Quick Answer

Use dunning-kruger effect and imposter syndrome as a risk check, not a personality label. Compare confidence with evidence from recent deliverables, revision counts, and client feedback. Run a one-page proof log before pricing or proposals, confirm goals and assumptions in writing during intake, and route unclear briefs into paid discovery. If a request reaches legal or tax territory beyond your track record, refer it to a specialist instead of improvising.

The Diagnostic: Your Mental Biases as Unseen Balance Sheet Liabilities#

Misreading your own ability is not an abstract mindset issue. For a freelancer, it can show up in pricing, scope decisions, delivery promises, and confident calls made outside your current expertise.

What many freelancers describe as imposter-syndrome-like self-doubt often shows up as under-crediting. You discount evidence you already have, assume your work is worth less than it is, or treat normal uncertainty as proof that you are not ready. The Dunning-Kruger effect, while still debated and not a settled law of human behavior, is a useful label for the opposite pattern. Low knowledge can feel like enough knowledge because you cannot yet see your own mistakes. Framed another way, dunning-kruger effect and imposter syndrome both distort judgment, just in opposite directions.

| Pattern | How it can show up in day-to-day freelance work | What to check first | First corrective action |

|---|---|---|---|

| Underconfidence | You cut your price before the client pushes back, keep revising solid work, or accept vague scope because you feel lucky to be hired | Are you ignoring evidence of outcomes you already deliver? | Before sending a proposal, list the specific outcomes or skills the client is actually paying for |

| Overconfidence | You estimate unfamiliar work quickly, assume a complex issue is simple, or commit before you can explain the main risks | What assumptions are you making without verification? | Write down what you do not know yet and what you will verify before agreeing |

| Mixed pattern | You doubt your core service but feel oddly certain in areas you rarely handle | Where do you have real evidence vs. brief exposure? | Separate "I have evidence" from "I have only touched this briefly" |

One checkpoint helps on both sides. If you spent only a few days with a new tool, market, or rule set and can do the equivalent of "10 to 15 sentences," that is early progress, not fluency. The mirror check matters too. If something feels easy to you, that may be because you are skilled, not because anyone could do it.

Once you can name the pattern, stop relying on mood. The next step is to calibrate your judgment with evidence you can actually use. For the broader mindset framing, see The 'Mental Game' of Freelancing Blueprint: From Imposter Syndrome to Confident CEO.

The Calibration: Forging Internal Systems of Proof#

Use systems, not mood, to make pricing and scope decisions. These three controls force slower, more deliberate thinking before you commit.

| System | Bias it corrects | Business decision it improves | Failure mode if skipped |

|---|---|---|---|

| Proof dashboard | Underconfidence | Pricing, proposals, sales conversations | You downplay proven strengths and sound generic about your value |

| Rate escalation policy | Underpricing tied to self-doubt | Rate updates, package design, negotiation | Pricing falls behind your actual value and complexity load |

| Post-project debrief | Overconfidence and fuzzy self-critique | Scope boundaries, service claims, next-project decisions | You repeat avoidable mistakes or label skill as luck |

Proof dashboard#

Treat your proof dashboard as an evidence file, not a motivation file. Review it before proposals, renewal conversations, and any call where you need to explain your value clearly.

Keep inputs narrow and verifiable: outcome notes, client emails, testimonial screenshots, links to shipped work, before-and-after metrics, and a short note on what you specifically did. If a result depends on a benchmark, note that the benchmark must be verified against current evidence before use.

Use a cadence you will actually keep, such as before sales activity and during a recurring admin block. Decision trigger: when you think "I might be overcharging" or "I might be more advanced than I am," check the evidence first. If you only learned a new tool or rule set a few days ago and can explain about 10 to 15 sentences, tag it as early familiarity, not marketable expertise.

Rate escalation policy#

Make your rate policy rule-based, not feeling-based. You do not need a fixed percentage; you need preset review points and evidence-based decisions.

Use the same inputs every review: recent outcomes, revision load, demand at current pricing, project complexity, and one external benchmark marked "verify before use." Keep a consistent cadence, for example monthly or quarterly. Trigger a pricing decision when the same signals repeat, not when confidence swings up or down.

Post-project debrief#

Run a debrief while project details are still fresh. Your goal is to separate skill, luck, fit issues, and client-caused friction.

| Debrief prompt | What to capture |

|---|---|

| What produced the outcome? | Note what produced the outcome while details are still fresh. |

| Where were your assumptions wrong? | Record where your assumptions were wrong. |

| What should be added to future scope language? | Note what should be added to future scope language. |

| In newer areas, how do you catch blind spots early? | Ask a client, collaborator, or specialist to point out wrong assertions. |

Capture three things: what produced the outcome, where your assumptions were wrong, and what should be added to future scope language. In newer areas, add one correction loop: ask a client, collaborator, or specialist to point out wrong assertions so you catch blind spots early.

With these three controls in place, your self-assessment becomes usable evidence for the next step: screening risky briefs and setting cleaner scope boundaries. For a step-by-step walkthrough, see A guide to the 'Ben Franklin Effect' for building client relationships.

The External Threat: Using Dunning-Kruger as a Client Vetting Tool#

Once your own evidence is straight, apply the same discipline to client intake. If a prospect shows high confidence before the problem is clear, treat that as a potential scope and delivery risk until you verify the basics.

Use one lens: the gap between decision competence vs decision confidence. The point is not to judge personality. Your job is to check whether that confidence holds up when you ask for constraints, stakeholder input, and written assumptions.

What to watch for before you sign#

Stay with observable behavior in calls, briefs, and feedback:

- They call the outcome "simple," but cannot explain constraints, dependencies, or tradeoffs when asked.

- They push for a quote before goals, users, decision-makers, or source material are clear.

- They treat clarifying questions as delay instead of part of decision quality.

- They insist on a tactic or tool, but cannot define success criteria.

- Feedback is broad certainty ("just make it pop") without examples, evidence, or alignment.

- One confident contact wants to decide alone and blocks access to people who approve, implement, or use the work.

That last pattern matters because better decisions often involve stakeholder consultation before one person finalizes the call. If stakeholder access is blocked, assume higher uncertainty and scope accordingly.

Intake triage table#

Use this as a repeatable screen, not a diagnosis.

| Observable signal | Risk level | Validation question to ask next | Recommended action |

|---|---|---|---|

| "This is simple" + vague requirements | Medium | "Which constraints, approvals, or dependencies could change delivery?" | Proceed if specifics are clear; otherwise paid discovery |

| Rush to price before goals/inputs are clear | High | "What decision should this work support, and how will success be judged?" | Paid discovery |

| Dismisses clarifying questions | High | "Which assumptions do you want confirmed in writing before scope?" | Paid discovery; decline if written assumptions are refused |

| Demands a tactic without outcome criteria | Medium | "What problem does this solve better than alternatives?" | Proceed only with clear outcome and tradeoff |

| Single sponsor blocks stakeholder access | High | "Who will approve, use, or be affected by this work?" | Paid discovery or decline |

After the call, send a short written recap of goals, constraints, stakeholders, and assumptions, then ask for corrections before pricing. If they resist that step, take it as a signal to tighten scope or walk away.

Your pre-engagement workflow#

- Qualify first: problem, target outcome, decision owner, affected stakeholders, available inputs.

- Gate uncertainty: if answers are thin or contradictory, use paid discovery before full delivery scope.

- Set boundaries in writing: deliverables, review rounds, client responsibilities, and "not included."

- Log risk assumptions: capture dependencies like approvals, access, and data quality in proposal language.

Vetted clients plus clear boundaries give you stronger leverage in pricing and cleaner control during delivery, which is exactly what the next section builds on. We covered this in detail in A guide to the 'Mere-Exposure Effect' for building your personal brand.

The Deployment: Weaponizing Accurate Self-Perception for Profit and Control#

Accurate self-perception pays off when you use it the same way every time: in negotiation, in scope decisions, and in day-to-day operations. Lead with what you can verify, set boundaries in writing, and route work that sits outside your reliable control.

Negotiation#

Negotiate from evidence, not certainty theater. Because uncertainty is part of everyday and high-stakes decisions, your advantage is being explicit about what you know, what you have delivered, and what this fee includes.

| Part | Talk track |

|---|---|

| Evidence statement | On similar projects, I delivered [verified result] under [relevant constraint] using [specific method or deliverable]. |

| Business outcome | That supports [client outcome] by reducing [specific friction or risk]. |

| Scope boundary | This fee includes [deliverables/review rounds/client inputs] and excludes [out-of-scope requests]. |

Use this talk track on calls and in follow-up notes:

- Evidence statement

"On similar projects, I delivered [verified result] under [relevant constraint] using [specific method or deliverable]."

- Business outcome

"That supports [client outcome] by reducing [specific friction or risk]."

- Scope boundary

"This fee includes [deliverables/review rounds/client inputs] and excludes [out-of-scope requests]."

Before the call, pull 2-3 proof points from your own records and keep them with your proposal draft. In group settings, challenge assumptions without public takedowns; one public critical comment can shut down participation. If behavior keeps blocking progress, move the issue to written assumptions, private follow-up, or end the session.

Scoping#

Treat every change request with one repeatable decision flow. This is how you protect delivery quality and margin without sounding rigid.

| If the request is... | Next action |

|---|---|

| In scope | Confirm in writing and schedule it. |

| Adjacent and reliable for you | Re-scope first. Update fee, timeline, dependencies, and approval before work starts. |

| Outside core competence | Refer out. Keep ownership clear and protect the main engagement. |

| Control/compliance is unclear | Pause or decline. No written assumptions, no clear owner, or no required access means do not proceed. |

- Match the request to written scope.

If it is in scope, confirm in writing and schedule it.

- If adjacent and reliable for you, re-scope first.

Update fee, timeline, dependencies, and approval before work starts.

- If outside core competence, refer out.

Keep ownership clear and protect the main engagement.

- If control/compliance is unclear, pause or decline.

No written assumptions, no clear owner, or no required access means do not proceed.

Your minimum change log: request, impact note (time/fee), revised scope text, and written approval.

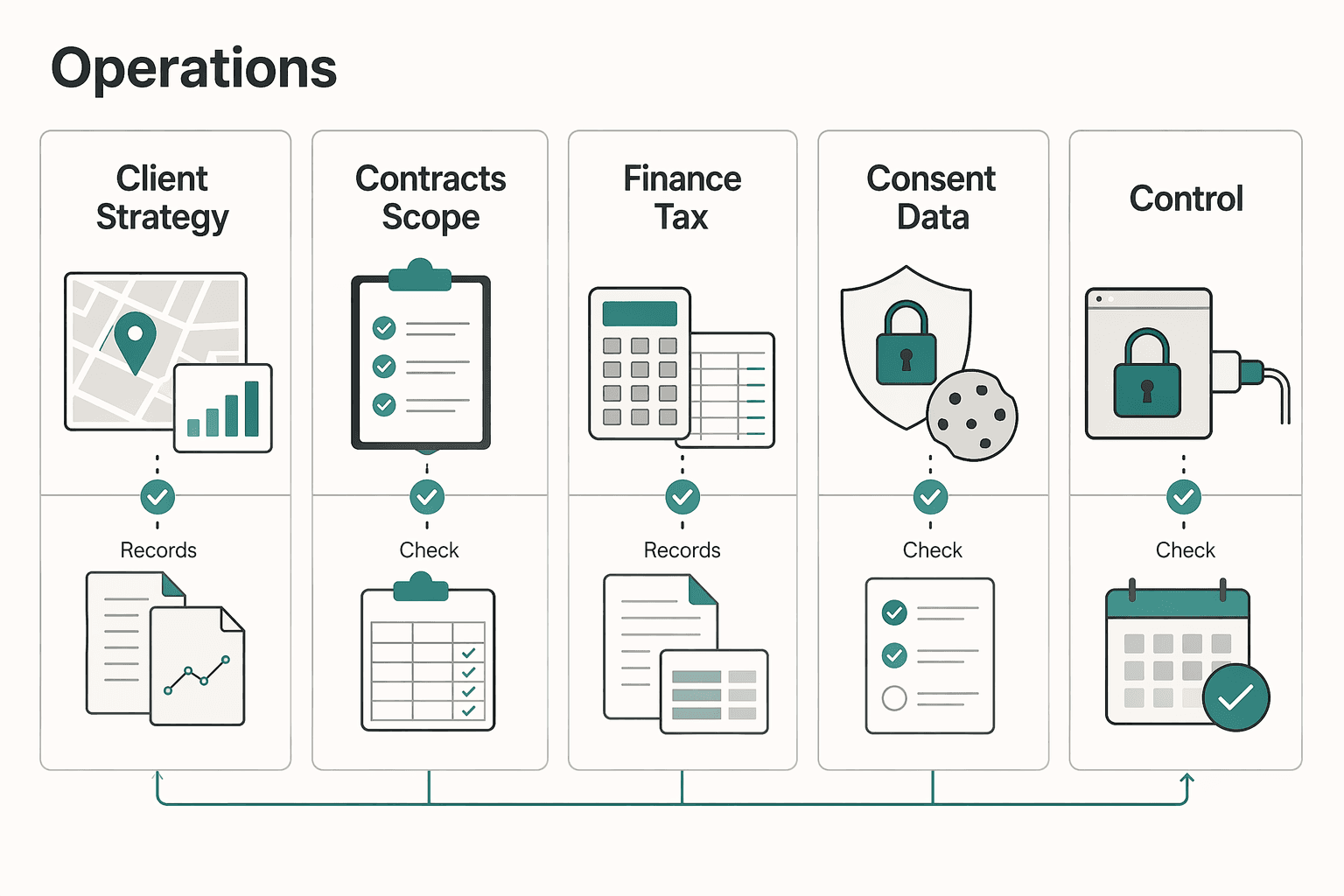

Operations#

Operational discipline keeps your self-perception accurate over time. Keep core work where you are consistently reliable, and hand off non-core areas when DIY starts reducing control, compliance, or delivery reliability.

| Function | Core vs non-core ownership | DIY risk signal | Outsourcing or handoff trigger |

|---|---|---|---|

| Client strategy and delivery | Core when you can show repeatable quality and clear decision ownership | You promise outcomes you cannot evidence | Quality inconsistency or capacity strain starts affecting delivery |

| Contracts and scope docs | Core only if you maintain accurate, current project terms | Scope disputes repeat | Disputes or complexity keep rising |

| Finance and tax admin | Core only if records and filings stay current | Reconciliations or filings slip | Visibility on cash, liabilities, or reporting drops |

| Consent and data-handling setup | Core only when you can separate required settings from optional tracking | You treat consent as cosmetic | Tool setup affects compliance or client trust beyond your comfort |

| Access control and recovery | Core only when permissions and recovery are reliable | Access and backup processes are ad hoc | A single failure would stop delivery or expose sensitive data |

Use concrete checkpoints. If a system distinguishes necessary cookies from analytical cookies, treat that as a control decision, not design polish. If a file or portal is password-gated, verify access before you depend on it. For a deeper process on client data handling, see GDPR for Freelancers: A Step-by-Step Compliance Checklist for EU Clients.

Used consistently, this approach builds trust through fewer surprises and cleaner boundaries while protecting margin and execution quality. For a mindset companion to this operating style, see A guide to 'Growth Mindset' for freelancers.

From Anxious Freelancer to Confident CEO#

You do not need a new identity. You need better decision quality. Treat both patterns as judgment risks in pricing, scope control, and the point where you stop guessing and bring in legal or tax support.

Diagnose#

First, find where your confidence and your evidence do not match. Across 4 studies, people often rated their abilities too favorably; in one reported gap, low performers were at the 12th percentile but estimated themselves at the 62nd. In your freelance work, that mismatch appears when you price quickly without checking comparable outcomes, or when you avoid a strong-fit project despite clear samples, client feedback, and repeatable results.

Calibrate#

Before important calls, run a short proof check. Keep a one-page evidence log with recent deliverables, revision counts, client comments, written assumptions, and approved changes. Then score your confidence for the current job and compare it with results from similar work. If you cannot support a capability claim with your own evidence, narrow scope, add discovery, or refer the work out.

| Moment | Anxious Freelancer | Confident CEO |

|---|---|---|

| Pricing | Discounts to reduce nerves | Sets price from past scope and evidence |

| Client intake | Accepts vague briefs | Confirms goals, risks, and assumptions in writing |

| Project scoping | Leaves gray areas open | States inclusions, exclusions, and change process |

| Post-project review | Skips review and moves on | Debriefs wins, misses, and friction points |

| Legal or tax issues | Keeps improvising outside core expertise | Escalates to specialists when expertise is thin |

Deploy#

Make calibration repeatable. Keep your evidence log current, apply written rules for pricing and scope, and run a short debrief after each project. Overconfidence is one failure mode, but paralysis from second-guessing is another. A routine keeps both in check: evidence first, boundaries in writing, and early escalation when work moves beyond your proven competence.

If you want a deeper dive, read How to Deal with Imposter Syndrome as a Freelancer.

Frequently Asked Questions

How do you tell the difference between imposter syndrome and the Dunning-Kruger effect?

The difference is the direction of the mismatch. If you have real evidence of ability and still feel inadequate, that points more toward imposter syndrome. If you feel very sure without tested evidence, you are closer to Dunning-Kruger territory. A useful next step is to rate yourself on three current service tasks, then compare those ratings with actual outputs, revision history, and client feedback.

Can you experience both at the same time?

You can, sometimes in different parts of your business. You might doubt your core service even when your work is strong, while being too casual in areas where your knowledge is thinner. Review one revenue-driving skill and one support function side by side, and check where your confidence is not matched by proof.

What is the fastest way to check whether your self-assessment is accurate?

Score your confidence first, then check it against measured performance. In freelance terms, that means comparing what you think you can do with what you actually delivered, how many revisions it took, and whether the client accepted the outcome. A one-page evidence sheet with recent wins, misses, and repeated friction points can be enough to start.

Does imposter syndrome mean you should say no to a project?

Not on its own. It is described here as a belief pattern, not a clinical disorder, and it often shows up in new situations or challenges. Decide from evidence, not nerves: list similar work completed, named risks, client dependencies, and any gap that needs support.

How can you spot this pattern in a client before signing?

Watch for strong certainty paired with weak problem definition. If a client dismisses your clarifying questions, gives an overly simple brief for complex work, or cannot define success in concrete terms, that can be a delivery risk. Put assumptions in writing before you quote, and do not start until the client confirms them.

When should you refer work out instead of stretching?

Refer the work when you cannot support your capability claim with your own evidence, or when the request creates delivery risk outside your real competence. If you use a numeric rule for referral decisions, verify it against current evidence before you rely on it. Document why you are referring it, then introduce a specialist instead of quietly improvising.

How do you communicate boundaries without losing trust?

Be specific, not defensive. Tell the client what your fee includes, what it excludes, and what happens if the request changes. That can read as control, not reluctance. Send the boundary in writing with the revised fee, timeline impact, or referral option.

What evidence should you keep so pricing and scope stay grounded?

Keep proof that is easy to verify: finished deliverables, short result summaries, client notes, before-and-after examples, written assumptions, and change approvals. One failure mode is agreeing to extras verbally and leaving your documents unchanged. Keep those records in the same folder as your proposal so you can check claims before a call, not after a dispute.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 6 external sources outside the trusted-domain allowlist.

- nist.gov/system/files/documents/2020/07/10/pnt-0015-a...trusted

- researchonline.ljmu.ac.uk/id/eprint/14905/1/2021SwettenhamDProf.pdftrusted

- brainzmagazine.com/post/three-signs-you-have-an-incompetent-man...external

- dokumen.pub/the-art-of-making-decisions-under-uncertaint...external

- gettherapybirmingham.com/category/psychologyexternal

- illinoisscience.org/blog/dunning-kruger-effect-imposter-syndromeexternal

- jakesmolarek.com/articles/ceo-imposter-syndromeexternal

- jakesmolarek.com/articles/what-is-career-coachingexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

GDPR Compliance Checklist for Freelancers Working With EU Clients

Start by separating the decisions you are actually making. For a workable **GDPR setup**, run three distinct tracks and record each one in writing before the first invoice goes out: VAT treatment, GDPR scope and role, and daily privacy operations.

How to Deal with Imposter Syndrome as a Freelancer

**Freelance impostor feelings can flare when your work lacks clear, documented boundaries-even when you *do* have talent.** You're the CEO of a business-of-one, and your job is to turn shaky moments into repeatable operations.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.