Quick Answer

Use a payment-first workflow. Your solo creator financial blueprint should require written terms, send complete invoices, and start work only after status is paid, not open. Keep one evidence folder per invoice ID with scope approval, delivery logs, and acceptance messages so you can answer chargebacks quickly. Then run a monthly payout reconciliation check that ties invoice totals, processor fees, and net bank deposits before you commit new spending.

Start here and stop cashflow surprises before they start#

Start with collection reliability, not growth targets. A solo creator financial blueprint is less about having a bigger revenue month and more about getting booked revenue to arrive on time, with fewer delays, fee leaks, and reversals. If you are moving from a side hustle into steady solo consulting, a creator business, or a small service team, the first upgrade is your get-paid setup.

Cash timing pressure is common, and it compounds quickly. In the Federal Reserve's 2024 small business survey, 56% of employer firms said paying operating expenses was a challenge, and 51% cited uneven cash flows. EU commercial-transaction law also notes that late payment hurts liquidity and complicates financial management. One slow client invoice can distort the whole month.

This hits harder when the business is you. A sole proprietorship does not create a separate business entity, so delays, processor fees, and write-offs can affect your personal cash position more directly. Side-work income is also still taxable. The IRS says gig economy income is taxable, and if net self-employment earnings from gig work are $400 or more, you must file a tax return.

Two early risks can reduce cash availability after you think you are paid:

- A chargeback is a cardholder-initiated dispute through the card network. If the issuer decides for the customer, the payment can be withdrawn from your account.

- A payment hold is a temporary restriction on access to funds imposed by a platform based on account activity. The exact logic varies by processor. PayPal explicitly says it may hold payments for various reasons based on account activity.

Your first control is operational. Treat invoice quality and payment status as gates, not as admin cleanup. In formal payment workflows, payment depends on a proper invoice and satisfactory performance. A noncompliant invoice can be returned within 7 days. Even if your client is not following FAR 32.905, the process lesson is the same.

Confirm the legal entity name, deliverable labels, due date, agreed payment terms, and any required tax fields before you send the client invoice. If you work with EU B2B clients, invoicing is generally mandatory for VAT purposes, so missing invoice data can create avoidable delays.

The failure pattern is predictable. Work starts on a verbal "we're good," terms stay vague, the invoice is incomplete, or funds are not actually available. Then scope shifts, approvals blur, or a dispute appears, and you are collecting from a weaker position. The fix is not more hustle. It is a cleaner order of operations and better records.

That is what the rest of this piece focuses on: a get-paid setup that clarifies payment terms, tightens invoice handling, and reduces avoidable downside from holds, disputes, and timing gaps.

Related: The European Content Creator Blueprint for Cross-Border Client Work.

What a solo creator financial blueprint actually includes#

Think of this blueprint as the set of rules you decide before work starts, so money does not depend on improvisation later. It is not just a budget. It is how you structure offers, set payment terms, time invoices, keep records, and verify payouts.

Define these decisions up front:

- Your payment terms: the mutual agreement for how and when the buyer will pay

- Your client invoice timing: when invoices go out based on contract terms, work type, and client relationship

- Your billing model by offer: how each offer is billed, including whether a retainer-style arrangement is appropriate

- Your recordkeeping system: a clear trail of income and expenses, with summaries and supporting documents such as invoices

- Your payout reconciliation owner: who matches bank deposits to underlying payment batches and invoices

A useful blueprint connects revenue design to collection reliability. If these rules change client by client without a standard, cash flow gets harder to predict.

Set the rules before kickoff, not after a delay or dispute. Decide when an invoice goes out. Decide what payment conditions must be met before work begins, when a retainer-style arrangement makes sense, and who verifies what reached the bank against invoices and payout records.

Keep reconciliation practical. If your processor offers reconciliation reporting, use it. If it does not, run a manual check so you still have a clean record of what was sold, invoiced, paid, and deposited.

You might also find this useful: The Solo Agency Blueprint for Productized Services and Subcontractor Control.

Build a revenue mix that smooths income volatility#

If you want steadier cashflow, make recurring revenue your base and layer project income on top. That reduces your dependence on one-off launches or a single pay-at-end invoice, so one delay is less likely to break the month.

Recurring payments are charges processed on a predetermined schedule, and they fit subscriptions, memberships, and long-term contracts. You do not need to force every offer into a membership model. You do need some scheduled inflow you can reasonably expect each month. When billing does not match delivery, collections stay lumpy.

Match the offer to the collection pattern#

| Offer type | Best-fit collection pattern | Why it helps | Key check |

|---|---|---|---|

| Subscription or membership | Recurring payments on a set schedule | Creates baseline recurring cashflow | Confirm the renewal schedule |

| Delivery-heavy fixed project | Milestones or progress invoicing | Splits one project into partial collections by stage | Do not start the next stage until that stage is funded or paid |

| Ongoing advisory or access | Retainer | Recurring fee for access within a defined scope | Define scope before the first invoice |

Progress invoicing lets you split one estimate into multiple invoices, so you collect partial payments over time instead of waiting until the end. Milestones apply the same logic to fixed-price work. Each stage has a defined payment, and work should start only when that stage is funded.

Use staged collections when scope risk is real#

If scope is fuzzy or delivery risk is high, avoid pure pay-at-end pricing. Break the work into stages and collect as the project moves.

This helps with scope control as much as cashflow control. Defining each milestone up front can reduce scope creep and misaligned expectations. Keep one checkpoint non-negotiable: no funded milestone, no next phase of work.

Retainers solve a different problem. They fit ongoing access rather than a single deliverable, and they rely on explicit scope boundaries from the start.

Stress-test for delay, not just demand#

A strong revenue mix can still fail if settlement timing slips. Federal Reserve reporting published December 05, 2024 notes that roughly four of every five small firms face payment-related challenges. Delayed settlement or fund availability is a major obstacle for firms collecting through third parties.

Before you count on a month's revenue, run a delay test:

- Assume one major client invoice lands late or a payout is delayed.

- Check whether subscription, membership, or retainer income still covers fixed operating costs.

- Flag any month where one end-of-project payment is required to stay current on essentials.

If that test fails, your mix is too dependent on a single collection event. Shift more revenue into scheduled recurring payments, or stage project collections earlier so cash arrives before most work is done.

Related reading: Handling Hyperinflation: A Financial Guide for Nomads in Argentina.

Set payment terms clients can accept and you can enforce#

For a one-person business, payment terms should reduce ambiguity and follow-up work, not create more of either. When one person is handling strategy and execution, unclear terms add admin load and increase burnout risk.

Treat payment terms as part of your operating process. Set your decision criteria before kickoff, then reuse that process so you are not improvising under pressure.

Choose a structure with a repeatable worksheet#

No single structure is universally better. Use the same planning questions each time, and decide case by case.

| Structure | Where it may fit | Questions to answer before you commit | Decision checkpoint |

|---|---|---|---|

| Deposit | Projects where an upfront payment is part of the agreement | How much is paid upfront, when is it due, and what starts after payment? | Confirm both sides agree to the terms before kickoff |

| Milestone payment | Work delivered in defined phases | How is each phase defined, and when are approval and invoicing expected? | Confirm the current phase terms before starting the next |

| Retainer | Ongoing work with recurring support | What is included each cycle, and how are out-of-scope requests handled? | Reconfirm scope and billing expectations each cycle |

Fill out this table as an internal decision record. The value is consistency, especially when your workload is already high.

Put key terms in writing every time#

Document the terms that matter most to your project, including payment timing, scope boundaries, and how changes are handled. Keep them in a consistent document set, for example proposal or SOW, acceptance record, invoice schedule, and written scope changes, so conversations stay clear.

Add one kickoff checkpoint#

Before you commit delivery capacity, run one final check that the agreed terms are documented and understood by both sides. If you use staged approvals or payments, repeat that same checkpoint at each stage so the project can adapt without forcing ad hoc decisions.

For a step-by-step walkthrough, see How to Create a Business Budget for Your Freelance Business.

Turn invoices into an order of operations, not admin busywork#

The invoice should work as a delivery gate, not a document you send after work is already underway. Once scope is confirmed, use the same sequence every time: lock payment terms, issue the invoice, verify payment status, then begin delivery.

That order protects your leverage. If you start before an agreed upfront payment clears, scope changes and payment drift are much harder to manage.

Use one sequence every time#

Use one repeatable flow so payment decisions do not get made in the middle of delivery.

- Confirm final scope in writing, using deliverable labels you will reuse on the invoice.

- Lock payment terms before kickoff, including any upfront requirement.

- Send the client invoice with the agreed details and payment instructions.

- Check payment status before fulfillment or delivery starts.

- If payment is late, partial, or failed, move it to an exception path instead of continuing work.

If your platform uses statuses, treat paid as the green light for kickoff. Statuses like open should stay blocked until payment is confirmed.

Standardize the fields that prevent arguments#

Use one invoice template and keep the wording aligned with your proposal or SOW.

As a baseline, include:

- A unique identification number

- The customer company name and address

- Deliverable or service labels that match agreed scope

- The agreed payment terms (for example, due date and any upfront requirement)

- VAT amount where applicable

Before sending, run a quick check: legal names match the agreement, deliverable labels match scope, and payment terms match what was agreed. If no payment date is agreed, UK guidance defaults payment to within 30 days of receiving the invoice or goods/services, so set terms explicitly instead of relying on defaults.

Add status checks and escalation points#

Track clear checkpoints: invoice sent, payment confirmed, reminder triggered, exception escalated, and closed in reconciliation.

If an invoice stays open because payment is incomplete or fails, route it to exceptions immediately. Send a reminder first. If reminders fail, escalate with a letter of demand.

Then reconcile by linking the invoice ID to the payout record so you confirm funds received, not just invoice status. This matters because card payments can later be reversed through chargebacks, and UK guidance notes exposure can extend up to 120 days.

Cut risk before it becomes a hold, dispute, or write-off#

Once invoicing is standardized, the next job is to protect the transaction record. A chargeback starts when a cardholder questions a payment with their issuer, and you can lose both transaction revenue and the goods or services already delivered.

Process gaps increase that risk quickly. If scope, acceptance proof, and invoice records are unclear, it becomes harder to show what was agreed, what was delivered, and why the charge was valid.

Build the evidence pack while the job is live#

Build your evidence before any dispute appears. If a network or processor asks for supporting evidence, you usually get a short response window. It is often 7 to 21 days depending on the card network. Missing that deadline can automatically lose the dispute.

Tie every proof item to the invoice ID from day one. For each project, keep a compact pack with:

- Signed proposal, SOW, or approval email that matches billed deliverables

- Client invoice, payment confirmation, and any deposit or milestone record

- Delivery logs, such as file timestamps, portal uploads, meeting notes, or sent links

- Written approvals, revision signoff, and final acceptance messages

Before marking work complete, run one check: can someone open the invoice record and see scope, delivery date, and client acceptance without hunting across tools? Keep evidence grouped by type, such as receipts, communications, policies, and system logs, so it is faster to review under deadline pressure.

Treat payment holds like an expected exception#

Assume holds will happen and decide your response in advance. A payment hold is a temporary restriction while a transaction is reviewed or a dispute is involved. Holds can also come from account inactivity, high-risk transactions, tax issues, or backup withholding, depending on the provider.

That means cash can stall even when a client thinks payment is done. In some payout setups, paused in-flight payouts can stay pending for up to 10 days. PayPal notes some held funds are released 7 days after an order is marked Completed.

Set rules before this happens:

- define what pauses if a hold appears, such as subcontractor spend, ad spend, or discretionary withdrawals

- keep a ready client message that confirms status, explains the delay, and gives the next update time

- assign one check, even if it is just you, to review processor status, payout status, and whether delivery continues, pauses, or shifts to a lower-risk milestone

One avoidable mistake is treating authorized or pending funds as fully settled.

Choose checkout friction by risk tier#

Set checkout controls by risk tier, not by habit. Streamlined checkout can improve conversion, while fraud controls are meant to block payments that might later turn into fraudulent disputes.

Use lower friction for known, repeat clients when risk is lower. Use stronger verification and tighter approval steps for first-time buyers, high-ticket work, rushed requests, or mismatched billing details, even if completion rate dips.

Place friction where replacement cost, delivery effort, and dispute exposure are highest. That keeps payment risk controls practical instead of slowing every transaction equally.

We covered this in detail in Mental Game of Freelancing Blueprint for Confident Solo CEOs.

Keep a cashflow buffer policy you can follow in bad months#

A cashflow buffer works best when it is tied to real costs, kept separate from operating cash, and funded automatically. Keep it in a separate business savings account, set a target from actual monthly cash use, and automate contributions so progress does not depend on willpower during busy stretches.

A common benchmark is 3 to 6 months of expenses, but that is a starting point, not a universal rule. If collections are uneven, size the target around both fixed and variable costs and your actual burn rate. Review what leaves the business each month across rent, software, payroll or contractor commitments, set-aside taxes, insurance, debt payments, and variable delivery costs.

Size the buffer from cash usage, not optimism#

Your reserve should protect continuity in a bad month, not mirror a best-case forecast. If one late invoice or short payment delay would force you to pause delivery, miss payroll, or cut tools needed for current clients, the buffer is probably too thin.

Use a simple check: if your largest expected payment arrives late, how long can you keep operating without new sales? If the answer is "not long," increase the target. Short delays can still trigger ripple effects when reserves are limited, and uneven cash flow remains a common small-business challenge.

Fund it from your most predictable inflows#

Build the buffer with scheduled transfers, then top it up when stronger months allow. If you have recurring inflows such as retainer, subscription, or membership revenue, routing a fixed amount or percentage on a set schedule can be easier to forecast than relying only on one-off project income.

You can add extra contributions from deposits or milestone payment receipts when projects close cleanly, but avoid depending on leftover cash from irregular launches. Scheduled automatic transfers are usually more reliable than manual sweeps.

Run one monthly check: confirm the transfer happened, confirm the funds stayed in the separate reserve account, and confirm the balance is moving toward your target.

Decide your bad month triggers before the bad month arrives#

Set withdrawal triggers in writing before pressure hits. Ad hoc withdrawals for non-urgent spend can drain the reserve before continuity risk is real.

Document the few cases that qualify, such as:

- delayed collections that threaten core operating expenses

- short payment delays that create continuity risk

- essential delivery costs required to complete already sold work

- urgent continuity needs, not discretionary growth spend

Also set a warning line for spending controls. For example, if collections keep slipping in your business, pause discretionary spend first, such as new tools, optional contractors, travel, experiments, or nonessential marketing, before cutting essential delivery capacity.

After any withdrawal, define the refill plan immediately: how much to replace, from which receipts, and by what date.

This pairs well with our guide on Build a Creator Community You Can Run Like a Business.

Choose payment channels based on reliability and margin#

Choose payment channels by one rule first: use the path that keeps collections dependable and margins visible, then layer in convenience. In practice, score each option on payout predictability, customer friction, and reconciliation clarity before you commit.

Match the channel to the sale#

Direct invoices, storefront platforms like Shopify or Etsy, and digital-product rails like Payhip or Amazon KDP can serve different collection needs depending on your setup. Assign each one to the sale type it handles best in your business. The label matters less than whether you can enforce your payment terms, track what was collected, and keep delivery moving when cash timing shifts.

For each path, test one live transaction end to end and confirm you can reconcile gross, deductions, and net in your records. If terms or payout pages show an Effective Date, save that version so you have a dated reference if policies change later.

Judge channels on four mechanics that affect cashflow#

Look at the mechanics that change real cash availability:

- Fee drag: Track what comes off gross sales so true margin is visible.

- Settlement timing: Track the gap between customer payment and usable funds.

- Dispute handling: Check what records you can keep and submit if a payment is challenged.

- Control over payment terms: Confirm whether the channel can support the terms you rely on.

| Channel family | Typical fit in your operating model | Payout predictability score (1-5) | Customer friction score (1-5) | Reconciliation clarity score (1-5) | What to verify before relying on it |

|---|---|---|---|---|---|

| Direct invoices | Can fit work where you need explicit terms and clear acceptance records | ___ | ___ | ___ | Can you confirm collection status and match each invoice to a bank receipt without guesswork? |

| Storefront platforms (for example Shopify or Etsy) | Can fit offers sold through a platform checkout flow | ___ | ___ | ___ | Do reports explain orders, deductions, refunds, and net deposits clearly enough for your books? |

| Digital-product rails (for example Payhip or Amazon KDP) | Can fit standardized digital offers or platform-native publishing | ___ | ___ | ___ | Can exported reports tie back to cash actually received in a way you can audit month-end? |

Separate service and product collection paths#

If you sell both services and products, keep at least two collection paths so one platform event does not control every inflow. That does not remove hold risk, but it can reduce single-channel exposure when one rail is temporarily interrupted.

This matters in routine situations too, not just extreme ones. A platform can be unavailable during scheduled maintenance, so a separate path helps you keep collecting while one route is paused.

Treat regional and compliance caveats as decision points#

Read "where supported" and "when enabled" literally, especially for cross-border use. If country options or regional selectors appear in an interface, treat that as a signal to verify availability in your own account before you forecast cashflow from that feature.

Before launch, confirm your country and account setup are supported. Then confirm the report detail is sufficient for reconciliation. Make these checks part of channel selection, not a cleanup task after money starts moving.

Reconcile money monthly so leaks do not compound#

Reconcile money on a regular cadence before you close the books. Otherwise, unresolved mismatches can quietly distort your cash position. The goal is to match four views of the same funds: invoice amount, processor status, fees or deductions, and net cash received in your bank.

Use payout reconciliation reports to tie bank deposits to underlying transactions, then complete bank reconciliation so your accounting records match actual account activity. If you use Stripe, automatic payouts keep transaction-to-payout links intact. If you create manual payouts, Stripe puts reconciliation responsibility on you.

Match movement, not just totals#

A month-end total that "looks close" is not enough. For each payout or receipt, confirm:

- invoiced amount

- amount paid

- fees or dispute deductions

- net amount that reached the bank

Before month-end decisions, confirm your ledger and processor balance or wallet view reflect the same expected movements. Treat funds marked pending as unavailable until status changes. For example, Stripe states pending funds cannot be withdrawn or spent yet. PayPal labels payments as Pending or On hold when they are under review or temporarily held due to review or dispute.

Tag exceptions by type so the fix is obvious#

Classify each mismatch so the next step is clear.

| Exception type | What it usually means | What to check next |

|---|---|---|

| Short-paid client invoice | Payment is less than invoiced | Compare invoice total, received amount, and any approved partial-payment note |

| Delayed payout | Transaction exists, but bank receipt has not arrived | Check payout status, expected payout date, and failed payout details if available |

| Duplicate charge or duplicate transaction | Same payment or entry appears twice | Review processor export and ledger for duplicate or missing entries |

| Chargeback | Cardholder dispute triggered formal reversal | Confirm original payment, reversal, and any dispute fee shown |

| Unresolved payment hold | Funds are under review or tied to a dispute | Check status details, release conditions, and client communication history |

Handle chargebacks quickly. Stripe says the original payment is reversed immediately and your balance is debited for the payment amount plus dispute fee.

Use a close checklist that names an owner#

Use a close checklist so open items do not roll forward silently:

- item ID or invoice number

- exception type

- owner

- due date

- current status

- resolution notes

- supporting evidence, such as payout export, invoice copy, bank line, or dispute message

This still applies if you are a team of one. Naming an owner forces action.

If numbers do not tie, check for record edits first. Accounting tools commonly flag missing or duplicate transactions, plus previously reconciled entries that were later edited or deleted. If a line cannot be explained, do not close the month as settled.

Add compliance and tax checkpoints at the right moments#

Once your cash handling is in order, add compliance checks at the moments that matter. Use a staged checklist: intake, before the first client invoice, and before year-end close. You usually do not need bank-style KYC on every client; those CDD obligations are scoped to obliged entities and covered financial institutions. You do need a proportional process for tax documents, VAT checks, and proof that your payment terms and payments match.

Run the checks in sequence instead of all at once. At intake, capture legal name, billing country, entity status, signed terms, and tax profile status. Before kickoff or a deposit request, confirm whether the client's jurisdiction or program changes what you must collect. For EU cross-border work, VAT rules are standardized at EU level but applied differently by country, so do not assume one rule or threshold works everywhere.

Check cross-border details before money moves#

If a client provides an EU VAT number, validate it in VIES before finalizing the invoice. An invalid VIES result means the number is not registered in the relevant national database. A valid result is still not final proof on its own, because VIES depends on national-source data and procedures vary by country. If you work with UK clients, note that VIES stopped validating UK (GB) VAT numbers through that service path on 01/01/2021.

For U.S. tax forms, collect the right document before payment when your payer relationship requires it. Form W-9 provides a correct TIN to payers filing information returns, while Form W-8 BEN is for a foreign person providing tax status information to a U.S. withholding agent or payer. Avoid collecting forms after a retainer or milestone payment lands.

Keep a lightweight evidence pack#

For each client, keep one folder with:

- signed terms and approved scope

- invoice trail and payment confirmations

- tax form status, if relevant

- supporting business records such as invoices, receipts, deposit slips, or paid bills

This evidence pack supports both your books and your tax return. If you are still operating like a side hustle, use this as your baseline, then deepen filing and estimated-tax setup once income is consistent. The IRS says gig income is taxable, you must file if net self-employment earnings reach $400, and you may need estimated payments if you expect to owe at least $1,000 after withholding and refundable credits. For that next step, read How to Handle Taxes for a Side Hustle.

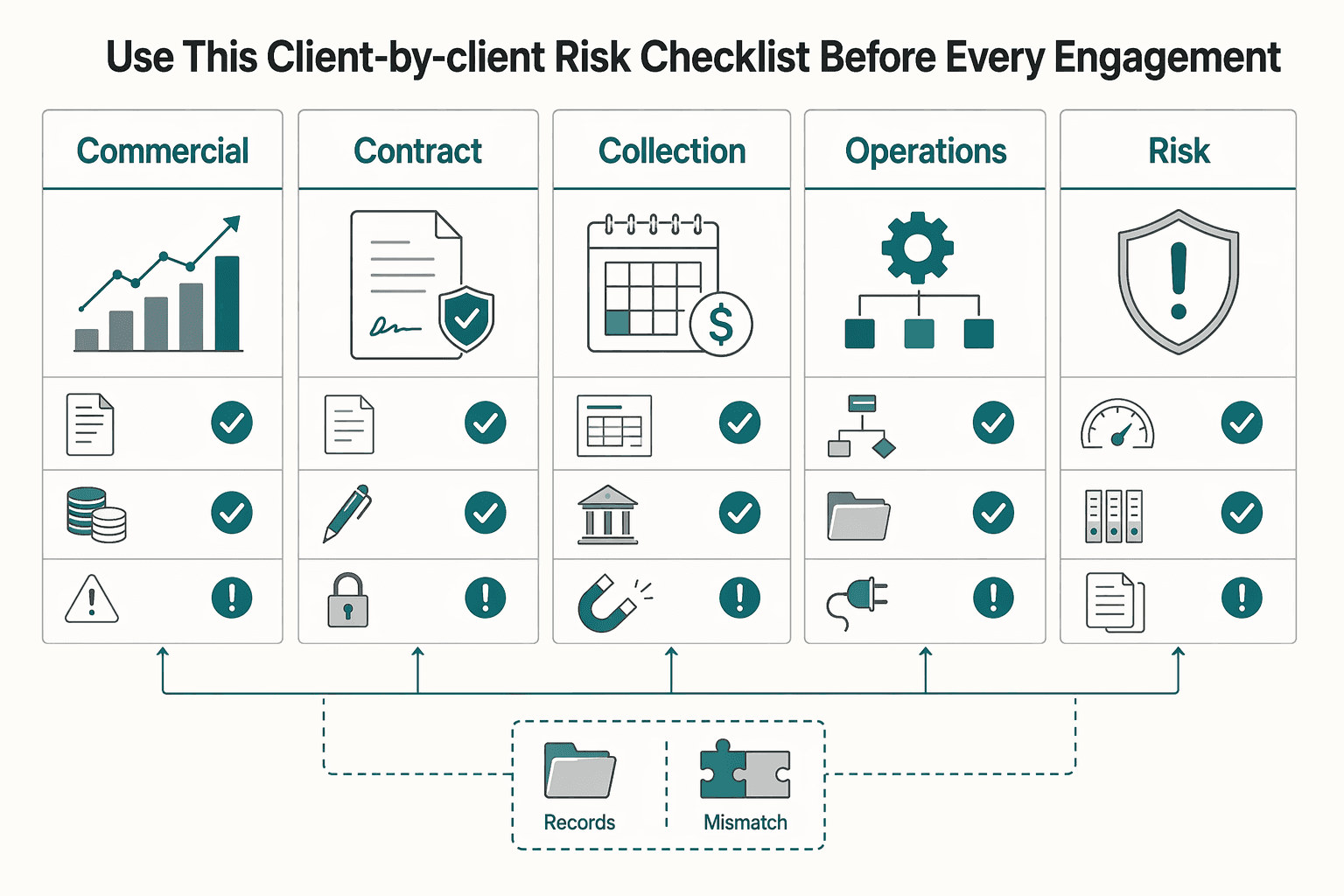

Use this client-by-client risk checklist before every engagement#

Before you start work, run one hard gate. If any of these five checks is missing, do not begin.

| Check | Focus | Key detail |

|---|---|---|

| Commercial | Match billing model to delivery risk | A retainer fits ongoing services, a subscription fits recurring access payments, and milestone payment structures fit staged delivery where each step is funded before the next begins |

| Contract | Lock scope, rates, and payment terms before kickoff | In NYC, contracts at $800 or more must be written, including agreements with the same hiring party totaling $800 within a 120-day period; if no payment date is listed, payment is due within 30 days after completion |

| Collection | Confirm first payment before production starts | Verify paid status and confirm funds or a funded milestone before kickoff; Upwork fixed-price includes a 14-day review period after submission and a five-day security hold before withdrawal |

| Operations | Set reminders and assign reconciliation ownership | QuickBooks can schedule reminders up to 90 days before or after due dates, and Xero supports up to five reminders |

| Risk | Prepare dispute and hold response in advance | Keep signed terms, invoices, approvals, and delivery records together, and keep a ready client message for payment holds |

1. Commercial check. Match pricing model to delivery risk#

Choose the billing model that fits how the work is delivered. A retainer fits ongoing services, a subscription fits recurring access payments, and milestone payment structures fit staged delivery where each step is funded before the next begins.

If scope is still moving, approvals are likely to drag, or the client is new, avoid relying on one final invoice. Upfront or staged collection reduces the risk you carry.

2. Contract check. Lock payment terms before work starts#

Set scope, rates, and payment terms before kickoff. At minimum, state due dates, late-payment consequences, and how follow-up or escalation will work.

If your work is covered by NYC freelance rules, contracts at $800 or more must be written, including agreements with the same hiring party totaling $800 within a 120-day period. Those contracts must state work, pay, and payment date, and if no date is listed, payment is due within 30 days after completion. New York State added Article 44-A on August 28, 2024, so clear written terms matter.

3. Collection check. Treat first payment as a non-negotiable gate#

Treat the first deposit or kickoff client invoice as a non-negotiable gate before production starts.

Verify paid status in your system and confirm funds or a funded milestone are committed before kickoff calls, production calendars, or file access go live. On milestone platforms, funding and availability can differ. For example, Upwork fixed-price includes a 14-day review period after submission and a five-day security hold before withdrawal.

4. Operations check. Assign reminder flow and reconciliation ownership#

Set reminder timing before invoices are due, and define escalation if reminders are ignored.

Automation is available. QuickBooks can schedule reminders up to 90 days before or after due dates, and Xero supports up to five reminders. Also assign one owner for payout reconciliation so payouts are matched to settled transactions and mismatches or delays are caught quickly.

5. Risk check. Keep dispute and hold response ready#

Prepare a dispute file before anything goes wrong. A chargeback is a cardholder dispute with their issuer, and responses usually require reason-specific text, evidence, and a clear counterargument.

Keep your signed terms, invoices, approvals, and delivery records together so you can respond quickly with evidence. A payment hold is different from a chargeback, but it also needs a plan, including a ready client message so a temporary hold does not turn into silence or mistrust.

Before kickoff, turn this checklist into a repeatable terms package with the freelance contract generator.

Build consistency first and scale from there#

Consistency is the first scaling move when cashflow is fragile. Use a repeatable get-paid sequence before you chase bigger revenue claims.

If you adopt only three habits now, make them stronger written payment terms, a pre-work deposit policy where appropriate, and monthly payout reconciliation. These controls do not guarantee profit, but they can reduce avoidable delays and payment surprises.

Start with terms you can actually enforce#

Your terms should clearly state what is owed, when it is due, and how the client should pay. Keep those same core terms in both the contract and the invoice so payment expectations stay aligned.

If you work in NYC, Freelance Isn't Free sets a clear floor: contracts at $800 or more must be in writing, including agreements with the same hiring party that total $800 in a 120-day period. The contract must include the work, the pay, and the payment date, and if no payment date is listed, payment is due within 30 days after completion. Outside NYC, this is still a practical baseline to copy.

Make the deposit rule real#

Treat deposits as policy, not as case-by-case negotiation. Freelancers Union recommends collecting part of payment upfront or in installments so you are not carrying all the risk.

Use "payment confirmed" as the true start gate, not "invoice sent." A disputed card payment can become a chargeback that reverses funds. Payment platforms can also place funds on hold based on account activity. That is why "paid" and "available to use" are not always the same thing.

Reconcile payouts before you make spending decisions#

Reconcile monthly before you spend: match your records to bank and card statements. This is how you catch bookkeeping errors, suspicious activity, and payout gaps early.

At month-end, compare:

- Invoice totals

- Processor or marketplace payout reports

- Fees and dispute deductions

- Actual bank deposits

Your checkpoint is simple: expected net receipts should match deposits plus clearly identified holds, reserves, or pending payouts. If not, flag the exception immediately.

As channels grow, timing differences matter. Stripe payout schedules can be daily, weekly, monthly, or manual. Manual payouts typically arrive in 1-4 business days after initiation. Shopify notes payouts can take an additional 1-3 days to appear in your bank and says settlement timing varies by country, risk level, and transaction type. Etsy may also place a percentage of some new-sale funds in reserve for a period. Practical rule: do not spend from gross dashboard numbers.

Get these three habits stable first, then scale into taxes, income mix, and hiring with How to Handle Taxes for a Side Hustle, The Best Ways to Diversify Your Income as a Freelancer, and Hiring Your First Subcontractor: Legal and Financial Steps.

If you want one operational system for collecting client payments and managing payout flow as you grow, review Gruv for freelancers.

Frequently Asked Questions

What is a solo creator financial blueprint in practical terms?

A solo creator financial blueprint is your payment system: what you sell, when you invoice, when work starts, and what proof you keep if payment is challenged. It is less about budget theory and more about collection discipline. If you cannot clearly answer what triggers payment and what proves delivery, the setup is still too loose.

How do I move from side hustle income swings to stable monthly cash flow?

Start with predictable cash-in dates, not one final invoice at the end of a project. Keep recurring work where possible, and when risk is higher, collect upfront or in funded milestones so one delay does not break the month. Before each month starts, map expected payments to due dates, then record transactions daily, which the IRS generally recommends.

What should payment terms include for freelance or creator client work?

At minimum, written terms should state the work, the pay, and the payment date. In NYC, freelance contracts at $800 or more must be in writing, including agreements with the same hiring party totaling $800 within a 120-day period. In NYC, if no payment date is listed, payment is due within 30 days after completion. New York State added Article 44-A on August 28, 2024, so in New York, clear written terms are a core protection.

When should I use a deposit, milestone payment, or retainer?

Use a deposit when kickoff starts fast, the client is new, or your downside is high if they disappear. Use milestone payment when delivery is staged and each stage should be funded before the next begins. Use a retainer for ongoing work in a stable relationship.

How do I reduce late payments and chargeback risk without scaring off clients?

Keep the process calm and standard: clear scope, clear due date, prompt invoicing, payment confirmed before production, and on-time reminders. A chargeback is the outcome of a payment dispute process, so build your evidence file from day one. Keep signed terms, invoice records, approvals, delivery confirmations, and customer communications organized so you are not reconstructing proof after scope or timeline drift.

What is the minimum finance stack I need to run this reliably as one person?

Keep it lean: a business bank account, one recordkeeping system that summarizes transactions, a way to send and track invoices, and one client folder for contracts, approvals, and payment proof. The SBA says to open a business bank account as soon as you start accepting or spending business money. The IRS says it is generally best to record transactions daily.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far/32.905trusted

- business.gov.au/finance/financial-trouble/what-to-do-when-yo...trusted

- commission.europa.eu/topics/business-and-industry/doing-business-...trusted

- dol.ny.gov/freelance-isnt-free-acttrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- fdic.gov/consumer-resource-center/2025-01/saving-unex...trusted

- irs.gov/businesses/small-businesses-self-employed/ma...trusted

- irs.gov/businesses/gig-economy-tax-centertrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Hiring a Subcontractor for the First Time Without Costly Surprises

**Start with a risk-control sequence, not an ad hoc handoff.** As the Contractor, your goal is simple: deliver cleanly, control scope, and release payment only when the work and file are complete.

How to Handle Taxes for a Side Hustle

If you want less stress at filing time, use sequence instead of shortcuts. When one year includes payroll income, contractor income, and time in more than one country, the order of operations matters. This guide gives you a defensible path so you can make each decision once, document it, and avoid rebuilding the return later.

The Best Ways to Diversify Your Freelance Income: A Risk-First Framework

Most freelancers add new revenue lines reactively: a course after a slow month, an affiliate link because someone else said it works, a consulting offer because one client asked for it once. The result is usually the same: more moving parts, unclear priorities, and no real protection when one major client or platform wobbles.