Quick Answer

Start with a same-day corridor pilot, not the marketing headline. In the fintech race to zero fx fees, the safer choice is usually the provider with the best verified landed outcome after spread, payout charges, and exception costs are included. The article shows that explicit FX fees can be low while total cost still rises, and it recommends evidence capture before migration. Use the quote-to-settlement trail as your decision baseline, then scale only after reliability and controls are proven.

The race to zero sounds good but can cost you more in practice#

A zero FX fee headline is not the same thing as a low-cost payment. If you are choosing a setup for cross-border payments, the real goal is the lowest-risk total cost, not the cheapest number on a fintech landing page.

| Lens | What it covers |

|---|---|

| Total cost | Explicit fee, spread, payout charges, and any downstream return or correction costs |

| Reliability | Whether the payment lands predictably in your actual corridor and method |

| Controls | Audit trail, status visibility, and how exceptions are handled |

| Evidence quality | What is documented and testable versus what is just claimed |

Start with the terms, because this is where most comparisons break down. An FX fee is the visible line item you can point to on a quote or receipt. The foreign exchange spread is different. It is the gap between a benchmark market rate and the rate you actually get. A provider can also create hidden FX fees by baking cost into the exchange rate instead of showing it as a separate charge. Wise says this plainly on its pricing page: other providers may "hide fees in the exchange rate," while it says it uses the mid-market rate as its benchmark.

That distinction matters more than the headline fee. A provider can advertise low or zero explicit fees and still cost you more if the rate is widened or the payment method is more expensive. The race to zero only looks buyer-friendly if you ignore everything around the conversion.

What you can usually verify from public information is narrower than the marketing suggests. You can often see whether pricing is usage-based, whether a provider names its benchmark rate, and whether fees vary by sending currency, receiving currency, or payment method. For example, Wise says you "only pay for what you use," that fees start from 0.57%, that pricing depends on the sending currency, receiving currency, and payment method, and that discounts can apply above 25,000 USD.

Useful, yes, but still incomplete. Those facts do not, on their own, tell you your total cost in every case. When you compare Wise, Revolut, Airwallex, or an infrastructure-first option, use four lenses at the same time:

- Total cost: explicit fee, spread, payout charges, and any downstream return or correction costs.

- Reliability: whether the payment lands predictably in your actual corridor and method.

- Controls: audit trail, status visibility, and how exceptions are handled.

- Evidence quality: what is documented and testable versus what is just claimed.

A practical checkpoint is to run the same amount and corridor through your shortlist on the same day. Save the quote timestamp, fee screen, rate shown, and final settlement record. If a provider cannot give you a clean explanation for rate source or method-based pricing, treat that as a red flag before you migrate volume. Fintech promises more efficient finance, but even the April 28, 2020 CRS report notes that new technology can also create "unanticipated financial losses." That is the right mindset for the rest of this comparison.

What fee compression changes in fintech strategy#

When quoted FX costs cluster, price is no longer the best tie-breaker. If two providers look similar on fees, choose the one with stronger controls, clearer auditability, and better exception handling, because that is usually where total cost diverges later.

This is a market-structure shift, not just marketing language. Treasury's November 2022 report describes both value-chain disaggregation and later re-aggregation/re-bundling, while BCG's September 2025 Global Payments Report (23rd annual) says software platforms are taking a larger share of payments revenue and raising expectations on capability, speed, and integration. In practice, that points competition toward interoperable infrastructure, data flows, and execution quality, not just headline pricing.

Growth alone is not proof of a durable FX-fee edge, even when expansion stories are compelling. The sources here do not establish Africa-specific fee superiority. They do show persistent crowding; McKinsey's February 2016 view tracked more than 2,000 startups and estimated as many as 12,000, which signals competition rather than durable advantage.

A zero-fee hook may work in consumer contexts, but B2B buyers usually need operational proof:

- Reconcile quote, rate, and settlement back to the invoice.

- Enforce approval policy before conversion.

- Track payout status through completion.

- Resolve holds, rejects, returns, and reversals with a clear owner and record.

That standard matters more as regulatory focus expands and sanctions/geopolitical risk stay active. Ask each provider for one complete payout trail: quote timestamp, applied rate, fee components, internal transfer ID, payout status events, and any return/reversal reference. If that record is hard to produce in UI, API, or exports, small pricing differences can disappear in month-end cleanup.

When fees are close, the common failure is not a fake quote. It is thin controls around a real quote. Treasury explicitly flags reliability/fraud and data privacy/security as risk areas, so prefer the provider whose records make it easy to prove what happened, who approved it, and how failures are resolved.

Build a total-cost view before you compare providers#

A "zero fee" headline is not enough if the rate treatment or downstream payout costs make the total higher. Compare quoted price, settled outcome, and exception handling side by side before you decide between Wise, Revolut, and Airwallex.

| Provider | Explicit FX fee | Rate / spread treatment | Transfer or payout charges | Return fees | Exception-handling cost | Non-price checks to capture |

|---|---|---|---|---|---|---|

| Wise | Wise shows pricing starting from 0.57%, and says the fee varies by currency and can depend on how you pay for your transfer | Wise says it uses the live mid-market rate with a separate upfront fee | Verify by corridor, currency, and payment method; Wise also says some currency and payment-method combinations saw a small fee increase | Verify from your route and records | Verify who owns fixes and what records you receive when something fails | Quote validity window, stale-quote handling, payout status visibility, failed-payment support path |

| Revolut | Verify from live quote and pricing terms for your corridor | Verify whether the quoted rate tracks a benchmark or includes spread | Verify route and payout-method charges | Verify | Verify | Quote validity window, stale-quote handling, payout status visibility, failed-payment support path |

| Airwallex | Verify from live quote and pricing terms for your corridor | Verify whether the quoted rate tracks a benchmark or includes spread | Verify route and payout-method charges | Verify | Verify | Quote validity window, stale-quote handling, payout status visibility, failed-payment support path |

Wise is the only provider in this section with sourced pricing detail, so treat it as a checklist for what to confirm across all providers, not as proof of the cheapest total cost. One important variable is Wise's 25,000 USD monthly threshold: Wise says discounts apply after you pass that level for the rest of the month, then reset on the first.

Check the live quote against the settled outcome#

Run the same corridor, amount, and payout method through each provider on the same day. Save the quote screenshot, timestamp, shown rate, fee breakdown, and expected delivery estimate, then save the final settlement record after completion. If available, archive transfer IDs, payout status events, and any return references.

This gives you a like-for-like comparison and shows whether each provider can connect the quote to the final result for reconciliation.

Add the fields pricing pages skip#

Add columns for quote validity windows, stale-quote handling, payout reliability, and failed cross-border payment support paths. Those fields often decide real operating cost when issues occur, even when headline pricing looks similar.

Use a simple rule: if "zero fee" comes with a wider spread or higher downstream payout cost, it is not the cheaper option.

For a step-by-step walkthrough, see The Best Way for a UK Freelancer to Get Paid by an Australian Client.

Use a buyer decision rule based on your operating pattern#

Use one rule: pick based on how payments actually show up in your business, not on headline fee language. An occasional freelancer invoice and recurring, payroll-like B2B payments create different operational risk, so they should not be judged the same way.

Match the tool to the payment pattern#

- Occasional invoices, low volume, few corridors: prioritize transparent pricing and low setup friction.

- Recurring B2B payments, growing team, month-end pressure: prioritize controls, clean reconciliation records, and clear exception handling.

Before switching, test your real payment pattern: destination country, currency pair, payout method, and typical transfer size. Then keep the quote record, timestamp, expected delivery estimate, settlement record, and transfer references together.

Run the corridor check before you commit#

Do not make this a brand-level decision. Validate the specific routes you actually run, then decide from those results. If you pay different countries or use different payout methods, treat them as separate checks until your own records show consistent outcomes.

Trust evidence over promo language#

Put more weight on records you can verify than on promotional fee claims. Ask for the operational trail you will need later: status history, failure path, and reconciliation-ready exports.

A broader caution: BIS reports in a different fintech context that after CCPA (identified there as a 2020 privacy law), fintechs showed more individualized pricing. That is not evidence about FX or cross-border payouts, but it is a useful reminder not to rely on blanket pricing narratives.

Verify reliability and controls before switching#

Do not switch on price alone; switch only when the provider can show how payments complete, fail, and reconcile in your real workflow. The corridor test shows cost when things go right. This step checks whether operations and compliance still hold when they do not.

Use a pre-switch checklist, but treat it as evidence gathering, not vendor marketing. Ask each provider to show sample onboarding gates, hold/exception statuses, payout lifecycle visibility, event/webhook behavior, and reconciliation exports, then verify those same items in a sandbox or pilot.

| Checkpoint | Evidence to request | Pilot validation |

|---|---|---|

| Onboarding and account gating | Required documents, review path, and rejection handling | Whether your entity setup can complete onboarding without repeated manual rework |

| Holds and exceptions | What status appears during a hold and how resolution is communicated | Whether operators can distinguish a hold from a normal delay and track it with a stable reference |

| Lifecycle visibility | Status trail from creation to settle/return | Whether timestamps, IDs, and outcomes are consistent and exportable |

| Events/webhooks | Sample payloads and ordering for lifecycle changes | Whether your environment receives complete, deduplicated status changes |

| Reconciliation data | CSV/API fields for IDs, fees, rate, settled amount, and returns | Whether one payout ties cleanly to invoice, ledger entry, and bank movement |

Ask for an evidence pack before you sign#

Require a sample payout lifecycle, one failed transfer path, one reversal/return path, and audit-trail export fields. If a vendor cannot show exception behavior before contract, treat that as a risk signal for recurring cross-border payments.

Add the EU compliance check before rollout#

For European Union activity, confirm tax handling against the specific VAT program you are using. If treatment is complex, VAT Cross-border Rulings (CBR) can be used to request an advance ruling on complex cross-border transactions. The request is filed in the participating EU country where you are VAT-registered, under that country's VAT-ruling conditions; when multiple companies are involved, one company should file on behalf of the others.

| EU check | What the article says | Grounded detail |

|---|---|---|

| VAT Cross-border Rulings (CBR) | Can be used to request an advance ruling on complex cross-border transactions | The request is filed in the participating EU country where you are VAT-registered; when multiple companies are involved, one company should file on behalf of the others |

| One Stop Shop | Allows registration in one Member State for VAT declaration and payment | Guidance explicitly covers record keeping and audits; the EU-wide threshold is EUR 10 000; the B2C e-commerce VAT rule change took effect on 1 July 2021 |

| SME cross-border scheme | Check eligibility before designing process around it | One condition is turnover not exceeding EUR 100 000 in the current and previous calendar year; the stated registration process should not take longer than 35 working days after receipt of prior notification |

| GDPR | Is a separate check | Confirm those points directly with the vendor and your legal/privacy owners before rollout; this grounding set does not define GDPR handling or data-retention duties |

For covered VAT activity, One Stop Shop allows registration in one Member State for VAT declaration and payment, and OSS guidance explicitly covers record keeping and audits. In this context, the EU-wide threshold is EUR 10 000, and the B2C e-commerce VAT rule change took effect on 1 July 2021.

If you are a small enterprise, check SME cross-border scheme eligibility before you design your process around it. One condition is turnover not exceeding EUR 100 000 in the current and previous calendar year, and the stated registration process should not take longer than 35 working days after receipt of prior notification.

GDPR is a separate check. The material here does not define GDPR handling or data-retention duties, so confirm those points directly with the vendor and your legal/privacy owners before rollout. For adjacent context, see GDPR for Freelancers: A Step-by-Step Compliance Checklist for EU Clients.

Then run a live pilot week with small real payments and verify end-to-end reconciliation, including wallet/balance movement where relevant. If your internal ledger, platform records, payout IDs, and bank settlement do not reconcile one-to-one, the apparent savings are weaker than they look.

Red flags that make zero-fee claims risky#

Treat a zero-fee claim as unverified until you can see how costs and exceptions work in a real payment flow. "Free" is a headline, not an operating model.

| Red flag | Why it is risky |

|---|---|

| Market-size or growth narrative instead of transaction-level evidence | Scale projections do not show your all-in corridor cost or failure outcomes |

| Headline pricing without mechanics from quote to settlement to exception handling | Pricing may not show how cost actually moves through the payment flow |

| Speed or acceptance claims without clear approval-rate evidence | Performance claims stay incomplete without evidence on the share of attempted payments that are authorized |

| Documentation does not clearly show what records you can keep when a payment is held, returned, or reversed | You may not be able to verify cost, status, and exception handling from your own records |

Red flags to screen for first:

- The claim leans on market-size or growth narratives instead of transaction-level evidence. A projection like cross-border flows reaching

$250 trillion by 2027signals scale, not your all-in corridor cost or failure outcomes. - Pricing shows a headline but not the mechanics from quote to settlement to exception handling.

- Performance claims mention speed or acceptance without clear approval-rate evidence, the share of attempted payments that are authorized.

- Documentation does not clearly show what records you can keep when a payment is held, returned, or reversed.

Before you move forward, get written answers on the exact fee components at quote and settlement, any charges on returns or failed transfers, and which IDs and status fields persist through exceptions. Then run one live test payment and compare quote, settlement, and exception records for that same transfer.

If those records do not connect cleanly, pause. Trust drops quickly when loss and failure handling are unclear, and Pew reported that nearly 30% of consumers avoided mobile payments to protect against loss of funds.

How to use AI and automation claims without being misled#

Treat AI as a supporting claim, not a buying reason, until the provider can tie it to an operational result you care about and show the controls behind it. The key question is not whether a provider uses AI, but whether automation improves payment operations without adding new risk.

Start by pinning down scope. If a provider says its models improve FX performance, ask what the model actually predicts or decides. Predicting transaction volumes is not the same as reliably predicting FX rate movements, so do not treat those claims as interchangeable.

For B2B payments, ask outcome-linked questions in plain terms:

- Does automation reduce failed payouts in the corridors you use?

- Does it shorten resolution time when a transfer is held, returned, or misrouted?

- Does it improve reconciliation quality by preserving reference IDs, status changes, and exception reasons?

- When automated decisionmaking flags something, where does human review start, and what audit trail do you get?

Then verify with evidence from a live use case, not a demo. Ask for a sample payout lifecycle, one exception case, timestamps, status fields, and the final settlement record tied back to your ledger or export.

That caution is not anti-automation. CRS report R46332 says fintech can improve efficiency and outcomes, but it can also create unanticipated financial losses, and automated decisionmaking can behave in unintended ways. Legal scholarship also warns that AI can enable financial misinformation and market manipulation. If controls are vague, keep the AI story secondary to price transparency, failure handling, and auditability.

Related reading: A Deep Dive into Deel's Pricing and Fees for Contractors.

The evidence standard your team should require#

Use a simple rule: no material claim should influence your buying decision until it is graded. If a provider compares itself with Global banks, treat that as unverified until you can inspect the method, scope, and evidence.

Treasury's November 2022 report explicitly separates evidence of consumer benefits from "Outstanding Gaps" (page 91), so your process should do the same.

| Claim grade | What it means | What to do |

|---|---|---|

| Verified data | Primary evidence you can inspect | Allow it into decision criteria |

| Partial evidence | Some support, but important context is missing | Record missing items and keep it conditional |

| Unverified statement | Marketing, reposts, or unsupported comparisons | Keep it out of the decision case until validated |

Keep a short source log for internal decisions: what came from vendor docs, what came from external commentary, including BCG, and what came from social posts. For each claim, record source, grade, outstanding gaps, and owner for follow-up.

Set a hard "decision can proceed" checkpoint only when your top two options both have complete answers on costs, controls, and compliance. If one option still has outstanding gaps, treat that as decision-relevant risk. That aligns with the April 28, 2020 CRS framing: fintech can improve efficiency, but it can also create harmful outcomes.

Related: The 'Compliance Moat': Why RegTech is a Defensible Strategy.

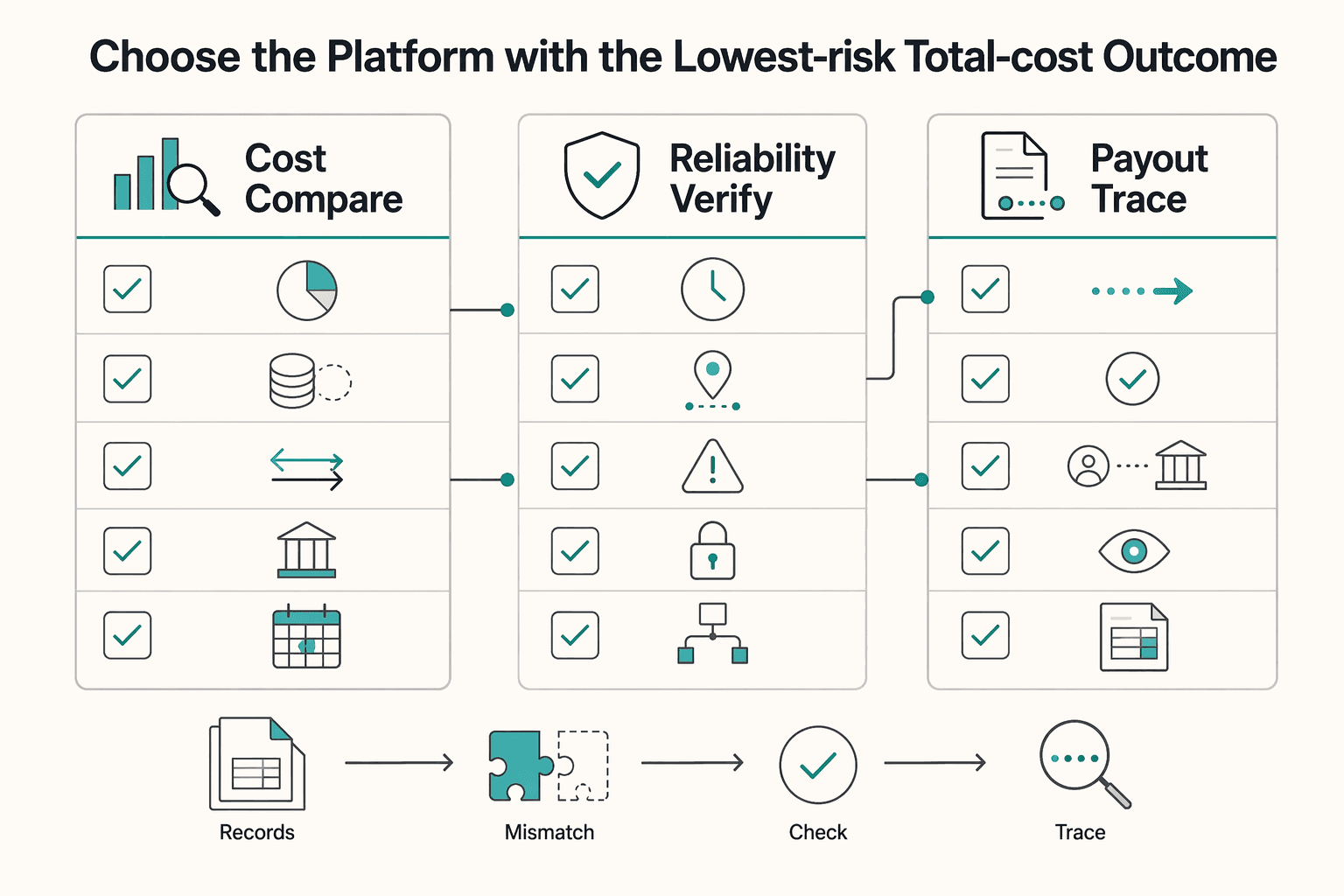

Choose the platform with the lowest-risk total-cost outcome#

Make your final choice on lowest verified total-cost risk, not on fee headlines alone. The better option is the one with the lowest real landed cost and the fewest operational surprises, not the cleanest pricing banner.

Before migrating real volume, run a short side-by-side pilot with the same corridor, amount, funding method, payout method, and day. Save the quote capture, executed transfer details, and final settlement record for each provider. If one option looks cheaper at quote stage but creates payout friction, unclear status visibility, or messy reconciliation, treat that as decision-relevant.

Use three checkpoints:

- Cost: compare the full landed outcome, including applied rate, transfer or payout charges, and any return or correction costs.

- Reliability: verify whether the payout lifecycle is visible end to end, including failed transfers, reversals, and delays.

- Compliance and controls: confirm who owns key checks, what documentation is required, and what audit trail you receive after settlement.

A practical red flag: if a provider cannot share an evidence pack before signature, assume that gap will surface later. Ask for a sample failed-transfer path, reversal handling, status history, and reconciliation export.

Do not assume one winner across all routes. Coverage, payout behavior, and rules vary by country and program, so selection should follow corridor-specific testing. That fits the broader market signal: BCG's March 13, 2026 view ties durable fintech scale to interoperable digital infrastructure, trust, and predictable regulation, not pricing alone.

Keep the final step light but disciplined: ask each provider for evidence packs, operational controls, and reconciliation depth before signing. If you get corridor-level proof and clear auditability, you have decision-grade evidence; if you mostly get savings claims or vendor-authored benchmarks, keep testing.

Frequently Asked Questions

Is zero FX fee actually cheaper in real cross-border payments?

Not necessarily. A provider can advertise no explicit FX fee and still be more expensive once you account for the rate used and other transfer costs. Wise, for example, says it uses the mid-market rate, but it also says its fee varies by currency, starts from 0.57% in some cases, and is not universally zero.

What should I compare besides FX fees before choosing a provider?

Compare the full money path, not just the headline line item: exchange-rate treatment, transfer fees tied to route and payment method, and what actually lands at payout. A practical verification step is to run the same corridor and amount through each provider on the same day, then save the quote capture and the final settlement record. If a vendor cannot show clear exception handling and audit evidence, treat that as decision-relevant.

Why is competing only on FX fees risky for fintech buyers?

Because price compression does not remove operating risk. The U.S. Treasury competition report from November 2022 explicitly calls out “Reliability and fraud” and “Data privacy and security” as risk areas, so a cheaper quote does not automatically mean a lower-risk setup. A common mistake is choosing on price first and validating risk controls too late.

How can a small team choose safely between Wise, Revolut, and Airwallex?

Use a narrow pilot, not a brand decision. Ask each provider for the same corridor, amount, payment method, payout method, and support evidence, then compare what you can verify: total landed cost, settlement predictability, and controls. If your monthly volume may cross Wise’s 25,000 USD threshold, check whether discounting changes the economics, but do not assume that one threshold makes it the best option everywhere.

What is still unknown in current public claims about hidden FX fees?

Public claims can still miss method, scope, or corridor-level detail. The Treasury report itself has an “Outstanding Gaps” section, which is a useful reminder that unresolved evidence is part of the picture. Be skeptical of savings claims that do not show customer type, route, payout method, capture date, and whether the result reflects quoted price or final settlement.

When should I prioritize infrastructure and controls over the lowest quoted rate?

Do that as soon as payments become recurring, material, or hard to unwind. If reliability, fraud, privacy, security, or reconciliation issues would create real finance ops pain, stronger controls can be worth more than a slightly lower quoted rate. A good rule is simple: if you need dependable audit trails and clean month-end close, choose the option with clearer operational evidence over the cheapest marketing claim.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bis.org/publ/work1103.pdftrusted

- congress.gov/crs_external_products/R/PDF/R46332/R46332.1.pdftrusted

- congress.gov/crs_external_products/R/PDF/R46332/R46332.3.pdftrusted

- dash.harvard.edu/bitstreams/f0fc918c-e124-4ace-aa7d-020fc1294...trusted

- elibrary.imf.org/view/journals/063/2025/008/article-A001-en.xmltrusted

- farmingdale.edu/courses/index.shtmltrusted

- gsb.stanford.edu/insights/future-debt-can-fintech-fill-gaptrusted

- home.treasury.gov/system/files/136/Assessing-the-Impact-of-New...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

GDPR Compliance Checklist for Freelancers Working With EU Clients

Start by separating the decisions you are actually making. For a workable **GDPR setup**, run three distinct tracks and record each one in writing before the first invoice goes out: VAT treatment, GDPR scope and role, and daily privacy operations.

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

Why RegTech Becomes a Defensible Compliance Moat

RegTech becomes a moat only when it makes compliance decisions easier to execute and defend. The buying decision comes down to one question: does this investment create durable capacity, or does it add overhead your team must carry?