Quick Answer

An all-in-one ETF portfolio is a good fit if you want broad diversification and less day to day maintenance, but it is a weaker fit if you need custom weights, detailed tax positioning, or a specific fund domicile. One fund can package stocks and bonds and handle rebalancing, but you still need to verify costs, account wrapper, domicile, and currency fit before buying.

The Portfolio Automation System: Reimagining the All-in-One ETF for Global Professionals#

If your priority is broad diversification with less day-to-day portfolio admin, an all-in-one ETF portfolio can be a practical default. It is a weaker fit when you need custom asset weights, detailed tax positioning, or a specific fund domicile for your filing situation.

What you are actually delegating#

An asset allocation ETF is a single fund that packages a diversified mix of stocks and bonds. In practice, that single holding is often built from several underlying ETFs across regions and asset classes, so one trade can give you broad exposure.

You are also delegating rebalancing. In a manual multi-fund setup, allocations drift as markets move, and you need to place trades to get back to target. In an all-in-one structure, the manager monitors those allocations and rebalances as needed.

You are also delegating risk alignment, but only within preset choices. Some lineups offer fixed profiles across a range, such as 20% stocks / 80% bonds through 100% stocks / 0% bonds. You choose the profile, and the fund maintains it. The tradeoff is less customization inside that profile.

| Dimension | Manual multi-fund portfolio | All-in-one ETF portfolio |

|---|---|---|

| Setup workload | Higher: you select and buy each fund. | Lower: one product can package the portfolio. |

| Ongoing maintenance | Higher: you monitor drift and rebalance yourself. | Lower: manager monitors and rebalances toward target weights. |

| Customization | Higher: you can set your own weights and tilts. | Lower: stock/bond mixes are typically preset. |

| Operational error risk | Can be higher because there are more moving parts and trade decisions. | Can be lower for maintenance, but you still need solid upfront product and tax checks. |

The tradeoffs that matter#

The main benefit is simplicity. You cut down the number of moving parts, recurring decisions, and maintenance trades.

The price of that simplicity is flexibility. If your plan needs separate income sleeves, specific tilts, or account-specific allocation design, a one-fund core can feel restrictive and may need add-on funds.

Costs still deserve a direct check. Start with the prospectus fee table and confirm the expense ratio. Then look at what is not included there, such as brokerage commissions or other trading costs. Example figures differ by fund, so use the current prospectus for the exact product you are considering.

A quick selection filter#

Before you buy, run five checks. This is where a simple product either stays simple or turns into a tax and reporting headache later.

| Check | What to confirm | Article note |

|---|---|---|

| Fund mandate | Whether the mandate is conservative, balanced, or growth-oriented | Confirm whether the stock/bond split is fixed |

| Underlying exposure design | Which ETFs are inside and what geographic and asset-class exposures you are actually getting | Review holdings or methodology |

| Rebalancing approach | How the issuer describes maintaining target weights | Do not assume every fund family uses the same cadence |

| Cost transparency | The current prospectus fee table | Account for any separate trading costs at your broker |

| Domicile fit | For U.S. persons, whether non-U.S. fund exposure is a tax checkpoint | PFIC-related Form 8621 filing obligations may apply |

- Fund mandate: Confirm whether the mandate is conservative, balanced, or growth-oriented, and whether the stock/bond split is fixed.

- Underlying exposure design: Review holdings or methodology to see which ETFs are inside and what geographic and asset-class exposures you are actually getting.

- Rebalancing approach: Verify how the issuer describes maintaining target weights. Do not assume every fund family uses the same cadence.

- Cost transparency: Read the current prospectus fee table, then account for any separate trading costs at your broker.

- Domicile fit: For U.S. persons, treat non-U.S. fund exposure as a tax checkpoint, not a minor detail, because PFIC-related Form 8621 filing obligations may apply.

The CEO's Framework: Automating Your "Core" to Unleash Your "Satellite"#

A Core-Satellite split is mostly about attention control. Keep most of your portfolio, around 80-90%, in a broad, maintenance-light core. Limit satellites to a smaller sleeve, around 10-20%, for higher-conviction ideas you can actively defend.

Sequence matters. Build the core first, then add satellites. Reversing that order makes it easier for the speculative sleeve to grow beyond your intended allocation.

| Dimension | Core | Satellite |

|---|---|---|

| Purpose | Broad market exposure and portfolio foundation | Targeted, high-conviction ideas outside the core |

| Expected effort | Lower ongoing effort after setup | Higher effort before entry and while holding |

| Risk role | Portfolio foundation | Deliberate, limited additional risk |

| Allocation guide | Around 80-90% of the portfolio | Around 10-20% of the portfolio |

| Common mistakes | Constant tinkering, relying on labels instead of implementation details | Concentration creep, thesis drift, adding positions without a clear risk budget |

What belongs in your core#

Your core should do the routine work with minimal intervention: broad exposure, consistent structure, and fewer recurring decisions. An all-in-one ETF portfolio can do that job, but the label matters less than the function.

Do not use "active" or "passive" as a shortcut for quality. Neither label is automatically better, and that binary framing can hide meaningful implementation differences, so verify what the fund actually holds and how it is built.

What earns a place in your satellite#

A satellite position should earn its way in. Write down why you think you have an edge, what would prove you wrong, and how long the idea needs. Possible upside is not guaranteed, and this sleeve is usually more speculative and more volatile. Keep a short evidence pack for each satellite position. If you will not write it down, it probably does not belong in your satellite sleeve.

| Evidence item | Details |

|---|---|

| Thesis | thesis in 3-5 lines |

| Informational or analytical edge | why you believe you have an informational or analytical edge |

| Holding period | expected holding period |

| Disconfirming facts or exit conditions | disconfirming facts or exit conditions |

| Maximum capital | maximum capital you will commit |

At minimum, note:

- thesis in 3-5 lines

- why you believe you have an informational or analytical edge

- expected holding period

- disconfirming facts or exit conditions

- maximum capital you will commit

Attention rules and guardrails#

Your core should be boring to run. Automate repetitive actions, review on a schedule, and keep satellite decisions manual and thesis-driven. Do not use satellites to recreate exposures your core already gives you.

Set concentration guardrails before you add risk: a cap per satellite position and a cap for the full satellite sleeve. If any position, theme, or sleeve weight moves beyond your preset limit, pause and review before adding more. Apply the same pause rule if your thesis changes or you cannot explain in one sentence why you still own the position.

For a step-by-step walkthrough, see A Guide to Index Fund Investing for Freelancers.

The Global Professional's Risk Matrix: A Deep Dive into Real-World Threats#

Once your core is set, implementation can be a bigger risk than market noise: right fund, wrong account wrapper, wrong domicile, or wrong currency exposure for your real liabilities. If you want your portfolio to stay low effort, audit those three areas before you buy and on a fixed review cycle.

Start with account wrapper, not fund marketing#

Convenience does not replace asset location. A single asset allocation ETF can bundle stocks and bonds and rebalance to target weights. You still need to separate taxable, tax-deferred, and tax-exempt wrappers before you decide what belongs where.

Use this matrix as a decision aid, not a universal template. Tax drag can vary by geography, asset class, structure, domicile, and account wrapper.

| Account wrapper | Fund profile fit | Tax drag risk to check | Operational notes |

|---|---|---|---|

| Taxable brokerage | Can fit some portfolios, depending on local tax rules | Ongoing taxation of distributions, foreign withholding, and domicile-specific reporting | Verify treatment of distributions and sales in your filing jurisdiction. Confirm whether domicile changes reporting duties. |

| Tax-deferred account | Can be useful where current income tax drag is a concern, if local rules support it | Future taxation at withdrawal may still matter; withholding outcomes may differ by wrapper and domicile | Confirm local rules for contributions, withdrawals, treaty treatment, and whether the wrapper is recognized where you file. |

| Tax-exempt account | Can fit some portfolios if the wrapper actually shields gains and income | Do not assume foreign withholding disappears just because the wrapper is locally tax-exempt | Verify eligibility, cross-border recognition, and whether withholding is recoverable or permanently lost. |

Quick control: label every holding by account wrapper first and fund domicile second. If you cannot do that from one statement view, you have an avoidable operational gap.

Domicile is not a detail if you are a U.S. person#

ETF domicile can change tax treatment. For U.S. persons, that can turn into a PFIC analysis. Under 26 USC 1297, a foreign corporation can meet PFIC tests if 75 percent or more of gross income is passive income. It can also meet them if at least 50 percent of assets produce or are held to produce passive income.

That does not mean every foreign-domiciled ETF is automatically a PFIC for every investor. It does mean you should not guess if you are treated as a U.S. person for tax purposes and you hold, or plan to hold, non-U.S. funds.

The practical move is simple: confirm taxpayer status, wrapper, and domicile before you trade. If this might apply, run this checklist:

- Are you a U.S. person for tax purposes?

- Is the fund in a taxable account, or is wrapper treatment unclear?

- Is the ETF non-U.S.-domiciled?

- If any answer is yes or unclear, ask a qualified cross-border tax advisor to review PFIC exposure and Form 8621 filing triggers before you add or keep the position.

Form 8621 instructions (revised 12/2025) state that a U.S. person who is a direct or indirect PFIC shareholder generally must file, with a separate form for each PFIC, and they list five filing circumstances.

Pick currency exposure based on liabilities, not convenience#

Currency exposure is not a side issue. If your investment currency and base currency differ, exchange-rate moves become part of your return. With unhedged exposure, exchange-rate moves can help or hurt results. Hedging aims to reduce that currency effect, but hedged share classes can lag unhedged versions in some periods.

Before you choose your core fund, map four items:

- Your current spending currency

- Your major future liability currency

- The base currency exposure in the fund

- How rebalancing decisions would change if exchange rates move sharply

Working rule: align the core primarily to the currency of long-term liabilities, not a temporary location or payroll currency. If your liabilities are split across currencies, document that explicitly before you choose hedged versus unhedged exposure.

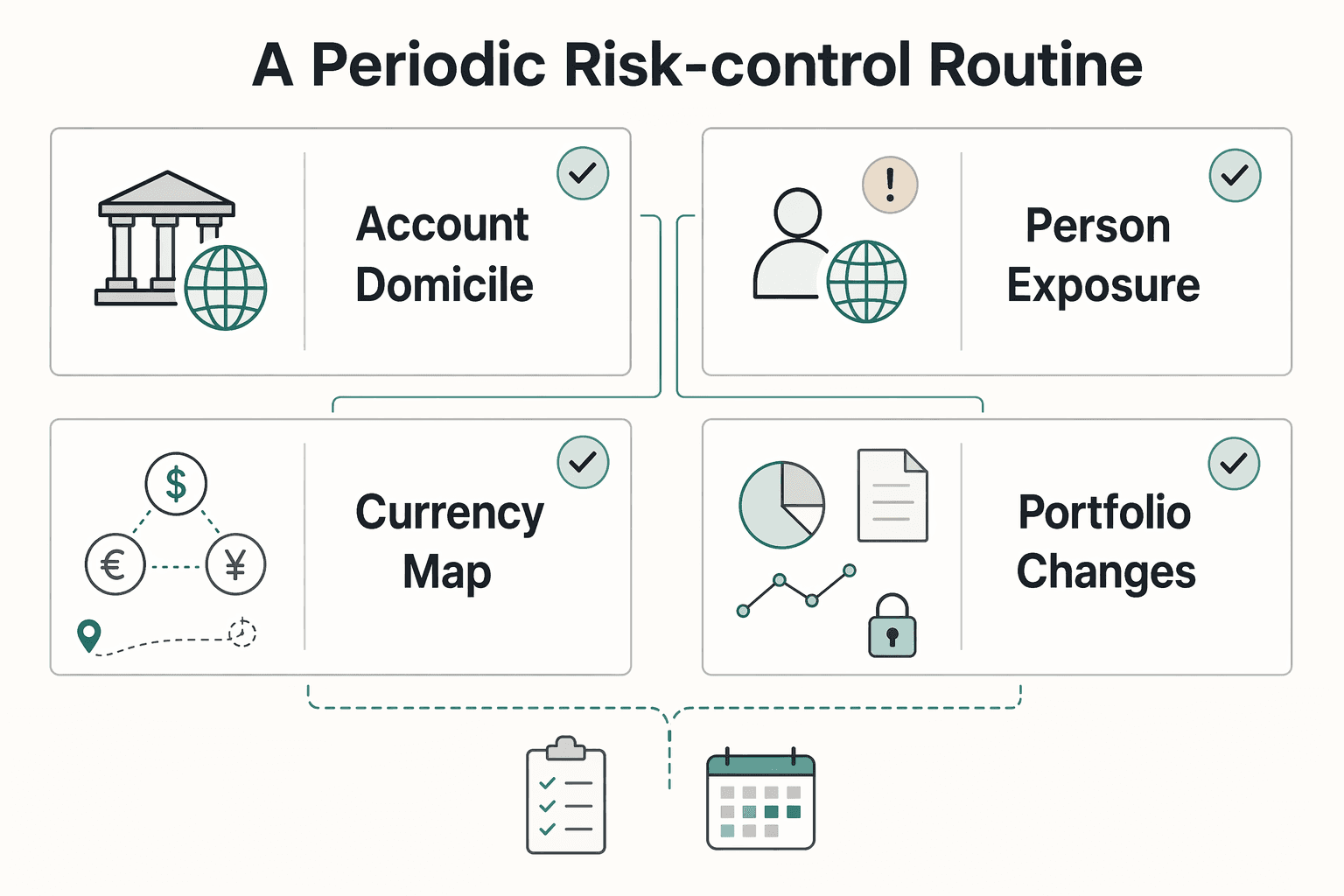

A periodic risk-control routine#

The review process should stay short enough that you will actually do it. Keep it repeatable:

| Review task | What to update or confirm |

|---|---|

| Account and domicile inventory | Update a one-page inventory of each account wrapper, each ETF domicile, and where each fund sits (taxable, tax-deferred, tax-exempt) |

| U.S.-person exposure | Recheck any U.S.-person exposure to non-U.S.-domiciled funds and confirm whether Form 8621 or related filings may apply |

| Currency map | Refresh spending currency, major liability currencies, and the currency exposure of your core fund |

| Portfolio changes | Rebalance or replace only after checking tax and reporting consequences |

On a quarterly or semiannual review, the sequence is:

- update a one-page inventory of each account wrapper, each ETF domicile, and where each fund sits (taxable, tax-deferred, tax-exempt)

- recheck any U.S.-person exposure to non-U.S.-domiciled funds and confirm whether Form 8621 or related filings may apply; verify the current trigger, exception, or compliance threshold for your exact case

- refresh your currency map: spending currency, major liability currencies, and the currency exposure of your core fund

- rebalance or replace only after checking tax and reporting consequences; clean allocation math is not worth creating a filing problem

Before you lock your core ETF setup, validate your residency assumptions so your tax and account choices stay aligned. Track your status with the Tax Residency Tracker.

Conclusion: A Tool for Empowerment, Not Abdication#

An all-in-one ETF portfolio is a tool for reducing routine work, not a substitute for judgment. It can combine diversified stock-and-bond exposure in one fund and handle internal rebalancing, but you still own the fit decision.

It can be a strong fit when your target mix is clear, the fund's target mix matches it, and your total holdings across accounts still reflect your intended allocation. It is a weaker fit when you need more customization inside the fund. It is also weaker when other accounts materially change your real allocation, or when jurisdiction-specific rules make a one-fund setup less practical. Diversification also does not remove currency risk, so exchange-rate moves can still change results.

Before you buy or add, set a review routine:

- Confirm your current risk tolerance.

- Confirm account and tax considerations across each account you use.

- Confirm the level of currency exposure you are willing to accept.

- Confirm who handles rebalancing and how you will review ongoing fit.

If the fund rebalances internally, your review is mostly about continued fit, not constant trading. A review every six to 12 months can be a useful prompt, but not a universal rule. Taxable-account changes can still have tax implications. Verify implementation details for your jurisdiction before you commit, especially in cross-border setups where legal protections and rules can differ. If you still need to choose the allocation framework first, start with A Guide to Asset Allocation for Your Investment Portfolio. Related: Tax Implications for an Australian Resident Owning a US LLC.

If you want a practical next-step checklist after choosing your core portfolio, use Gruv's finance tools to turn decisions into repeatable workflows.

Frequently Asked Questions

Are all-in-one ETFs tax-efficient for U.S. expats?

Sometimes. An all-in-one ETF can simplify investing, but PFIC and Form 8621 treatment depends on your facts, so confirm your filing position with a qualified tax advisor. Keep state rules separate from fund choice, and if California is relevant, verify your taxpayer status, residency period, account wrapper, and fund domicile before you file.

How should I use an all-in-one ETF in a taxable brokerage account?

Use taxable only after you confirm the setup fits your tax and reporting reality. A single asset allocation ETF can work in taxable, but convenience does not replace wrapper and domicile checks. If California applies, keep source income and residency mechanics separate from portfolio design, then review your year-end tax documents with your advisor before you lock in placement.

All-in-one ETF vs. building your own portfolio: which is better for a high earner?

There is no universal winner for high earners. A one-fund core can reduce moving parts, while a DIY setup can offer more control. Define the exact control you need before you add complexity.

What is the right "core" portfolio for a busy professional?

The right core is one you can explain clearly, fund consistently, and keep through stress. Match your risk mix, account wrapper, and currency exposure to your real plan instead of choosing by brand alone. Write down your target mix, liability currency, and review cadence before you compare funds.

Can an all-in-one ETF be my only investment?

Yes, it can be your only investment if the fund's allocation and reporting fit your plan. It stops being a clean one-fund solution when wrapper needs, domicile and reporting risk, or multi-currency liabilities call for a split approach. Test the setup against your account access, tax status, and reporting obligations before you commit.

How do I choose between Vanguard, iShares, and others?

Start with fit, not brand. Compare domicile fit, allocation style, cost structure, account compatibility, and operational simplicity for your situation. Make one checklist with ticker, wrapper, and domicile before you place any order.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ftb.ca.gov/file/personal/residency-status/part-year-and...trusted

- ftb.ca.gov/file/personal/residency-status/index.htmltrusted

- investor.gov/introduction-investing/getting-started/asset...trusted

- investor.gov/introduction-investing/general-resources/new...trusted

- irs.gov/instructions/i8621trusted

- irs.gov/forms-pubs/about-form-8621trusted

- uscode.house.gov/view.xhtmltrusted

- uscode.house.gov/quicksearch/get.plxtrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Japan Digital Nomad Visa 2026: Six-Month Planning Runbook

Treat this as your operating model: identify the right mission first, commit to one route, and keep dated records before you make irreversible plans. That is what keeps the rest of your timeline, paperwork, and decisions coherent.

Tax Implications for an Australian Resident Owning a US LLC

There is no one-size-fits-all shortcut for US LLC tax decisions across Australia and the United States. Setting up a US Limited Liability Company (LLC) is one step; getting the tax treatment right in both systems is where risk starts. If you are handling **australian owning us llc tax** decisions, treat this as a classification and documentation problem first, not a shortcut hunt. If you run a business of one, your job is to pick the defensible path and keep the paperwork tight.

Asset Allocation for Freelancers With Uneven Income

Start here: keep money you may need in the near term separate, and invest only money that can stay invested. Your portfolio should serve long-term goals, not compete with short-term needs. That is the job of [asset allocation](https://www.investor.gov/additional-resources/general-resources/publications-research/info-sheets/beginners-guide-asset): set target percentages across major asset classes like stocks, bonds, and cash, then maintain that mix with rebalancing from time to time instead of reacting to headlines.