approved expense: a cost the client approved before you incurred it.

A conservative internal approach is to keep clear documentation for any billed-back cost and flag mixed personal/business spend for professional review.

Keep contract, invoice, and records aligned#

Your contract, invoice, and backup file should not conflict. Consistency helps you track revenue sources and explain how amounts were billed.

| Document layer | What to include | What to retain |

|---|---|---|

| Contract (MSA/SOW) | Whether client-paid costs are billed separately from service fees; client legal entity and location | Signed contract versions and change records |

| Invoice | Separate service lines from billed-back cost lines; clear client identifier and dates | Final invoice copies and submitted attachments |

| Support file | Backup for billed-back items and revenue-source tracking | Receipts/invoices, proof of payment, and your running Spanish vs non-Spanish revenue log |

Quick test: pick one billed-back line and trace it from contract language to invoice line to supporting records.

Bundled fee vs separated fee#

| Model | Tracking impact | Limitation |

|---|---|---|

| Bundled fee model | Simpler billing layout | Harder to isolate components when you later review revenue composition |

| Separated fee + billed-back costs model | Clearer line-level tracking | More admin work, and still not a standalone tax determination |

Add controls when risk justifies them#

Use controls you can maintain consistently, and treat them as operational choices rather than automatic tax outcomes.

- Add pre-approval rules or caps when client budgets are tight.

- Use a consistent submission timeline to reduce disputes.

- Keep categories simple and review unusual items before billing.

If you are self-employed under Spain's digital nomad visa framework (introduced through Ley 28/2022), the referenced rule says income from Spanish clients must not exceed 20% of total earnings for self-employed applicants. Track Spanish vs non-Spanish client income explicitly so you can monitor that threshold. This limit is specific to that visa context.

When to escalate to a tax pro#

Bring in help early if classification or revenue-source tracking is unclear:

- You have cross-border clients and need country-level revenue tracking.

- A cost is mixed personal and business.

- The treatment of a billed-back item is unclear.

- Your records are incomplete.

- You are unsure whether your Spanish-client income is approaching the 20% threshold.

Related: Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

Conclusion: You Are the CEO of Your Compensation#

For digital nomad stipend tax, do not let a label decide the outcome. Classify each payment intentionally, apply accountable-plan rules only when they truly fit, and treat the payment as taxable when those requirements are not clearly met.

Use the accountable-plan test as your anchor for employee reimbursements: business connection, substantiation, and return of excess amounts. When those conditions are met, payments are generally excluded from gross income and not reported on Form W-2. When they are not met, allowances, advances, and reimbursements are wage-reportable compensation. The practical check is simple: does your actual process require receipts, a business-purpose standard, and return of unused amounts?

Use this decision sequence before you file or sign terms:

- Classify the payment type. Is it service compensation, an allowance, or a documented reimbursement?

- Confirm documentation standards. Keep receipts or vendor invoices, proof of payment, and a short business-purpose note.

- Align contract and payroll workflow. Your contract, pay slip, invoice, and policy should describe the payment the same way.

- If requirements are not met, use taxable treatment. U.S. citizens and resident aliens abroad generally still report worldwide income.

Closeout checklist:

- Update agreement or policy language before the next payment cycle.

- Separate service-fee lines from reimbursement lines in contracts and invoices.

- Maintain one audit-ready substantiation file.

- Retain the trail for at least 3 years from filing.

Escalate to a qualified tax professional when facts are cross-border, expenses are mixed personal and business, EOR process ownership is unclear, or FEIE treatment is uncertain. That matters even more if you are relying on a foreign tax home and the 330 full days in 12 consecutive months physical presence path, or if you are self-employed and assuming FEIE removes self-employment tax.

We covered related cross-border planning in Colombia Digital Nomad Visa Tax Planning.

If your setup spans contracts, reimbursements, and cross-border payouts, talk to Gruv to confirm the right compliance-first workflow for your case.

Frequently Asked Questions

Is a digital nomad stipend taxable?

Usually yes, unless the payment is properly set up and documented as reimbursement instead of compensation. A label like stipend, allowance, or benefit does not control tax treatment by itself. Keep the written policy, pay-stub label, and substantiation rules together, and escalate if they conflict or the payment moved through multiple countries or entities.

How do I prove my stipend expenses for taxes?

Build one audit-ready file rather than scattered receipts. Keep the policy or contract, pay-stub or invoice label, receipt or vendor invoice, proof of payment, and a short business-purpose note for each item. If receipts are missing, spending is mixed personal and business, or dates cross tax years, escalate before claiming favorable treatment.

Can a freelancer or contractor receive a non-taxable stipend?

For contractors, the word stipend does not by itself make a payment non-taxable. Use separate lines for service fees and expense items, and keep the contract, invoice, approvals, receipts, and proof of payment together. If terms are vague, billing is bundled, or records are incomplete, get professional review before treating any amount as outside taxable income.

How does a stipend work with an EOR?

An EOR label or pay slip entry does not by itself resolve U.S. tax classification. Confirm who owns the policy, where the payment appears on payroll, and who keeps the expense records. If those answers conflict or the income flows through more than one country, escalate to a cross-border tax professional.

What’s the difference between a stipend and per diem?

Per diem is tied to specific travel dates and locations, while a recurring allowance for general costs should be classified separately. Keep travel policy, dates, locations, and business purpose for each trip. Verify current rates and documentation rules before filing because those details are not established here.

Does a taxable stipend count toward the FEIE?

If the payment is taxable compensation for your services, it may be foreign-earned income and still must be reported on a U.S. return even when you claim FEIE. For 2026, the FEIE maximum is $132,900 per person. Eligibility also requires a foreign tax home and a qualifying path such as 330 full days in 12 consecutive months under the physical presence test, and part-year qualification reduces the limit.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

How to Handle Taxes for a Side Hustle

If you want less stress at filing time, use sequence instead of shortcuts. When one year includes payroll income, contractor income, and time in more than one country, the order of operations matters. This guide gives you a defensible path so you can make each decision once, document it, and avoid rebuilding the return later.