Quick Answer

The most overlooked freelancer deductions are usually ordinary, necessary business costs that get missed because they are poorly classified or weakly documented, such as the business portion of communications, self-employed health insurance, one-half of self-employment tax, qualifying business travel and education, and eligible retirement contributions. The key is proving business purpose, current income activity, documentation, and any mixed-use allocation.

The CEO Mindset: Frame Your Deductions as Investments, Not Loopholes#

Do not approach deductions like a scavenger hunt. Treat them like any other business decision, something you should be able to justify, document, and defend if the IRS asks about it later.

The burden of proof is on you. A deduction needs substantiation, not just a business label in your bank feed. Use these anchors:

- Ordinary: common and accepted in your trade or business.

- Necessary: helpful and appropriate for your business, even if not strictly required.

- Contemporaneous-style record: created at or near the time of the expense and supported by documents such as receipts, bills, or canceled checks.

Use a practical test: business purpose, expected operational value, documentation trail. If you cannot clearly explain the business reason, the benefit you expected, and where the proof lives, do not treat it as deductible yet. For higher-scrutiny categories under Section 274, unsupported estimates or memory alone are not enough.

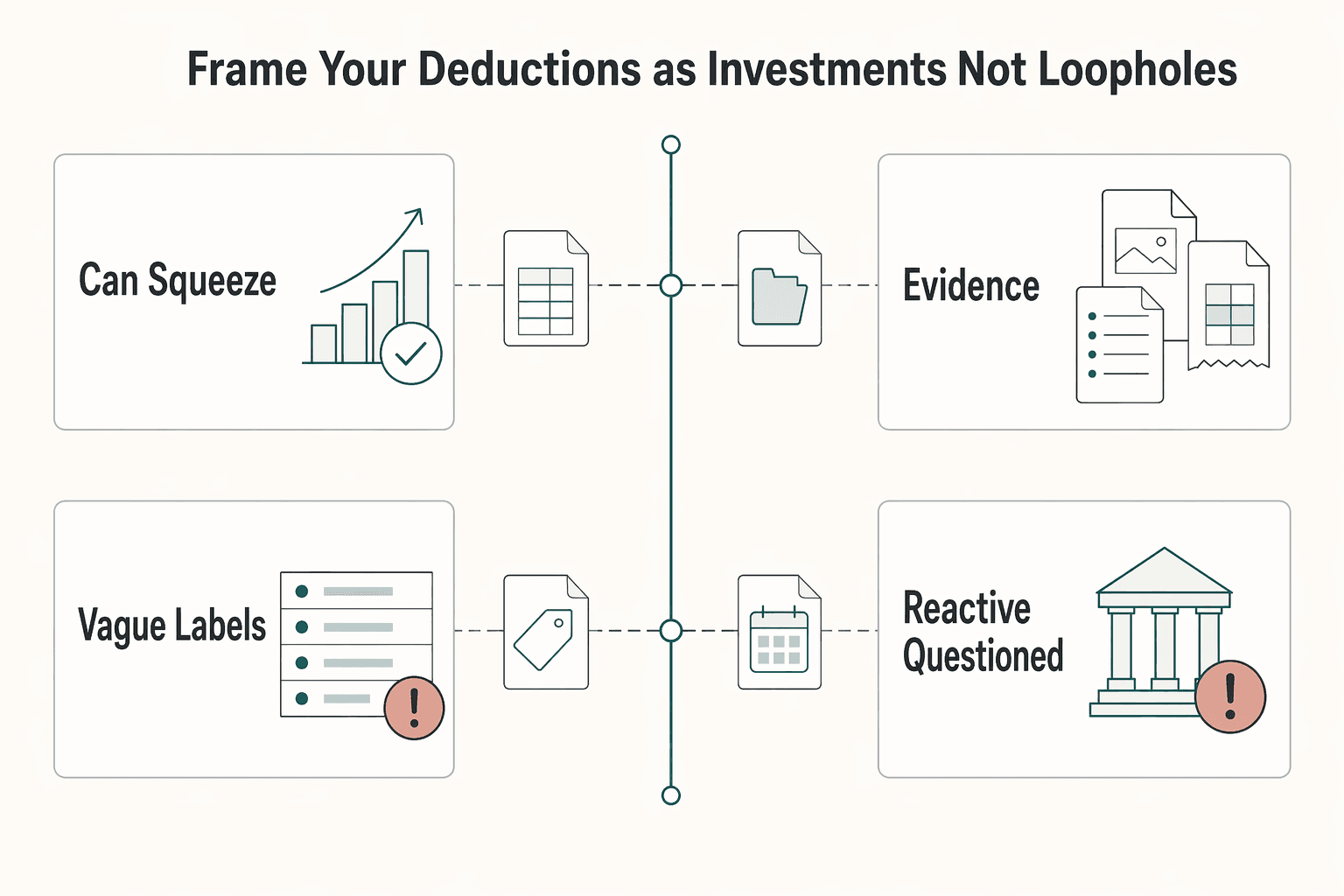

| Loophole thinking | CEO thinking |

|---|---|

| "Can I squeeze this in?" | "What business problem did this solve?" |

| Weak evidence, often just a card charge | Receipt or invoice plus a note with business purpose |

| Documentation created months later | Record created at or near the transaction |

| Vague labels like "supplies" | Details that show the business link |

| Reactive when questioned | Ready to substantiate with organized records |

Be especially careful with mixed-use and borderline expenses. If the business link is thin or the personal benefit is obvious, flag it for review instead of forcing it into your books. The IRS lets you choose any recordkeeping system that clearly shows income and expenses, but "I know what it was" is not a system. Before Part 1, run this quick checkpoint:

- Classify the expense

- Confirm the business link

- Capture proof now

- Add a note on expected business benefit

- Flag edge cases for professional review

For a separate, non-U.S. tax context, see A Deep Dive into the UAE's Corporate Tax for Freelancers and LLCs.

Part 1: A Strategic Framework for Identifying Your Deductions#

The simplest way to stay consistent is to sort spending by what it does for the business, then apply the legal test. RUN, PROTECT, GROW, and FUND are working buckets, not legal tax categories. The rule does not change: an expense must be ordinary and necessary. Personal or family costs are generally not deductible. You also must be able to substantiate what you claim.

| Bucket | Examples mentioned | Key caution |

|---|---|---|

| RUN | software, cloud storage, invoicing systems, domains, and the business portion of communications costs used for client delivery | If phone or internet use is mixed, split business and personal use and keep records that support your allocation |

| PROTECT | business risk management and business tax/compliance work; self-employed health insurance deduction; self-employment tax adjustment | Do not deduct personal legal or financial work, and do not leave blended invoices unsplit |

| GROW | business travel that meets IRS tests and education that maintains or improves skills used in your current work | Education that prepares you for a new trade does not belong here. Exclude personal-purpose portions and trips that fail the tax-home or assignment rules |

| FUND | retirement contributions; one-participant 401(k); SIMPLE IRA; SEP-IRA or other self-employed plans | Do not rely on brokerage transfers, rough estimates, or prior-year assumptions that you have not rechecked |

Use this four-step screen before you classify any expense:

- What specific business purpose did this serve?

- Is it tied to your current income activity, not personal use or training for a new trade?

- What proof do you have now: receipt, invoice, statement, contract, itinerary, agenda, and a short business-purpose note?

- Is it mixed use? If yes, deduct only the business portion.

The IRS has discontinued current revisions of Publication 535, so rely on current IRS topic pages and form instructions for each deduction you claim.

RUN#

Start with the costs that keep the business moving. For many mobile freelancers, that may include software, cloud storage, invoicing systems, domains, and the business portion of communications costs used for client delivery, when those costs are ordinary, necessary, and substantiated.

Do not group personal, vague, or unsupported spending into this bucket. If phone or internet use is mixed, split business and personal use and keep records that support your allocation.

PROTECT#

This bucket covers spending tied to business risk management and business tax/compliance work.

Do not deduct personal legal or financial work, and do not leave blended invoices unsplit. If one bill includes both business and personal services, separate the charges before you deduct anything. Two items in this bucket deserve extra care:

- Self-employed health insurance deduction: Use Form 7206 and confirm eligibility under the form rules before claiming it.

- Self-employment tax adjustment: If net self-employment earnings are $400 or more, you usually owe self-employment tax. Generally, 92.35% of net earnings is subject to the tax, made up of 12.4% Social Security plus 2.9% Medicare, and you can deduct one-half of that tax. Use your Schedule SE result, not an estimate.

If your year includes structure changes, multiple income streams, or mixed personal and business treatment questions, escalate to a tax pro.

GROW#

Growth spending is deductible only when it supports the business you already operate. That can include business travel that meets IRS tests and education that maintains or improves skills used in your current work.

The main traps are qualification and allocation. Education that prepares you for a new trade does not belong here. Travel also needs extra discipline. Exclude personal-purpose portions and trips that fail the tax-home or assignment rules. An assignment expected to last more than 1 year is treated as indefinite.

For travel, build a basic evidence pack every time: itinerary, meeting or event details, receipts, and a short note linking the trip to current income activity. If travel is material, raise your file standard and review A Guide to Deducting Business Travel Expenses.

FUND#

Retirement contributions can be valuable, but only after you confirm the right plan and calculate the deductible amount under self-employed rules. Do not rely on brokerage transfers, rough estimates, or prior-year assumptions you have not rechecked. For current-year caps, verify the latest IRS limits before filing.

| Option | Eligibility constraints | Admin burden | Contribution flexibility | Best fit |

|---|---|---|---|---|

| One-participant 401(k) | Owner-only business or owner plus spouse | Can require additional filing once combined one-participant plan assets exceed $250,000, using Form 5500-EZ | Flexible design, but calculations and compliance still matter | You have no employees other than a spouse and want an owner-focused plan |

| SIMPLE IRA | Generally for small employers with 100 or fewer employees; employer contributions are part of plan design | Ongoing employer-plan administration | Structured, rule-based contributions | You run a small business and can meet SIMPLE plan rules |

| SEP-IRA or other self-employed plans | Verify current IRS plan rules and eligibility | Varies by plan and setup | Varies by plan and self-employed calculation method | You want a plan option that fits your business after current-year calculations |

Across all four buckets, the standard does not change. If you cannot show business purpose, a link to current income activity, documentation, and the correct mixed-use allocation, do not deduct it yet. Related: How to Handle Taxes for a Side Hustle.

Part 2: An Operational System for Frictionless Documentation#

If you want deductions to hold up, treat documentation as part of the expense itself. The safe default is simple: capture it when it happens, do a short weekly cleanup, and if evidence is missing, do not deduct it yet.

"Contemporaneous documentation" means creating records at or near the time of the expense or use, not rebuilding them later from memory. "Adequate substantiation" means you can support each required element with records or other corroborating evidence. In practice, payment proof alone is not enough. For each expense event, build this proof stack:

- Receipt or bill: amount, date, place or vendor, and what was purchased.

- Business-purpose note: one clear sentence tying the spend to current income activity.

- Participant or context note: who benefited or attended, and the business relationship or context when relevant.

- Category tag: your internal bookkeeping label, which helps your process but is not stand-alone legal proof.

Your weekly operating procedure#

Keep the process simple. It just needs to happen on time and in the same order every week.

| Step | What to do | Key detail |

|---|---|---|

| Capture | Save the receipt, invoice, confirmation, or trip log at the time of spend or use | For many non-lodging expenses, documentary evidence is generally required at $75 or more, but keep support for smaller items too |

| Classify | Post the item to your books right away using your Part 1 bucket and accounting category | Right away |

| Annotate | Add the business-purpose note immediately | For meals and similar items, include the business context and the people involved when relevant |

| Store | Attach records to the transaction in your system and keep a consistent folder structure | Keep files easy to retrieve |

| Review | Once a week, clear uncategorized items, attach missing documents, and complete open notes while details are still fresh | If support is incomplete, keep the item as pending, not deductible |

The order matters. Capture first, classify while the transaction is obvious, add the note before details fade, and leave anything with missing support in pending status rather than treating it as deductible.

Vehicle and home office claims need tighter proof than routine overhead. For vehicle use, log each business trip as it occurs. You need substantiation for the amount of business use, plus time and business purpose for each use. If you use the 2026 standard mileage rate (72.5 cents per mile), the logging requirement still applies.

For home office claims, keep records that show the business area and how it is used over time. Make sure your records support both tests: exclusive use and regular use.

Common failure points#

| Common record-keeping failure | Defensible system behavior |

|---|---|

| Meal receipt with only amount and restaurant name | Receipt plus near-time note covering business purpose, date, amount, place, number of people served, and business relationship or context when relevant |

| Travel paid by card but no trip file | Keep records that establish time, place, amount, and business purpose (for example, itinerary or booking details plus a short business-purpose note) |

| Mileage rebuilt at year-end | Log trips as they happen, then classify and complete purpose notes during weekly review |

| Home office claim with no setup proof | Keep records supporting exclusive and regular business use (for example, dated photos and measurements of the business area) |

When to escalate#

Some files stop being routine once allocation, missing logs, or multiple jurisdictions enter the picture. Escalate to a tax professional when mixed personal and business use is hard to allocate, logs are incomplete, or cross-border records add complexity.

For cross-border files, keep the original foreign-currency records and use one consistent USD translation method for the year. Verify any local invoice, VAT or GST, or residency-specific requirements before you rely on them.

If foreign account reporting overlaps with your bookkeeping, follow the separate retention timeline for those records. FBAR records generally must be kept for 5 years from the due date, April 15, with an automatic extension to October 15.

For a step-by-step walkthrough, see The S-Corp Election for LLCs: A Tax-Saving Strategy for High-Earning Freelancers. Before you lock your documentation workflow, run your assumptions through the Mileage Deduction Calculator so your tracking categories match what you plan to claim.

Part 3: Fortifying Your Major Deductions#

Once your basic capture process is in place, raise your standards on deductions that are often scrutinized: meals, home office, and QBI. Do not file from memory, assumptions, or partial records. If a required element is missing, pause the claim until the file is complete.

Meals#

Business meals are easy to overclaim and easy to under-document. Buying food while working does not make it deductible. Keep the entry only if it is ordinary and necessary, you or your employee were present, and it was not lavish or extravagant. Then apply the general 50% limit for unreimbursed non-entertainment business meals.

Before you file each meal, make sure your file shows:

- amount

- date and place

- who attended or who benefited, plus business relationship or context when relevant

- specific business purpose tied to current income activity

- proof you or your employee were present

If your note says only "networking" or "client meeting," treat it as incomplete. You should be able to say what business was discussed and why the meal was helpful and appropriate to your trade.

| Entry pattern | High-risk version | Defensible version |

|---|---|---|

| Client lunch | Receipt only, no topic or attendee context | Receipt plus near-time note with attendees, business relationship or context, and the deal or project issue discussed |

| Solo meal during travel | Card charge with no trip linkage | Meal tied to a travel file that shows time, place, and business purpose |

| Per diem or standard meal allowance | Assumes allowance replaces records | Keeps records proving time, place, and business purpose even when allowance is used |

Home office#

Home office claims turn on qualification first and method second. Where exclusive use is required, mixed personal and business use disqualifies the area. Pause the claim unless a recognized exception applies, such as certain storage or daycare situations.

Once the space qualifies, choose the method you can support:

| Decision factor | Simplified method | Actual-expense method |

|---|---|---|

| Simplicity | Higher | Lower |

| Record burden | Lower | Higher, because you must support business-use percentage and prorated costs |

| Upside potential | Capped by fixed rate and square-foot limit | Can be higher if records are strong |

| Documentation sensitivity | Lower, with fewer inputs to support | Higher, because allocation support is easier to challenge when weak or inconsistent |

For the simplified method, verify the current amount and cap before filing. For the actual-expense method, keep dated photos, measurements, a basic floor plan, and support for regular and exclusive use where required.

QBI#

Treat the Qualified Business Income deduction under Section 199A as an eligibility check, not an automatic win.

- Confirm income type. Many sole proprietorship, partnership, and S corporation owners may qualify; C corporation income and employee wages do not.

- Check your taxable income before the QBI deduction against the current threshold in the applicable instructions.

- If you are above that level, evaluate limitation triggers, including business type and tests tied to wages or property basis, before relying on the result.

For 2026, verify current instructions before you lock your position. Current IRS materials are not fully harmonized. Older QBI language references a period ending on or before December 31, 2025. A newer IRS 2026 fact sheet says post-July 4, 2025 law made the deduction permanent. Use current Form 8995 or 8995-A instructions as your filing anchor.

If meal purpose is unclear, office use is arguably mixed, or your QBI result changes based on threshold or limitation assumptions, escalate to a tax professional before filing. You might also find this useful: Top 10 Tax Deductions for Freelancers.

Part 4: The Global Layer for Cross-Border Professionals#

Cross-border deductions often fail on allocation and conversion even when an expense feels business-related. If the file is incomplete, pause the claim.

| Topic | Core rule | Key risk |

|---|---|---|

| FEIE expense allocation | Use the allocation rule: excluded foreign earned income over total foreign earned income, and apply it only to deductions that are definitely related to excluded earned income. FEIE does not reduce self-employment tax | Deducting 100% of expenses while excluding most or all of the same income; claiming a foreign tax credit on income you excluded |

| Foreign home office | A foreign home office follows the same core rule as a domestic one: exclusive and regular use for your trade or business | If the space is also used personally, the deduction is generally disallowed for that area |

| International health insurance | Run them through Form 7206. The potential deduction can include qualifying medical, dental, vision, and qualified long-term care premiums | Claiming a full-year deduction when subsidized-plan eligibility existed for part of the year |

| Multi-currency tracking | Report U.S. return amounts in U.S. dollars and use one consistent conversion method | Changing methods to optimize deductions and breaking consistency |

FEIE expense allocation#

Start by classifying the income, because the deduction treatment follows from that. Excluded income is foreign earned income you exclude on Form 2555, up to $132,900 per qualifying person for 2026, prorated if you qualify for only part of the year. Taxable self-employment income is the rest, including income above the FEIE limit, income from nonqualifying days, or income you did not exclude. FEIE may apply to foreign earned self-employment income, but it does not reduce self-employment tax.

For deductions tied to excluded income, use the allocation rule: excluded foreign earned income over total foreign earned income. Apply this only to deductions that are definitely related to excluded earned income. Use this decision path:

- If an expense relates only to taxable income, deduct it under normal rules.

- If an expense is definitely related to income that is partly excluded and partly taxable, prorate it with the FEIE fraction.

- If an expense is definitely related only to excluded income, do not use that portion against regular taxable income.

- Flag the return for professional review if you have mixed excluded and taxable income, part-year FEIE qualification, or FEIE plus a foreign tax credit position. You cannot claim a foreign tax credit on income you excluded, and doing so can put the FEIE election at risk.

Keep a workpaper showing total foreign earned income, excluded amount, the fraction used, and which expenses you treated as definitely related. A key risk is deducting 100% of expenses while excluding most or all of the same income.

Foreign home office#

A foreign home office follows the same core rule as a domestic one: exclusive and regular use for your trade or business. If the space is also used personally, the deduction is generally disallowed for that area.

Document it like you would any other high-scrutiny claim. Keep records that support business use and allocated costs, such as dated photos, measurements, a simple floor plan, and rent or utility support when relevant. If personal use appears, pause the claim unless an IRS exception applies.

International health insurance#

Do not assume premiums are fully deductible. Run them through Form 7206. The potential deduction can include qualifying medical, dental, vision, and qualified long-term care premiums.

Apply the monthly eligibility rule carefully. If you were eligible for an employer-subsidized plan, yours or your spouse's, for a month, exclude that month's premium amount from the deduction calculation. One mistake to avoid is claiming a full-year deduction when subsidized-plan eligibility existed for part of the year.

Multi-currency tracking#

Report U.S. return amounts in U.S. dollars and use one consistent conversion method. In practice, that means choosing a posted rate source, picking a method for the year, documenting that choice, and avoiding transaction-by-transaction switching.

| Conversion approach | Best use | Records to keep | Common mistake to avoid |

|---|---|---|---|

| Spot rate on payment date | Infrequent or high-value expenses | Receipt or invoice, payment date, exchange rate used on that date, saved source record, USD calculation | Using a statement-closing date instead of the payment date |

| Yearly average rate | Recurring, similar expenses where average-rate treatment is appropriate | Method memo for the year, rate source, list of expenses converted with that same yearly average, underlying receipts | Mixing yearly average and spot-rate treatment without a documented rule |

| Ad hoc switching | Not a method to rely on | None | Changing methods to optimize deductions and breaking consistency |

Use this checklist to keep the method consistent:

- Choose a posted exchange-rate source and apply it consistently.

- Choose one conversion method for the tax year.

- Write down the method decision.

- Keep evidence for each converted expense.

- Retain records as long as needed to support the return position. The general assessment window is generally 3 years.

If you want a deeper dive, read Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

Conclusion: You Are the CEO - Build the Systems to Prove It#

Deductions work only if your records can substantiate them. You carry the burden of proof, so claim only expenses that are ordinary, necessary, and supported by records you can produce.

Capture proof when money moves#

- What to do: Save the receipt, bill, or similar documentary evidence when you spend, and record the business purpose right away.

- Where to track it: Use a recordkeeping system that clearly shows income and expenses, and keep it current year-round.

- Done looks like: Any expense in your books can be matched to documentation plus a short business-purpose note without relying on memory. For travel, gifts, and auto expenses, keep the added substantiation those categories require.

Review on a fixed calendar#

- What to do: Run a recurring review of income, expenses, and tax paid, then do an estimated-tax check each quarter.

- Where to track it: Calendar reminders and a simple tax tracker with year-to-date profit, payments made, and expected balance due.

- Done looks like: Before April 15, June 15, Sept. 15, and Jan. 15 (following year) for calendar-year taxpayers, you know whether you may owe $1,000 or more and whether underpayment penalty risk is building, even if you expect a refund at filing.

Plan spending before you incur it#

- What to do: Tie major purchases, training, and travel to a current business goal before spending.

- Where to track it: Budget notes, project plans, or purchase notes.

- Done looks like: The business purpose is documented before or at purchase, not reconstructed at return time.

Know when to self-manage and when to escalate#

Self-manage when your records are contemporaneous, deductions are straightforward, and foreign-currency amounts are translated into U.S. dollars consistently. Escalate to a qualified tax professional when cross-border income, Form 2555, an FEIE decision, overlap between excluded income and foreign taxes, or multi-country records create ambiguity. If you hire a preparer, you still remain responsible for what is filed.

For the next filing cycle, use the safe default: claim only what you can document, explain, and repeat consistently. This pairs well with our guide on A Guide to the Qualified Business Income (QBI) Deduction for Freelancers. If your year spans multiple countries, use the Tax Residency Tracker to keep your residency timeline and filing records organized before tax season.

Frequently Asked Questions

What is the safer way to handle your home office deduction?

Confirm the exclusive and regular use test first, then choose the method you can document consistently. The simplified method uses a flat $5 per square foot deduction, up to 300 square feet, and is usually lighter on records. If your records are thin, simplified is usually safer. If your records are complete and organized, the regular method may be worth the extra work, but you cannot switch methods later for that same tax year.

What does a meal deduction need in your file by filing time?

A receipt alone is not enough. Keep records for the date, place, amount, and business purpose, plus clear business context when relevant. If you cannot explain the business purpose without relying on memory, or you only have a card statement total, the claim is too weak to file.

Can you deduct self-employed health insurance if you also claim the FEIE?

Yes, but handle it in order. Confirm you qualify for the self-employed health insurance deduction, then confirm whether you are filing Form 2555. If you file Form 2555, use Form 7206 and report deductions disallowed as allocable to excluded income as required on Form 2555. If your year includes both excluded and taxable self-employment income, do not estimate allocations and talk to a cross-border tax professional.

What records do you need for a vehicle deduction?

Vehicle deductions need stronger substantiation than many other business expenses. Keep a log showing the date of each trip, mileage or amount claimed, destination or place, business purpose, and supporting records such as receipts or bills. If the log was rebuilt at tax time, trip purposes are missing, or the mileage does not tie to your work activity, the claim is too weak to claim.

Are professional courses, certifications, and training deductible?

They are deductible only if the education maintains or improves skills you use in your current work, or is required to keep your current status or pay. They are not deductible if the program qualifies you for a new trade or business, even if some skills overlap. A course that deepens skills you already use for client work can fit, but training for a different profession does not.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

How to Handle Taxes for a Side Hustle

If you want less stress at filing time, use sequence instead of shortcuts. When one year includes payroll income, contractor income, and time in more than one country, the order of operations matters. This guide gives you a defensible path so you can make each decision once, document it, and avoid rebuilding the return later.

A Guide to Deducting Business Travel Expenses

**For deducting business travel expenses, use a repeatable compliance system so you only claim costs you can prove.**