Quick Answer

Financial control for freelancers comes from building a three-tier Pyramid of Control: fix operations first, then tighten compliance, then build margin and optionality. Start by standardizing onboarding, billing terms, and reminder systems, then track residency, FBAR exposure, and authority boundaries, and finally use clear offers, capacity planning, and a small dashboard to protect margin and reduce stress.

For high-earning independent professionals, the jump from a six-figure income to durable wealth rarely comes from working harder. It comes from building control. Too many people stay in reactive mode, chasing invoices, absorbing scope creep, and dealing with global compliance issues after the fact. They may be strong practitioners, but they are still operating like reluctant CEOs.

The way out is to build a business that prevents problems instead of patching them. This is the Pyramid of Control, a three-tier framework for turning a fragile, high-stress practice into a resilient business. It starts with operations, not entity charts or complex structuring, because weak foundations make every later fix harder.

Tier 1: Conquer Operational Drag#

Tier 1 is where you stop small misses from turning into cash-flow stress or compliance exposure. Use one operating rule: no work starts until intake is complete, billing terms are clear, and a kickoff owner is assigned. A short gate often works better than a long packet, so your minimum handoff should be complete before kickoff:

Set a minimum onboarding standard#

- Finalize and sign the statement of work, or equivalent scope document.

- Send the correct tax form for the actual payer and payee setup.

- Confirm legal entity name, billing contact, and invoice delivery route.

- Assign kickoff owner and schedule kickoff only after the prior items are done.

- In kickoff, explicitly confirm deliverables, approvals, communication channel, and client obligations.

Pick tax forms by relationship, not habit. For U.S. payer reporting, Form W-9 is the baseline when you provide your TIN for information returns, and $600 or more in nonemployee compensation can trigger 1099-NEC reporting. For a foreign individual in U.S. withholding or reporting contexts, use Form W-8BEN. For a foreign entity, use Form W-8BEN-E.

| Area | Manual | Systemized | Automated |

|---|---|---|---|

| Onboarding | Ad hoc emails, scattered docs, kickoff scheduled too early | Standard intake checklist with scope and tax-form selection by payer/payee type | Form-driven intake, e-signature, kickoff task created only after signed scope and required form receipt |

| Billing follow-up | You chase late invoices manually | Contract defines deposits, milestones, due dates, and late-payment rights | Scheduled pre-due and overdue reminders, recurring billing where appropriate, MoR support for transaction handling in relevant models |

| Admin workload | Non-billable work is reactive and hard to see | Recurring admin tracked in a fixed review cadence | Reminders, routing, and status updates triggered automatically |

Tighten collections in the right order#

Collections get easier when you set payment control in the right sequence: contract terms, then reminder automation, then Merchant of Record, if needed.

| Control | Purpose | Key detail |

|---|---|---|

| Contract terms | Set deposits, milestones, due dates, and late-payment consequences | If work is governed by UK or EU rules, align clauses to the right jurisdiction; UK late B2B payment interest can be 8% plus the Bank of England base rate; EU summary rules say businesses generally pay within 60 days unless expressly agreed otherwise and not grossly unfair, and public authorities have a 30-day deadline. |

| Reminder automation | Make follow-up consistent instead of memory-based | QuickBooks can schedule reminders before or after due dates, up to 90 days; Xero supports up to five reminders. |

| Merchant of Record | Use when transaction compliance is the main risk | An MoR is legally responsible for processing payments and may handle calculating, collecting, and remitting sales tax, VAT, or GST; it is a scoped transfer of responsibility, not a blanket transfer of liability. |

Start with the contract because that is where deposits, milestones, due dates, and late-payment consequences are actually set. If your work is governed by UK or EU rules, align those clauses to the right jurisdiction. UK late B2B payment interest can be 8% plus the Bank of England base rate. EU summary rules say businesses generally pay within 60 days unless expressly agreed otherwise and not grossly unfair, and public authorities have a 30-day deadline.

Then add automation so follow-up is consistent instead of memory-based. QuickBooks can schedule reminders before or after due dates, up to 90 days, and Xero supports up to five reminders. That improves timing and reduces chasing, but it does not replace your withholding, reporting, or contract-law obligations.

Bring in a Merchant of Record when transaction compliance is the main risk, not just slower collections. An MoR is legally responsible for processing payments and may handle obligations like calculating, collecting, and remitting sales tax, VAT, or GST. That can reduce compliance exposure, but it is a scoped transfer of responsibility, not a blanket transfer of liability.

Run a short admin audit every two weeks#

A short audit is enough if you use it to make decisions instead of just reorganizing tasks. Run a brief review every two weeks and put each recurring non-billable task in one of three buckets: eliminate, automate, delegate.

Eliminate tasks with no client, legal, or financial value. Automate rule-based repeats, such as reminders and scheduling prompts. Delegate tasks that need a human but not your judgment.

Close each audit with one check: did this free capacity for higher-value work, such as delivery, sales, or compliance review? If not, you only moved admin around.

You might also find this useful: The 'Autonomy Premium': Why High-Earners Choose Freelancing Over Stability.

Tier 2: Build Your 'Compliance Moat'#

Tier 2 is where you prevent avoidable compliance problems by making your location, account, and authority facts easy to track and easy to prove. Focus on four controls: residency tracking, FBAR monitoring, PE guardrails, and audit-ready records.

Make residency tracking a single source of truth#

Scattered calendars and inbox threads fail when you need to prove where you were. Keep one residency log as your source of truth.

| Jurisdiction | Threshold | Period |

|---|---|---|

| U.S. substantial presence test | 31 days during the current year; 183 days during the weighted 3-year period | Current year and weighted 3-year period |

| Spain | More than 183 days | Calendar year |

| UK | 183 days or more | Relevant tax year |

- Set up: Track each trip's arrival date, departure date, jurisdiction, and supporting evidence, such as tickets, booking confirmations, passport evidence, and calendar entries.

- Monitor: Check country rules tied to where you work and where clients operate. For the U.S. substantial presence test, track 31 days during the current year and 183 days during the weighted 3-year period. For Spain, track more than 183 days during the calendar year. For the UK, track 183 days or more in the relevant tax year. For other countries, use the verified local threshold.

- Act: Review weekly during active travel and run a forward-looking review monthly. Escalate when travel plans change, a stay is extended, or your client footprint changes in a frequently visited country.

| Control option | Reliability | Maintenance effort | Error exposure |

|---|---|---|---|

| Manual notes in email/calendar | Low | Low initially, high during reconstruction | High, with split dates and missing evidence |

| Spreadsheet + linked evidence folder | Medium to high, if maintained | Moderate | Medium, with missed entries and formula errors |

| Specialized tracker + evidence archive | High, if configured and reviewed | Moderate setup, lower ongoing effort | Lower, but still dependent on input and review |

If you travel only occasionally, a disciplined spreadsheet can work. If you move often or cover multiple jurisdictions, a dedicated tracker with an evidence archive is usually easier to keep consistent.

Monitor FBAR exposure before filing season#

If you are a U.S. person with foreign financial accounts, set this up now, not when filing season is already on top of you.

- Set up: Run a monthly aggregate-balance check across all foreign accounts.

- Monitor: The FBAR trigger is whether aggregate foreign account value exceeded $10,000 at any time during the calendar year.

- Act: If filing is required, file FinCEN Form 114 electronically through BSA E-Filing. The due date is April 15, with an automatic extension to October 15 and no separate extension request. File FBAR separately from your federal income tax return.

From the day you open a foreign account, keep statements, opening documents, and balance evidence in one place. Confirm that you can substantiate account balances and account details without rebuilding records later. FBAR civil maximum penalties are adjusted annually for inflation, so verify current-year requirements before filing.

Reduce the PE facts you create#

PE risk turns on the facts of your day-to-day work, not contract wording alone. The practical control is to keep authority boundaries clear in both documents and practice.

- Set up: Use scope language for advisory, delivery, or support work. State that you do not sign contracts for the client and do not approve final commercial terms on the client's behalf.

- Monitor: Keep authority boundaries clear in practice. Final pricing, signatures, and binding commitments stay with a named client employee.

- Act: Escalate for country-specific tax advice if your role starts to look like local representation.

Practical guardrails include avoiding any setup that makes you look like the client's local office, the person who habitually negotiates final terms, or the person who can close deals. Be cautious about using a dedicated local workspace in ways that look like the client's fixed place of business.

HMRC guidance highlights two broad PE routes relevant here: a fixed place of business and dependent-agent authority to conclude contracts. It also distinguishes independent agents from dependent-agent PE cases, but treatment still depends on the facts.

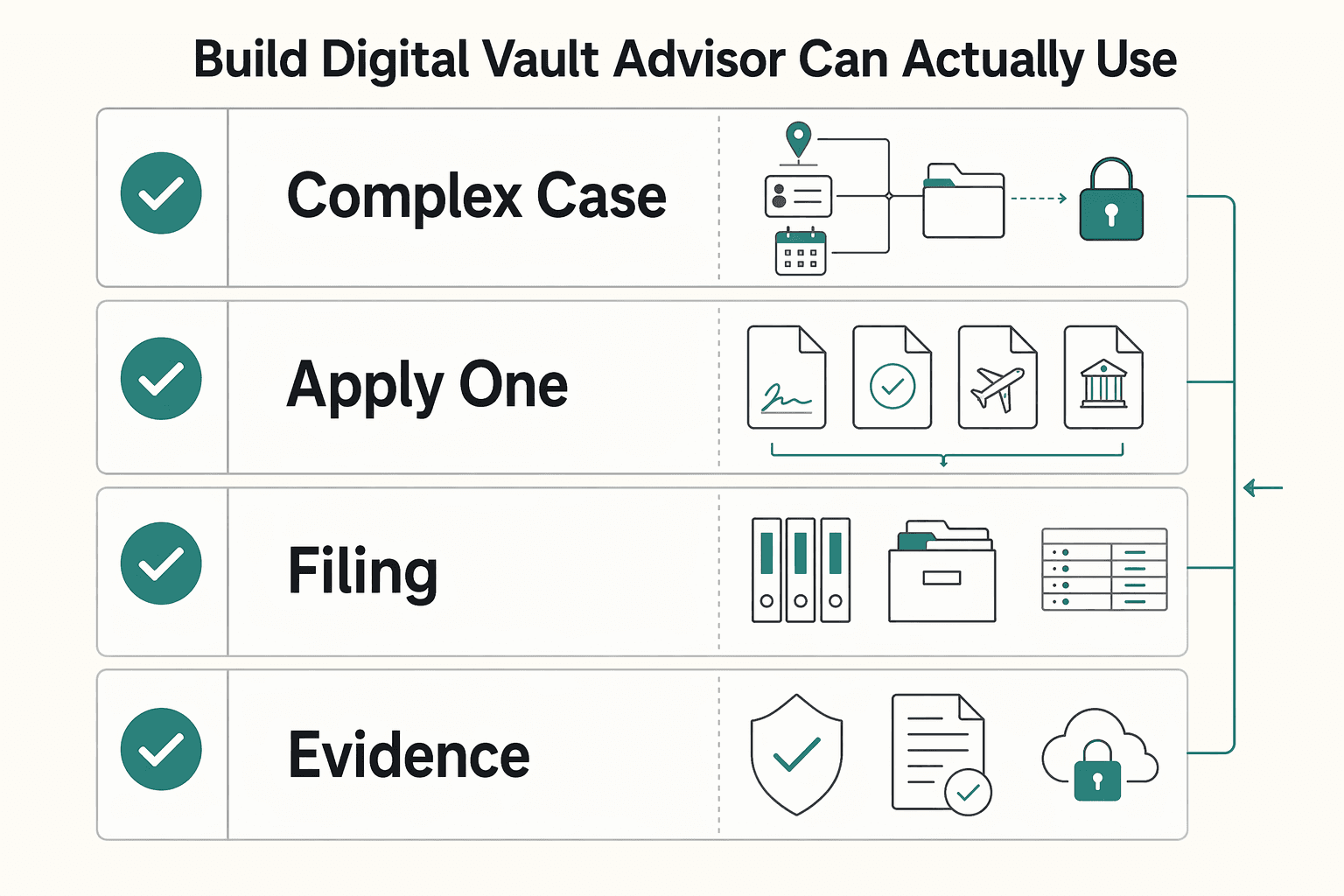

Build a digital vault an advisor can actually use#

A record system helps only if someone else can use it quickly under pressure, so use this checklist:

- Store records by year > entity/name > category.

- Apply one filename pattern, for example

2026-02-14_invoice_ClientName_4500_USD.pdf. - Keep contracts, amendments, invoices, receipts, bank statements, travel evidence, tax filings, FBAR confirmations, and residency-log exports together.

- Apply retention by record type: many IRS income-tax cases use a 3-year baseline, while FBAR records are generally kept for 5 years from the FBAR due date.

Run one handoff test: can an advisor find the signed contract, payment proof, travel support, and foreign-account records in 10 minutes without follow-up emails? If not, tighten the structure and naming until they can.

If you want a deeper dive, read GDPR for Freelancers: A Step-by-Step Compliance Checklist for EU Clients. Before taking on more cross-border work, centralize your residency-risk checks with the Tax Residency Tracker.

Tier 3: Achieve Ultimate Control Through Leverage#

Once operations and compliance are stable, the next job is leverage: make your offers easier to buy, protect your capacity, and use a small dashboard to correct course quickly.

Build an offer ladder that limits ambiguity#

Scope creep can start before delivery, when the offer is too vague to hold boundaries. A three-step offer ladder can help buyers enter at the right level and keep scope under control.

| Offer | What it includes | Boundary |

|---|---|---|

| Entry diagnostic | Assess, prioritize, and recommend next steps | Do not include implementation by default. |

| Core delivery offer | Fixed input, fixed output, fixed timeline, and fixed review limits | Price does not adjust if effort runs long, so you carry the cost and profit risk. |

| Ongoing option | Retainer agreement with explicit scope and procedure | Define included request types, request process, response windows, meeting limits, and out-of-scope work. |

Your entry offer is a diagnostic for buyers who know there is a problem but cannot define scope yet. Keep the promise narrow: assess, prioritize, and recommend next steps. Do not include implementation by default.

Your core delivery offer is productized: fixed input, fixed output, fixed timeline, and fixed review limits. In private freelance work, fixed-fee delivery can resemble a firm-fixed-price risk profile. Your price does not adjust if effort runs long, so you carry the cost and profit risk. Use this only when the work is repeatable enough to estimate with confidence. If scope is still unclear, route the buyer back to a diagnostic or use a custom model.

Your ongoing option is a retainer agreement with explicit scope and procedure. Define included request types, request process, response windows, meeting limits, and out-of-scope work. If you leave "access" undefined, delivery expectations and billing usually drift.

Before you publish any offer, create a one-page offer sheet and matching contract language with buyer fit, deliverables, exclusions, turnaround times, and acceptance criteria. Acceptance criteria define what "done" means, and that is a strong protection against work expanding beyond the original plan.

Choose the right service model for the job#

Match the service model to certainty, not to what sounds most attractive.

| Service model | Scalability | Predictability | Margin pressure | Operational complexity |

|---|---|---|---|---|

| Custom project | Low | Low to medium | High when scope changes | High |

| Productized offer | Medium to high | High if boundaries hold | Medium because fixed pricing keeps delivery risk with you | Medium |

| Recurring advisory | Medium | High on recurring revenue cadence, lower on incoming demand variation | Medium when access rules are loose | Medium to high |

If you cannot estimate scope, duration, or cost with reasonable confidence, treat that as a signal. Use custom or time-and-materials style work until you have enough repeat data to standardize.

Run a repeatable planning loop#

Capacity planning usually fails when it runs on optimism instead of actuals. Use one loop: set real capacity, filter work with acceptance criteria, and protect recovery and strategy time before the calendar fills.

- Set capacity from actuals and upcoming availability. Plan weekly and monthly using your verified numbers for

[weekly client delivery hours],[weekly admin/compliance hours],[weekly recovery time], and[monthly strategy time]. - Gate new work before you accept it. Accept work only when buyer fit is clear, deliverables are defined, completion conditions are explicit, and start timing fits available capacity.

- Protect recovery and strategy time as fixed calendar blocks. Do not run sustained 55+ hour weeks as your default operating mode.

- Check tax cash flow before committing large blocks. If you are self-employed and expect to owe $1,000 or more, estimated tax payments are generally required. Review reserves against Apr 15, Jun 15, Sep 15, and Jan 15, with weekend or holiday shifts in mind.

Use a compact dashboard that forces action#

A dashboard only matters if each number triggers a decision. Track a small monthly operator dashboard where every metric has a clear action.

- Offer economics: Compare estimated versus actual delivery effort by offer. Trigger: if one offer overruns twice, raise price, narrow scope, or tighten exclusions.

- Channel quality: Track source of inquiries and qualified-buyer conversion by channel. Trigger: if a channel produces low-fit leads for a full review cycle, reduce effort there and reallocate.

- Capacity strain: Track commitments against verified capacity and after-hours spillover. Trigger: if spillover repeats, push start dates, pause low-fit work, or change offer mix.

- Market signal: Track repeated requests from good-fit buyers you cannot serve yet. Trigger: if the same request repeats, invest in that skill or formalize a new offer.

That is what business intelligence looks like in practice: regular, data-driven reviews that surface problems early and force clear decisions.

For a step-by-step walkthrough, see Freelancer Transformation From Stressed Survivor to Strategic CEO.

Conclusion: From Managing Pain to Wielding Control#

The Pyramid of Control works only if each tier is operating in practice, not just sounding right in theory. The sequence matters too. Fix the first weak point that would break under pressure, then move up the stack. Use this readiness checklist to see which tier still needs work:

- Tier 1, operational drag: You use one recordkeeping system that clearly shows income and expenses, onboarding collects the correct tax form before work starts, and invoicing follow-up runs on a process instead of memory. For U.S. payees, that is usually Form W-9. For foreign individuals, Form W-8BEN. For entities, confirm Form W-8BEN-E is used instead of the individual form.

- Tier 2, compliance moat: You are tracking deadlines and exposure, not estimating from memory. If you are self-employed, account for annual filing and quarterly estimated-tax flow. Monitor day counts where residency thresholds apply, such as more than 183 days in Spain or 183 days or more in the UK. If you are a U.S. person with foreign accounts, review the FBAR trigger when aggregate value exceeds $10,000 at any point in the year.

- Tier 3, leverage: Your offer ladder, scope boundaries, exclusions, turnaround times, and acceptance criteria are documented. You compare estimated versus actual delivery effort by offer and act when one repeatedly overruns. If scope boundaries are unclear, control is still missing.

What to do next: fix one operational choke point this week, usually onboarding or invoicing. Add one compliance checkpoint, for example a quarterly estimated-tax review, an FBAR check before April 15 (automatic extension to October 15, if needed), and a travel-day review where residency thresholds apply. Then make one leverage move, such as tightening a diagnostic, productizing a repeatable service, or adding acceptance criteria to your retainer.

If those steps surface edge cases, check the FAQ before you execute. Related: The Anatomy of a 'Catastrophic' Freelancer Pain Point.

If you want your operations to match your strategy, review how Gruv for Freelancers supports invoicing, payouts, and compliance-ready records where enabled.

Frequently Asked Questions

What financial risks deserve your attention first?

Start with three separate risk types: tax residency, foreign account reporting, and client taxable-presence exposure. Set up one control for each this week, such as a dated travel log, year-to-date foreign account statements with maximum-value notes, and adviser review for scopes that could look like local representation. These risks sound related, but each needs a different control.

How should you operate if you want control, not constant cleanup?

Use a simple operating model with a weekly compliance review, standardized onboarding before work starts, and clear ownership for admin versus advisory work. When ownership is fuzzy, admin work expands until it starts causing deadline misses and avoidable risk. Keep the model visible and review it weekly, not only when something breaks.

How can you reduce the chance of accidental tax residency?

Reduce this risk by replacing memory with one record you can defend. Keep dated travel records, check them regularly with an adviser against applicable local rules, and review them before scheduling new travel. If your location history is incomplete, fix that first before adding more cross-border complexity.

What is FBAR, and why should you treat it as a live compliance item?

FBAR can apply when you are a U.S. person with a financial interest in or signature authority over foreign financial accounts and filing conditions are met. The trigger includes cases where the aggregate of maximum account values exceeds $10,000, including across multiple accounts. Value each account separately, keep a recurring compliance-calendar check, and document any currency conversion method you use.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

GDPR Compliance Checklist for Freelancers Working With EU Clients

Start by separating the decisions you are actually making. For a workable **GDPR setup**, run three distinct tracks and record each one in writing before the first invoice goes out: VAT treatment, GDPR scope and role, and daily privacy operations.

The Anatomy of a Catastrophic Freelancer Pain Point

You've seen the endless lists of familiar freelancer pain points: late payments, scope creep, inconsistent income, and the feast-or-famine cycle.

Why High-Earners Choose Freelancing for the Autonomy Premium

Freedom only pays off when control keeps pace. Freelancing happens project by project outside a single employer structure, so you need explicit rules for scope, pacing, and follow-through. Freedom without structure turns into chaos. Durable independence comes from controls you can repeat, not motivation spikes.