Quick Answer

Start with sequence, not speed: define how money and approvals will flow, then decide whether a Delaware C-Corp with Stripe Atlas fits your actual path. In this global saas founder blueprint, the practical order is operating model first, formation second, payment controls third, and reporting discipline throughout. A strong checkpoint is whether one planned sale can be traced from contract to collection to payout approval and monthly reporting without gaps.

How to treat Delaware C-Corp and Stripe Atlas as operating infrastructure, not a formation checklist#

A strong start for an international founder is less about filing fast than making the right decisions in the right order. This piece takes a practical, execution-first view: choose your structure with intent, test your payment motion early, and build records that still make sense once revenue, contractors, and buyers span borders.

The core question is simple: treat company setup as part of a broader operating decision, not the whole answer. Structure can matter, but it will not fix weak ownership records, unclear money movement, missing approvals, or inconsistent reporting. Those issues are what usually create avoidable surprises after first revenue, especially when you are selling across multiple regions.

This article is built around decision rules and checkpoints, not startup folklore. In practice, the order that matters most is straightforward: define the operating model before you add structure, decide whether your setup fits your actual path, then build payments, controls, and reporting in a way you can verify. An early checkpoint is whether you can state, in one sentence each, your initial customer segment, your payment collection path, and who approves payouts or refunds. If any of those answers are fuzzy, more setup usually adds noise before it reduces risk. A BI blueprint for early-stage SaaS founders makes a similar point: move from gut-feel decisions toward answering key business questions quickly and accurately with data.

The market lens matters too. One SaaS growth source notes that early validation in India can be harder because of payment behavior, expectations, and ROI cycles, and recommends aiming for the first 10 customers in the US, Europe, or Australia. That does not make one region universally better. It does mean your early market choice affects how quickly you learn whether buyers understand the problem, pay on time, and renew without heavy hand-holding. If feedback cycles are slow, clean setup will not save you.

You will see concrete operator detail throughout: verification moments such as checking whether invoices, payments, and payouts can be traced cleanly, and failure modes such as onboarding customers before your payout controls or reconciliation views are tested end to end. It also includes evidence hygiene: where core records live, how approvals are captured, and what you will want on hand when a bank, provider, or partner asks basic questions.

The goal is not to make your company look sophisticated on paper. It is to help you build a SaaS business that stays operable, explainable, and easier to trust as it grows. You might also find this useful: How to Set Up a US LLC for an Australian SaaS Founder.

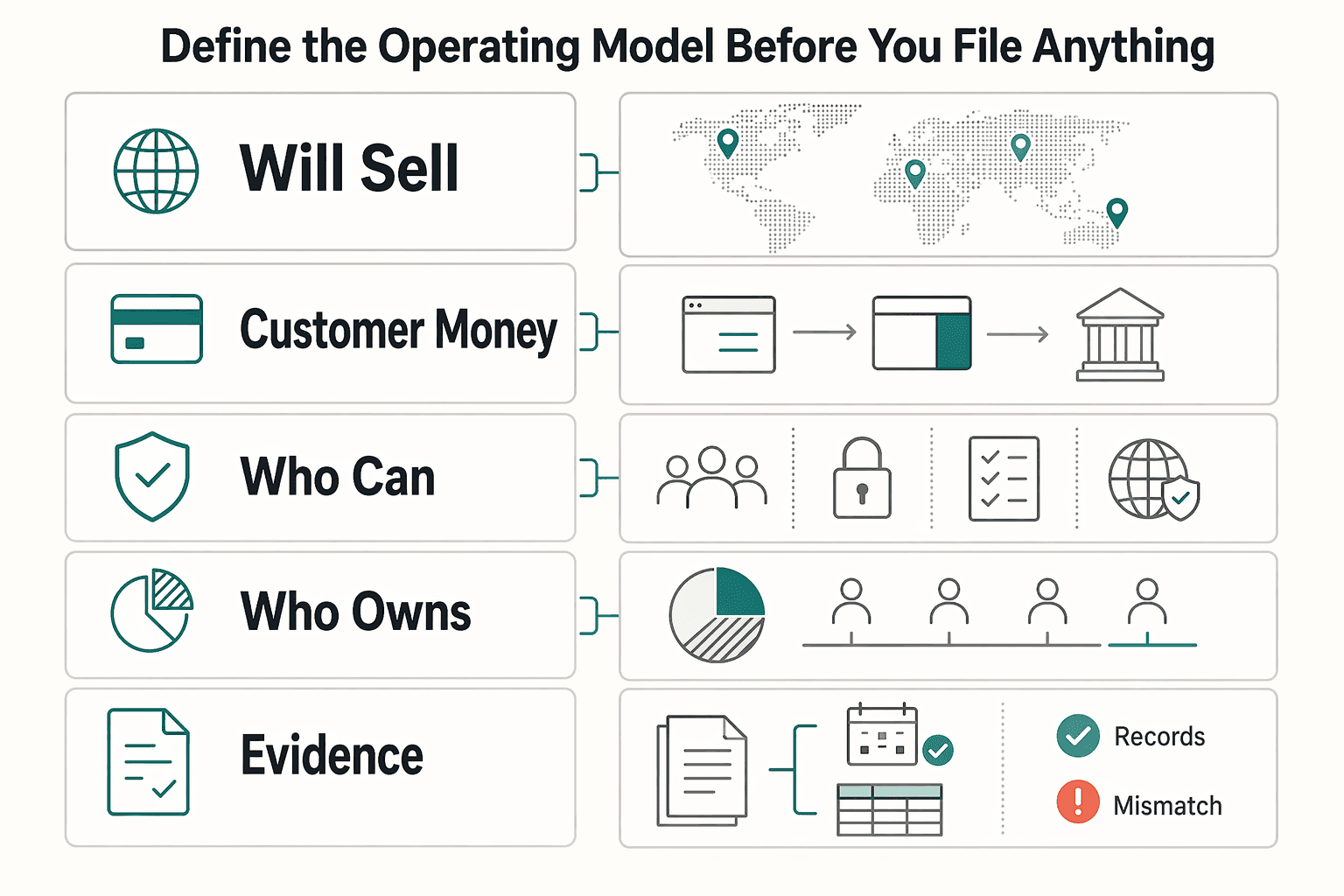

Define the operating model before you file anything#

Before you file anything, define the operating model. Here, that means clarifying legal structure, money movement, compliance controls, and reporting discipline before you optimize paperwork.

| Question | When |

|---|---|

| How you will sell | Before filing |

| How customer money will be collected | Before filing |

| Who can approve payouts or refunds | Before filing |

| Who owns monthly reporting | Before filing |

| Where core ownership and approval records will live | Before filing |

If you are considering a Delaware C-Corp and Stripe Atlas, treat formation as one step, not the full system. Before you file, you should be able to answer each question above in plain English.

Be explicit about your market posture too. A transatlantic model can support US expansion from day one, including strategic US beachheads, while keeping your operating center in Europe or another home market. The practical checkpoint is whether you can trace one planned sale from contract to collection to payout approval to reporting ownership without hand-waving.

Treat setup as staged risk reduction. Validate product and market first, then add the governance depth your path requires. If your likely path includes institutional capital, larger US buyers, or a future Series A, set C-Corp-grade governance expectations early. If not, do not confuse incorporation with operational readiness. For payment setup questions, see The Best Payment Gateways for SaaS Businesses.

Decide if Delaware C-Corp plus Stripe Atlas fits your case#

Choose this path when you need a Delaware-incorporated company now and are preparing for real operations. If your offer, customer segment, or payment motion is still unclear, the better answer is usually not yet.

The case here is narrow but practical: Stripe Atlas is presented as a way to start a company and get ready to charge customers, hire your team, and fundraise. Stripe also references the operational topic "Accepting payments and banking before your EIN arrives," which makes this more relevant after validation than during early idea testing.

| Option | What you are deciding | What this section can safely say | What needs separate analysis |

|---|---|---|---|

| Sole Proprietorship | Whether to sell personally while validating demand | This evidence does not rank it for investor fit, admin overhead, or cross-border credibility | Legal exposure, tax treatment, banking access, contract posture |

| LLC | Whether to use a company structure without committing to a Delaware corporation yet | This evidence does not support a hard investor-fit or admin-overhead conclusion | Tax treatment, ownership plans, hiring needs, conversion path |

| Delaware C-Corp | Whether to operate as a Delaware-incorporated company now and use Atlas for setup | Atlas is explicitly framed around starting a company and preparing to charge customers, hire, and fundraise; "Delaware" is the incorporation label | Ongoing filings, tax obligations, governance records, cap table discipline |

Stripe Atlas and Firstbase.io are formation decisions, not the whole operating model#

In the evidence for this section, only Stripe Atlas has grounded positioning. We do not have grounded feature, pricing, or process details for Firstbase.io here, so treat that comparison as separate diligence, not a settled conclusion. For a direct side-by-side, see Stripe Atlas vs. Firstbase.io: A Comparison for US Company Formation.

Use a hard not-now checkpoint#

If these answers are still moving, pause before you add complexity:

- What exact SaaS offer are you selling?

- Who is the first customer segment?

- How will they pay?

- Which entity will sign contracts?

- Who will own records after formation?

If you cannot answer those cleanly, delay setup and validate demand first. If you want a broader structure primer, read Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers.

Execute the first 90 days in the right order#

Treat the first 90 days as a staged roadmap, not a pile of parallel tasks. The pattern is simple: validate painful demand first, then execute each next step with a clear owner and definition of done.

A step-by-step SaaS MVP launch in about 90 days is a useful planning frame, not a rule every company must follow. If your setup work is moving but your customer signal is still weak, the order is wrong at this stage.

Start with demand signal, then scale execution#

The fastest way to waste those 90 days is to build before you confirm pain. Keep validation active while you handle setup so you do not mistake admin progress for market proof.

A practical operating checklist:

- Assign one owner per step and define what "done" means before work starts.

- Keep approvals and final documents in one shared location so handoffs stay verifiable.

- Run a full dry run of your real customer path before you treat onboarding as live.

- Continue pain-first validation during execution; examples like messaging 50 potential customers or running a $50 ad test for 10+ signups are heuristics, not benchmarks.

If you want a step-by-step walkthrough, see The Agency Scaling Blueprint: From Solo Freelancer to Hiring Your First 5 Global Contractors.

Build payment operations that are audit-ready from day one#

Build this layer around what is verified now: SaaS billing automation for invoicing, subscription management, and revenue recognition. Treat wallets, FX conversion, Virtual Accounts, and compliance-gated payouts as confirm-first items until you have direct proof for your setup.

| Founder need | What is supported now | What to verify before relying on it |

|---|---|---|

| Invoicing and collection | Billing automation for invoicing, subscriptions, and revenue recognition | Invoice states, collection statuses, export format, and approval controls |

| Wallets, FX conversion, Virtual Accounts | Verify with your payment provider | Availability by entity, market, currency route, reference fields, and exports |

| Compliance-gated payouts | Verify with your payment provider | Approval rules, payout statuses, review logs, hold/release behavior, and exception handling |

Keep your review focused on the event chain, not product copy: request created, provider reference returned, ledger posting recorded, export produced, then status updates written back to your records. For retries, check duplicate protection. For async updates, check webhook (or equivalent machine-readable) delivery, retry behavior, and logging.

If you expect cross-border contractor payouts early, put policy gates and payout status handling in place before volume ramps. Define who approves, which statuses trigger action, what is held for review, and where the final record is stored.

One caveat: this section's sources do not establish rail or treasury availability in the United States, Europe, or Australia. Coverage can vary by market or program, so confirm your entity, route, and export requirements in writing before you depend on them.

We covered this in detail in The European Content Creator's Blueprint: From Registering in Estonia to Invoicing Global Brands.

Create the compliance and tax evidence pack investors expect#

Build this pack so you can answer one question quickly: can your team produce accurate GAAP or IFRS financial statements and explain how money moved? That standard usually becomes critical once you start seeking outside investment, because cash-based financials alone are not enough.

| Record set | Why it belongs here | What to keep |

|---|---|---|

| Verification/compliance records your providers require | Shows key accounts and workflows were approved through documented checks | Status records and timestamps from the provider |

| Tax profile and tax-document workflow records | Preserves how counterparties were configured in your systems | Current profile data, status history, and change logs |

| Accounting and reconciliation exports | Supports close, reporting, and investor diligence | The exact exports used for accounting and the mapping logic you relied on |

For international founders, process evidence matters more than memory. If a provider has W-8 or W-9 collection paths enabled, keep the status trail, timestamps, and the exact export used downstream. Keep an audit trail of who changed key settings and when.

Revenue recognition is part of this same evidence standard. For SaaS P&L reporting, recurring revenue and professional services revenue need revenue recognition support; cash-only reporting may still help with tax prep, but it does not show investors the full economics of the business.

This is what real risk reduction looks like before a major raise: reporting discipline, traceable records, and a pack that holds up when someone asks hard follow-up questions.

Need the full breakdown? Read The Onshore-Offshore Blueprint: Combining a US LLC with a BVI Company for Asset Protection.

Choose early markets with explicit tradeoffs#

Choose your first market for learning speed and repeatability, not for size alone. Treat the United States, Europe, Australia, and India as discovery environments. Test your motion with real customer interviews, then update your decision as the evidence improves.

Use a market scorecard you can defend#

Score each market against the same criteria for your specific SaaS offer, then revise after interviews, demos, and first proposals.

| Market | Willingness to pay | Sales cycle speed | Support burden | Compliance friction |

|---|---|---|---|---|

| United States | Which budget owner feels this pain, and do they already pay for adjacent tools? | Does a demo move to a clear trial or pilot next step? | How much onboarding, integration, and success support is expected early? | Which buyer-side security, vendor setup, tax, or contracting checks appear before close? |

| Europe | In your first target countries, is the pain urgent enough to fund now? | Are you running one country-specific motion or treating Europe like one market? | How much localization, documentation, and timezone coverage will be required? | Which pre-close requirements typically block progress? |

| Australia | Are buyers signaling urgency or only curiosity? | Do discovery calls convert into defined next steps quickly? | Can your team support customers in-region without overextending? | Are account setup and contracting workable with your current operations? |

| India | Is the problem treated as mission-critical or optional? | Do prospects move forward after discovery, or stay in evaluation? | Will implementation and enablement dominate early delivery? | Do billing, procurement, or approval workflows slow first revenue? |

Filter out weak signals early#

Positive calls are not enough. Buyers are overloaded by AI positioning, so interest without a concrete next step is weak validation.

Pressure-test delivery model risk too. Some teams win with embedded, highly customized work (for example, forward-deployed engineer style support), but that approach is not a universal scaling playbook. If early wins depend on heavy customization, treat that as an explicit tradeoff in your market choice.

Narrow before expanding#

If payment behavior or ROI timing is still unclear, prioritize faster-feedback segments before broad expansion. After each interview or demo, capture the buyer role, core pain, expected payoff, blockers, and exact next step. If that evidence is not comparable across your target markets, keep narrowing until it is.

| What to capture | When |

|---|---|

| Buyer role | After each interview or demo |

| Core pain | After each interview or demo |

| Expected payoff | After each interview or demo |

| Blockers | After each interview or demo |

| Exact next step | After each interview or demo |

Run lean BI without losing control#

Keep early BI lean. Use it to answer a small set of key business questions fast enough to make decisions, not to produce more dashboards. If a metric does not change a product, pricing, or market decision, treat it as noise.

| Risk | Question |

|---|---|

| Product risk | Where do users stall before first value, and which behaviors indicate real usage? |

| Market risk | Which segment, country, or buyer type moves forward with the least friction and clearest next step? |

| Scale risk | Which channels, plans, or customer profiles stay healthy without heavy manual support? |

Define a short core funnel you can compare week to week, then keep definitions stable. Track only the steps that show movement from initial interest to meaningful use, paid conversion, and early repeat usage. For each step, assign one owner, one calculation method, and one source of truth you can verify quickly from product events, invoices, or payment status.

Keep the work tied to the risk you are managing. Keep governance simple: one weekly metrics review, one monthly operating review, and explicit owners for each core metric. Weekly, focus on movement, broken instrumentation, and immediate decisions. Monthly, check whether your current metrics still match your stage and PMF signal.

The usual failure mode is dashboard sprawl before process discipline exists. Lean BI works when every metric leaves a clear trail: owner, anomaly, decision, and next check. Related reading: The 'Mental Game' of Freelancing Blueprint: From Imposter Syndrome to Confident CEO.

Conclusion#

The path that holds up is not "incorporate and hope." It is sequence and proof. Pick the right structure for your likely path, install money and compliance controls early, verify that each transaction can be traced, and only then push for speed.

A legal and operational setup can be a strong starting point if your trajectory points toward specific buyers, investor expectations, or future fundraising. But it is still only a starting point. The durable part is what happens after formation: clear ownership records, tested payment and payout handling, clean reconciliation, and a review cadence that catches problems while they are still small.

That is the standard worth keeping. Before you call your setup done, make sure you can trace one invoice through payment status, provider reference, payout outcome where relevant, and the ledger record that explains it. Keep the evidence that proves those steps were configured and approved, including the settings, onboarding approvals, exports, and screenshots you relied on. One avoidable risk is taking live revenue before those checks exist, then discovering later that payout states, reconciliation, or status ownership were never defined clearly enough.

The market side matters just as much as the paperwork. One SaaS growth source recommends targeting the United States, Europe, or Australia for the first 10 customers, with the caution that payment behavior, expectations, and ROI cycles can make early validation in India harder in some cases. That is not a universal rule, but it is a useful decision test. If your first target market makes it slow to prove value or collect clean signals, favor a segment or geography that gives faster feedback before broad expansion.

That advice lines up with a wider shift in SaaS thinking away from aggressive expansion and toward efficiency and sustainability. In practice, that means fewer assumptions, tighter checkpoints, and less tolerance for messy back-office work you plan to "fix later." Product-market fit remains a critical factor, but you do not help yourself by hiding weak fundamentals under a polished company setup.

So use this as an execution map, not a promise that one structure or provider solves the whole problem. Choose the route that fits your actual business, verify each step against your exact country and program reality, and expand only when your records, controls, and customer learnings stay coherent under pressure. This pairs well with our guide on Delaware C-Corp vs Wyoming LLC for Your Next Growth Stage.

Frequently Asked Questions

What is a global saas founder blueprint in practical terms?

It is an operating sequence that moves you from intuition to answerable business questions: test your core hypothesis with an MVP, then build just enough BI to answer key questions quickly and accurately. One early BI guide describes this as a 6-step move from zero analytics to data-driven decision making. In practice, it is more about disciplined learning and repeatable decisions than adding more reporting.

Why would an international founder choose a Delaware C-Corp with Stripe Atlas?

Separate setup decisions from validation work: an MVP is a learning tool, and early traction depends on proving demand before over-indexing on structure.

What should I do first in the first 90 days to avoid compliance rework?

Start by validating your core hypothesis with real users, then define a small set of business questions you will answer with data every week. Put lightweight measurement in place early so decisions are not driven only by gut feel. Keep early sales founder-led and authentic, since trying to sound overly salesy can hurt early traction.

Which mistakes create the biggest delays in cross-border payments and payouts?

These sources do not provide specific evidence on cross-border payout operations. The broader failure patterns they do highlight are poor market choices, weak data systems, and weak execution discipline. If your team cannot answer core business questions reliably, delays and rework are more likely.

What are the minimum BI metrics I should track before Series A?

There is no universal required list in these sources. A practical minimum is the smallest set of metrics that helps you test your core hypothesis and answer key business questions accurately. If a metric does not inform a decision, it is probably not part of your minimum yet.

Which parts of setup and compliance vary by country or program, and how do I confirm safely?

Treat jurisdiction requirements as case-specific, and confirm them through official program documentation and qualified local advice before making commitments.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- congress.gov/committee-report/111th-congress/house-report...trusted

- iese.edu/media/research/pdfs/ESTUDIO-137.pdftrusted

- publishing.vt.edu/books/33/files/b85e4a8e-a61c-4878-955c-d5e34...trusted

- sec.gov/Archives/edgar/data/1804468/0001493152250044...trusted

- sec.gov/files/ctf-written-input-private-market-token...trusted

- stripe.com/resources/more/what-is-a-go-to-market-strate...trusted

- a16z.com/the-palantirization-of-everythingexternal

- blog.startupstash.com/the-30-day-cash-out-blueprint-how-to-validat...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

Stripe Atlas vs Firstbase.io for US Formation Without Compliance Surprises

You can make this decision fast if you compare execution risk, not launch-day polish. Use one lens from start to finish and verify your assumptions before you pay.

The Best Payment Gateways for SaaS Businesses

**Choose your gateway stack by cashflow risk first, then optimize for features and price.** If you want the best payment gateway for SaaS, start where money can stall, not where brand buzz is loudest. You are the CEO of a business-of-one, which means a payout delay or a payment hold is not an inconvenience. It is an operating event.