Quick Answer

Yes - an e-2 visa for entrepreneurs can work if you build and document a real U.S. enterprise before filing. Confirm treaty-country nationality, show at least 50 percent treaty-country ownership with genuine control, and prove capital is commercially at risk rather than parked. Then keep forms, financial records, contracts, and interview responses consistent so an officer can verify the same case across your file.

Stage 1: The Viability Audit - Is the E-2 Your Winning Move?#

The E-2 is a strong option only if you can clear five gates before major spending: treaty nationality, ownership and control, a real develop-and-direct role, an enterprise that is real and operating and not marginal, and nonimmigrant intent. If any gate is weak, stop and fix the structure first. Use these plain-language checks first:

- Treaty nationality: Pass if you are a national of a country with a qualifying U.S. treaty basis. Pause if you are relying on residence instead of nationality.

- Ownership and control: Pass if the business is at least 50 percent owned by persons with the treaty country's nationality and your stake gives you real control. Pause if governance, side deals, or entity layers blur who actually controls decisions.

- Develop and direct: Pass if you are entering to run and steer the enterprise you invested in. Pause if the file makes you look passive.

- Enterprise viability (real and operating; not marginal): Pass if the business is a real and operating commercial enterprise with present or future capacity to generate more than minimal living income. Pause if it looks like a paper setup or only supports minimal living income.

- Nonimmigrant intent: Pass if your record consistently reflects intent to depart when E status expires or terminates. Pause if other filings or statements point the other way.

Keep these terms straight:

- Develop and direct: You are leading operations, not just funding them.

- Marginal enterprise: Under 8 CFR 214.2, the business lacks present or future capacity to produce more than minimal living income.

- Nonimmigrant intent: You must maintain intent to depart when E status expires or terminates.

- Common freelancer misconception: E-2 is not a blanket freelance work authorization. A solo founder may still qualify, but the record should show a real and operating commercial enterprise, not only personal labor routed through an entity.

| criterion | what officers look for | evidence to prepare | red flags to fix before filing |

|---|---|---|---|

| Treaty-country nationality | Qualifying nationality and treaty-country ownership alignment | Passport, cap table, formation and ownership records, owner nationality evidence | Residence presented as a substitute for nationality, no clear treaty-country majority |

| Ownership and control | At least 50% treaty-country ownership and real decision control | Operating agreement, shareholder records, voting and control terms | Hidden dilution, side letters, convertibles, governance deadlocks |

| Develop and direct | You will direct day-to-day and strategic operations | Role description, org chart, management duties, business plan | Passive investor profile, someone else clearly running core operations |

| Real and operating enterprise | Actual commercial operations, not a paper entity | Business records, commercial activity evidence, customer and vendor materials, LOIs where relevant | Formation-only footprint, no credible operating activity |

| Not marginal | Capacity now or in the future to exceed minimal living income | Financial model, revenue logic, growth and hiring plan, supporting commercial evidence | No path beyond founder-only income, single-point dependency, unsupported narrative claims |

For solo founders, use a practical risk signal: if the business stops when you stop delivering client work, viability may look weaker. The case usually gets stronger when the file shows enterprise traits such as market-facing operations, credible demand evidence, and a path to generate income beyond your own billable time.

Position intent carefully#

Intent to depart should read consistently across the whole file, not just as a sentence on a form.

- Affirm clearly: this is a temporary, nonimmigrant classification, and you will depart if status ends.

- Avoid overstating: do not frame E-2 as automatic U.S. residency, a green card grant, or a personal freelance work authorization.

- Escalate early: if prior filings, public statements, ownership records, or narrative framing create mixed signals on control or departure intent, align the record with counsel before filing.

- Use current-rule checks where needed: if your fact pattern turns on timing or threshold details, confirm current requirements with counsel before you file.

Final gate before Stage 2: every core claim above should be backed by documents, not just stated in a cover letter. Related: 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

Stage 2: The Capital Strategy - How Much is "Substantial" for Your Business?#

Start with the right rule: for E-2, "substantial" is not a fixed dollar floor. Your investment has to make sense for this specific business, be committed in a verifiable way, and be enough to support successful operations.

Think of this as the capital version of Stage 1. Your file must show both commitment and readiness. It is not enough to have money available. The money must be tied to launching and running a real operating enterprise.

Use proportionality, not rumor#

The core test is proportionality. Officers compare what you invested to what it costs to establish a viable business, or to buy an existing one. Because this test compares your investment to total business cost, lower-cost models may need clearer evidence that core startup costs are already spent or irrevocably committed. Higher-cost models may still be substantial when the committed amount is clearly tied to launch and operations.

| business model | typical cost structure | investment posture expected |

|---|---|---|

| Solo service firm | Low hard-asset cost, with heavier spend on setup, software, marketing, and early operating capacity | Core launch costs should be spent or irrevocably committed. Large idle balances with little business use are weak. |

| Small agency with staff | Moderate setup cost plus payroll runway, systems, customer acquisition, workspace, and vendors | Commitments should show the business can open and operate as presented in the filing. |

| Inventory or equipment-heavy business | Higher upfront spend on equipment, inventory, buildout, and lease obligations | A lower percentage can still be substantial if committed funds are clearly tied to launch and operations. |

| Existing business acquisition | Purchase price plus working capital and transfer costs | The file should connect the price paid and post-close operating funds to the operating plan. |

Decision point: commit now to defensible, launch-critical spend and delay optional growth spend until the core readiness case is clear. Uncommitted or revocable funds sitting in an account are usually weak support.

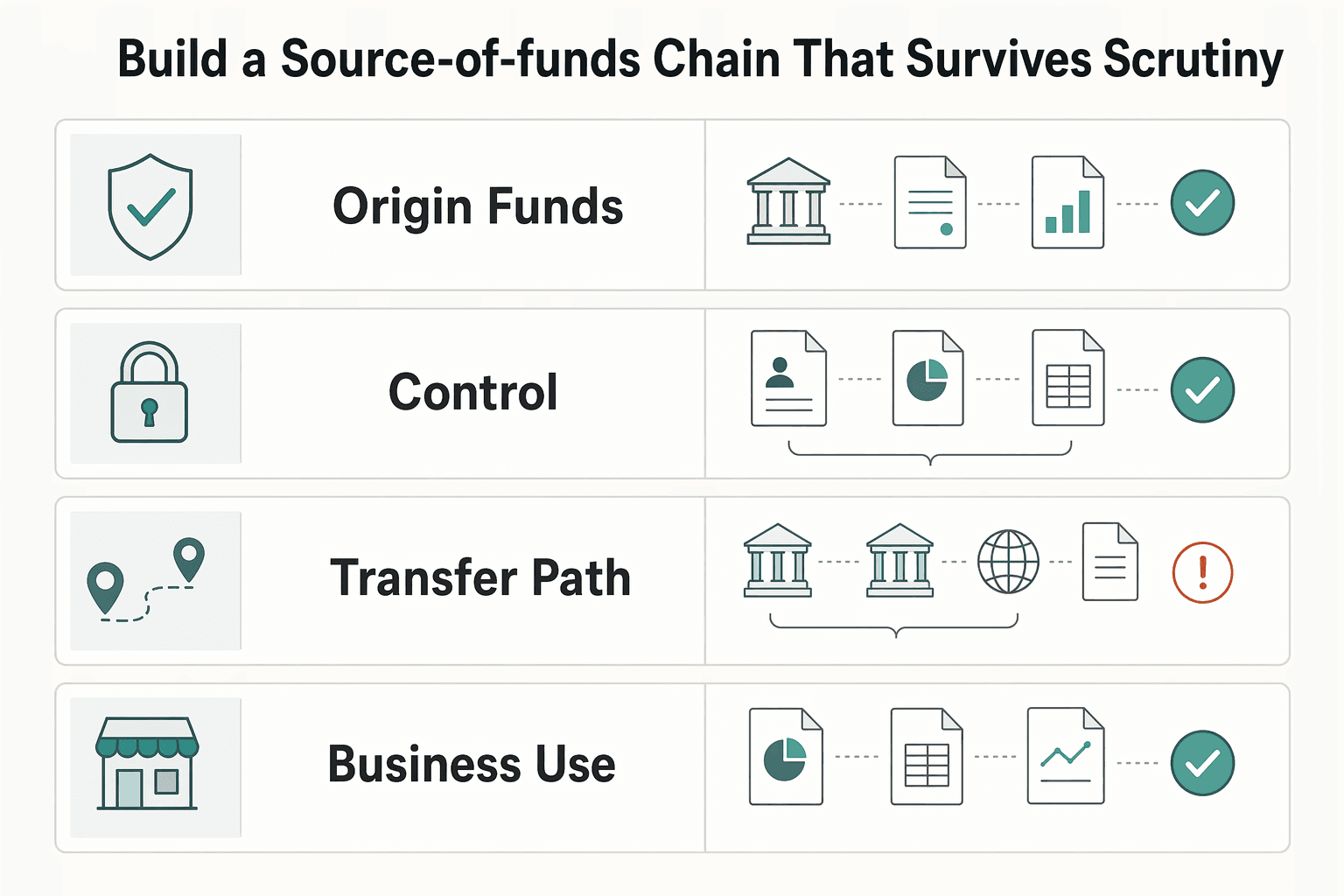

Build a source-of-funds chain that survives scrutiny#

Amount alone is not enough. You need a clean documentary chain showing origin, control, transfer path, and business-use destination.

| Chain step | What to show | Records named |

|---|---|---|

| Origin of funds | Where the funds came from. | Earnings; property sale; inheritance; business sale; loan documentation where relevant |

| Possession and control | You controlled the funds before investment. | Bank records; savings evidence; financial statements |

| Transfer path into the U.S. | Each movement step into the U.S. | Wire confirmations; bank drafts; transfer receipts; exchange records; account statements |

| Business-use destination | The funds were invested in, or irrevocably committed to, the enterprise. | Business bank statements; contracts; receipts; invoices; titles; payment evidence |

- Origin of funds: Show where the funds came from.

- Possession and control: Show that you controlled the funds before investment.

- Transfer path into the U.S.: Show each movement step into the U.S.

- Business-use destination: Show that the funds were invested in, or irrevocably committed to, the enterprise.

Broken chains raise questions, especially when the documents do not clearly explain fund origin, movement, and business use.

How service-business spending strengthens or weakens the record#

For service businesses, the spending pattern can matter as much as the headline total. Prioritize costs that clearly support launch and operations, and keep personal spending separate from the investment story.

| spend item | how it usually reads | evidence to keep |

|---|---|---|

| Company formation, legal setup, licensing, accounting setup | Supports launch readiness when tied to the operating plan | Engagement letters, invoices, payment proof |

| Essential hardware and software needed to deliver services | Supports operational capacity when tied to the model | Receipts, subscriptions, vendor contracts |

| Website, branding, customer acquisition spend | Helpful when aligned with the business plan | SOWs, invoices, ad contracts, payment proof |

| Lease or coworking, insurance, core vendor contracts | Helpful when actually required to operate | Lease, policy, signed contracts, bank proof |

| Personal relocation, household purchases, living costs | Typically treated as personal spending, not core enterprise investment support | Keep separate from core investment support |

| Cash parked without binding business use | Weak support because the funds are not committed | Convert to documented business use or commitment |

Final timing check: funds can qualify before issuance when they are irrevocably committed and contingent only on visa issuance. If your case has a complex funding or transfer history, flag it for attorney review before filing.

Once the amount and the money trail make sense, the next question is how to commit capital without taking avoidable loss before a decision.

Stage 3: The Commitment Protocol - How to Invest "At-Risk" Without Risking Everything#

The goal here is to show real, credible commitment without taking unnecessary downside before a decision. Commit enough capital to prove the business is real, then structure major obligations so release depends on visa issuance.

In plain language, at-risk means your capital is exposed in the commercial sense with a profit objective. Irrevocably committed means the funds are genuinely tied to the enterprise, not left fully revocable in your personal control. Contingent commitment means the funds are already bound, but release is conditioned only on visa issuance. That distinction matters because E-2 can cover investors who are actively in the process of investing, not only those who have already spent everything.

Use a stepwise commitment ladder#

The safest approach is usually staged commitment. Spend first on items that prove the business is real, lock in larger obligations with visa-conditioned terms, and hold back optional expansion costs until the core case is already strong.

- Commit foundational spend first.

Pay core launch costs that demonstrate an operating business, and keep matching proof: invoices, wire or check records, and bank debits. Checkpoint: if each payment does not match a business invoice and bank record, pause and fix the paper trail first.

- Bind major commitments next.

For larger items such as lease obligations, equipment, inventory, or acquisitions, use signed commitments that are binding and conditioned only on visa issuance, with escrow where appropriate. Checkpoint: if contract language allows broad non-visa walk-away rights, it may look optional rather than committed.

- Defer optional expansion spend.

Delay nonessential growth costs until the filing already shows a viable operating case. Checkpoint: if a cost does not improve current readiness evidence, treat it as deferrable.

| commitment method | when useful | evidence created | main downside |

|---|---|---|---|

| Expense already paid | Core launch and operating essentials | Invoices, canceled checks or wires, bank statements with matching debits | Hard to recover if refused |

| Escrow | Large transfers, acquisitions, high-value commitments | Signed escrow agreement, transfer records, bank records, related agreement | Weak if release or return terms are vague |

| Contract with contingency | Lease, equipment, inventory, purchase agreements | Signed, dated agreement showing a visa-conditioned obligation | Overbroad contingencies can look nonbinding |

Get escrow right on paper#

Escrow only helps if the terms are clear. The agreement should explicitly confirm how funds will be distributed if the visa is issued and what happens if it is not issued. Some posts specifically expect that level of clarity and may accept a signed purchase agreement plus a binding escrow agreement.

Include a complete escrow package in the filing: signed escrow agreement, transfer and bank records, and the underlying contract. Do not treat interview scheduling as approval, and do not trigger release based on scheduling alone.

Pre-filing readiness check#

Before filing, confirm you can show:

- Paid startup expenses with matched payment records

- Signed, dated business agreements

- Lease and payment evidence when premises are part of the model

- Equipment or inventory purchase evidence when relevant

- Major-fund commitments structured so visa issuance is the only operative remaining condition

If post-specific rules or jurisdiction-specific wording may affect the commitment language, pause before crossing the point of no return and verify with counsel. Consular instructions vary by post.

Once the capital is properly committed, your next job is to package the case so an officer can verify it quickly.

Stage 4: The Dossier Assembly - Telling a Story of Success#

Your job now is to make verification easy. The strongest E-2 file is a business case, not a paperwork dump. Put one clear summary page first, then group evidence by eligibility element so an officer can confirm each point quickly.

Post rules differ, so lock the format first and then refine the substance. Requirements can conflict by location. France describes a one-PDF submission capped at 10 MB and says E-2 investors there do not need DS-156E. Colombia requires DS-156E Parts I-III. Mexico allows up to 100 single-sided pages with a 25 MB email cap. Belgium sets a 50-page cap. Italy uses seven attachments with a 5 MB limit per attachment. If you are filing through USCIS instead of a consular post, follow the USCIS evidence checklist for that path.

Build the file around eligibility claims#

A good summary page should map each legal claim to its proof. That lets the reviewer move from claim to evidence without hunting.

| claim | supporting file | what it proves | consistency check |

|---|---|---|---|

| Real, active, operating for-profit enterprise | Entity filings, operating records, and commercial activity evidence (for example, vendor or client contracts) | Bona fide enterprise | Legal name, address, and start date match across the plan and exhibits |

| Substantial investment | Bank statements, wire records, invoices, escrow agreement, signed contracts, proof of spend | Capital is invested or actively being invested and is commercially at risk | Investment totals match the summary, plan uses, and transaction trail |

| More than marginal | Five-year business plan where required, projected expenses and profits, hiring plan | Business is more than a vehicle for the investor's living | Hiring and revenue logic align with financial projections |

| Develop and direct | Operating or share documents, ownership records, role description, resume, relevant credentials | You are in a position to develop and direct the enterprise | Ownership percentage, title, and control rights match forms and entity records |

| Treaty-country ownership | Ownership table, owner nationality documents | Treaty-country ownership requirement is met where applicable | Ownership percentages reconcile across every filing artifact |

Make the business plan do adjudication work#

The plan should read like evidence-backed logic, not a pitch deck. Where posts ask for it, the plan may need a five-year horizon with projected expenses and profits and a path to profitability within that period. Tie the projections to concrete operating steps.

Keep four threads explicit:

- Viability narrative: what you sell, who buys, and why the U.S. entity is operationally credible now

- Hiring intent: when hiring starts, which roles come first, and what supports the payroll assumptions

- Develop and direct: how control is documented, including ownership and control evidence, and why you can run the business

- Non-marginality: how the enterprise grows beyond supporting only your personal living

If you include foreign-language records, include full certified English translations.

Run a consistency check before filing#

Contradictions can delay or weaken a file even when the package is large. Before filing, verify:

| Check area | What must match |

|---|---|

| Names and addresses | Forms, entity documents, contracts, invoices, bank records, and plan narrative should be identical. |

| Ownership and nationality details | Operating or share records, identity documents, and filing forms should match. |

| Funds trail | It should be traceable from source to U.S. deployment without unexplained gaps. |

| Dates | Formation, account opening, commitments, transfers, and startup milestones should follow a coherent timeline. |

| Summary totals | They should reconcile exactly with the underlying records, including escrow and staged payments. |

If any one of those points conflicts, fix it before filing.

Assemble by priority#

If time is tight, build in this order:

| Priority | Include | Use |

|---|---|---|

| Mandatory for your filing path | Required post or USCIS format and forms; lead summary page; ownership and nationality proof; substantial-investment evidence; complete funds trail where requested; core entity records; develop-and-direct evidence; certified translations where needed | Required for your filing path |

| Strongly helpful | Five-year plan where expected; profitability and hiring projections; premises and operations evidence; contracts showing active commercial activity | Strengthens the core file |

| Contextual | Additional corroboration only when it directly strengthens a weak point and stays fully consistent with the core file | Use only when it directly strengthens a weak point |

The best dossier is not the biggest one. It is the one that lets a reviewer verify each claim quickly and without contradictions. A well-built file should make the interview feel more like confirmation than rescue.

For a step-by-step walkthrough, see Choosing the Right Residency Path After Spain's Golden Visa Closure.

Before you lock your interview prep, run a final documentation and timing check with this practical planning template: Visa Cheatsheet for Digital Nomads.

Stage 5: The Consular Interview - Embodying the CEO Mindset#

At the interview stage, you are not making a new pitch. You are proving that your spoken case matches the filed record on intent, business viability, investment commitment, and legal compliance.

If your case requires an interview, the process is not complete until you appear before a consular officer. Treat it as an eligibility check. The officer is testing whether the operator in the room matches the evidence in the dossier.

Readiness checks before interview day#

Many interview mistakes are preventable. The fix is disciplined preparation, not a bigger speech.

- Lock your message into five clear answers: what the business does, who pays, what you invested, how the funds are at risk, and how you will develop and direct the enterprise.

- Recheck DS-160 details line by line against your file so dates, addresses, ownership, titles, and travel history do not conflict at interview.

- Confirm post-specific form expectations for your case and role, then align every spoken answer to those submitted forms.

- Practice a concise structure: direct answer first, one record-backed fact second, then stop.

- Memorize where the core proof sits in the dossier: funds trail, contracts, operating evidence, ownership and control records, and the five-year plan if submitted.

- If you need an interpreter, verify that post's current rule set in advance.

Core interview prompts#

| likely officer prompt | what the officer is testing | dossier evidence to reference | concise response framework |

|---|---|---|---|

| What does your company do? | Real, operating enterprise | formation and operating records, client and vendor contracts, operating activity evidence | Define the product or service, identify the buyer, explain how revenue is generated now |

| How much have you invested and where did it go? | Substantial investment and at-risk commitment | bank statements, wire records, invoices, escrow or committed contracts | State the total invested, show the main uses, explain why the funds are commercially committed |

| What is your role in the business? | Develop-and-direct control | ownership records, governance and role documents, resume and experience evidence | State your ownership or control position, decision authority, and daily leadership role |

| How does this business avoid being marginal? | Non-marginality | five-year plan, hiring plan, expense and profit projections | Explain the hiring sequence and growth path beyond supporting only your personal living |

| What are your plans when E status ends? | Nonimmigrant intent consistency | DS-160 answers and intent statements already in the file | Confirm intent to depart when E status ends and keep the answer consistent with the filed record |

Readiness signals in high-risk areas#

Use these signals when you practice:

| area | generally safer signal | concern signal |

|---|---|---|

| Marginality | You can explain hiring and growth logic tied to your plan | You only describe personal self-support with no credible growth path |

| Funds at risk | Funds are committed to real business use and traceable in the records | Funds sound parked, reversible, or not clearly under your control |

| Develop and direct | You describe active control and operating decisions | Your role sounds passive, nominal, or outsourced |

| Nonimmigrant intent | You describe temporary E status and intent to depart when status ends | You frame E-2 as permanent residence |

Consistency controls#

Consistency is the real risk control. Keep every interview claim aligned with the submitted documents, avoid speculative numbers you cannot support, and do not expand the story beyond what the file proves. Bring the required interview documents, be ready for additional document requests, and avoid locking travel before issuance.

The E-2 Visa Isn't a Form to Fill - It's a Business to Launch#

E-2 approval turns on a credible operating business case, not form completeness alone. If your file cannot show treaty-country eligibility, substantial capital in a bona fide U.S. enterprise, capital truly at commercial risk, a lawful source of funds, and your role to develop and direct the business, better paperwork will not fix the gap.

The real standard is launch readiness. Before filing, you should be able to show a viable model, funds placed at commercial risk, and a clear source-and-path-of-funds record. Your interview narrative should also match your documents line by line. If an officer picks any transfer, contract, ownership record, or forecast assumption, you should be able to explain it quickly and consistently.

Decide your next step like an operator:

- Proceed now if treaty nationality is verified, capital is substantial and exposed to commercial risk, the enterprise is not marginal, and your evidence set supports lawful funds plus a real develop-and-direct role.

- Pause and fix gaps if the business is still mostly conceptual, funds are not yet clearly at risk, or the source-of-funds chain is incomplete.

- Reconsider strategy if you cannot support treaty eligibility, cannot show a real develop-and-direct role, or the business is likely to be viewed as self-support-only.

| Workstream | What "ready" looks like | Common failure signal |

|---|---|---|

| Treaty eligibility | Nationality confirmed against the current treaty-country list | Filing before verifying current treaty-country status |

| Investment | Capital is substantial for this business and placed in a bona fide U.S. enterprise | Chasing a generic minimum dollar figure |

| Risk and commitment | Funds are subject to possible loss in a real operating business | Money parked safely or terms that allow easy reversal |

| Source of funds | Clear lawful trail from origin to U.S. business use | Missing links between transfers or unclear origin |

| Business case and role | Non-marginal operating case and you will develop and direct operations | Passive-owner narrative or self-support-only economics |

If you are outside the United States, the normal route is visa issuance before travel. If you are already in the U.S., USCIS provides change or extension through Form I-129. Treat the filing route as logistics, not a substitute for readiness. Build the business first, then file the case that business can support.

If you want a compliance-first setup for collecting client payments and running cross-border payouts once your move is in motion, talk with Gruv.

Frequently Asked Questions

What is a "substantial investment" for an E-2 visa?

There is no universal dollar minimum. "Substantial" is judged in proportion to the total cost of this specific business and whether the amount makes the enterprise credible and operational. Before filing, verify that your full startup or acquisition budget, what is already paid, what remains unfunded, and your bank records, invoices, contracts, and business plan all align.

How do I prove my investment is "at risk"?

"At risk" means the capital is exposed to normal commercial gain or loss in pursuit of profit, not parked safely. Officers also look for funds that are already invested or irrevocably committed. Before filing, make sure your source-and-path-of-funds records, wire evidence, escrow or purchase terms, proof of real business use, and control of the funds are all clear.

Can an E-2 visa lead to a green card?

Not by itself. E-2 is a nonimmigrant category for temporary stay, so it is not a direct permanent-residence path. Keep your DS-160 and supporting statements consistent, and avoid framing E status as an automatic bridge to permanent residence.

How long can I stay in the U.S., and what affects renewal?

There is no guaranteed long-term stay from one approval. Ongoing eligibility depends on continued qualification, continued develop-and-direct control, intent to depart when E-2 status ends, and the business not being marginal, meaning it has present or future capacity beyond minimal living income. Before filing or renewing, check current treaty-country validity details, plus operating evidence, ownership and control records, updated financials, hiring progress, and whether actual performance still matches the original case theory.

Can my spouse work?

A qualifying E dependent spouse may be employment authorized incident to status, but the document record still matters. Since January 30, 2022, an unexpired I-94 with E-2S can be used as employment-authorization evidence, and some spouses still file Form I-765 for an EAD. Verify the spouse's exact I-94 class code, expiration status, employer I-9 process, and that you are applying spouse rules rather than assuming the same rule for all dependents. Weak verification creates avoidable E-2 problems. If any answer depends on "we will explain it later at interview," treat that as a red flag and fix the evidence pack first.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The 2026 Global Digital Nomad Visa Index for 50+ Countries

Start with legal fit, not lifestyle filters. The practical order is simple: choose a route you can actually document, then decide where you want to live. That single change cuts a lot of wasted comparison work and stops you from falling in love with places that were never a real filing option.

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

The Best Podcast Hosting Platforms for Beginners

**Pick podcast hosting like an operator: optimize for control, continuity, and clean workflows, not whatever looks appealing on a pricing page.** Podcast hosting is infrastructure. What you choose at signup sits upstream of your RSS feed, Apple Podcasts listing, analytics, monetization options, and how painful it is to change systems later.