Quick Answer

Yes. The first year election tax residency option can work when your timeline is clean, your records support the filing position, and you can meet following-year substantial presence before submitting the election-year package. Core checkpoints are extension timing with Form 4868, correct dual-status return assembly, and evidence for the residency start date tied to the earliest qualifying 31-day period. If spouse-related choices, state exposure, or foreign-income timing remain unclear, pause and get cross-border review first.

For global professionals establishing a foothold in the United States, the IRS first-year choice can be a powerful tax decision. Used well, it can let you control your tax residency start date and change what you can claim. Used poorly, it can create a large and avoidable tax problem.

The right answer depends on your dates, your income, your records, and, if relevant, your spouse's facts. Move in order. First assess whether this is even worth modeling. Then compare both filing paths with verified inputs. Execute only after the timing and documentation are solid. This guide follows that sequence so you can make a defensible decision, not just a hopeful one.

Step 1: Assess - Is This Powerful Tax Lever Right for You?#

Use Step 1 as a go or no-go gate. If your facts are not complete enough to model, stop here and clean them up first.

Before you get into filing mechanics, separate the labels you are considering: first-year choice, dual-status, and a separate spouse election. Keep them distinct in your notes rather than using them interchangeably. Confirm the exact legal definitions and filing effects from current IRS guidance before applying them.

The practical question is simple: based on documented facts, do you have a defensible reason to model an earlier U.S. filing position, or are you still dealing with uncertainty you cannot defend?

Start with your pre-move timeline#

Your timeline is the foundation. Build it from dated events tied to the period you are evaluating, and gather the records before you draw conclusions.

Red flags:

- Major cross-border income events with unclear dates or incomplete documentation.

- Conflicting records on when income was recognized or where it was taxed.

- Any decision logic that depends on assumptions you cannot verify.

Green lights:

- A quiet pre-move period with routine, well-documented activity.

- Clean date evidence for meaningful transactions.

- A consistent record trail across statements, contracts, and tax documents.

Then test the expected upside#

Do not model from a general sense that the result will be "better." Write down the specific benefit you expect, then confirm you can support it with records already in hand.

Red flags:

- You cannot clearly state the expected benefit.

- The upside works only if multiple assumptions all break your way.

- Supporting documents are partial or not yet available.

Green lights:

- The expected upside is concrete, documented, and testable.

- Records are complete enough to survive a line-by-line review.

- Your assumptions are few, explicit, and checkable.

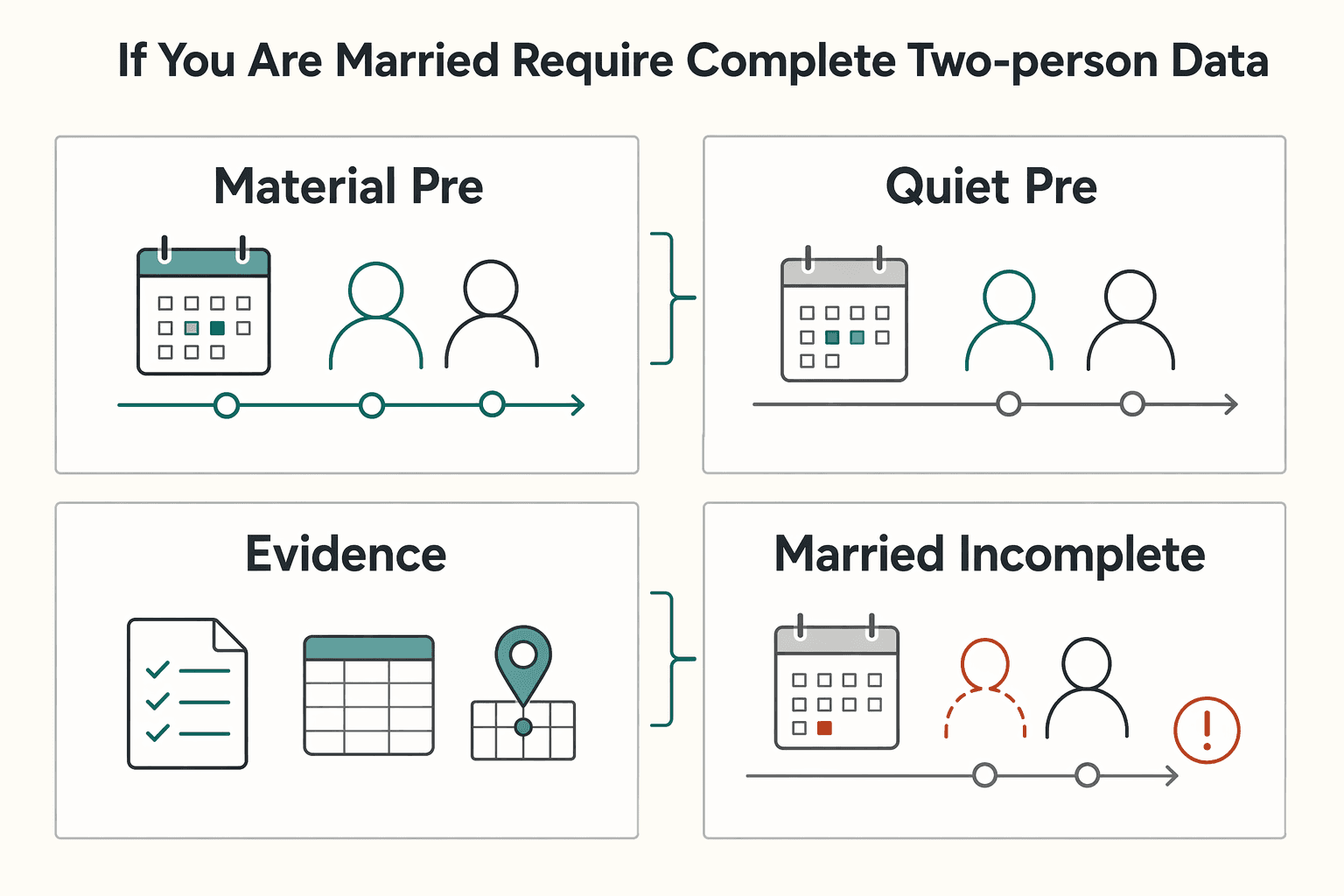

If you are married, require complete two-person data#

If your scenario includes a spouse, incomplete spouse records make Step 1 speculative very quickly. If you cannot place both spouses' major events on one dated timeline, do not model yet.

Red flags:

- Missing spouse income records, account data, or timeline details.

- Unresolved cross-border treatment questions for either spouse.

- Different versions of the year's facts across your files.

Green lights:

- Both spouses' records are complete and date-aligned.

- Major events are easy to place on a shared timeline.

- You can model both spouses from the same verified dataset.

| Scenario | Likely direction | Why | Documents to gather |

|---|---|---|---|

| Material pre-move cross-border events with unclear timing | Pause | High uncertainty in core inputs | Transaction records, contracts, statements, tax records |

| Quiet pre-move period with routine activity | Proceed to Step 2 modeling | Lower complexity, clearer baseline | Income statements, account summaries, year-end records |

| Clear expected upside with strong documentation | Proceed to Step 2 modeling | Upside is testable, not theoretical | Benefit-specific records and support files |

| Married with incomplete spouse data | Pause | Incomplete two-person facts can skew results | Spouse income/tax/account/timeline records |

| Travel and move timeline not fully documented | Pause | Timeline uncertainty weakens model reliability | Entry/exit evidence, itinerary and residency records |

If your records are clean and the fact pattern is straightforward, move to Step 2 and compare outcomes. If material facts are missing, ambiguous, or the cross-border issues are still unresolved, stop here and involve a qualified tax professional before you take a filing position.

You might also find this useful: A Guide to the 'Look-Back' Rule for US Tax Residency.

Step 2: Model - When the First-Year Choice Is a Win (and When It's a Trap)#

Step 2 helps only if your model is built from verified records and current, relevant authority, not memory or summaries. Verify that any regulatory source you rely on is current, officially authoritative, and directly relevant to tax-residency rules — not banking or other regulatory domains. Check for recent Federal Register updates and confirm you are reading the version in effect for your tax year.

Before you compare outcomes, make sure your worksheet uses labels as placeholders, not as settled legal conclusions. Use these as modeling labels only until you confirm legal meaning in the correct current IRS sources:

dual-status return: one comparison path label.full-year resident treatment with spouse: one spouse-related comparison path label.worldwide income: one scope label for income streams you may need to test.

If your worksheet treats those labels as final legal answers, pause and fix that before you calculate anything else.

Set working labels before you calculate anything#

Model both paths first, then mark what is still unverified. The goal is not a polished estimate. It is to see whether the result still works after you strip out weak assumptions.

| Factor to test | Path A: do not elect | Path B: elect | Verification required |

|---|---|---|---|

| Timing | List material events by date | List same events by date | Dated records; current governing text; version/date check |

| Core assumptions | List each assumption explicitly | Re-test each assumption explicitly | Primary documents; current, relevant IRS sources |

| Label usage | Keep legal/tax labels as placeholders | Keep legal/tax labels as placeholders | Confirm legal meaning before treating labels as conclusions |

| Sensitivity check | Remove low-confidence inputs and note the result | Remove low-confidence inputs and note the result | Side-by-side recheck using only verified inputs |

Add a confidence tag (high, medium, low) for each row. If the projected upside depends mostly on low-confidence rows, treat the result as unresolved.

Compare both paths side by side#

Use a strict filter here:

| Outcome | Use when | Driver |

|---|---|---|

| Elect | Authority is current and relevant, records are date-clean, and the result still holds after removing uncertain assumptions | Verified inputs still support the outcome |

| Do not elect | Key terms remain unverified or the model weakens once low-confidence inputs are removed | The upside depends on uncertain assumptions |

| Escalate | Unresolved authority, relevance, or version questions drive the result | Source or version issues control the outcome |

- Make the election only when the authority is current and relevant, your records are date-clean, and the result still holds after you remove uncertain assumptions.

- Default to not elect when key terms remain unverified or the model weakens once low-confidence inputs are removed.

- Escalate to a qualified advisor when unresolved authority, relevance, or version questions are driving the result.

Decision criteria#

For broader tax-residency context, see The 'Closer Connection' Exception: How to Avoid US Tax Residency Even if You Spend Time in the US.

Before you file, use the Tax Residency Tracker to keep date records and documentation aligned with the sources you verify.

Step 3: Execute - Your Compliance Blueprint for Making the Election#

If your Step 2 model still holds after you remove low-confidence assumptions, execution becomes a timing and assembly exercise. The core rule is simple: do not file the election-year Form 1040 package before you meet the substantial presence test in the following year.

Pre-filing checks#

Run these checks before you draft anything. Many filing problems here come from date errors, timing mistakes, or incomplete support.

| Check | Requirement | Timing/evidence |

|---|---|---|

| Required inputs | Day-by-day U.S. presence log, passport/travel records, dated absence log, and following-year day count worksheet | Have the records before you draft anything |

| Deadline dependency | For a 2025 return, the regular deadline is April 15, 2026; Form 4868 gives six (6) more months to file, but not more time to pay | Estimate and pay by the original deadline if tax is due |

| Eligibility checks | Confirm a 31-day continuous U.S. presence period in the current year, at least 75% presence from day 1 of that period through year-end, and following-year substantial presence test status | Check before filing |

| Unverified rule or criteria | Current criteria pending official tax-source verification | Verify the rule, exception, treaty position, or criteria before using it |

| Common failure point | If valid, the residency start date is the first day of the earliest qualifying 31-day period | Do not use the wrong residency start date |

- Build your day-by-day U.S. presence file before you draft anything.

- If you are filing a 2025 return, remember that April 15, 2026 is the regular deadline. Form 4868 gives six (6) more months to file, not more time to pay, so estimate and pay by the original deadline if tax is due.

- Before you file, confirm a 31-day continuous U.S. presence period in the current year, at least 75% presence from day 1 of that period through year-end, and following-year substantial presence test status (commonly modeled as 31 days in that year and 183 days over the 3-year period).

- If any step depends on exceptions, treaty positions, or criteria you have not confirmed, verify the rule from current official tax sources before you use it.

- The most common miss here is the residency start date. If valid, it is the first day of the earliest qualifying 31-day period.

Election filing package#

For this election, build a dual-status package with a clear resident and nonresident split.

| Document | Purpose | Where it goes | Verify before submission |

|---|---|---|---|

| Form 4868 | Extends time to file | Filed by the regular due date | Filed on time; payment estimate made because extension does not extend time to pay |

| Form 1040 or 1040-SR marked "Dual-Status Return" | Main return | Main return package | "Dual-Status Return" appears across the top; resident-period items are treated under resident rules |

| Nonresident-period statement (often Form 1040-NR marked "Dual-Status Statement") | Shows nonresident-period income | Attached to Form 1040/1040-SR package | "Dual-Status Statement" appears across the top; only nonresident-period items included |

| First-year choice statement | Formally makes the election | Attached to Form 1040 or 1040-SR | Includes name, address, TIN, statement making the choice, prior-year nonresidency, following-year substantial presence statement, and qualifying day counts/dates |

| Residency start-date evidence file | Supports day count and start date | Kept in records | Travel log reconciles to stamps, tickets, calendar, and any of the up to 5 absence days treated as presence |

Return assembly#

Keep the period boundaries explicit and consistent. Every line item should follow the same date logic you used in the model.

- Nonresident period: the part of the year before your residency start date; taxed under nonresident rules on U.S.-source income.

- Resident period: from the residency start date through December 31; taxed on income from all sources.

- Assembly control: every income item needs a date and a period bucket. If timing or characterization is unclear, verify that treatment from tax records and current official guidance before using it.

- Common failure point: claiming the standard deduction on a dual-status return. Dual-status filers cannot use the standard deduction, though certain itemized deductions may be allowed.

Post-filing records and risk control#

Do not treat audit support as cleanup after the fact. Build the record file as part of execution.

| Topic | Action | Timing/trigger |

|---|---|---|

| Records to retain | Keep the filed return package, first-year choice statement, Form 4868, travel logs, passport stamps, flight records, and resident/nonresident split worksheet | Build the record file as part of execution |

| Retention baseline | Keep records supporting reported items through the applicable limitations period | Generally 3 years from filing, and longer where another rule applies |

| Next-year dependency | Monitor the following tax year closely | The election depends on meeting substantial presence in that later year |

| Escalate for review | Treaty-dependent positions, or day-count issues where treaty residency and Internal Revenue Code residency may diverge | Get review when treaty or day-count issues affect the result |

- Keep the filed return package, first-year choice statement, Form 4868, travel logs, passport stamps, flight records, and your resident/nonresident split worksheet in one record file.

- Keep records supporting reported items through the applicable limitations period, generally 3 years from filing and longer where another rule applies.

- Watch the following tax year closely because the election depends on meeting substantial presence in that later year.

- Get review if treaty-dependent positions, or day-count issues where treaty residency and Internal Revenue Code residency may diverge, affect the result.

If day-count myths are part of the confusion, see 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

The Bigger Picture: Downstream Financial Consequences#

This is more than a one-form decision. It can affect your federal filing scope, state analysis, foreign-account review, and the records you will need later if any part of the return is questioned.

Map what needs verification now, then file only after each item is supported by current instructions and your own records. For this section, use these working buckets, not legal conclusions: federal return scope, state filing exposure, worldwide review, and downstream documentation.

Practical obligations matrix

| Area to review | What to report or test | Who may be affected | When it may apply | Records to retain |

|---|---|---|---|---|

| Federal return scope | How you separate election-year items across the federal package | Anyone making this election | During return build and final review | Filed return package, election statement, dated income/workpapers |

| Foreign accounts | Whether any foreign-account reporting review is needed (thresholds are unverified in this section) | Potentially relevant for filers with non-U.S. financial accounts or signatory authority; confirm case-by-case | Before filing, after full account inventory | Account list, statements, highest-value support, ownership/signatory details |

| Foreign assets and related information returns | Whether any additional international reporting review is needed (form triggers are unverified in this section) | Potentially relevant for filers with non-U.S. assets, entity interests, or foreign investments; confirm case-by-case | During prep, after ownership/timing inventory | Acquisition dates, basis support, issuer/entity details, related tax records |

| State exposure | Whether a separate state filing analysis is needed (state outcomes are unverified in this section) | Anyone with state work, housing, withholding, or other ties | In parallel with federal prep, before filing | Lease/move records, payroll/withholding records, location logs, state notices |

Federal versus state. Use this as a decision tool.

The main point here is evidence control. This pack does not establish how a federal election affects state treatment, so keep federal and state analyses separate until both are independently verified.

| Decision question | Working treatment in this section |

|---|---|

| What does the election control directly? | Not established by this evidence pack; verify from current federal instructions for your facts. |

| What does it not settle by itself? | State filing conclusions and separate downstream reporting determinations are not established by this evidence pack. |

| Why run a separate state analysis? | The evidence pack here does not support state conclusions, so state treatment must be verified independently before you file. |

Risk triage before filing

Use this as a final screen before you lock the return.

- High-risk profile signals: multiple foreign accounts or entities, material transactions near the residency transition, or unresolved state ties.

- Documentation gaps: incomplete presence timeline, missing account statements, missing basis/history records, or no clean item-by-item support file.

- Default actions: pause when a threshold or form trigger is unclear, verify from current instructions, keep federal and state analyses separate, and escalate unclear cross-border issues before filing.

Next-cycle control plan

Set up one forward file now so next season is controlled, not reactive. Keep the filed package, election statement, timeline support, account and asset inventory, and any records that may matter for later-year positions. Mark all unresolved items for professional review.

Any threshold-specific or jurisdiction-specific conclusions should remain explicitly unverified until supported by a valid, current source.

We covered this in detail in A Guide to the UK's 'Split Year Treatment' for Tax Residency.

Conclusion: You Are the CEO of Your Tax Strategy#

Treat this as a formal residency election with compliance consequences, not a shortcut. The final test is straightforward: make the first-year choice only when eligibility is confirmed, worldwide-income exposure is acceptable, and your filing documentation is ready. If those pieces are not in place, pause and use a safer filing posture until they are.

Assess. Start with eligibility before strategy. Confirm a qualifying 31-day continuous U.S. presence period, at least 75% presence after that period through year-end (with only up to 5 days of absence treated as presence), and that you can meet the substantial presence test in the following year before filing the Form 1040 package for the election year. This keeps you from building a return around an election you are not yet allowed to file.

Model. Model the income scope before you optimize anything else. Under the first-year choice, residency starts on the first day of the earliest qualifying 31-day period, and you are then treated as a U.S. resident for the rest of that year. In a dual-status year, the resident period is taxed on worldwide income, and dual-status limits include no standard deduction on Form 1040. This keeps an upside story from hiding foreign-income exposure and dual-status constraints.

Execute. Execute only after the filing mechanics are lined up. You cannot file until the following-year substantial presence test is met. IRS guidance says to use Form 4868 for an extension of time to file. Dual-status filing requires correct return labeling and an attached statement for the nonresident period. This helps you avoid deadline errors, missing attachments, and unsupported return treatment.

If spouse elections, state residency conflicts, or foreign-income characterization are unclear, escalate to a cross-border tax professional before filing, especially when federal treatment appears settled but state facts still point another way.

Before submission, confirm your assumptions, retain day-count and income evidence, and prepare the required labels, statements, and filing attachments in the same file you would rely on if the return is reviewed. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2026. If your case includes spouse elections, state residency conflicts, or mixed foreign income, contact Gruv to review workflow options while your tax advisor confirms filing positions.

Frequently Asked Questions

What do you mean by the first-year choice?

Here, it means the IRS-labeled topic shown on the page titled “Tax residency status - first-year choice.” It may change how you frame your federal year analysis. Use it as a verification checkpoint against current IRS guidance, and do not treat a secondary summary as the rule itself.

What is a residency start date in this context?

Use this as a working label for the date you are trying to determine in your tax-residency analysis. It matters because your recordkeeping and review may hinge on that date. If the date is not clear from current IRS instructions, pause and verify before modeling exposure.

What does dual-status filing mean here?

In this section, it is only a plain-language planning label. It may indicate a year with mixed treatment and added reconciliation risk. Use the label for planning, but do not assume forms or statement mechanics until you confirm current IRS instructions.

Does a spouse automatically come along with this election?

Treat your election and spouse-related filing choices as separate decisions unless current IRS guidance says otherwise. If marriage changes filing position, income scope, or signature requirements, treat that as a formal review point.

When should I stop and get a professional review?

Escalate when facts can materially change the filing path: date uncertainty, spouse-related choices, or foreign income events near a possible transition period. These are the cases where timing errors can affect the whole return. Bring a dated presence log, income timeline, account inventory, and your draft treatment for review.

Why is this FAQ cautious on specifics?

Verify any rule, test, threshold, or form step from current IRS source text before relying on it. If someone gives you exact tests, thresholds, or form steps without current IRS source text, ask for the source before relying on it. Quick decision table | Common scenario | Likely filing path | Primary compliance risk | Safest next step | |---|---|---|---| | You think the election may help, but your dates are still rough | Election analysis only, not a filing conclusion yet | Date assumptions that are not yet verified | Build a day-by-day presence log and verify current IRS rule text | | You have a spouse and are considering a combined filing position | Separate spouse-election review before locking the return | Unverified assumptions about income scope or signatures | Review both spouses' records together and confirm current IRS guidance | | You had foreign income, a sale, or another material event near the transition | Mixed-year review with extra documentation | Timing misclassification and unsupported positions | Build a dated event ledger and verify each trigger from current instructions | | One part of your analysis seems settled, but another key fact conflicts | No filing conclusion yet | Carrying one conclusion into unrelated issues | Keep separate evidence for each issue and verify each rule independently | | Your source for a key rule is a secondary article only | No filing conclusion yet | Unsupported election position | Pull the live IRS pages titled "Tax residency status - first-year choice" and "Determining an individual's tax residency status", then document what you relied on | If your answer depends on a date, spouse choice, or foreign event, keep source-backed support in your file, not just a confident summary.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- apps.irs.gov/app/IPAR/resources/help/subprestest.htmltrusted

- irs.gov/individuals/international-taxpayers/tax-resi...trusted

- irs.gov/individuals/international-taxpayers/taxation...trusted

- taxpayeradvocate.irs.gov/wp-content/uploads/2020/08/VOL-2_TAS-Researc...trusted

- taxpayeradvocate.irs.gov/wp-content/uploads/2024/01/ARC23_MSP.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

How to Make a Defensible US Tax Residency Call Under the Look-Back Rule

If you searched for "look-back rule us tax residency," the goal is practical: take a U.S. tax residency position you can defend under IRS rules with records that hold up.