Quick Answer

Start with three filing lanes: the decedent’s final Form 1040, the estate’s Form 1041 for post-death income, and Form 706 when transfer-tax filing or portability is in scope. A final tax return for estate administration is strongest when you confirm who can sign, submit Form 56, secure the estate EIN, and keep one complete record of documents, deadlines, and notices before distributing assets.

You've been named the executor of an estate. It is an honor, but it often arrives in the middle of grief and with real fiduciary risk. Handle it like a temporary operation with high stakes. Secure control, sort assets and liabilities, keep the tax lanes separate, and document every decision. This guide follows that path from the first month through final closeout, with the tax work as the thread that holds the whole process together.

Phase 1: Triage & Team Assembly (Your First 30 Days)#

Your first 30 days are about control and risk containment. Get legal authority in hand, put records in one place, and surface the issues that can create tax problems or personal liability if they sit too long.

Know what your duty actually is#

Start with the basic line you cannot blur: the decedent's final individual return is separate from the estate's income tax return. As fiduciary, you are responsible for making sure required returns are filed and taxes due for the decedent or the estate are paid.

Bring in an estate attorney or CPA early if any of these are in play: possible insolvency, foreign accounts, digital assets, or uncertainty about what belongs on the final individual return versus the estate return. If the estate may be insolvent, personal liability risk can increase. Do not guess on payment or distribution decisions.

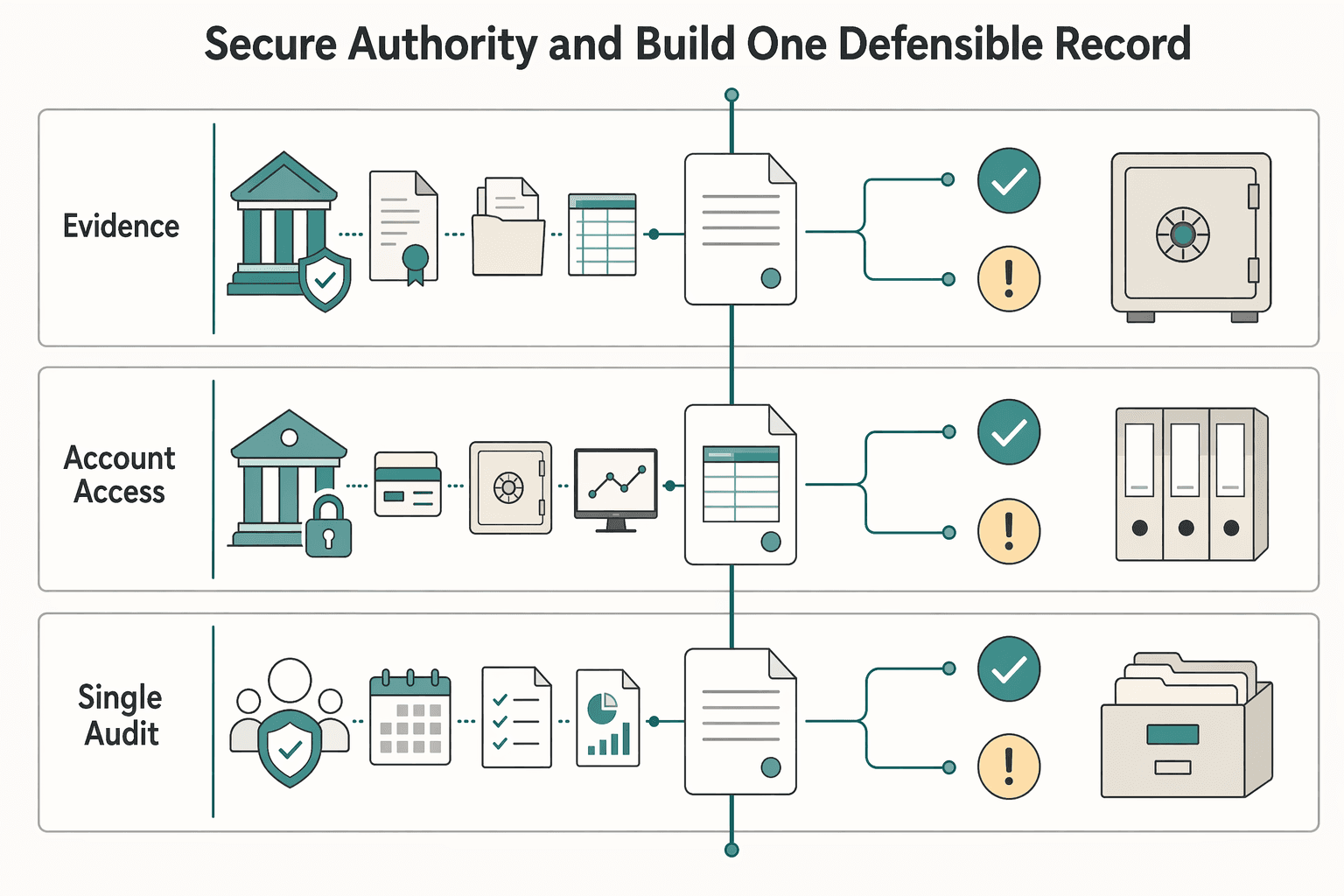

Secure authority and build one defensible record#

Use this first-month checklist to get authority, access, and documentation under control, so you can show one clear file if questions come later.

| Workstream | Key actions | File record |

|---|---|---|

| Authority documents | Collect court appointment papers, estate documents, and account records showing control of the decedent's property; file Form 56 when the fiduciary relationship starts and again if it ends | Court papers, control records, Form 56 status |

| Account-access workflow | Apply for the estate EIN using Form SS-4; use the EIN and authority documents to standardize outreach to banks and brokers | EIN setup and outreach records |

| Single audit trail system | Keep one folder structure and one tracking log; store prior returns, W-2s, 1099s, statements, basis records, and correspondence; log calls and instructions tied to money movement, account closures, or distributions | Date received, source, account or payer, tax year, action needed, owner, file location |

-

Authority documents

-

Collect court appointment papers if you have them, along with the estate documents and account records showing you control the decedent's property. - File

Form 56to notify the IRS that the fiduciary relationship started, and again if it ends. - If court-appointed, include appointment proof with the final return filing package. - If there is no appointed representative and no surviving spouse, the person controlling the decedent's property signs as personal representative. -

Account-access workflow

-

Apply for the estate EIN using

Form SS-4(U.S. applicants can obtain an EIN on IRS.gov without charge). - Use the EIN and your authority documents to standardize outreach to banks and brokers instead of handling access one request at a time. -

Single audit trail system

-

Keep one folder structure and one tracking log for every document and decision. - Track at least: date received, source, account or payer, tax year, action needed, owner, and file location. - Store prior returns, W-2s, 1099s, statements, basis records, and all bank, broker, and payroll correspondence in that same system. - Log calls and instructions tied to money movement, account closures, or distributions.

Checkpoint by day 30: you should be able to show the status of Form 56, EIN setup, known assets, known debts, and missing tax documents in one place.

Triage the estate before you value it#

Before you get deep into valuations, do a control review. Identify what exists now, then hand classification and tax treatment to the right professional.

| What to identify now | What to verify with professionals |

|---|---|

| Bank and brokerage accounts, including title/ownership and recent statements | Whether income is reported on the decedent's final return or the estate return, especially across date-of-death statement periods |

| Retirement accounts, life insurance, and deposit accounts with beneficiary/POD designations | Whether transfer follows account terms and what tax reporting follows payouts |

| Real estate, business interests, and major personal property | What valuation support and records are needed for tax filing and administration |

| Digital assets (exchange accounts, wallets, platforms, transaction records) | What access is legally available and how related income is reported |

| Foreign bank, brokerage, and mutual fund accounts, including signature authority | FBAR exposure, ownership versus authority, and highest-balance data |

| Debts, medical bills, tax notices, and expected W-2 or 1099 reporting | Insolvency risk and whether payment or distribution sequencing needs counsel |

Two items are easy to miss early: beneficiary-designated deposit arrangements such as POD accounts, and digital assets. Either one can change the tax work right away, and POD designations can also change the transfer path.

FBAR trigger for global estates#

If foreign accounts are in the mix, treat FBAR as its own compliance track. Build the full account list first, then have your CPA confirm the filing position.

| Item | Current detail | Note |

|---|---|---|

| Form | FinCEN Form 114 (Report of Foreign Bank and Financial Accounts) | Treat FBAR as its own compliance track |

| Who files | A U.S. person, including an estate, files when FBAR rules are met | Have your CPA confirm the filing position |

| Threshold | Aggregate foreign financial account value over $10,000 at any time during the calendar year | Verify before filing |

| Timing | Due April 15 | Automatic extension to October 15; verify before filing |

| Gather first | Account type, institution, account number, country, ownership versus signature authority, and highest annual value | Build the full account list first |

- What it is: FBAR is FinCEN Form 114 (Report of Foreign Bank and Financial Accounts).

- Who files: A U.S. person, including an estate, files when FBAR rules are met.

- Current threshold (verify before filing): aggregate foreign financial account value over

$10,000at any time during the calendar year. - Current filing timing (verify before filing): due

April 15, with an automatic extension toOctober 15. - What to gather first: account type, institution, account number, country, ownership versus signature authority, and highest annual value.

Related: 183-Day Rule Explained: Stop the Tax Myths Before They Cost You. If your intake checklist surfaces foreign financial accounts, run a quick pre-check before you finalize filing decisions with the FBAR Calculator.

Phase 2: Mastering the Final 1040 (The Decedent's Personal Return)#

The deliverable in this phase is the decedent's final Form 1040 or Form 1040-SR. It covers income only through the date of death. Income received after death belongs on the estate's Form 1041, not here.

Set the date-of-death cutoff first. Then reconcile each information return to that cutoff, classify possible IRD items, test deductions and credits, and run filing quality control.

Build the final 1040 from source documents, not from year-end summaries#

Do not rely on annual totals if the date of death falls inside the reporting period. Build the return from source records so you can split pre-death and post-death amounts correctly.

| Source document | What to map to the final 1040 | What to verify before posting | Red flag to escalate |

|---|---|---|---|

W-2 | Wages and withholding attributable to the decedent period | Whether any payroll paid after death is being included incorrectly | Year-end wage total does not match pre-death payroll records |

1099-INT | Interest attributable to the pre-death period | Statement period crossing date of death | Annual interest is posted without a pre-/post-death split |

1099-DIV | Dividends or distributions attributable to the pre-death period | Payment timing around date of death | Annual dividend total is posted with no cutoff review |

| Brokerage year-end package | Investment income attributable to the pre-death period | Transaction-level timing around date of death | Package total is used without transaction-date reconciliation |

| Business, farm, or partnership records | Amounts properly includible before death | For cash-method taxpayers, whether amounts were actually or constructively received before death | Unpaid or late-reported amounts with unclear timing |

| Estimated tax and withholding records | Pre-death payments or withholding credits | That each payment is reflected once | Missing or duplicated payment credits |

If a form total looks too high for the pre-death period, stop and reconcile the underlying statements before you file. That keeps you from posting year-end totals that cross the date of death.

IRD is the classification checkpoint#

This is where many returns go off track. Income in respect of a decedent, or IRD, is income the decedent was entitled to as gross income but that was not properly includible before death. Common categories include wages, farm income (crops, crop shares, livestock), partnership income, and U.S. savings bonds acquired from the decedent.

A practical rule is simple. For cash-method taxpayers, if the decedent had a right to the income but did not actually or constructively receive it before death, treat it as a potential IRD item and escalate classification before filing.

Deductions and credits worth testing#

Some deductions and credits are straightforward, but end-of-life expenses often need a closer look. Test them against payment timing and the current-year rules before you post anything.

| Potential item | Eligibility test | Required records | Escalate to CPA when |

|---|---|---|---|

| Medical expenses paid before death | Deductible only if allowed under current-year Form 1040 rules; verify the exact threshold from current official IRS guidance or adviser records before use. | Bills, proof of payment, insurance reimbursement records | Large end-of-life care costs, reimbursements, or mixed payors |

| Medical expenses paid by the estate within the 1-year period beginning with the day after death | Special election may be available under Publication 559 | Estate checks, invoices, payment dates, estate ledger | You need to decide whether to claim them on the final return or elsewhere |

| Other deductible expenses paid before death | Final individual return generally claims expenses the decedent paid before death | Canceled checks, statements, invoices, prior-year return pattern | You are unsure whether payment occurred before or after death |

| Credits shown by current-year instructions and source documents | Claim only if the decedent otherwise qualifies under current-year rules | Prior return, carryover support, original source documents | Any credit depends on year-specific limits or carryforwards |

Filing quality control checklist#

Before the final Form 1040 goes out the door, run these checks so the filing package matches the estate authority documents and refund position:

- Check the

Deceasedbox and enter the date of death on the return. - Ensure signature authority is correct: if an appointed personal representative exists, that person signs; for a joint final return, the surviving spouse also signs.

- If court-appointed, attach a copy of the court appointment document to the original return.

- If a refund is due, confirm whether

Form 1310is required; surviving spouses filing a joint return and court-appointed or court-certified personal representatives generally do not need it. - Do not attach a death certificate.

- Verify the exact filing deadline and extension rules from current official IRS guidance or adviser records before filing; for calendar-year decedents, confirm whether the regular April tax date applies.

For a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Phase 3: Running the Estate as an Entity (The Form 1041 Lifecycle)#

Once the date of death passes, the estate becomes its own filing track. The decedent's final Form 1040 covers income up to death, and income generated after death belongs to the estate and may require reporting on Form 1041.

In practice, this phase is about maintaining a clean cutoff. Pre-death income stays on the final individual return. Post-death income from estate assets moves to the estate return.

Set up the estate side before money starts moving#

Do this setup first. If you wait until filing season, the records are usually harder to untangle than they needed to be.

- Obtain the estate EIN before filing

Form 1041, and use that tax ID on the return. - Consider opening estate accounts in the estate's name using that EIN.

- Route post-death receipts, bill payments, and distributions through that estate ledger.

- Keep estate activity separate from personal funds and household spending.

That recordkeeping is what lets you prove which amounts are estate income, which expenses were paid by the estate, and which payments were distributions.

Choose the filing cadence deliberately#

Do not treat the tax year choice as a default administrative step. The estate can report on a calendar year or a fiscal year, and you lock that in when you file the first Form 1041.

| option | when it helps | tradeoff | coordinate with CPA |

|---|---|---|---|

| Calendar year | You want alignment with most annual tax documents | Form 1041 and Schedule K-1 are due by April 15 | Yes, if timing is tight or foreign items are involved |

| Fiscal year | You want the tax year to better match administration timing | Due date becomes the 15th day of the 4th month after year-end, which can complicate beneficiary timing | Yes, especially when distributions span periods |

| Either option with extension | You need more time to assemble records | The automatic 5-month extension extends filing time, not classification quality | Yes, if records or allocations are still being finalized |

Classify income and expenses before you post them#

Build Form 1041 from transaction-level records, not just year-end summaries. That is usually the clearest way to preserve the cutoff between the decedent and the estate and to avoid double counting or misclassifying expenses.

Track the estate side in separate buckets before you decide what belongs on the return. Post-death income can include:

- Interest

- Dividends

- Rental income

- Other post-death income from estate assets

Track expenses separately and review them before any deduction decision:

- Administration expenses paid by the estate

- Professional administration costs tied to estate administration

- Other estate-paid administration costs that may be deductible for income-tax purposes

One control point matters here: do not claim the same administration expense for both estate income-tax and estate-tax purposes.

Filing trigger checkpoint:

- A domestic estate generally files

Form 1041if gross income is $600 or more for the tax year, or if it has a nonresident-alien beneficiary. - Confirm current IRS instructions before filing.

Use Schedule K-1 intentionally#

Do not assume every distribution creates a matching deduction. Amounts paid, credited, or required to be distributed may pass through to beneficiaries on Schedule K-1. The estate's distribution deduction is limited to DNI, so this is a place to slow down and confirm the treatment.

| K-1 point | Current rule | Action |

|---|---|---|

| Distribution deduction | Do not assume every distribution creates a matching deduction | Slow down and confirm the treatment |

| Pass-through amounts | Amounts paid, credited, or required to be distributed may pass through to beneficiaries on Schedule K-1 | Confirm what was paid, credited, or required to be distributed for that year |

| DNI limit | The estate's distribution deduction is limited to DNI | Review the limit before finalizing the return |

| Beneficiary details | Confirm each beneficiary's legal name, address, and taxpayer ID | Before delivery |

| Delivery changes | Deliver each Schedule K-1 by the Form 1041 filing deadline; if beneficiary amounts change after an amended Form 1041, issue amended K-1s to affected beneficiaries | By the filing deadline and after amendments |

Use this beneficiary communication checklist:

- Confirm each beneficiary's legal name, address, and taxpayer ID.

- Confirm whether income was actually paid, credited, or required to be distributed for that year.

- Deliver each

Schedule K-1by theForm 1041filing deadline. - If you amend

Form 1041and beneficiary amounts change, issue amended K-1s to affected beneficiaries.

Foreign assets need a separate compliance check#

Foreign assets add a second reporting layer, so review them early. Form 8938 and FBAR are separate regimes, and one does not replace the other.

Compliance-first checkpoints:

- Identify reportable foreign income for the U.S. estate return.

- Test whether FBAR applies, including the $10,000 aggregate value test for foreign financial accounts.

- Flag potential double-tax exposure where the same foreign-source income may be taxed abroad and in the U.S.

- Review possible foreign tax credit treatment (

Form 1116) with your CPA based on source-country tax records and income character. - Verify current reporting thresholds, forms, and deadlines from official IRS, FinCEN, or adviser records before using this checklist.

You might also find this useful: A Guide to Estate Planning for Digital Nomads.

Phase 4: The Final Transfer (Navigating Form 706 & Closing the Estate)#

Before you make final distributions, answer one threshold question: is Form 706 required, including for portability? Keep that transfer-tax analysis separate from the estate's income-tax work and from probate closeout.

Make the Form 706 decision first#

Form 706 is for federal transfer-tax reporting, including estate tax and GST tax on direct skips. It is not the estate's income-tax return. Start with the filing threshold for the decedent's year of death: the IRS FAQ shows $13,990,000 (2025) and $15,000,000 (2026).

Then test portability. If you want to transfer any DSUE amount to a surviving spouse, Form 706 still has to be filed even if the estate is below the normal threshold. Also flag nonresident, noncitizen decedents with U.S.-situated assets for attorney or CPA review.

| form | primary scope at closeout | decision gate |

|---|---|---|

Form 706 | Federal transfer-tax reporting for the gross estate, plus GST tax on direct skips | Above the year-of-death threshold, or portability election (DSUE) |

| Estate income-tax return | Separate income-tax reporting analysis | Use your estate income-tax filing analysis from Phase 3 |

Build an asset-by-asset valuation file before release#

Before final distributions, make sure assets are organized in the return package so updates are manageable if questions come later.

| asset class | filing checkpoint |

|---|---|

| Real estate | If the gross estate contains real estate, report it on Schedule A (Form 706). |

| Stocks and bonds | If the gross estate contains stocks or bonds, report them on the stocks-and-bonds schedule in Form 706. |

| Other material assets | Use the applicable Form 706 schedule and keep the file complete for possible updates. |

Close with a release checklist, not assumptions#

Final distribution is a control step, not just a paperwork step. Before you release assets, confirm that these closeout items are complete:

- The Form 706 filing decision is documented (threshold and portability review).

- If a filed

Form 706package is returned, IRS-required follow-up steps are in motion to preserve timely-filed treatment. - If you need to update a filed return, file another

Form 706or706-NA, mark page 1 with "Supplemental Information," and include pages 1-4 of the original filing. - Escalate to an attorney or CPA when the facts are disputed, incomplete, or complex.

For a step-by-step walkthrough, see How to File a Defensible Final US Tax Return After Renouncing Citizenship.

You're Not Just an Executor; You're the CEO#

A practical way to run an estate is with one decision owner, one record set, clear filing lanes, and no guessing about deadlines or authority. Your job is to keep that discipline from appointment through final distribution.

Your role has four responsibilities:

- Decision owner: confirm who has authority to file and sign.

- Timeline manager: calendar the regular April tax date for the decedent's final return, unless an extension applies.

- Documentation owner: keep appointment documents, tax records, filed returns, and correspondence in one organized file.

- Beneficiary communication lead: give clear status updates so expectations stay aligned.

| Phase | Primary objective | Key deliverable | Handoff to CPA or attorney |

|---|---|---|---|

| 1 | Confirm filing authority | Authority file (will, court appointment, or property-control facts) | Escalate immediately if no surviving spouse or appointed representative is in place |

| 2 | File the decedent's final return correctly | Signed final return with death clearly indicated | Share prior returns, income records, and filing-status facts for review |

| 3 | Keep filing lanes clean | Workpapers showing how items were classified and who signs | Escalate if classification or signature responsibility is unclear |

| 4 | Close with proof | Filing copies, refund-claim support, notices log, and closure record | Request final legal or tax review if unresolved probate or tax issues remain |

Critical checkpoints:

- If there is no appointed representative and no surviving spouse, the person controlling the decedent's property must file and sign as personal representative.

- On a paper return, write "deceased," the decedent's name, and the date of death across the top.

- If you are court-appointed, attach proof of appointment.

- If you are not court-appointed and are claiming a refund, include

Form 1310.

Escalate before filing if any of these apply:

- You are not sure who has filing authority or signature responsibility.

- There is no surviving spouse or appointed representative, and control of the decedent's property is unclear.

- You are unsure whether proof of appointment or

Form 1310is required for your filing. - You cannot confidently classify an item into the correct filing lane.

Close the estate for risk control, not just completion. Keep a full audit trail, confirm what was filed and when, log and resolve notices, document beneficiary communications and distributions, and record formal signoff that the estate file is ready to close.

For broader cross-border planning context, see The Tax-Efficient Repatriation Blueprint for US Expats Returning Home.

If this process highlighted broader cross-border compliance and record-keeping needs, review operational workflows and coverage details in the Gruv docs.

Frequently Asked Questions

What is the difference between Form 1041 and Form 706?

Form 1041 reports income the estate earns after death. Form 706 handles federal transfer-tax calculations. If assets are generating post-death interest, dividends, rent, or similar income, that belongs on the estate income-tax side. If the question is whether the estate crosses the transfer-tax filing threshold for the year of death, that belongs on the Form 706 side.

What should you file first?

There is no universal first form for every estate. If the decedent had an individual filing obligation, start the final personal return process. If post-death income exists, get the EIN and open the Form 1041 track right away. If transfer-tax filing may apply, calendar the Form 706 deadline immediately. If duties are unclear, especially in cross-border situations, escalate to an estate CPA or attorney before any deadline passes.

How do you handle foreign bank or investment accounts?

Run two separate checks: income-tax reporting and FBAR reporting. If the estate is a U.S. person and foreign accounts exceeded $10,000 in aggregate at any time during the year, file FBAR (FinCEN Form 114), even if those accounts produced no taxable income. The FBAR is due April 15 with an automatic extension to October 15. Escalate if ownership or control of the account is unclear or the estate has cross-border entities.

What is a step-up in basis, and why does it matter?

Inherited property basis is generally the fair market value at date of death, subject to applicable valuation-election rules. That means later gain is usually measured from that inherited basis, not from the decedent’s original purchase price. Keep valuation support organized now, because beneficiaries may need it long after the estate closes. Escalate if valuations are disputed or an asset is difficult to price.

Do you have to file `Form 1041` if the estate has very little income?

If estate gross income is more than $600 for the year, you must file Form 1041. If income is below that, do not assume the file is closed. Review whether nonresident-beneficiary facts create additional filing checks, including possible Form 1040-NR obligations in context. For calendar-year estates, Form 1041 is due April 15 of the following year; for fiscal-year estates, it is due on the 15th day of the fourth month after year-end, with an automatic 5-month extension available. Escalate if you are unsure about gross-income classification or beneficiary residency status.

Can you pay yourself an executor fee?

Yes, but treat executor compensation as taxable income to you. In a typical non-business case, report it on Schedule 1 (Form 1040), line 8z; if your executor activity rises to a trade or business, reporting can shift to Schedule C with self-employment treatment. If you plan to take a fee, model the tax effect before payment. Escalate before paying yourself if the estate is contested, has nonresident beneficiaries, or the reporting treatment is not clear.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

Estate Planning for Digital Nomads: Legal Intent and Cashflow Continuity

Treat estate planning for digital nomads as a two-part continuity system: legal intent plus operational execution, so your business keeps moving when you cannot. The common trap is thinking, "I have a will, so I'm covered." If you run a business-of-one, cashflow, logins, and process often live in your head until you deliberately externalize them.