Quick Answer

By December 31, a U.S. expat freelancer should have a filing-ready file with reconciled income records, foreign tax support, a detailed travel calendar, a clear FEIE or FTC working position, and a list of issues to escalate. The checklist starts with confirming you still must file on worldwide income, then organizing source records, separating income and tax lanes, and checking related account, state, and timing issues early.

Start here with the year-end outcome you need#

Your year-end target is filing readiness. By December 31, you want a complete file for your U.S. federal return, not a last-minute chase for documents. For a globally mobile freelancer, the hard part is usually proving what happened, choosing the likely FEIE or FTC lane, and spotting the facts that need professional review.

Define success like an operator#

A filing-ready outcome has three parts:

- Complete, supportable records.

Your income, payments, and foreign tax documents should tie to the amounts you plan to report. If FTC is in play, Form 1116 is prepared by income category and reported in U.S. dollars, so organize your records that way.

- A clear FEIE vs. FTC working position.

FEIE applies only if you are a qualifying individual with foreign earned income, and you still file a U.S. return reporting that income. If you are leaning FEIE, your file should already show whether you are relying on the Physical Presence Test or the Bona Fide Residence Test.

- Explicit escalation triggers.

If travel days are unclear, residency facts conflict, or foreign tax support is incomplete, escalate early instead of forcing a self-serve answer.

What this checklist is built for#

This checklist is for freelancers and consultants with cross-border, mixed-income records. The goal is to separate and document items early so classification does not happen under deadline pressure.

The IRS rule that sets the tone#

Treat year-end as a proof exercise under IRS rules. If you are testing FEIE through physical presence, the threshold is 330 full days during a 12-month period, and a full day means 24 consecutive hours from midnight to midnight. The 330 qualifying days do not need to be consecutive. Missing the minimum count fails the test regardless of the reason.

If you are testing FEIE through bona fide residence, keep the guardrail in mind. Living abroad for one year does not automatically make you a bona fide resident. The determination depends on your facts, and the uninterrupted period must include an entire tax year, January 1 through December 31.

What "ready" looks like by December 31#

By year-end, your folder should include:

| Item | Requirement |

|---|---|

| Complete income log | Tied to source documents |

| Foreign tax payment support | Can be traced, grouped by income category, and reported in U.S. dollars |

| Travel calendar | Detailed enough to test FEIE eligibility |

| FEIE or FTC memo | States your likely FEIE or FTC lane and why |

| Unresolved issues list | To take to a qualified advisor |

Practical checkpoint: if you expect to use Form 1116, verify now that each foreign tax amount has support and is grouped correctly. Each Form 1116 uses only one income category box.

Lock in the non-negotiables before optimization#

Lock in your filing obligation first. If you are a U.S. citizen or resident abroad, start from the rule that you generally must file U.S. returns on worldwide income, then test your facts before you optimize anything.

Set the filing posture first#

Use this order:

- Confirm your status up front (U.S. citizen abroad vs. resident abroad).

Do not build decisions on the wrong posture. The core question is whether you are a U.S. citizen or resident abroad whose filing obligations you must test under U.S. rules.

- Run the must-file check before exclusions or credits.

Use the filing requirements table in chapter 1 of Publication 54 as your checkpoint. It keeps the rest of your plan from being built on a bad assumption.

- Apply the gross-income test correctly.

For filing-requirement purposes, treat as gross income any income you may later exclude as foreign earned income or a foreign housing amount. Do not remove those amounts too early and conclude you do not need to file.

Exclusion or credit planning comes after this step. It does not replace it.

Don't build on treaty assumptions#

Do not assume that foreign filing, foreign tax payment, or a treaty lets you skip the U.S. filing check. Confirm whether you must file under IRS rules first.

If you cannot clearly state your status and the Publication 54 chapter 1 table you used, pause and fix that before moving into exclusion or credit analysis.

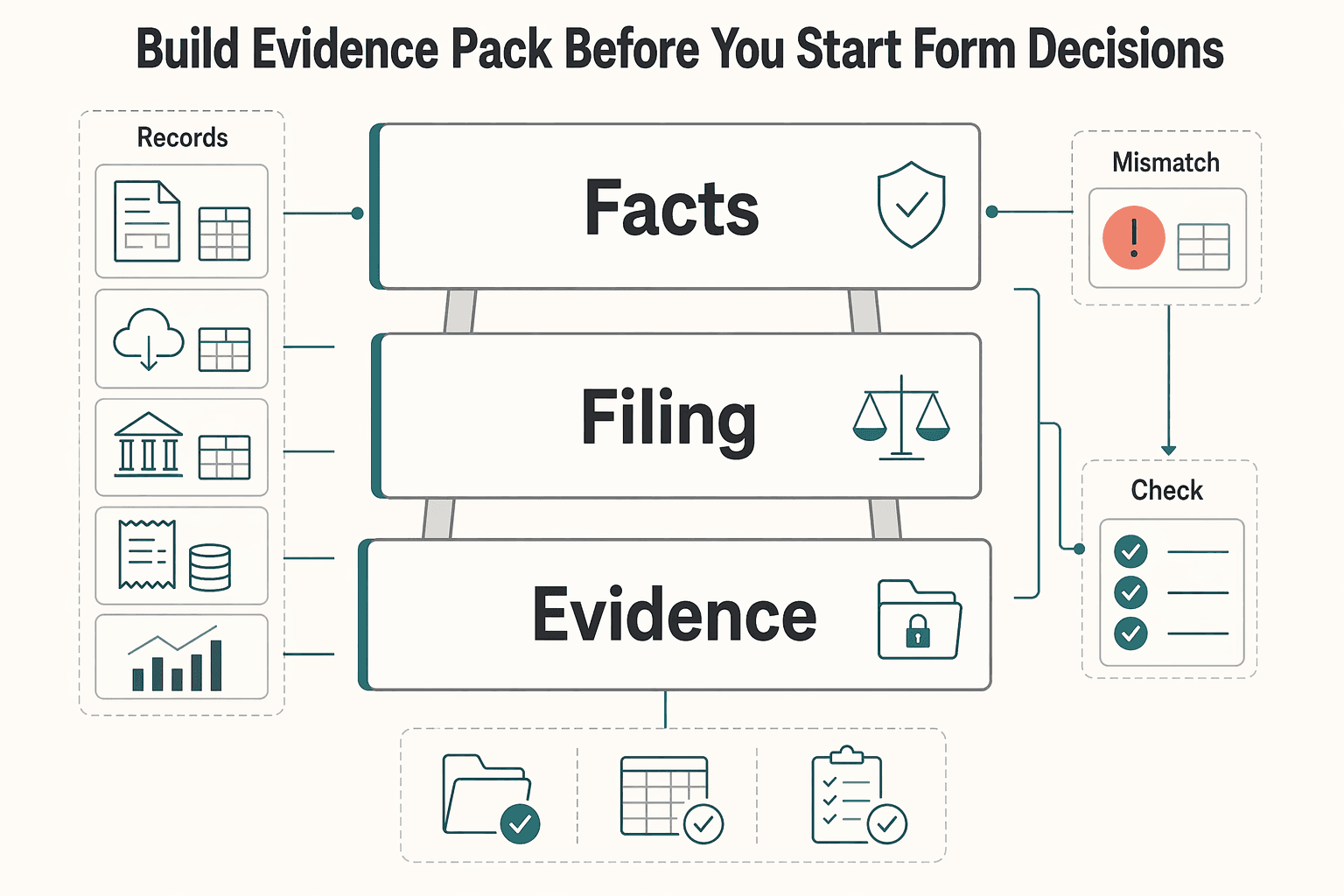

Build the evidence pack before you start form decisions#

Build the evidence pack first, then choose forms. If you pick Foreign Earned Income Exclusion (FEIE) or Foreign Tax Credit (FTC) too early, you risk forcing facts to fit a position. Also remember: claiming FEIE still means filing a U.S. return that reports the income.

Start from source records, not memory summaries. Useful records can include client invoices, platform payout exports, bank exports, foreign tax receipts or assessments, and investment statements. The output from this step is one audit-ready folder with source documents, USD conversion notes, and a missing-items list.

Map records to the claim they may support#

Use this three-lane sort before touching forms:

| Lane | Records | Supports |

|---|---|---|

| Earned income lane | Invoices, contracts, payout reports, and matching bank receipts | Define income you can substantiate as earned income and separate it from transfers or reimbursements |

| Foreign tax lane | Tax assessments, withholding statements, payment confirmations, and receipts | FTC analysis and Form 1116 |

| Accounts and investments lane | Bank and brokerage statements, including non-U.S. accounts | Keep separate so account and investment records do not get mixed into earned-income and FTC analysis |

Do that sort once, early, so account data does not get mixed into earned-income and FTC work later.

Build FEIE support before assuming FEIE#

If FEIE is in play, collect evidence for the test itself. For the Physical Presence Test, the standard is 330 full days in a 12 consecutive months period, and a full day is 24 consecutive hours. Use a real travel calendar with supporting records.

Missing the 330-day minimum fails this test, including common disruptions like illness, family problems, vacation, or employer orders. If you may rely on bona fide residence, keep proof of an uninterrupted foreign residence period that includes an entire tax year. Living abroad for about a year alone is not enough.

Make Form 1116 support usable#

For each foreign tax amount you may claim, make sure the support is traceable and reportable in U.S. dollars. Form 1116 also requires category-specific reporting, so use a separate form for each income category and check one category box per form.

If a tax payment cannot be tied to the relevant Form 1116 income category, or cannot be converted to USD for reporting, move it to the missing-items list now.

Verification checkpoint. Before leaving this step, confirm that every foreign tax payment you may claim has traceable support that is usable for Form 1116.

For a step-by-step walkthrough, see The 'First Year Election' for US Tax Residency: A Deep Dive.

Reconcile your income streams before year-end close#

Before you start return prep, reconcile income into clear lanes so you can support FEIE and FTC analysis with records, not memory. Keep earned income, foreign tax support, and account or wallet movements separate from the start.

Reconcile income by source, not by bank balance#

Use a revenue log as your master record. Bank feeds are supporting evidence, but they often combine income and non-income movements. Track receipts in clear buckets:

- client work and project invoices

- retainers or prepayments

- platform payouts

- investments

- other account or wallet movements

For client work and retainers, record both dates when they differ: when the work was performed and when payment was received. For FEIE, income is considered earned in the year you do the work, even if paid later. If you are cash-basis, you still report income in the year you receive it. FEIE does not remove the need to file a U.S. return reporting that income. That timing check helps you catch internal mismatches before you make form decisions.

Keep non-service activity in a separate lane unless it is clearly tied to earned service income. If a transaction is unclear, mark it unresolved and keep the source export.

Use this order of operations#

- Build the revenue log first

Match invoices, contracts, payout statements, exchange exports, and bank receipts. Aim for one line per economic event, not one line per bank movement.

- Build the foreign tax paid log second

Tie each foreign tax amount to the related income item or income bucket. If you file Form 1116, use a separate form for each income category and check only one category box per form.

- Convert to U.S. dollars last

Form 1116 generally requires U.S.-dollar reporting. Converting only after matching income and tax records makes final numbers easier to trace back to source documents.

Catch failure modes early#

Watch for reconciliation errors such as:

- double-counting the same economic event, for example treating a platform payout and its bank deposit as two revenue events

- missing source records

- unclassified wallet movements

If a movement cannot be tied to an invoice, payout report, investment statement, or wallet export, stop and classify it before you continue.

Tie each item to its filing lane#

By year-end, each line should map to the lane it may support. Service-income items may support FEIE. Foreign-tax items may support FTC analysis and Form 1116. Keep those lanes separate even when they relate to the same client work.

If FEIE under the Physical Presence Test is in play, timing detail is critical. Qualification depends on 330 full days during any 12 consecutive months, and a full day is 24 consecutive hours. If 330 full days are not reached, the test is not met regardless of reason. Your records should clearly show when work happened, when payment was received, and which tax year each amount falls into.

Choose FEIE or FTC with explicit decision gates#

Choose your first lane based on what you can prove now, not what feels easier at filing time. A practical starting point is FEIE when your eligibility facts are clear, and FTC when your foreign tax records are clearer.

| Practical criterion | Evaluate FEIE first when | Prioritize FTC analysis first when | What to verify now |

|---|---|---|---|

| Core gate | Your FEIE eligibility is clear under the Physical Presence Test or Bona Fide Residence Test | You have foreign tax paid with strong records | For FEIE, confirm 330 full days during any period of 12 consecutive months, or facts supporting bona fide residence for an uninterrupted period that includes an entire tax year. For FTC, confirm each tax amount ties to the related income category on Form 1116. |

| Income shape | Most of the file is foreign earned income | You have multiple income categories | Separate foreign earned income from other categories before deciding. Form 1116 requires a separate form by category, and only one category box per form. |

| Documentation burden | You can support your day count and foreign earned income with records | You can support foreign taxes paid with traceable records | For FEIE, align your travel calendar and work dates. For FTC, keep payment proof and report amounts in U.S. dollars, except where Form 1116 Part II specifies otherwise. |

| Timing sensitivity | Your 12-month day count or full-year residence pattern is already established | Your tax records are complete but FEIE qualification is still uncertain | A full day for Physical Presence is 24 consecutive hours from midnight to midnight. If only part of the year qualifies for FEIE, the maximum exclusion must be adjusted by qualifying days. |

Use a simple if then rule#

If foreign tax paid is well documented, start with FTC analysis on Form 1116. If FEIE eligibility is clearly met and your file is mostly foreign earned income, evaluate FEIE first.

The Physical Presence Test can be a cleaner FEIE gate because it is based on time abroad, not intent. It is also strict: miss 330 full days for any reason and that test fails. If you are using the Bona Fide Residence Test, expect a more fact-specific analysis. Living abroad for one year by itself does not automatically establish bona fide residence.

Know the tradeoff before you commit#

FEIE can reduce current U.S. taxable income for qualifying individuals with foreign earned income, but you still file a U.S. return reporting that income. For 2025, the maximum FEIE is the lesser of foreign earned income or $130,000 per qualifying person, and partial-year qualification requires a qualifying-day adjustment. For 2026, the maximum exclusion is $132,900 per person. If housing exclusion is in play, compute it first because FEIE is limited afterward.

FTC may be the more practical lane when your foreign tax documentation is already strong. The tradeoff is practical: weak category mapping or missing payment support can make Form 1116 prep harder.

What remains unknown until you have full facts#

Escalate before committing to FEIE or FTC if any of these are still unclear:

- exact travel-day count, including whether each claimed foreign day is a full 24 consecutive hours

- residency pattern, especially if relying on the Bona Fide Residence Test

- income mix across foreign earned income and other income categories

- foreign tax support that does not tie cleanly to related income items

- whether any claimed physical-presence days could be disqualified (for example, time in a foreign country in violation of U.S. law)

If one lane depends on assumptions and the other depends on documents, start with the document-backed lane. If FTC is that lane, continue with A Deep Dive into the Foreign Tax Credit (Form 1116).

If your FEIE vs FTC path is still borderline, run a quick scenario in the FEIE calculator before locking your filing lane.

Check foreign account and asset reporting exposure#

Once you have the income side organized, check reporting obligations that may still apply. Treat Form 8938 and FinCEN Form 114 (FBAR) as separate checks. Filing one does not automatically satisfy the other.

Form 8938 is attached to your annual U.S. federal tax return and follows that return's due date, including extensions. FinCEN Form 114 is a separate filing obligation, so keep it on its own compliance track.

Build one account inventory first#

Before testing thresholds, build one account file you can use as a starting point for Form 8938 and FBAR review. For each foreign account, capture details such as:

- Account owner or control details.

- Financial institution and account identifier.

- Maximum value during the year, not only the year-end balance.

- Whether the account was closed during the tax year.

This aligns with Form 8938 checkpoints, including maximum value and whether foreign deposit or custodial accounts were closed.

Run a Form 8938 checkpoint without guessing thresholds#

Form 8938 may apply when the total value of specified foreign financial assets is above the threshold for your profile. IRS guidance includes financial accounts maintained by a foreign financial institution in that asset scope.

Quick screen only: IRS materials show an aggregate-value trigger of $50,000 for certain taxpayers. Form 8938 instructions show $50,000 at year-end or $75,000 at any time for certain specified domestic entities. Use the threshold set that matches your actual filing facts.

If you are not required to file an income tax return, you do not need to file Form 8938, even if asset values are above a threshold.

Keep FBAR timing as a separate check#

Do not fold FBAR into return prep and assume it is covered. Keep FinCEN Form 114 on its own track and confirm timing close to filing. Relief can be event-specific, for example an additional extension notice dated 10/11/2024.

Run state residency exit checks for high-risk states#

Treat state residency as an open compliance question until your records support a clear exit narrative, especially if your prior state was California. For New York, apply the same caution without assuming unsupported thresholds. Federal expat benefits may not, on their own, close state filing risk when material state ties remain.

For California, use a facts-and-circumstances file, not a single indicator. California treats residency as a factual determination, and the FTB does not issue written residency opinions for a specific period. Incomplete or inconsistent records can increase the risk that you will need to defend your position later.

California needs a documented timeline#

California distinguishes among resident, part-year resident, and nonresident status, and the tax outcome changes with that status. Part-year residents are taxed on worldwide income during the resident period, while nonresidents are taxed on California-source taxable income.

If you moved abroad midyear, confirm both:

- When your resident period ended.

- Whether you still had California-source income afterward.

If you physically performed services in California after moving, that compensation can still be California-source income, and Form 540NR can remain relevant. A practical check is to reconcile travel records and work logs using California's sourcing method: CA Workdays / Total Workdays = % Ratio, then % Ratio x Total Income = CA Sourced Income.

New York deserves the same caution, without unsupported specifics#

For New York, do not assume a day count or one document change is your full exit analysis. Use the same evidence discipline here: dated move records, a coherent timeline, and work-location support.

If you are leaning on day-count assumptions, read 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

Evidence quality triage#

Use this as an illustrative triage tool, not a state-issued checklist.

| Proof quality | What your file might include | Risk signal |

|---|---|---|

| Strong | Dated move timeline, housing records aligned to the move, travel logs, and work-location records that match your filing position | Better support for a clear residency narrative |

| Weak | Address changes, rough day counts, or partial records that do not clearly match where you lived and worked | Higher risk in a facts-and-circumstances review, including with FTB |

| Missing | No dated move proof, no work-location support, no explanation for California trips or ongoing ties | State filing risk may remain open |

Year-end decision rule. If old-state ties are still material, treat state filing as an active risk even when federal positions look strong. California residents are taxed on all income regardless of source, and part-year residents are taxed on worldwide income during their resident period.

Make one explicit year-end call: either your evidence supports a clean state exit, or it does not. If it does not, preserve records now and escalate before finalizing your return position.

Set your filing calendar and extension checkpoints#

Once your facts and exposure areas are clear, put dates around them. Set your federal timeline from current IRS guidance each year, then build your internal deadlines ahead of those dates. Use the Form 2555 instructions, including When To File and Special extension of time to file, as your live source, not last year's calendar. If you are abroad, review current IRS extension guidance and confirm eligibility before assuming an extension applies.

Put these checkpoints in sequence#

- Lock baseline dates from current IRS guidance

Confirm timing from current IRS guidance and the Form 2555 instructions, then set your own milestones earlier so review and corrections are not rushed.

- Complete the evidence pack before choosing FEIE or FTC

Organize records so either path is supportable. For Form 1116, keep amounts in U.S. dollars, split by income category, and organize multi-country taxes by country or territory for separate lines or columns where required.

- Make the FEIE vs FTC decision before drafting

If you are leaning FEIE, calendar the eligibility check itself. Under the Physical Presence Test, you need 330 full days in a 12-consecutive-month period, and a full day is 24 consecutive hours. If you do not reach 330, that test is not met. For the Bona Fide Residence Test, one year abroad alone does not automatically establish status, and the period must include an entire tax year.

- Run separate reporting prep on its own track and set reviewer handoff

Prepare related reporting data early as its own workstream, then set a reviewer handoff date with a short memo: chosen FEIE or FTC path, open questions, and the IRS timing guidance used. This keeps separate reporting steps from collapsing into last-minute work.

Define escalation triggers before mistakes compound#

Escalate before you draft final forms whenever facts conflict, filing scope expands across Form 1116 categories or countries, or FTC eligibility and election choices are unresolved.

- Your FTC file is not internally consistent

Escalate if treaty re-sourcing treatment is unclear or your support is incomplete for Form 1116. Form 1116 requires separate handling by income category, only one category checkbox per form, separate country or territory lines or columns when relevant, and U.S. dollar reporting, except where Form 1116 says otherwise. Use a simple pre-draft check: source support, conversion support, correct category, and a clear creditability call under the IRS four-test framework.

- Eligibility and election choices may conflict

Escalate if you excluded foreign earned income or housing costs and are also considering an FTC on taxes tied to that excluded income. The IRS states you cannot claim both on the same excluded income, and a conflict can cause one or both elections to be treated as revoked.

- Creditability is still uncertain after initial review

Escalate when a foreign tax type is ambiguous, even if the four FTC tests appear to be met. IRS guidance notes that some foreign taxes are non-creditable despite meeting the basic tests, so unresolved tax-type questions should be reviewed before filing.

Build a filing-ready handoff packet your tax pro can use fast#

A filing-ready packet is a one-page decision summary plus linked evidence folders, so your preparer can verify facts quickly instead of reconstructing them.

Put the decision summary on one page#

Keep this page readable in two minutes. It should cover:

- Status and location facts

Your filing status context, countries of residence during the year, and move dates that could affect the analysis.

- Income mix

Income grouped into earned, investment, and other relevant buckets, plus where foreign taxes were paid and on which income type.

- Preliminary FEIE or FTC direction

State your current direction and support without forcing a final conclusion from incomplete facts. For a Foreign Earned Income Exclusion (FEIE) path, note whether you are testing under the physical presence test or bona fide residence test. If using physical presence, list the exact 12 consecutive months and your count against 330 full days, with 24 consecutive hours per full day. If using bona fide residence, note whether your uninterrupted period includes an entire tax year, January 1 through December 31 for calendar-year taxpayers.

If you are also evaluating a foreign housing exclusion, flag it separately, since that amount is figured first and reduces income available for FEIE.

Add a forms map, not just a folder dump#

Add a simple forms map with owner or responsible-party notes so key forms and evidence are visible before document review:

- Form 1116 for expected FTC analysis. Organize inputs by income category, because each category uses a separate Form 1116 with one category box checked per form. If taxes were paid to multiple countries or territories, prepare separate country lines or columns as needed. Prepare amounts in U.S. dollars except where the form says otherwise.

- Any additional reporting forms your tax pro flags. For each related account or asset, note the owner or responsible party and the supporting file used for confirmation.

Verification rules your future self will thank you for. Your packet is ready only when a reviewer can trace each figure without guesswork.

- Every number has source support.

- Every source follows one filename convention.

- Every unresolved item has an owner and a date.

Include the reference docs that reduce ambiguity#

Include the Publication 54 extracts you relied on and your prior-year filing notes. If FTC work is likely, attach prior-year category and country split notes with this year's draft support so Form 1116 review is faster and less assumption-driven.

Related reading: Can I Claim the Foreign Tax Credit for Taxes Paid to a 'Blacklisted' Country?.

Use Gruv records to reduce year-end friction where enabled#

Gruv records can speed year-end prep when available, but treat them as supporting evidence, not your only proof for a U.S. federal tax return.

Pull the records that remove rework first#

Start with exports that connect activity to money movement: invoice history, payout summaries, transaction trails, and status or destination changes. Use a simple checkpoint: can someone trace one payment from invoice to payout without extra explanation? If not, log the gap now and attach outside support, for example institution records, tax receipts, or remittance documentation.

Map each output to the filing task it supports#

For Foreign Tax Credit (FTC) work, exports can help you reconstruct income and tax flow, but they do not decide eligibility. Form 1116 still requires separate handling by income category, separate country or territory lines or columns where relevant, and generally U.S.-dollar reporting.

For Report of Foreign Bank and Financial Accounts (FBAR) review, platform records can help you build a candidate account list where supported. They do not replace other records you may need for filing.

Use one decision rule before relying on an export. Include a Gruv record when it clearly answers at least two of these: what happened, when it happened, and which account or counterparty was involved. If it does not, keep it as context and pair it with another source.

Watch two failure modes:

- Do not use platform data as sole legal proof for FTC claims. Not all foreign taxes qualify, and FTC cannot be claimed on income you exclude under foreign earned income or housing exclusions.

- Do not assume one platform captures every reportable account. Coverage varies by market and program, so confirm scope before depending on it for account completeness.

Keep exports audit-ready. Save exports with enough context to re-check later, including owner, date range, and download date. For FTC prep, tag each export to the Form 1116 income category and country it supports. For FBAR prep, tag each item with the account details you still need to confirm.

Use Gruv exports to reduce manual assembly, document missing pieces early, and backstop material numbers with external records.

Finish year-end with clear decisions, not open loops#

The finish line is not hoping you are covered. It is being able to show why you chose your filing position. Finish year-end by locking your position now: collect defensible evidence, choose your FEIE or FTC path with an explicit gate, and escalate early where facts are messy.

Close the three decisions that matter most#

- Evidence is sufficient for the claim

If you plan to use FEIE, document which qualification test you are relying on and why. For the Physical Presence Test, your records should support 330 full days in a 12-month period, with a full day defined as 24 consecutive hours from midnight to midnight. The days can be non-consecutive, but missing 330 fails the test regardless of the reason.

- FEIE vs. FTC path is explicit

Do not leave this as a decide-later issue. If you claim FEIE, you still need to file a U.S. tax return reporting that income. If you are preparing for FTC, build a Form 1116-ready package by income category. Keep the mechanics clean: each Form 1116 has only one income-category box checked, and amounts are generally reported in U.S. dollars.

- Escalation trigger is acknowledged

If the facts do not fit cleanly, treat that as a real issue now. Living abroad for one year alone does not automatically create bona fide resident status. The Bona Fide Residence Test requires an uninterrupted period that includes an entire tax year, January 1 through December 31.

Do not self-guess messy facts near deadline#

If a major unknown remains around FEIE qualification or FTC documentation, escalate instead of guessing from memory. Typical escalation triggers include unclear travel-day support for FEIE, incomplete foreign-tax records for Form 1116 categories, or uncertainty about whether your facts satisfy the bona fide residence standard. Also escalate when timing crosses tax years, because income earned in one year and paid in the next can change how much income is excludable.

Leave a usable handoff, not scattered notes#

Your year-end file should show the claim, the support, and the open items. For FEIE, keep the selected test and date support. For FTC, keep category-level foreign tax support and U.S.-dollar reporting ready for Form 1116. Keep unresolved questions in one place so they can be closed before filing.

If one area is still weak, read next in this risk order: 183-Day Rule Explained: Stop the Tax Myths Before They Cost You. Then review the Foreign Tax Credit (Form 1116) deep dive, then digital-shoebox documentation habits. The finish line is not "I think I'm covered." It is "I can show why this is the filing position I chose."

Before final handoff, consolidate your checklist into one working stack from Gruv tools so unresolved items do not spill into filing week.

Frequently Asked Questions

Do U.S. expat freelancers still have to file a U.S. federal return if they already pay tax abroad?

Usually yes. Paying tax abroad does not automatically end your U.S. filing obligation. FEIE does not remove the need to file, and FTC claims still require return work through Form 1116.

What is the FBAR trigger, and how is FinCEN Form 114 different from my tax return?

Confirm the FBAR trigger before filing instead of relying on memory. FinCEN Form 114 is separate from your tax return, so it should be tracked as its own filing obligation with account records organized before year-end.

Does claiming Foreign Earned Income Exclusion (FEIE) or Foreign Tax Credit (FTC) remove the need to file?

No. FEIE is an exclusion for qualifying individuals, not permission to skip filing, and you still file a return reporting the income. FTC also requires detailed Form 1116 preparation by income category, with amounts reported in U.S. dollars.

When should I evaluate Form 8938 under Foreign Account Tax Compliance Act (FATCA)?

Evaluate Form 8938 early if you hold foreign financial assets or accounts. The threshold depends on your filing status and facts, so confirm the current IRS criteria instead of guessing. Early review helps you avoid late-stage gaps in statements, ownership details, or valuation support.

Do I get extra time to file if I live abroad, and what still needs early preparation?

There may be special filing-time relief for some taxpayers abroad, and the Form 2555 instructions include a Special extension of time to file section. Extra time does not fix missing records, so prepare early. If you may use the Physical Presence Test, track 330 full days in a 12-consecutive-month period, with each full day being 24 consecutive hours from midnight to midnight.

What documents should I gather before year-end so my preparer can file quickly and accurately?

Gather records that support foreign income, foreign taxes, and travel days if FEIE is in play. For FEIE, your file should support either the physical presence test or bona fide residence analysis, since living abroad for one year alone does not automatically create bona fide resident status. For FTC, prepare a Form 1116-ready package with income category detail and U.S.-dollar reporting.

Try a related tool

Rina focuses on the UK’s residency rules, freelancer tax planning fundamentals, and the documentation habits that reduce audit anxiety for high earners.

With a Ph.D. in Economics and over 15 years of experience in cross-border tax advisory, Alistair specializes in demystifying cross-border tax law for independent professionals. He focuses on risk mitigation and long-term financial planning.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

Portugal NHR vs Spain Beckham Law for High-Earning US Expats in 2026

Start with documentation, not tax projections. In the portugal nhr vs spain beckham law decision, the safer first move is to choose the path you can prove from end to end before you optimize for headline outcomes.

A Deep Dive into the Foreign Tax Credit (Form 1116)

If you paid qualifying foreign income taxes and still owe U.S. tax, start with the Foreign Tax Credit and Form 1116. A credit usually beats a deduction because it offsets tax dollar for dollar. Do not start entering numbers until you decide whether you are taking a credit, an itemized deduction, or an exclusion. If you use the [Foreign Earned Income Exclusion](https://www.irs.gov/individuals/international-taxpayers/foreign-earned-income-exclusion) or the foreign housing exclusion, remove the excluded income and related foreign taxes from the credit path first.