Quick Answer

Yes, the feie physical presence test waiver may still protect your exclusion path after a forced departure, but only when your country and timing fit the applicable IRS guidance. You must support that your tax home was abroad, show you reasonably expected to meet the normal day requirement, and file Form 2555 with records that match your timeline. It does not add extra qualifying days, so the exclusion amount remains tied to actual presence. If coverage or dates are uncertain, evaluate alternatives before filing.

The 'Physical Presence Test' Waiver: A Crisis Playbook for US Expats#

If you had to leave a foreign country because of war, civil unrest, or similar adverse conditions, you may still be able to protect your FEIE claim. The physical presence waiver is narrow relief from the minimum time requirement. It is not automatic, and it does not guarantee the full exclusion.

Under the standard Physical Presence Test, you must be physically present in a foreign country or countries for 330 full days during any period of 12 consecutive months. A full day is 24 consecutive hours (midnight to midnight). The waiver can apply if that timeline was cut short by adverse conditions. You still need to show that you reasonably would have met the requirement without that disruption.

What it does and does not do#

| Waiver effect | What it means |

|---|---|

| Does | Can waive the minimum time requirement if the IRS has listed the country and applicable dates, your tax home was in that foreign country, and you were there on or before the waiver start date. |

| Does not | Does not convert days after departure into qualifying foreign-presence days, remove the tax-home requirement, or guarantee a full-year exclusion amount. |

FEIE still turns on actual qualifying days, and you still have to file a return reporting the income. If your qualifying period covers only part of the year, the exclusion cap is adjusted by those days. For tax year 2026, the maximum FEIE is $132,900 per person, but the waiver alone does not grant that full amount.

Before you build a claim, check the IRS country list and effective dates for the relevant year. As of March 2026, Rev. Proc. 2026-16 addresses taxpayers who failed section 911(d)(1) requirements for 2025 due to adverse conditions. Listed examples include Haiti: January 1, 2025, Ukraine: January 1, 2025, and Mali: October 30, 2025.

Do not assume every evacuation qualifies. If the country is not listed for that year, or you cannot support the reasonable-expectation standard, the claim may not hold. Work through this in order: Assess, Document, and Claim. If your timeline, tax home, or country status is complicated, get professional review before filing Form 2555. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Step 1: ASSESS - Do You Qualify for This Critical Exception?#

Start with a hard screen, not paperwork. If one of these gates fails, treat that as an early warning and adjust your plan before you spend time building a waiver claim.

Use a four-gate screen first#

- Confirm FEIE basics: foreign earned income + foreign tax home.

Start with the IRS baseline: to claim FEIE-related benefits, you must have foreign earned income, and your tax home must be in a foreign country. If your work base was not actually abroad, this path is weak.

- Confirm your country and dates against filing-year IRS waiver guidance.

Check your location and timeline against IRS waiver guidance for your filing year. Do not assume a disruption by itself is enough.

- Confirm your timeline records are complete and dated.

Before you invest more time, make sure your file clearly shows where you were and when. If timeline support is thin, flag the claim as higher risk.

- Confirm the likely exclusion impact before investing more time.

FEIE still requires foreign earned income and a foreign tax home, and not every payment item is foreign earned income. For example, employer-provided meals and lodging are not foreign earned income.

Eligibility checkpoint table#

| Requirement | What to verify | Proof you should have | If missing, do this |

|---|---|---|---|

| Foreign tax home | Your main work base was in a foreign country | Dated records that show where you were working and based | Build a dated timeline first; if the work base is unclear, pause and get review |

| Foreign earned income | Income was earned from services performed abroad | Dated pay, invoice, or payment records tied to work performed abroad | Separate potentially nonqualifying items before estimating any exclusion |

| Waiver guidance checkpoint | You reviewed filing-year IRS waiver guidance, including the Form 2555 instructions section titled Waiver of Time Requirements | A saved copy of the filing-year guidance and timeline notes | Verify current IRS waiver guidance before moving forward |

| Standard time-rule context | The ordinary requirement is 330 full days in a 12-month period | Complete day-count records for your 12-month period | Calculate your day count first; if you already qualify, that may be the cleaner route |

| IRS eligibility pre-check | IRS Interactive Tax Assistant results align with your planned position | Saved output or notes from the tool | Run the tool before drafting waiver-specific paperwork |

What should make you pause#

Pause if your tax home was not clearly abroad, your records do not clearly support foreign earned income, or your day-count timeline is incomplete. Also run your facts through the IRS Interactive Tax Assistant and review the Form 2555 instructions section titled Waiver of Time Requirements as a checkpoint.

If all four gates hold, move to Step 2 and build the evidence file that proves each gate with clear dates and records. For a step-by-step walkthrough, see Qualifying for the FEIE with Physical Presence or Bona Fide Residence.

Step 2: DOCUMENT - How to Build an Unassailable "Contingency File"#

In practice, the waiver is won or lost on the file. Your goal here is to collect the records that support the claim and let you complete Form 2555 accurately. Prioritize required Form 2555 fields first, because missing requested information can cause the exclusion to be disallowed.

Build the file around the three proof tests#

Use each record to support one of three points: foreign tax home and actual presence, reasonable expectation that you would have met the time test, and forced-departure context.

| Proof test | Must-have | Strong support | Helpful backup |

|---|---|---|---|

| Tax home and actual foreign presence | A dated travel timeline for your 12-month period with exact arrival and departure dates for Form 2555, plus records that tie your work activity to the foreign country. | Visa or residence-period records, if applicable, along with work/location records that show where you were based. | Dated day-to-day records that reinforce that your work base and life were abroad. |

| Reasonable expectation you would have qualified | The written statement attached to your return explaining that you expected to meet the time requirement. | Pre-disruption records showing your stay and work were expected to continue. | Contemporaneous emails or messages showing you expected to remain. |

| Forced departure and business disruption | The IRS waiver-country authority for the tax year filed, plus proof that your departure date fits that country window. For tax year 2025, Rev. Proc. 2026-16 lists: Haiti and Ukraine (on or after January 1, 2025); Democratic Republic of the Congo (January 28, 2025); South Sudan (March 7, 2025); Iraq (June 11, 2025); Lebanon (June 22, 2025); Mali (October 30, 2025). | Official U.S. Department of State travel advisories and records showing that conditions prevented normal business. | Your own dated notes and communications on what changed and when. |

| Document type | What it proves | Best format | Common weak spot |

|---|---|---|---|

| Day-count timeline | Form 2555 12-month period and actual presence days | One master dated timeline with file references | Dates do not reconcile across records |

| Waiver statement | Expected qualification + disruption impact | Final return-ready statement stored with tax file | Vague on dates, country, or business impact |

| Work/location records | Foreign tax home and work base abroad | Dated work and location records | Shows clients abroad, not where services were performed |

| IRS waiver-country record | Country/date eligibility for the filing year | Saved copy of the applicable IRS bulletin or procedure | Using the wrong tax-year list |

| Official condition records | Adverse-condition timing context | Saved advisory copy with visible date and URL | Only general news, no official date anchor |

| Visa/residence records (if used) | Residence period and entry status details | Clear scans of visa, permit, or registration | Missing dates or entry category |

Make it easy to review later#

A good file should read like a timeline, not a pile of attachments. For your own organization, use a consistent internal filename pattern, such as YYYY-MM-DD_country_documenttype_shortnote.pdf, and keep an index with the date, event, proof test, and filename. Sort records chronologically so an examiner or advisor can follow the story quickly.

Store everything digitally in a reliable system. Electronic records can satisfy recordkeeping when the storage system meets IRS electronic-record requirements.

Do not wait months to reconstruct this. If core dates do not reconcile, you cannot clearly support a foreign tax home, or your expected-stay evidence is thin, pause filing and get professional review. Keep the final file at least through the general 3-year IRS assessment window, and longer if another rule could extend it.

This pairs well with our guide on The Bona Fide Residence Test: A Deep Dive for US Expats. Before you file, run your travel timeline through the Tax Residency Tracker so your contingency file and waiver narrative stay consistent.

Step 3: CLAIM - A Line-by-Line Guide to Form 2555#

Do not file the claim until the current-year instructions and the current-year waiver list clearly fit your facts. If either one is unclear, stop and confirm before you submit.

Minimum claim package#

Your waiver claim is a package, not just one checkbox. At minimum, complete the waiver-related entry on Form 2555, include affected country details tied to the current-year IRS waiver authority, and provide a written explanation if the current instructions call for it.

That explanation should line up three points: foreign tax home, reasonable expectation that you would have met 330 full days in a 12-month period absent adverse conditions, and the disruption timing.

| Form field | What to enter | Why it matters | Common error to avoid |

|---|---|---|---|

| Physical Presence Test section | Enter your 12-month period so it includes part of the tax year at issue. | This test is measured across 12 consecutive months, not only the calendar year. | Picking a period that does not match your day-count timeline |

| Waiver question or checkbox | Mark the waiver entry only when your country and departure timing match the current Revenue Procedure. | This is the formal signal that you are claiming a waiver of the minimum time requirement. | Treating illness, family issues, vacation, or employer orders alone as enough for waiver eligibility |

| Country and authority entry | Enter the country name and the applicable current-year IRS waiver authority, following the current instructions. | Waiver eligibility is filing-year specific. | Using the wrong year's guidance |

| Presence dates and day-count support | Enter dates that reconcile exactly with your timeline. Count only full days, meaning 24 consecutive hours from midnight to midnight. | Date accuracy supports both your claim period and your waiver explanation. | Counting travel days incorrectly or submitting dates that conflict across records |

| Foreign tax home and income sections | Complete these sections to match where you actually worked and your foreign earned income records. | The waiver does not replace foreign tax home or foreign earned income requirements. | Leaving tax-home or foreign-earned-income details incomplete |

Days spent in a foreign country while in violation of U.S. law do not count toward physical presence, and related income from that period does not qualify as foreign earned income.

Pre-file checklist#

- Confirm Form 2555 dates, country naming, and work-location facts match your day-count timeline and your Step 2 documentation.

- Confirm your waiver entry, affected-country details, and explanation are complete and consistent with current-year instructions.

- If any field, date, or authority reference is uncertain, escalate to a qualified tax professional before filing.

You might also find this useful: The Physical Presence Test: A Day-by-Day Guide for the FEIE.

What If My Situation is More Complex? Strategic Alternatives#

When the waiver is uncertain, the right move is to compare paths before you file. Use this sequence: waiver fit -> bona fide residence fit -> Foreign Tax Credit model -> filing choice based on documentation strength and risk.

| Path | Best use case | What you must prove | Main upside | Main tradeoff | When to escalate to a pro |

|---|---|---|---|---|---|

| Physical Presence Test waiver | You may still qualify, but fit is unclear and needs a supportable file | Facts that align with applicable waiver guidance and your filing records | Keeps a waiver path on the table while you test alternatives | Can fail if your facts or documentation do not hold up | Borderline facts, inconsistent records, or unresolved filing-year questions |

| Bona fide residence test | Day-count facts are weak, but your life and work abroad show real residence | Foreign tax home plus bona fide residence facts | May fit better when travel disruption makes day counting unreliable | Fact-heavy and documentation-intensive | Multi-country year, weak ties, or unclear residence story |

| Foreign Tax Credit (FTC) | The same income is taxed by both the U.S. and a foreign jurisdiction | Potentially creditable foreign taxes and Form 1116 support if required | Intended to reduce double taxation; IRS says a credit is usually better than a deduction | You cannot claim FTC on income you exclude; some taxes are noncreditable | Mixed income streams, withholding complexity, amended returns, or uncertain tax character |

Check bona fide residence fit#

If waiver fit is weak, test whether your file supports residence abroad, not just presence abroad. Build the case in four buckets and keep the story consistent across your timeline, income records, and filing positions.

| Bucket | What it covers |

|---|---|

| Residency ties | Documents showing where and how you were based abroad. |

| Work continuity | Records showing work activity remained centered in that country. |

| Local integration | Records that show day-to-day life abroad beyond short stays. |

| Disruption timeline | A clear sequence of events showing how disruption affected an established setup. |

If housing is part of your plan, keep this rule in view. Foreign housing exclusion or deduction requires a foreign tax home plus qualification under either the bona fide residence test or the physical presence test. The housing deduction applies only to amounts paid with self-employment earnings.

Model the Foreign Tax Credit before you choose#

Run a side-by-side model before filing: waiver path, bona fide residence path, if supportable, and FTC. Separate income streams cleanly, and mark any income you plan to exclude so you do not also claim FTC on that excluded income.

Use Form 1116 as your FTC checkpoint when it is required for your claim. Foreign taxes generally must meet 4 tests to qualify, and some taxes are still noncreditable even if those tests appear satisfied. If dividend withholding is involved, check the holding-period rule, including the 16 days within a 31-day period test around the ex-dividend date. If timing or excess-credit treatment affects the result, confirm the current carryforward rule before filing.

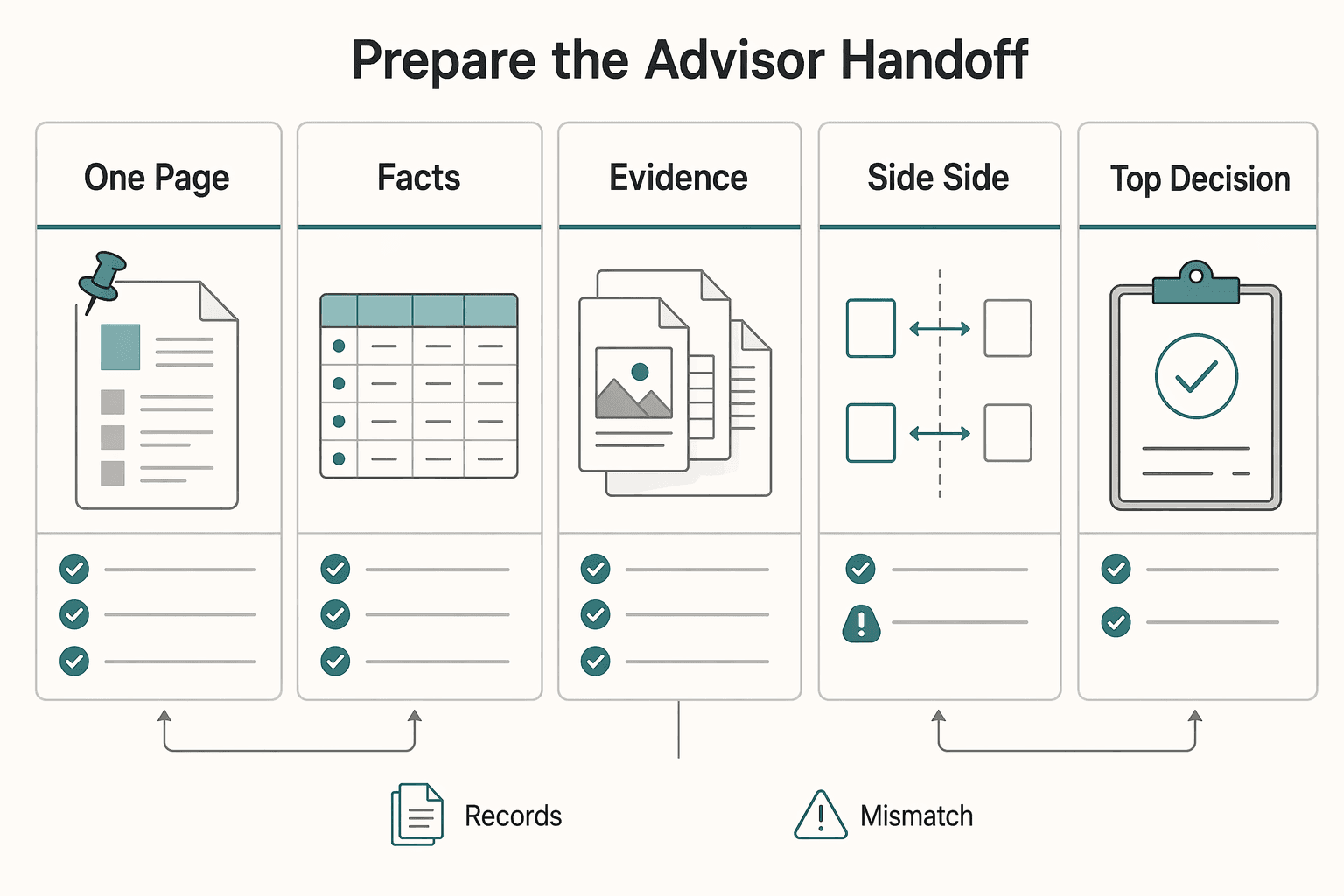

Prepare the advisor handoff#

If you need help, hand over a decision file, not a narrative. Use this brief template:

| Decision file item | What to include |

|---|---|

| One-page timeline | Arrival, work period, disruption, departure, return if any. |

| Draft Form 2555 facts | If pursuing FEIE, with supporting records. |

| Foreign tax records | Grouped by tax type. |

| Side-by-side worksheet | Waiver vs bona fide residence vs FTC. |

| Top decision questions | Ranked by tax impact and risk. |

I may qualify for the waiver, but I want it tested against bona fide residence and the Foreign Tax Credit before filing.

My tax home facts, disruption timeline, and foreign tax records are attached with a side-by-side model.

Please advise on the strongest filing position, main audit risk, and any missing evidence.

If you are filing an amended return for French CSG/CRDS FTC treatment, flag it early so the Form 1040-X labeling step is handled correctly.

We covered this in detail in Bona Fide Establishment Test FEIE for Form 2555 Decisions.

Beyond the Crisis: Solidifying Your Financial Position#

Once this year's return is filed, the practical next step is to keep the same discipline going. Turn Assess, Document, Claim into a repeatable annual process so you are not rebuilding your tax position from scratch every time the facts change.

| If you stay reactive | If you stay early |

|---|---|

| You gather leases, travel logs, and work records only after a filing issue appears. | You keep a living contingency file current with travel, housing, work, and waiver-period support records when relevant. |

| You wait until return prep to decide between FEIE and FTC. | You run FEIE-vs-FTC reviews before year-end and again before filing while records are still easy to confirm. |

| You contact an advisor only when your timeline is incomplete. | You keep a pre-vetted advisor active and share updates when country, status, or travel patterns change. |

| You file using partial records and weak comparisons. | You choose your Form 2555 or Form 1116 path with documented inputs and a clear filing rationale. |

The goal is better decisions, not generic preparedness. FEIE-related benefits require foreign earned income and a foreign tax home. The physical presence route is time-based: 330 full days in a 12-consecutive-month period, with each full day measured as 24 consecutive hours from midnight to midnight. A waiver of the minimum time requirement may apply if you had to leave because of war, civil unrest, or similar adverse conditions, and the filing-year Revenue Procedure supports the country and waiver start date.

Your next-year execution checklist#

- Maintain a living contingency file. Keep your travel timeline, housing records, work records, contracts, and the filing-year Revenue Procedure you may need for waiver country and date verification.

- Run a recurring FEIE-vs-FTC strategy review. FEIE limits are tax-year specific, for example, $130,000 for 2025 and $132,900 for 2026. Excluded income is still reported on your U.S. return. Housing exclusion is figured first when applicable. FTC setup on Form 1116 is done separately by income category with one category checkbox per form and separate country or territory columns or lines where required.

- Keep your advisor process active before disruptions. Maintain a working relationship with someone who already understands your countries, income mix, and qualification path.

Annual planning inputs (decision framework)#

| Input | What to review each year |

|---|---|

| Income type mix | Confirm whether your wages, salaries, professional fees, or other personal-service compensation still fit your planned treatment. |

| Tax residency posture | Reconfirm whether your facts still support a foreign tax home in the country you are relying on. |

| Foreign tax paid | Document taxes paid by income category and by country or territory for Form 1116 setup if FTC is in play. |

| Mobility pattern | Re-test whether your travel pattern still supports your day-count and documentation story. |

Escalate early, before filing, if your status changes or you move countries. Also escalate if your return adds cross-border complexity or your records no longer cleanly support the path you plan to claim. Related: 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

If your facts are mixed across FEIE qualification and FTC paths, contact Gruv to map a low-risk next-step workflow.

Frequently Asked Questions

How do you qualify for the FEIE physical presence test waiver?

You qualify only if you can support three points: your tax home was in a foreign country, you were physically present in or a bona fide resident of the affected country on or before that filing year’s waiver start date, and you reasonably expected to meet 330 full days in a 12-consecutive-month period before adverse conditions forced you out. Your timeline also has to hold up under the day-count rules, including that a full day is 24 consecutive hours from midnight to midnight. Action: Build a one-page timeline that aligns your travel records, work records, and the filing-year waiver dates.

Which countries are eligible for the waiver?

You should verify eligibility fresh for your filing year every time. The IRS publishes a Revenue Procedure each year with covered countries and waiver begin dates, and your country and dates both need to match. Action: Save the filing-year Revenue Procedure in your contingency file and mark the exact country and date match you are relying on. | Path | When to use | What you need to prove | Common failure point | |---|---|---|---| | Waiver path | You left because of war, civil unrest, or similar adverse conditions before reaching 330 full days | Foreign tax home, qualifying presence or residence tied to the waiver period, and a reasonable expectation you would have met the time requirement absent disruption | Country or period does not match filing-year guidance, or your expectation-to-stay evidence is weak | | Bona Fide Residence Test path | Your day count is weak, but your life abroad may support true residence | Bona fide residence in a foreign country for an uninterrupted period that includes an entire tax year | Your records do not support a full-year residence story | | Foreign Tax Credit path | You need to compare a non-exclusion path before filing | A supportable foreign tax credit position that stays consistent with the rest of your return | The comparison is incomplete or inconsistent with the rest of the return |

Do you get the full FEIE amount with the waiver?

No. You should not assume the waiver gives you a full-year exclusion. The waiver can preserve eligibility on the minimum-time requirement, but you still need to confirm the exclusion amount from your facts and current Form 2555 instructions. Action: Run your exclusion calculation before filing and compare it against your alternative path.

What form do you use to claim the waiver?

Use Form 2555 and the current instructions for waiver-related entries. Keep a filing checklist with your filing-year Revenue Procedure and retained backup documents such as the Revenue Procedure copy, timeline, travel records, and work or client records. Action: Draft Form 2555 from the current instructions before you finalize your return.

What if your country is not listed?

If your country and period do not match filing-year IRS guidance, do not rely on the waiver path. Your next step is to test bona fide residence fit and compare the Foreign Tax Credit before filing. Action: Hand this to a qualified expat tax professional before filing if the country and date match is unclear, your year spans multiple countries, or your records do not clearly support one path.

Does the waiver apply to the Bona Fide Residence Test?

No. The waiver is tied to the minimum-time requirement in the physical presence route, not the bona fide residence route. Bona fide residence stands on its own and requires an uninterrupted period that includes an entire tax year. Action: Choose your primary qualification path early and make sure your documents support that one story.

When should you stop and hand this off?

Stop and escalate before filing if your case depends on a borderline country-date match, conflicting day counts, or weak tax-home support. You should also escalate when your result depends on choosing between waiver, bona fide residence, and Foreign Tax Credit paths. Action: Send a pro your timeline, draft Form 2555 facts, and filing-year Revenue Procedure so they can validate the filing position quickly.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

The Physical Presence Test: A Day-by-Day Guide for the FEIE

Start with one objective: qualify for the Foreign Earned Income Exclusion through the Physical Presence Test using facts you can prove, not assumptions you hope survive review. This is not a loophole hunt, and it is not just a math exercise. The goal is a filing position that is clear, repeatable, and defensible.