Quick Answer

Returning to the U.S. cleanly and efficiently means separating pre-move and post-move income, using documented transfer routes, and keeping clear records for every foreign account. Once you are a U.S. citizen or resident alien, you are taxed on worldwide income, and FBAR and Form 8938 may apply on separate tracks. Confirm residency first, then evaluate treaty relief, FEIE, or FTC.

The Global Professional's Playbook for International Revenue#

If you are moving back to the U.S., the goal is not just compliance. It is a clean, low-stress way to handle foreign income, foreign accounts, and the records that show what happened before, during, and after your move.

Once you are a U.S. citizen or resident alien, you are taxed on worldwide income. Foreign account reporting runs on separate tracks. FBAR, FinCEN Form 114, is filed separately from the IRS and can be triggered when the aggregate value of foreign financial accounts exceeds $10,000 at any point in the year. Form 8938 is attached to your tax return and does not replace FBAR. For an unmarried taxpayer living in the U.S., one Form 8938 threshold is more than $50,000 on the last day of the tax year or more than $75,000 at any time during the year.

In practice, much of the risk is operational. Delayed filings, mismatched reporting, weak records, and advisor cleanup often start with unclear balances, ownership, or timeline details.

A practical way to handle this is a three-pillar workflow tied to your move timeline. Invoice decisions help you separate pre-move from post-move income periods. Transfer decisions determine when funds move and what records support that path. Hold decisions determine which foreign accounts stay open long enough to be useful without creating reporting confusion.

If FEIE is still relevant in your final year abroad, your move timing also affects whether you can support the 330 full days physical presence test or the bona fide residence test.

| Approach | Process quality | Documentation readiness | Risk control |

|---|---|---|---|

| Reactive repatriation | Decisions made after money arrives | Missing statements, unclear dates, weak account history | More reporting confusion and advisor rework risk |

| Blueprint-led repatriation | Decisions tied to move timing | Invoices, transfer proofs, and account records assembled as you go | Stronger handoff for FBAR, Form 8938, and return prep |

In the next sections, decide what to bill, when to transfer, and which accounts to keep or close. Gather invoices, account statements, account numbers, highest annual balances, and proof of move dates and travel days. Keep required foreign account records for 5 years. Escalate early to a qualified cross-border tax professional if you are unsure about FEIE eligibility, a move-year return, or foreign assets near Form 8938 thresholds. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2026.

Pillar 1: The Bulletproof Invoice That Always Gets Paid#

In your move year, every invoice does two jobs: it gets you paid, and it creates a record you may need to defend later. This section focuses on record quality, not form-level invoicing rules, so confirm scenario-specific requirements directly with the payer and your tax professional before you send anything.

Your move-year invoice checklist#

- Confirm who is actually paying you. Make sure the contract party, invoice payer, and remitting entity line up in your records. If different names appear across documents, resolve that before you send the invoice.

- Use current paperwork, not old templates. Documentation requests can vary by payer and your setup. Confirm what is needed for this engagement before sending.

- Describe the service clearly. Use plain-language deliverables and clear service dates or milestones. If work spans your move period, separate billing so the timeline is easy to follow.

- Keep a complete document trail. Store the final invoice, any revisions, the governing scope or approval record, and payment proof together.

| Client type | Confirm before first invoice | Why this matters |

|---|---|---|

| U.S. client | Legal payer entity, contract party, accounts-payable process, and current documentation request | Reduces payment delays and record mismatches |

| Non-U.S. client | Payer entity, cross-border billing expectations, remittance path, and current documentation request | Avoids rework from assumptions carried over from pre-move billing |

| Platform or client-of-record | Whether payer is platform or end client, payout statement format, and documentation already on file | Keeps payout records usable if payer identity is not obvious |

Monthly handoff to your preparer#

A simple month-end package makes later reconciliation much easier. Keep one clean file set per client or platform: invoice, scope or approval record, payment proof, and a short note on service dates. If payer identity, documentation treatment, or tax handling is unclear, escalate before you invoice and involve a qualified cross-border tax professional. For a step-by-step walkthrough, see The Final Tax Return Blueprint: A Guide for the Executor of an Estate.

Pillar 2: The Transfer Playbook for Maximizing Every Dollar#

Once the invoice is clean, the next decision is the transfer route. If you let the payer, bank, or platform choose by default, you lose visibility first and margin second.

Use this sequence: pick the gateway, invoice in the client's currency when appropriate, then decide when to convert and how to pay yourself. In a move year, favor routes that are predictable enough to plan around, documented enough to reconcile, and flexible enough to support repatriation records.

Pick the rail by control, not habit#

Do not compare routes on headline fees alone. A route can look cheap and still cost more if the FX spread is hidden, settlement timing is unclear, or reports are thin. Screen each option on fee visibility, settlement predictability, reconciliation effort, and documentation quality.

| Transfer route | Control over timing and FX | Settlement predictability | Reconciliation and audit trail | Where it fits |

|---|---|---|---|---|

| Traditional wire | Lower FX control if conversion happens before funds arrive | High for domestic U.S. Fedwire, which is immediate, final, and irrevocable once processed; cross-border wires can involve more moving parts | Can be workable, but details may be split across statements, wire advice, and fee deductions | Larger transfers or payers that only use wires |

| Local bank rail to multi-currency account | Higher control if you receive in client currency and choose when to convert | Can be strong on domestic rails; Same Day ACH supports up to $1 million per payment with published windows | Can be cleaner when provider statements are downloadable by currency and period | When you want client-currency invoicing and separate FX control |

| Platform payout | Medium to lower control when platform handles batching or conversion | Can be solid, but timing varies by provider settings and risk controls; Stripe shows expected payout deposit dates | Good if you export the right reports, for example Stripe payout reconciliation with automatic payouts or PayPal history reports | When the client relationship already runs through a platform |

If your client can pay by local rail into a multi-currency account, that can give you more control. Wise, for example, supports receiving payments through shared account details, and Wise statements can be downloaded by currency and time period. That can make it easier to track receipt, conversion, and repatriation as separate events instead of one opaque bank event.

Make hidden transfer cost visible#

Transfer or payout fees are only one cost bucket. FX spread is another, and it is often embedded in the offered rate.

Before you commit to a route, capture these four items together: send amount, receive amount, exchange rate, and separately stated fees or taxes. For covered consumer remittance transfers, these pricing inputs are disclosed before payment. Use that as a transparency benchmark, not as proof your business transfer is covered by the same rule. If those inputs are unclear, reconciliation usually gets harder.

Control FX on purpose#

Set your conversion rule based on cash needs, not market mood. Convert quickly when you need USD for rent, tax payments, or U.S. setup costs. Hold foreign currency only when you have near-term expenses in that currency or another clear operational reason, and document that choice.

Use this monthly checklist to keep it consistent:

- Set your conversion rule before the month starts.

- Save conversion evidence each time: date, rate, amount before, amount after.

- Apply one bookkeeping method consistently. U.S. return amounts must be in USD, and IRS guidance permits yearly average or another posted exchange rate when used consistently for items where that method is appropriate.

- Do not mix methods casually across items without a clear policy.

If you receive U.S. payments by ACH, plan with rail constraints in mind. Same Day ACH has a $1 million per-payment limit. Published settlement windows include 10:30 a.m. ET to 1:00 p.m. ET, 2:45 p.m. ET to 5:00 p.m. ET, and 4:45 p.m. ET to 6:00 p.m. ET. Treat those windows as planning inputs, not guarantees.

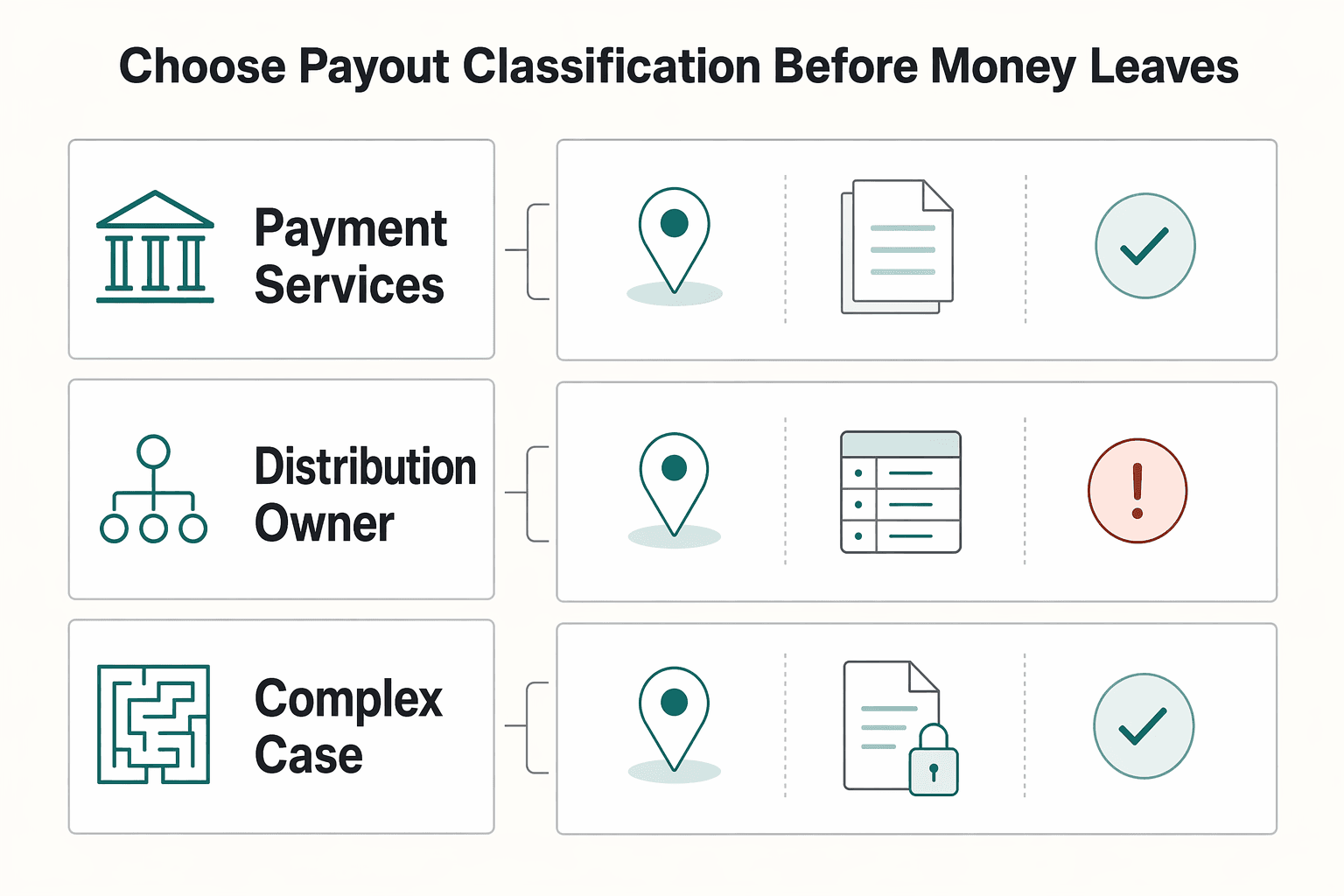

Choose payout classification before money leaves#

This is one of the easiest places to create avoidable problems. Decide payout classification before you initiate the transfer, and do not backfill the story later.

| Payout purpose | Action | Support |

|---|---|---|

| Payment for services performed | Use a clearly labeled services-payment path in your records | Service agreement; invoice/internal charge document; service period; payment record |

| Distribution of owner profits | Use a clearly labeled distribution path in your records | Owner approval/resolution; profit calculation; bank transfer record |

| Foreign entity involved or classification unclear | Pause before first payout | Confirm classification with a cross-border tax advisor before first payout |

If the purpose is not clear before the first payout, stop and sort it out then, not after the money moves.

Keep the support set together every time: payout report, bank proof, conversion confirmation, and the business document that explains the payout purpose. IRS recordkeeping rules require documents that support return items, and the general assessment period is 3 years.

You might also find this useful: The US Expat's Repatriation Blueprint: How to Re-establish US Residency Without Triggering a Tax Nightmare.

Pillar 3: The Holding Strategy That Prevents Compliance Nightmares#

Once money lands, the main risk usually shifts from execution to documentation. During repatriation, treat every account that touches cross-border funds as a verification item until you confirm how it should be handled under current guidance.

That applies before you move, during transition, and after you return. Your transfer plan controls timing and FX execution. Your holding plan is the evidence trail for who controlled the account, what happened to balances, and why money moved.

One caution: the source material behind this section includes Senate Hearing S. Hrg. 117-304, a Committee on Finance document printed by the U.S. Government Publishing Office, and the visible excerpt is front matter, not filing instructions. Use this section as a control framework, not legal authority. Confirm current filing requirements with up-to-date official guidance before you file.

Work the problem in three phases#

The cleanest way to manage account risk is in phases, not by trying to rebuild the story at year end.

| Phase | Main task | What to capture |

|---|---|---|

| Before move | Inventory every active and inactive account connected to your income, savings, or payouts | If you cannot explain why an account is still open, who controls it, and what it is used for, flag it for verification |

| Transition period | Expect frequent transfers and changing balances | Capture the reason for each move and keep records across the full period, including balance peaks when available |

| After return | Re-check documentation | Every account that stayed open, kept access rights, or held residual funds during the move year |

In practice, that means inventorying accounts before the move, capturing the reason for each transfer during the transition period, and re-checking any account that stayed open, kept access rights, or held residual funds after you return.

Classify each account before year-end filing#

Do this before filing season gets crowded. Use these as working tags for prep, then confirm final treatment with current rules and advice where needed.

- Needs verification (working tag): Use when facts are incomplete or account structure is unclear.

- Documentation in progress (working tag): Use when records are partial and still being assembled.

- Documentation complete (working tag): Use when records for your current treatment are organized and review-ready.

Use this checklist for each account:

- Do you have clear records of ownership and access rights?

- Can you identify the provider legal entity and account location from documents?

- Do you have complete statements or exports for the full period you used the account?

- Is there written support for your current working tag?

If any answer is "no," keep it in a verification bucket and resolve the gap before final filing decisions.

Run one standard holding log each month#

Use one row per account per month so your prep stays repeatable across all three phases. Suggested fields include:

- Account name

- Provider legal entity, if known

- Jurisdiction to verify

- Account purpose

- Ownership and access notes

- Balance notes (including peak points, if available)

- Key transfer references

- Evidence retained

- Follow-up status

Keep evidence with each row: statements or exports, transfer confirmations, provider account documents, and closure confirmations.

Compare the common holding locations#

Where you hold funds changes the documentation burden and the review complexity later. Use the table below as a review lens, not a substitute for account-by-account analysis.

| Account type | Verification focus (review lens) | Recordkeeping burden | Key follow-up question |

|---|---|---|---|

| Multi-currency account | Verify legal entity, account location, and permission details from account documents, not only app-level screens | Varies based on how many functions are combined in one account | Do your records clearly separate each use case? |

| Foreign bank account | Verify ownership and access history for the full move-year timeline | Varies with account activity and how long the account remains open | Can you map major transfers to supporting statements? |

| U.S. account receiving repatriated funds | Keep a clear source-of-funds trail into the receiving account | Usually focused on transfer traceability | Can each incoming transfer be matched to source-account records? |

Use one operating rule: consolidation can reduce gaps, but only if your closure and transfer records are complete. We covered this in detail in A Deep Dive into the 'Dividend' Article of the US-Germany Tax Treaty for LLC Owners.

The Strategic Layer: Your Shield Against Catastrophic Risk#

At this stage, the biggest tax risk is usually not the transfer itself. It is getting residency and relief in the wrong order, then ending up with the same income taxed twice without a valid claim path. For U.S. citizens and resident aliens, the U.S. taxes worldwide income, so the sequence is clear: confirm residency, test treaty relief, then choose FEIE or FTC without overlapping the same income.

Master tax residency in a strict order#

Start with domestic residency rules in each country, then move to treaty tie-breakers only if both countries can treat you as resident.

- Check domestic residency triggers first.

Do not treat "183 days" as a universal rule. For U.S. resident-alien determinations, the substantial presence baseline is 31 days in the current year and 183 days in a 3-year period, with one-third weighting for the first preceding year and one-sixth weighting for the second preceding year. UK SRT uses automatic overseas tests, automatic UK tests, and a sufficient ties test. 183+ UK days creates automatic UK residence, but fewer days can still produce UK residence based on ties.

- If both countries can classify you as resident, treat it as dual residence.

Then apply the treaty residency article for that specific treaty. Model tie-breaker logic starts with a permanent home available, then moves to closer personal and economic relations if both states have a home.

- Document evidence while facts are fresh.

Keep travel logs and tie evidence in one file set: entry or exit records, housing records, work records, family-location evidence, and local registration or residency records.

| Residency framework | What it evaluates | Common misread | What to document |

|---|---|---|---|

| Day-count style test | Physical presence in the relevant period | Assuming all countries use day count only | Entry or exit log, passport stamps, travel records |

| Weighted day-count style test | Presence across multiple years with weighting | Ignoring prior-year weighting in the U.S. resident-alien formula | Current-year and prior-two-year day totals with weighting support |

| Ties-based test | Personal or economic ties plus days | Assuming under 183 days always means nonresident | Home availability, family or work ties, local registrations, day log |

Use treaty relief as a checklist, not a hope#

Treaty relief is procedural. Verify coverage, match income to articles, choose the claim path, and keep proof. Also assume the saving clause can limit relief for U.S. citizens or residents unless an exception applies.

| Step | What to verify | Support or form |

|---|---|---|

| Confirm treaty coverage and current status | Verify coverage and current status for the tax year | Example changes: Hungary treaty termination effective January 1, 2024, for withholding taxes; Russia treaty suspension effective August 16, 2024 |

| Map each income type to the specific treaty article | Use the treaty text and tables for dividends, interest, royalties, pensions, annuities, and social security | If you need a rate, exemption, or threshold, verify the current rule before filing |

| Identify where the claim is made | U.S. treaty-based return positions are disclosed on Form 8833 when required | Foreign authorities often require Form 6166, requested via Form 8802 |

| Assemble claim support | Keep withholding or tax statements, payer records, residency certificate, and the contracts or invoices that identify the income type | Withholding or tax statements; payer records; residency certificate; contracts or invoices |

Run those four steps in that order: confirm coverage, map the income type to the article, identify where the claim is made, and assemble support before you file.

Compare FEIE against the credit route#

Choose one route per income item based on eligibility and documentation strength. Then document that choice clearly in your return workpapers.

| Route | Eligibility signals | Recordkeeping burden | When to escalate |

|---|---|---|---|

| FEIE | Foreign earned income, foreign tax home, and qualification under residence or 330 full days in 12 consecutive months physical presence | High: exact day tracking and move-year tax-home timeline support | Escalate for borderline day counts, mid-year country moves, or unclear residence-test support |

| Foreign Tax Credit (FTC) | Qualifying foreign taxes paid or accrued, with relief via credit or deduction election | Moderate to high: generally Form 1116 plus foreign-tax support records | Escalate when any income is also considered for FEIE, because you cannot claim FTC on excluded income |

If your 2026 FEIE eligibility is solid, the maximum exclusion is $132,900 per person. If eligibility is borderline, resolve that before filing, because FEIE day-count qualification is strict. Related: 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

Before you lock your filing position, pressure-test your travel and tie records in one place: Use the tax residency tracker.

Conclusion: From Anxious Operator to Confident CEO#

The strongest next step is simple: make the line between documented facts and unknowns explicit.

Keep the three pillars practical, and keep your source check practical too:

- The Congressional Record excerpt documents a bill entry (

H.R. 15682) on February 29, 1968, tied to amending the Internal Revenue Code of 1954. - That same entry shows referral to the Committee on Ways and Means.

- The Senate Finance excerpt is a download-wrapper page with a manual fallback link, not substantive policy guidance.

Before acting, run a short evidence check:

- Identify which points are directly supported by full source text.

- Note where the available excerpts do not provide enough detail.

- Resolve gaps with primary materials or professional review before making decisions.

If your facts span multiple jurisdictions or treaty treatment is unclear, pause and get professional review before acting. For related context, see The US Expat's Financial Offboarding Checklist: 15 Things to do Before Repatriating and A Deep Dive into the German Trade Tax ('Gewerbesteuer') for Freelancers.

Frequently Asked Questions

What is the most tax-efficient way for you to receive money from Europe?

For many freelancers, a clean setup is to invoice in EUR, receive payment by SEPA credit transfer into a multi-currency balance such as Wise or Revolut, and decide separately when to convert to USD. That keeps payment rails separate from FX timing and may avoid a SWIFT wire in some cases, but cost and speed still depend on your provider and corridor. Before you send each invoice, confirm the currency, beneficiary details, and payment instructions.

Does receiving money into a Wise account count as repatriation for U.S. tax purposes?

Usually not by itself. The key tax issue is income recognition, because U.S. citizens and resident aliens are generally taxed on worldwide income and income may be taxable when it is credited to you or otherwise made available, while repatriation is the later movement of cash. Keep your invoice date, service period, payment-availability date, and transfer date in one record set.

How do you avoid double taxation as a digital nomad or returning expat?

Use FEIE, FTC, or treaty relief based on your facts, and use one method per income item. Do not assume these options are freely interchangeable or automatically available. Document your choice clearly before filing, and do not claim FTC on income excluded under FEIE.

Do you need to worry about FBAR if money sits in Wise or Revolut?

You should check your actual account setup. FBAR depends on whether the aggregate value of your foreign financial accounts exceeded $10,000 at any point in the year, and whether an account produced taxable income does not change that test. Total all foreign accounts from statements, log each year's peak balances, and remember the general due date is April 15 with an automatic extension to October 15.

What does reverse-charge VAT mean on an EU invoice?

When reverse-charge treatment applies, the customer is liable for VAT rather than the supplier. The practical issue is invoice content, so include a reverse-charge reference where appropriate, but do not assume one wording fits every EU Member State. Verify your client's business details, confirm local treatment, and keep the exact issued invoice version in your records.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

U.S. Expat Repatriation Financial Checklist: Foreign Wind-Down, Compliance Cut-Over, and U.S. Relaunch

Use a phased checklist, not a flat one. The order of decisions can change your tax filings, account reporting, and cash-flow continuity. A move back to the U.S. affects how you handle worldwide income, which foreign accounts still need reporting, and how you sequence your U.S. relaunch to avoid gaps.