Quick Answer

Yes - choose a c-corp for freelancers only when you have a real ownership reason, such as adding shareholders or using stock. For a solo service business with straightforward income, the extra governance work and possible double taxation are often too heavy. Compare sole prop, LLC, and an S-corp path first, then make the filing call with a qualified tax advisor.

Start Here What a C-corp Decision Really Changes#

Entity choice is not just paperwork. It changes how the business is taxed, how ownership can be structured, and how much compliance work you take on. Use this article to make a practical call: keep your current setup, consider an LLC or S-corp path, or move to a C-corp only if the tradeoffs fit where you are headed.

The core comparison is simple: how the business is taxed, who can own it, and how much administrative work it takes to stay compliant. In the comparison used here, an LLC is pass-through by default and can elect S-corp or C-corp tax status. An S-corp is pass-through and avoids corporate-level tax. A C-corp is associated with double taxation at the corporate and shareholder levels.

Ownership rules can be a deciding factor. In this same comparison, a C-corp has no restrictions on the number or type of owners, while an S-corp is limited to 100 shareholders who must be U.S. citizens or residents. If you expect broader ownership or a structure built for scale and venture-capital fundraising, that points one way. If you expect to stay a solo operator, weigh that against the compliance workload before deciding. Before you decide, put these on one page:

- Your current setup

- Where you want the business in one, five, and even ten years

- Whether you expect additional owners

- How much ongoing admin work you are willing to handle

This article follows that same sequence: decision logic first, compliance checkpoints next, then what to confirm with a tax advisor. The baseline comparison is U.S.-oriented, especially the S-corp ownership rule, so verify location-specific details for your situation.

Define the Core Terms Before You Compare Anything#

Start with the labels. People often mix entity type and tax election, and that leads to bad comparisons. The table below keeps the terms straight before you compare options.

| Term | Working meaning here | Why it matters |

|---|---|---|

| C corporation (C-corp) | One named corporate structure option | Treat it as a specific structure choice, not a generic sign that a business is "more official." |

| Sole proprietorship | The owner and business are legally the same | This can mean direct personal liability for business debts. |

| Partnership | One of the recognized ownership structure types | It belongs in the comparison set, even if it is not your likely path. |

| Limited liability company (LLC) | One listed ownership structure option for new companies | It is often compared alongside corporation options. |

| S-corp election | A term frequently discussed next to entity choice | This is where people often mix up terms. |

A common terminology trap sounds like, "Is my LLC an S or C Corp?" If your notes blur those terms, stop there. Ask a qualified tax professional to confirm what you are actually comparing.

Why Freelancers Keep Looking at C-corps#

Freelancers often start looking at a C-corp when something concrete has changed, not just because they want a more polished label. Common triggers include growth plans, possible future shareholders, or eventual stock use.

| Reason or trigger | How it is framed |

|---|---|

| Growth plans | Often comes up when growth plans are part of what changed. |

| Possible future shareholders | Often comes up when possible future shareholders are part of what changed. |

| Eventual stock use | Often comes up when eventual stock use is part of what changed. |

| Liability concerns | Can be a valid prompt, but only if you are ready for the added rules, filings, tax implications, and ongoing overhead. |

| Legitimacy goals | Can be a valid prompt, but only if you are ready for the added rules, filings, tax implications, and ongoing overhead. |

| Tax savings rumor | A weak reason on its own; the support here does not justify guaranteed tax savings. |

The stronger reasons are structural. A C-corp is often framed as a growth-oriented option, and it can support shareholders and stock. That matters if ownership may expand beyond a solo practice. Liability concerns and legitimacy goals can also be valid prompts, but only if you are ready for the added rules, filings, tax implications, and ongoing overhead.

A weak reason is, "I heard it saves taxes." The support here does not justify guaranteed tax savings, and freelancer-focused advice commonly warns about complexity, expense, and double taxation. Use this quick screen before you go further:

- If you expect to add shareholders or use stock, the C-corp question is real.

- If you mainly want to look more established or feel safer, weigh that against the ongoing admin burden.

- If your reason is mostly tax rumor, pause and get professional legal review.

This is where search advice often falls short. It can jump straight to blanket "avoid it" messaging without giving you a test you can actually use. What matters is whether your ownership plans and day-to-day operations really call for a corporate structure.

Practical checkpoint: write your trigger in plain language before you choose. "Need room for future shareholders" is concrete. "Seems more professional" usually is not enough on its own.

Where a C-corp Is Usually Too Heavy for a Solo Freelancer#

If your income is straightforward, you work alone, and you do not expect shareholders or stock soon, a C-corp is usually more structure than you need. In that setup, the extra formality often creates more admin work and more room for expensive mistakes than a simpler entity path.

A C corporation is created by filing articles of incorporation, and it is legally separate from you. That separation can be useful, but it also brings formal governance work: directors, officers, and bylaws. For a one-owner business with simple ownership, that is often a heavy solution for a simple operating model.

Why the overhead gets real fast#

The real issue is not formation. It is the ongoing governance and recordkeeping load. If your current model is still "I provide services, get paid, and pay myself," a corporate structure can outpace what the business actually needs. Use a quick reality check:

- Can you clearly explain your ownership plan?

- Do you have a near-term reason to issue stock or add equity holders?

- Are you prepared to maintain core corporate records and governance documents?

If those answers are vague, the structure is probably ahead of the business. The common failure mode is not that a corporation is inherently wrong. It is choosing the wrong entity too early and ending up with constraints and costs you did not need.

Tax friction is where the sales pitch often falls apart#

Tax is where a lot of C-corp talk gets oversimplified. A C-corp can face tax at the corporate level, and shareholders can be taxed again on dividends, so double taxation is a real planning issue.

If you have not mapped how money will move from the company to you, you do not have a tax strategy yet. You have an assumption. Keep the labels separate too. C-corp status is different from an S-corp tax election, which is tied to IRS Form 2553.

Guidance in this area often notes that many small business owners choose S-corp status instead of C-corp. That is not an automatic answer for you. It is a reminder that a C-corp should be treated as a specific-fit choice, not a default upgrade.

Red flags that usually mean stop and re-check#

If any of these are driving your decision, pause before you file:

- You heard online that a corporation "saves taxes" but have no side-by-side model.

- You are relying on one anecdote from someone in a different business context.

- You do not expect shareholders, equity grants, or stock use soon.

- You cannot explain how you will pay yourself or whether profits will stay in the company.

If that sounds like your situation, keep things simpler for now and revisit the question when your ownership or capital plan makes it necessary.

We covered this in detail in How to Structure an S-Corp for a Husband and Wife Partnership.

When a C-corp Can Be Reasonable for a Freelancer#

These IRS excerpts do not tell you when a C-corp is generally better or worse for freelancers. They do give you concrete checkpoints to test self-employment-tax assumptions before you treat a C-corp rationale as settled.

A practical first pass is to document your current tax assumptions and verify them against IRS definitions, thresholds, and Schedule SE mechanics.

The business case should be specific#

Before you move forward, make sure you can clearly answer:

- Which parts of your decision rely on self-employment-tax assumptions

- Which Schedule SE (Form 1040) inputs you are using right now

- Which assumptions are outside these IRS excerpts and still need separate review

If you cannot explain that in plain language, pause before treating the tax case as complete.

Test tax assumptions before filing anything#

For IRS purposes, self-employment tax refers to Social Security and Medicare taxes only. If you are self-employed, such as a sole proprietor or independent contractor, you calculate self-employment tax using Schedule SE (Form 1040). IRS guidance says you usually must pay it when net earnings from self-employment are $400 or more. Key checkpoints to verify in your model:

| IRS checkpoint | Figure or rule | Context |

|---|---|---|

| Self-employment tax rate | 15.3% | Refers to Social Security and Medicare taxes only. |

| Social Security portion | 12.4% | One component of the self-employment tax rate. |

| Medicare portion | 2.9% | One component of the self-employment tax rate. |

| General base | 92.35% of net earnings from self-employment | Listed as the general base to verify in the model. |

| Usual payment threshold | $400 or more net earnings from self-employment | IRS guidance says you usually must pay self-employment tax at this level. |

| 2024 Social Security maximum | First $168,600 of combined wages, tips, and net earnings | Subject to the Social Security portion for 2024. |

In short, verify the 15.3% rate, the 12.4% and 2.9% split, the 92.35% base, and the 2024 Social Security limit on the first $168,600 of combined wages, tips, and net earnings.

Also remember that the IRS notes its self-employment-tax list is not all-inclusive. Receiving Social Security benefits does not by itself remove potential self-employment-tax liability.

Practical decision rule#

Use these IRS checkpoints to validate your Schedule SE assumptions first. If your C-corp rationale still depends on claims not covered here, treat those claims as unconfirmed until you review them with a qualified tax advisor.

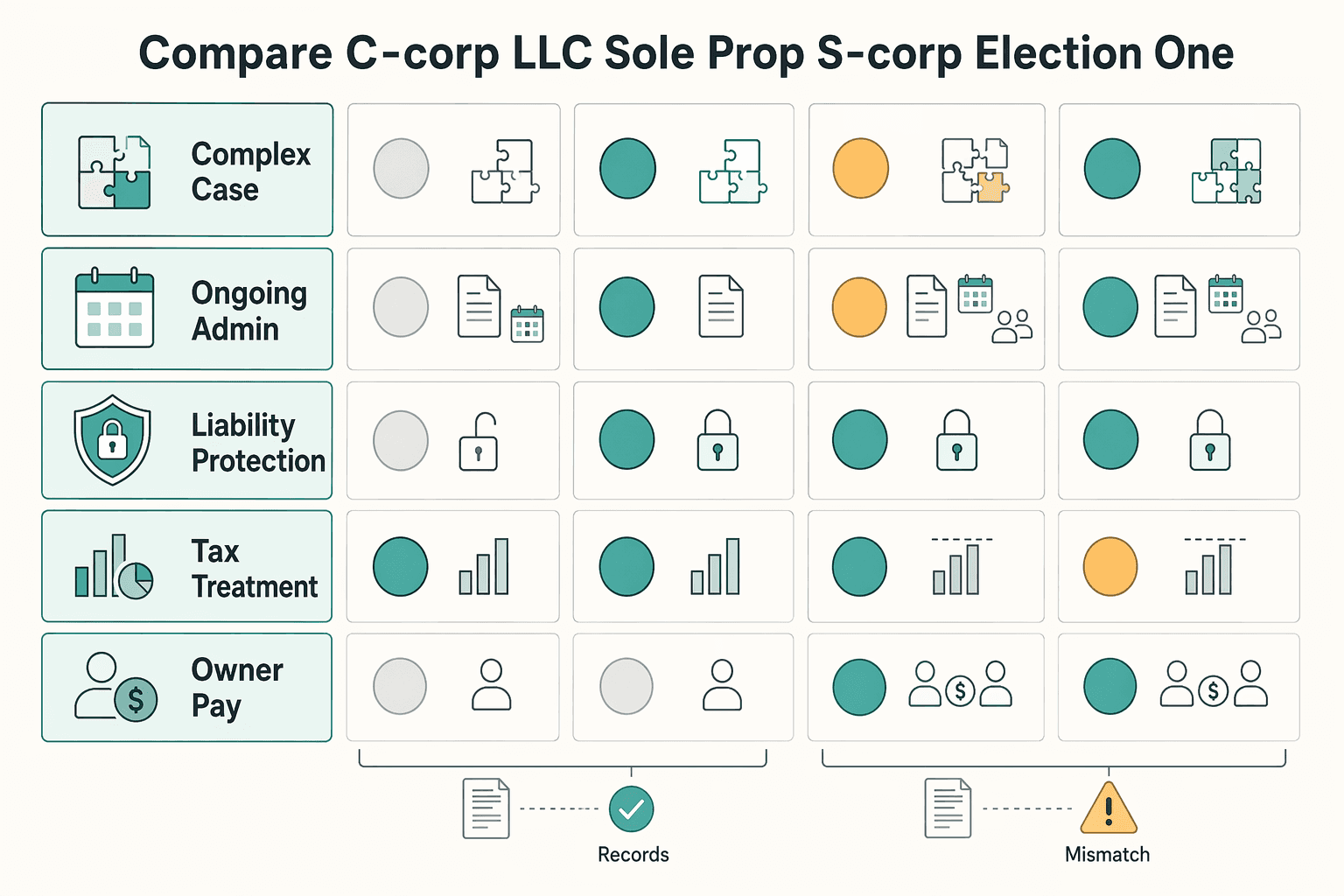

Compare C-corp LLC Sole Prop and S-corp Election on One Page#

If you want a clean decision, compare operating burden first and tax promises second. For most solo service businesses, start here: sole prop is often the default. An LLC adds liability protection without automatically changing taxes. An S-corp election adds payroll and compliance. A C-corp stays in scope only when the simpler options do not fit your actual plan.

| Criteria | Sole proprietorship | LLC | S-corp election | C corporation (C-corp) |

|---|---|---|---|---|

| Setup complexity | Common starting point for solo freelancers. | Relatively simple to set up and maintain, with flexible management. | Election path with IRS qualification rules. | More formal corporation path. Confirm formation, tax treatment, and operating requirements before treating it as the next step for a solo business. |

| Ongoing admin load | Can feel light, but owners can miss limitations by staying here too long. | Moderate. You still need clean records and entity upkeep. | Higher. Requires payroll setup and additional recordkeeping. | More formal corporate path in practice. Exact requirements need state and tax review. |

| Liability protection | Entity choice affects liability protection, so reassess this structure as contracts and risk grow. | Designed to provide liability protection. | Review liability context with the underlying entity and local rules. | Needs jurisdiction-specific legal review; avoid one-size-fits-all assumptions. |

| Tax treatment | Common baseline in freelancer comparisons. | An LLC by itself does not change how you are taxed. Most LLC owners are taxed as sole proprietors or partnerships, with self-employment tax on all profits. | Separate tax election often used for planning, but it adds compliance work. One firm says it generally recommends this when annual profit is more than $30,000; that is practitioner guidance, not an IRS threshold. | Needs separate review. Do not assume it behaves like an LLC or an S-corp election just because all three are business structures. |

| Owner-pay flexibility | Keep pay and records disciplined even in a simple setup. | By itself, an LLC does not change how you are taxed. | Less casual in practice because payroll setup is part of the package. | Needs separate review. Do not assume solo-owner draw habits carry over. |

| Best fit by business stage | Very early stage, validating demand, simple one-person service work. | Solo operator who wants liability protection without immediately taking on payroll complexity. | Business with steady profit and the discipline to run payroll and keep records on schedule. | Only when ownership, financing, or other corporate needs clearly justify extra formality. |

| Common failure mode | Staying here by default until a client, contract, or risk issue forces a change. | Assuming the LLC automatically lowers taxes. It does not. | Electing without being ready for Form 2553, payroll, W-2s, 1099 NECs, and qualification rules. | Choosing it because it sounds advanced or tax efficient, without a written reason simpler options cannot support your plan. |

Use the row for your current stage first, not your aspirational identity. If you are still one owner with straightforward freelance income, you should need a strong reason to move past sole prop or LLC.

If S-corp treatment is on your shortlist, verify the operating pieces before chasing savings. Confirm who files Form 2553, who runs payroll, how W-2 and 1099 NEC reporting is handled, and whether cross-border reporting such as FBAR is relevant.

Also keep entity choice separate from worker classification. In the FLSA context, an independent contractor is not an employee under the Act, but choosing an LLC, S-corp election, or corporation does not determine that status by itself.

If you want a deeper dive, read Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers.

If your decision depends on compensation assumptions, run a quick scenario with this W-2 vs 1099 calculator before your tax-advisor review.

Understand the Tax Mechanics Before You Commit#

If taxes are one of the main reasons you are considering this structure, stop and model the same business facts across every option first. Headline rates are not enough.

Where double taxation gets misunderstood#

Be careful with quick claims about "double taxation." In this section's IRS grounding, the detailed C-corp mechanics are not laid out. Broad tax slogans should be treated as unproven until your advisor models your actual facts.

The practical mistake is comparing different assumptions across structures. If owner cash needs, retained cash, or income assumptions change from one scenario to the next, the comparison will not tell you much.

Why self-employment tax keeps pulling freelancers into this question#

For many freelancers, this starts with self-employment tax. The IRS defines it as Social Security and Medicare taxes for people who work for themselves. The rate is 15.3%, split into 12.4% for Social Security and 2.9% for Medicare. The IRS also says:

- You usually must pay it if net earnings from self-employment are $400 or more.

- Generally, 92.35% of net earnings is subject to self-employment tax.

- Net earnings are gross business income minus ordinary and necessary business expenses.

- You calculate it on Schedule SE (Form 1040), and SSA uses Schedule SE information to determine Social Security benefits.

- The Social Security portion has an annual earnings limit, while Medicare applies to all net earnings. For 2024, the Social Security portion applies to the first $168,600 of combined wages, tips, and net earnings.

The tension is real. Concern about self-employment tax is reasonable, but compensation design and total cash flow assumptions can change the result. Without consistent assumptions, you are just comparing noise.

Bring this model to your tax advisor#

Bring one clean input set and use it across every entity scenario:

| Input | What to prepare | Why it matters |

|---|---|---|

| Entity assumptions | The exact options you are comparing | Prevents vague "incorporate" discussions |

| Income baseline | Last 12 months gross income and current YTD revenue | Net-earnings math starts from gross income |

| Expense baseline | Ordinary and necessary business expenses | Directly affects net earnings |

| Compensation assumptions | Owner cash needed monthly and annually | Cash-out assumptions can change outcomes |

| Distribution/retained cash assumptions | What stays in the business vs. what is taken out | Keeps scenarios comparable |

| Other wages and tips | Any wages, tips, or similar income | Affects Social Security portion exposure |

| Prior filing records | Most recent Form 1040 and Schedule SE (if filed) | Anchors modeling to filed facts |

The hard rule#

Do not choose a structure based on headline rates alone. Decide only after scenario modeling uses the same assumptions across each option: same income, same expenses, same owner cash needs, same outside wages, and same retained-cash plan.

One final IRS-grounded caution: self-employment tax guidance is not all-inclusive, and business-specific facts may change the result. That is why advisor review should be based on a full scenario model, not a one-line tax claim.

You might also find this useful: The S-Corp Election for LLCs: A Tax-Saving Strategy for High-Earning Freelancers.

Use Stage-based Decision Rules Instead of Generic Advice#

Use stage labels as a planning tool, not as proof that a C-corp is right. The available grounding for this section does not support hard, stage-based C-corp decision rules, so keep conclusions provisional until an advisor reviews your specific facts.

Early solo#

If you are still operating solo, keep the decision process simple. Document how the business runs today and compare options using one consistent set of assumptions. If your reason is mostly "it sounds better" or "more official," treat that as a signal to pause and sharpen the criteria.

Growing studio#

As the operation becomes more team-based, make ownership and control explicit before treating this as a structure choice. Write a short working memo covering current ownership, possible future ownership, and how cash is expected to move, then review it with your advisor.

Scaling firm with potential shareholders#

If you are actively discussing shareholders or broader equity planning, move from informal judgment to formal counsel review. At this stage, rely on documented facts and clear decision records, not generic tax narratives.

Baseline and revisit process#

If you are working from a United States baseline, confirm any cross-border entity or tax questions with local counsel before filing, since this section does not provide country-specific rules.

If you decide against a C-corp now, set a review date with your advisor so the decision can be revisited if your facts change.

If You Already Own a C-corp and Want to Route Freelance Income Through It#

Owning the entity is not enough by itself. Use this order: confirm the work fits the corporation's purpose, confirm the contract belongs in the corporation, keep records that support the arrangement, then review tax treatment with your tax advisor.

In one U.S.-focused legal response, this setup can be possible, but only with conditions.

For this decision, a C-corp is not just a different name on an invoice. When personal services, corporate activity, and owner decisions get mixed together, authority and documentation gaps are where issues often start.

Start with fit before tax assumptions#

Do not assume "invoice through the C-corp" automatically improves taxes. The grounding here does not support automatic tax savings. Ask first whether this freelance work is work the corporation is set up to perform. Check corporate documents, including articles or certificate of incorporation, bylaws, and any officer employment agreement, because they can limit freelance-service agreements.

Verification checkpoints#

Before routing new client income through the corporation, verify:

| Checkpoint | What to verify |

|---|---|

| Business purpose and authority | The services fit what the corporation is allowed and expected to do. |

| Contract alignment | The corporation is the service provider when the corporation is actually doing the work, and the terms do not conflict with your officer or shareholder obligations. |

| Related-party approval record | Where appropriate, board approval is in place before signing, with recusal if you are a board member. |

| Board resolution detail | Services, compensation, and intellectual property ownership rights are clearly recorded. |

| Documentation consistency | Records are consistent with the approved terms and corporate documents. |

Where people get into trouble#

The common failure mode is overconfidence: "I already have the C-corp, so I can route everything through it." That falls apart when purpose fit is unclear, approvals are weak, or ownership and compensation terms are not documented.

In a one-person corporation, these steps can feel low-stakes until someone else gets involved. That is exactly why it is better to clean up records early.

IRS Publication 17 can help with IRS interpretation context, but it also says it does not cover every situation and does not replace the law. Do not use it by itself to resolve governance or related-party agreement questions, and do not treat this as a substitute for legal advice.

A practical yes-no gate#

Keep the work in the existing corporation if purpose fit is clear, contract terms are clean, approval and IP ownership are documented, and records clearly match the approved arrangement. Then review tax treatment with your tax advisor.

Do not keep the work in the existing corporation if purpose fit is unclear, required approvals or documentation are missing, or the main reason is assumed tax savings. Pause and review whether the activity should stay separate or the structure itself should be reconsidered.

Set Up the First 90 Days Correctly if You Choose a C-corp#

In the first 90 days, operate with clear separation between business and personal activity from day one. The goal is simple: clean separation, clean records, and no backfilled paperwork later.

There is no supported federal rule in this grounding that requires one exact startup sequence. But this order can keep decisions and records aligned:

- Start with formation records. Keep incorporation documents and initial internal actions showing who can act for the corporation.

- Open banking in the corporation's name early. Route client receipts and business spending through corporate accounts, not personal accounts, where possible.

- Stand up bookkeeping immediately. Use a setup that ties each transaction to supporting records such as the contract, invoice, payment, and expense support.

- Set an owner-pay approach before paying yourself. If treatment is unclear, pause and get tax advice before moving funds.

- Set documentation standards early. Keep contracts, amendments, invoices, payment confirmations, owner-pay support, and approvals in one consistent file structure.

Your federal filing anchor is Form 1120, U.S. Corporation Income Tax Return. The 2025 IRS instructions describe Form 1120 as the return used to report income, gains, losses, deductions, and credits, and to figure income tax. Those instructions also cover payment operations, including electronic payments, direct deposit, and making a payment. They also note an increased penalty for failure to file.

Build the minimum evidence pack#

Keep a lean but complete record set that helps show the corporation is operating separately:

| Evidence item | What to keep | What it helps show |

|---|---|---|

| Board or internal actions (if used) | Written approvals for key decisions, especially owner-related decisions and major contracts | How corporate authority was documented for decisions |

| Owner-pay records | Pay authorization, payment records, and matching bookkeeping entries | Owner pay was intentional and recorded consistently |

| Contract files | Signed client agreements, amendments, invoices, and payment trail | The corporation, not you personally, provided services and earned income |

| Separation proof | Corporate bank statements, expense support, and records showing personal and business separation | Business and personal activity were kept separate in records |

Set monthly and quarterly controls early#

No federal source in this grounding sets a required monthly or quarterly checklist. A simple recurring control rhythm can still reduce cleanup later. Monthly, reconcile bank activity to the books. Confirm each client payment ties to contract and invoice records. Review owner-pay entries against support. Fix mixed personal and business charges while the details are still fresh.

Quarterly, run a readiness check: can your current file set support accurate Form 1120 preparation, and are unresolved classification or payment questions queued for your tax advisor? The IRS instructions also include a Who Must File section, including entities electing corporate taxation and LLC-related references. That is a useful reminder to keep legal form and tax treatment aligned in your records.

Related: The S-Corp Election vs. C-Corp: A Tax Comparison for US-Based Agencies.

Keep Compliance Boring and Predictable After Year One#

After year one, the goal is to run one repeatable review cycle so authority, records, and tax decisions stay aligned before they turn into cleanup work.

Use one repeatable review cycle#

Set a regular review point, then schedule a tax-planning check-in early enough for your tax advisor to affect the current year. The exact cadence depends on your facts, so confirm timing with your advisor. Keep it practical:

- Confirm records are complete and supportable: contract and invoice trail intact, with reimbursed expense items backed by receipts.

- Refresh authority documentation so it is clear who can approve payments, sign, and act for the corporation.

- Review owner pay and money movement with your tax advisor before changing approach.

- Check for new client, state, or industry compliance requirements that affect how you operate.

Know the triggers that justify a structure rethink#

Some changes justify a fresh review even if they do not automatically require a new structure. Possible triggers include ownership changes, stock-related decisions, or major changes in your delivery model.

Use a simple test: if ownership or revenue mechanics changed, re-check your documents, tax assumptions, and operating process. If stock is involved, get legal and tax input before signing. A practitioner checklist flags an 83(b) deadline as a risk point in some post-incorporation scenarios, so confirm whether it applies to your facts.

Set a records standard your future self can defend#

Use one clean file trail per client engagement. Keep the signed agreement, amendments, invoice trail, payment proof, and support for reimbursable expenses together.

If the client uses formal purchasing controls, keep those records too. In procurement-style workflows, a Purchase Order (PO) can be the key checkpoint before delivery starts, and a designated Contact Person may handle PO issuance, amendments, and termination. Also verify the corporation is the named contracting party. Contracts signed by the wrong entity are a known post-incorporation failure mode. For reimbursed expenses, keep the record standard tight: itemized support and receipts tied to the invoice file.

Escalate to the right person#

Route issues by authority so fixes happen faster:

- PO-level operations: in procurement-style workflows, use the designated Contact Person for PO issuance, PO amendments, and PO termination.

- Contract-level administration: use the Contracting Officer for contract administration and termination decisions; this role may not hold signing authority for contracts or amendments.

- Legal/tax/bookkeeping: use your advisors for entity, tax-position, and recordkeeping questions tied to your specific facts.

If you are unsure where to start, use this rule: rights and authority go to legal, tax outcomes go to your tax advisor, and book records go to bookkeeping.

Make the Decision Once Then Operate It Well#

Choose a C corporation (C-corp) only when your business model needs it, not because it sounds more advanced. Entity choice is an operating decision. It changes legal and tax treatment, and each option comes with its own rules, tax implications, filing requirements, and ongoing overhead.

Blanket advice in either direction can miss your context. You will see freelancer guidance that pushes against C-corps and growth guidance that emphasizes scaling or fundraising. Use both as context, then decide based on your current operation and likely next stage. If you do not need a scale-oriented corporate setup, a simpler structure may be the cleaner fit.

Take the next practical step: complete your side-by-side comparison, then run the same assumptions across each option before filing anything. If the decision depends on projected tax outcomes, validate those assumptions against your actual numbers. Bring a focused question list to your tax advisor:

- What is my current baseline structure right now?

- What changes in taxes and filings under each option based on my records?

- Where could reporting issues show up if I already have an entity?

- What compliance work will I need to maintain consistently?

The operating test matters as much as the tax test. If you stay a sole proprietor, you are responsible for tracking taxes and making estimated quarterly payments. If you move to a corporation, be realistic about whether you can keep up with the added compliance demands, which can be especially challenging for smaller businesses.

Also pressure-test the future without guessing. Look at your current needs and likely direction, and define real triggers for change, such as pursuing fundraising or taking on more complex growth plans. If you want a broader reset before deciding, review how to choose the right business structure for your freelance business.

The right corporate structure is the one you can explain, maintain, and defend without surprises.

After you choose your structure, map it to day-to-day money operations with Merchant of Record for freelancers.

Frequently Asked Questions

Is a C-corp good for freelancers or usually too much structure?

A C corporation is a different operating and tax posture from default freelance filing, so it should be a deliberate choice, not a default upgrade. If you are a sole proprietor or a single-member LLC with no election, your business activity is generally reported on Schedule C with your Form 1040. A C-corp is often discussed as a growth-oriented structure, so the decision should match your actual goals and facts.

Why do freelancers keep hearing about double taxation with C-corps?

Because C-corp treatment is not the same as Schedule C freelance reporting. The actual outcome is case-specific, so generic advice can miss important details. If someone presents it as an automatic tax win, take that as a sign to verify the numbers with a qualified tax professional.

How does an LLC compare with a C-corp for a solo service business?

By default, a single-member LLC is treated as a disregarded entity and files through Schedule C, similar to a sole proprietorship, unless you elect S-corp or C-corp status. A C-corp is a corporate structure typically positioned for growth. Compare based on reporting implications and goals, not labels alone.

Can I run freelance income through a C-corp I already own?

Possibly, but do not assume it automatically improves taxes. Keep reporting consistent and maintain clear transaction records to avoid duplicate income reporting. If records are unclear, fix that before routing new income through the entity.

What should I check before choosing a C-corp for my freelance business?

Start with your current filing baseline: sole proprietors and default single-member LLCs generally report through Schedule C attached to Form 1040. If net self-employment earnings are $400 or more, Schedule C filing is already in play. Also confirm the activity is operated for profit, because hobby treatment generally means expenses are not deductible.

What questions are still unknown until I review my case with a tax advisor?

The main unknowns are which entity or election fits your facts, how income should be reported, and where duplicate reporting risk may exist. Business-structure decisions depend on several variables, so review your case with a qualified tax professional.

When should I reconsider an S-corp election instead of staying with a C-corp?

Reconsider when you are comparing entity and tax-election options for your specific facts. Include S-corp status in that comparison alongside C-corp treatment, and confirm the decision with a qualified tax professional.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- congress.gov/bill/116th-congress/house-bill/6379/texttrusted

- dol.gov/sites/dolgov/files/WHD/flsa/IC_NPRM_092220.pdftrusted

- ecfr.gov/current/title-2/subtitle-A/chapter-II/part-200trusted

- gao.gov/assets/890/882024.pdftrusted

- grants.nih.gov/grants/policy/CFR-2008-title45-vol1-chapA-su...trusted

- irs.gov/businesses/small-businesses-self-employed/se...trusted

- irs.gov/taxtopics/tc554trusted

- pa.gov/content/dam/copapwp-pagov/en/dgs/documents/d...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

How to Choose the Right Business Structure for Your Freelance Business

Most freelancers end up in a business structure by default rather than by design, but that accidental choice shapes taxes, personal liability, and payment operations in ways that compound over time. This guide walks independent professionals through four entity types — Sole Proprietorship, Single-Member LLC, S-Corp election, and Corporation — covering the tax treatment, liability exposure, and operational overhead of each. Rather than prescribing a single best answer, it provides a trigger-based framework: start with the structure that fits today, then upgrade when specific signals — indemnification clauses, enterprise KYB requirements, a first hire, or material net profit — make the switch worthwhile. The result is a deliberate, revisable foundation that keeps records clean, reduces onboarding friction, and avoids the expensive mismatches that come from letting structure lag behind business growth.

The S-Corp Election vs. C-Corp: A Tax Comparison for US-Based Agencies

**Start with this rule: choose the structure you can qualify for, operate cleanly, and defend under review.**