Quick Answer

Yes. brrrr method real estate can work if you treat Buy, Rehab, Rent, Refinance, and Repeat as separate gates with written stop rules. Use the 70% rule only to screen out weak deals, then re-underwrite with current costs, rent demand, and timing. Before moving forward, confirm your fallback for a delayed or denied refinance and keep one evidence file with invoices, lease records, and collections so decisions stay tied to facts.

Start Here With a Risk-First View of BRRRR#

Treat BRRRR as a staged cashflow business, not a shortcut to scale. It can help you build a portfolio of rental properties, but only when each step earns the right to the next one.

The upside is obvious. The failure points are not. BRRRR stands for Buy, Rehab, Rent, Refinance, Repeat. The usual path is short-term money up front, improvements to the property, a signed tenant, then a move into long-term debt. It can work when a cash-out loan returns enough capital to help fund the next purchase. It can break quickly when repair costs run over, loan terms tighten, or the market moves against your original numbers.

If you want predictable cashflow, treat each letter as a gate with a clear go or no-go rule. A growing portfolio is the result, not the excuse.

Use five gates, not one big bet#

Think about the sequence this way:

- Buy only when the deal still works after you pressure-test lease price, construction cost, and timing. If the numbers only hold under optimistic assumptions, pass before you own the problem.

- Rehab with the long-term loan story in mind, not just the after photos. If new issues show up, stop and rework scope and budget before you spend your way into a thinner margin.

- Rent based on actual demand, not the price you hope to get. If leasing is slower or weaker than expected, revise the holding plan and preserve cash rather than forcing the next step.

- Refinance as a decision point, not a guarantee. If the new loan is delayed or denied, hold longer, improve the property's income profile, or accept that this deal may not fund the next one yet.

- Repeat only when the current unit is stable enough to carry itself. If the first property still depends on perfect occupancy or fragile financing, do not stack a second risk on top.

At every gate, use the same checkpoint: re-underwrite from current facts, not the original spreadsheet. Verify the latest construction spend, current leaseability, and whether monthly cashflow still holds after financing costs. That habit catches a common self-inflicted mistake in this strategy: assuming the plan is still valid because the first version looked good.

Keep your evidence tight as you go. Save purchase numbers, contractor invoices, scope changes, lease details, and actual collections in one place. That discipline helps you see whether the property is becoming a durable asset or just an expensive project you are trying to rescue.

This guide stays on that risk-first track. At each stage, watch for the checkpoint, the red flag, and the fallback move if the step does not cooperate.

Related: How to Invest in Real Estate as a Digital Nomad.

Build the Right Mental Model Before You Spend#

BRRRR is a long-term, hands-on cycle, not a quick-profit play. You buy a distressed property, improve it, rent it, then use a cash-out refinance to recycle equity into the next deal. The strategy only works when the property still performs as a rental after rehab.

That is the key difference from flipping: a flip ends at sale, while BRRRR depends on stable rent and workable long-term financing. Before you spend beyond essentials, confirm two things: credible rental demand and a realistic refinance path after the work is complete.

Treat each letter as a separate gate, not one commitment made at closing:

- Buy only if the deal still holds under conservative assumptions.

- Rehab to support durable rental performance, not just cosmetic upgrades.

- Rent based on real demand, not hoped-for pricing.

- Refinance only when terms support sustainable cashflow.

- Repeat only after the current property is stable.

Be cautious with the "passive income" label. Early cycles are operationally heavy, and vacancy or execution issues can quickly change outcomes. It can become lower effort later, but only after occupancy and financing are stable.

You might also find this useful: A Guide to Using a Series LLC for Real Estate Investing.

Decide if BRRRR Fits Your Cashflow Profile#

BRRRR fits when your business can stay stable through delays, overruns, and vacancy without depending on best-case timing. If one delayed loan step, one renovation miss, or one vacancy stretch would strain core obligations, this is a pacing issue before it is a deal issue.

The biggest pressure point is refinance timing. A common BRRRR path assumes a cash-out refinance after a 6-12 month seasoning period, often around 75-80% loan-to-value on investment property. If that timeline slips or proceeds come in lower, cash you planned to recycle stays locked longer. If current obligations depend on that cash, your plan is carrying refinance risk your business may not absorb.

Run a blunt stress test#

Before adding another property, ask:

- Can your business cover normal obligations if vacancy lasts longer than planned?

- Can you absorb a 15-20% renovation overrun without destabilizing operations?

- If refinance is delayed or lighter than expected, can you hold the property and keep the business steady?

If any answer is no, slow the acquisition pace. A practical rule: if one failed Refinance would stress client-payment obligations, do not add another project yet. Conservative investors are often described as buying 1 property annually; that is a useful reference point when income is variable.

Keep one page with your current business burn, property carrying costs, expected rent, renovation budget, and refinance assumptions. Then rerun it with harsher inputs: 6-12 months to refinance, 15-20% extra spend, and a vacancy gap. That usually makes the fit decision clear.

Set your personal risk ceiling before you buy#

If your income swings month to month, build reserves first, then add another distressed project. BRRRR can build a portfolio, but it carries real execution risk, so growth should be systematic and tied to adequate reserves.

Write your ceiling before you close:

- Maximum active projects at one time

- Minimum reserve months for business and property obligations

- Clear trigger for when you stop self-managing and hire a property manager

Do not confuse being able to close with being ready to scale. Scaling beyond 2-3 properties annually depends on a reliable team, including lenders and property managers. If that team is not in place yet, grow slower and protect cashflow first.

Screen Deals With a Buy Gate You Can Defend#

Your buy gate should help you reject weak deals early, with written reasons you can defend later. For distressed, foreclosure, or pre-foreclosure leads, speed matters less than clarity and repeatability.

One BRRRR case study reports a 16-unit rental portfolio built over five years with a five-deals-per-year rhythm. The useful takeaway is not the headline count. It is the operating discipline: standardized renovations and documented progress.

Filter before you tour#

Do a desk-first screen before you schedule a showing. If you cannot get enough basic information to judge whether the deal is even reviewable, treat that as a stop signal, not a maybe.

For troubled leads, confirm control of sale, occupancy status, obvious condition issues, and any title, permit, or compliance questions that could complicate a later long-term loan. If the ownership or documentation chain is unclear early, assume higher execution risk.

Use a simple pre-tour evidence folder for each address. Include the lead sheet, photos, occupancy notes, disclosed repair history, and the records you checked. If you cannot assemble a usable file quickly, the deal is usually not ready for serious time.

Use quick screens to reject faster, not to justify a yes#

A rule-of-thumb screen can help you say no faster. It should not be treated as proof that a deal works.

After a lead passes a first-pass screen, pressure-test assumptions with conservative underwriting and downside cases. If the deal only works on optimistic rent, repair, or loan assumptions, you are underwriting a hope case. If you need to revisit your income-risk math, keep How to Calculate Cap Rate for a Rental Property nearby.

Write the one-page memo before the buy call#

A one-page buy memo keeps the decision evidence-based. Include the buy price range, rehab budget with contingency, expected income assumptions, downside case, long-term loan path, and explicit walk-away triggers.

Set walk-away triggers before inspection and negotiation fatigue kick in. If new scope, weaker income support, unresolved legal issues, or a shaky refinance path breaks your memo, pass and protect your cash for a cleaner deal.

We covered related structuring decisions in How to Structure a US LLC for Investing in Foreign Real Estate.

Control Rehab Scope So the Refinance Story Still Works#

To protect your refinance path, treat rehab scope as a financing control, not a design exercise. Each line item should clearly support one of three outcomes: safer condition, stronger rentability, or a more defensible value story for equity recovery and a new long-term loan.

Do not assume upgrades automatically raise appraisal value or guarantee refinance approval. BRRRR returns can tighten when repair costs expand or refinancing gets harder, so scope discipline is part of risk control, not just project management.

Separate required work from optional work#

Before work starts, split the budget into two buckets:

- Must-do repairs: items needed for safe, leaseable, dependable operation and a credible refinance file.

- Optional upgrades: items that are mostly aesthetic or preference-driven.

If costs rise, cut optional work first so required work stays funded. Many investors use short-term debt to buy and renovate, then refinance into long-term debt, and some hard-money structures run on five to 12-month terms. That makes scope creep a timing risk as well as a budget risk.

Put checkpoints in writing before work starts#

Use written controls instead of ad hoc decisions:

| Control | Requirement |

|---|---|

| Scope sign-off | Approve one scope that labels each item as safety, rentability, or value-supporting. |

| Change-order rule | Require written cost and schedule impact before approving added work. |

| Pre-lease readiness standard | Define what must be complete before you market for rent. |

Keep your rehab evidence together, including the approved scope, change orders, invoices, and before/after photos, so you can explain what changed and why. For the refinance step, a reliable renter and documented equity progress can strengthen the loan case. The main failure mode is overspending on cosmetic work that does not improve rentability or refinance outcomes.

Lock in Rent Operations That Protect Cashflow#

Cashflow protection at the Rent stage comes from consistent operations, not just a finished rehab. In BRRRR, occupied, income-producing properties are generally more refinance-friendly, so leasing and maintenance discipline directly affect your loan story.

Treat Rent as a system: consistent tenant screening, a written and enforceable lease agreement, and a documented maintenance workflow. Keep records as you go, including signed lease files, condition photos, rent ledgers, and repair logs, so you can show stable performance without relying on memory.

Be realistic about management capacity. Self-manage only if you can keep response times, collections, repair coordination, and compliance tasks reliable; otherwise use a property manager. Weak execution usually shows up as longer vacancy, weaker collections, higher turnover, and thinner documentation at underwriting.

Tighten the vacancy gap#

Fast tenant placement should be structured, not rushed. Use a vacancy-response checklist so your process stays consistent:

- Recheck asking rent against current comps and adjust quickly if inquiry volume is weak.

- Set clear marketing standards for photos, listing accuracy, and lead-response speed.

- Define turnover standards for cleaning, minor repairs, and ready-to-show timing.

- Track days vacant from move-out to signed lease and review the trend monthly.

One source describes stabilization as market rents plus at least 90% occupancy. That is a benchmark, not a universal lender rule, but the operating principle is durable: prioritize stable occupancy at supportable rent to protect NOI.

Watch the leading indicators monthly#

Review rent operations monthly using three indicators: collection reliability, repair burden, and net cashflow consistency. Collection reliability shows whether income is dependable, repair burden shows whether operating noise is rising, and cashflow consistency shows whether performance is holding close to underwriting. That matters because stronger NOI generally supports property value in the refinance narrative.

| Indicator | What it shows |

|---|---|

| Collection reliability | Whether income is dependable. |

| Repair burden | Whether operating noise is rising. |

| Net cashflow consistency | Whether performance is holding close to underwriting. |

If those indicators trend in the wrong direction, fix operations before pushing the Repeat step.

If you're comparing BRRRR with passive real-estate exposure, read A Guide to Real Estate Investment Trusts (REITs).

Refinance Is the Make-or-Break Step#

Refinance is the gate that determines whether BRRRR recycles capital or stalls. In this strategy, a cash-out refinance converts added equity into reusable capital, often by replacing short-term buy/rehab debt with a long-term mortgage based on post-rehab value.

If refinance is approved, you may recover capital for the next purchase. If it is delayed or denied, the property may still perform as a rental, but Repeat is not automatic. This is also where weak assumptions show up: appraisal risk can cut proceeds, lenders may require a 6-12 month seasoning period, and investment-property refinance leverage is often around 75-80% LTV.

What a refinance result really means#

| Outcome | What it usually means | What you should do next |

|---|---|---|

| Approved | Value, operating performance, and documentation support the new loan. | Close carefully, confirm cash-back and payment terms, then stabilize reserves before another acquisition. |

| Delayed | A gate is not ready yet, often seasoning, appraisal, or documentation. | Hold longer, keep operations stable, and fix the specific issue before reapplying. |

| Denied | The current value, income story, or file quality does not support terms that work. | Stop Repeat and choose one path: hold longer, improve NOI, or exit the rental property. |

Confirm lender assumptions early, not after rehab is done. Ask about seasoning and target LTV before you model proceeds, because a deal that looks strong at purchase can still miss at refinance if value or terms come in below plan.

Even with interest rates above 7%, this approach can still work, but your margin for error is thinner. Underwrite conservatively so higher borrowing costs do not surprise your cashflow.

Build a refinance packet before you apply#

A complete file improves underwriting speed and makes your value story easier to defend. Build your refinance-readiness packet before you apply:

| Packet item | Includes |

|---|---|

| Rehab records | Original scope, change orders, contractor invoices, paid receipts, and before-and-after photos. |

| Lease documentation | Signed lease, move-in condition records, and renewals or amendments. |

| Rent history | Rent ledger and proof of rent collected. |

| Lender-required property data | Property details plus requested ownership, debt, insurance, tax, and related asset information. |

A common failure mode is a solid property with weak documentation. When costs and rent history are incomplete, underwriting and appraisal support become harder.

If refinance fails, do not force Repeat#

If terms are not workable, slow down and pick one path. Hold longer when seasoning or early stabilization is the issue. Improve NOI when occupancy is in place but the income story is still weak. Exit the property when holding ties up too much capital for too little return.

Do not push into another purchase just because time and money are already sunk into this one. If this gate breaks, fix this asset first. That is where the BRRRR plan proves whether it is repeatable or just a one-property project.

For a step-by-step walkthrough, see A Real Estate Agent's Guide to the Home Office Deduction.

Repeat Without Breaking Your Portfolio#

Repeat only after the current property is stable on rent performance, reserves, and financing. In BRRRR, scaling too fast can compress your margin for error: unexpected repairs, refinancing challenges, and local market changes can all hit returns at the same time.

Use a simple pacing rule: add one new acquisition only after the prior property clears occupancy and refinance checkpoints. Occupancy means the unit is leased with reliable collections. Refinance means the long-term loan is closed on terms your cashflow can carry.

This is a risk-control choice, not hesitation. A reserves-first approach to systematic scaling is the safer default, and a conservative pace is often around 1 property annually. If you push toward 2 to 3 properties annually, treat that as an operational threshold. Beyond that range, a reliable team of contractors, property managers, lenders, and agents becomes essential.

Also watch concentration risk. If you stack similar distressed properties in one local market, the same repair, refinance, or market shock can affect several assets at once. You do not need perfect diversification, but you do need to pace growth before one weak point spreads across the portfolio.

Put Repeat behind a written checklist#

A short written checklist keeps momentum from driving the decision. Before you buy again, confirm:

- the current property is occupied and collections are consistently documented

- refinance is closed and final loan terms are confirmed

- reserves remain adequate after closing costs, repairs, and turnover

- unresolved maintenance or operational issues are not dragging cashflow

- your team has capacity for one more project without weakening current operations

BRRRR can support long-term income, but it is a serious commitment. If the last property still needs work, stabilize it first, then Repeat.

Related reading: A Guide to Cost Segregation Studies for Real Estate.

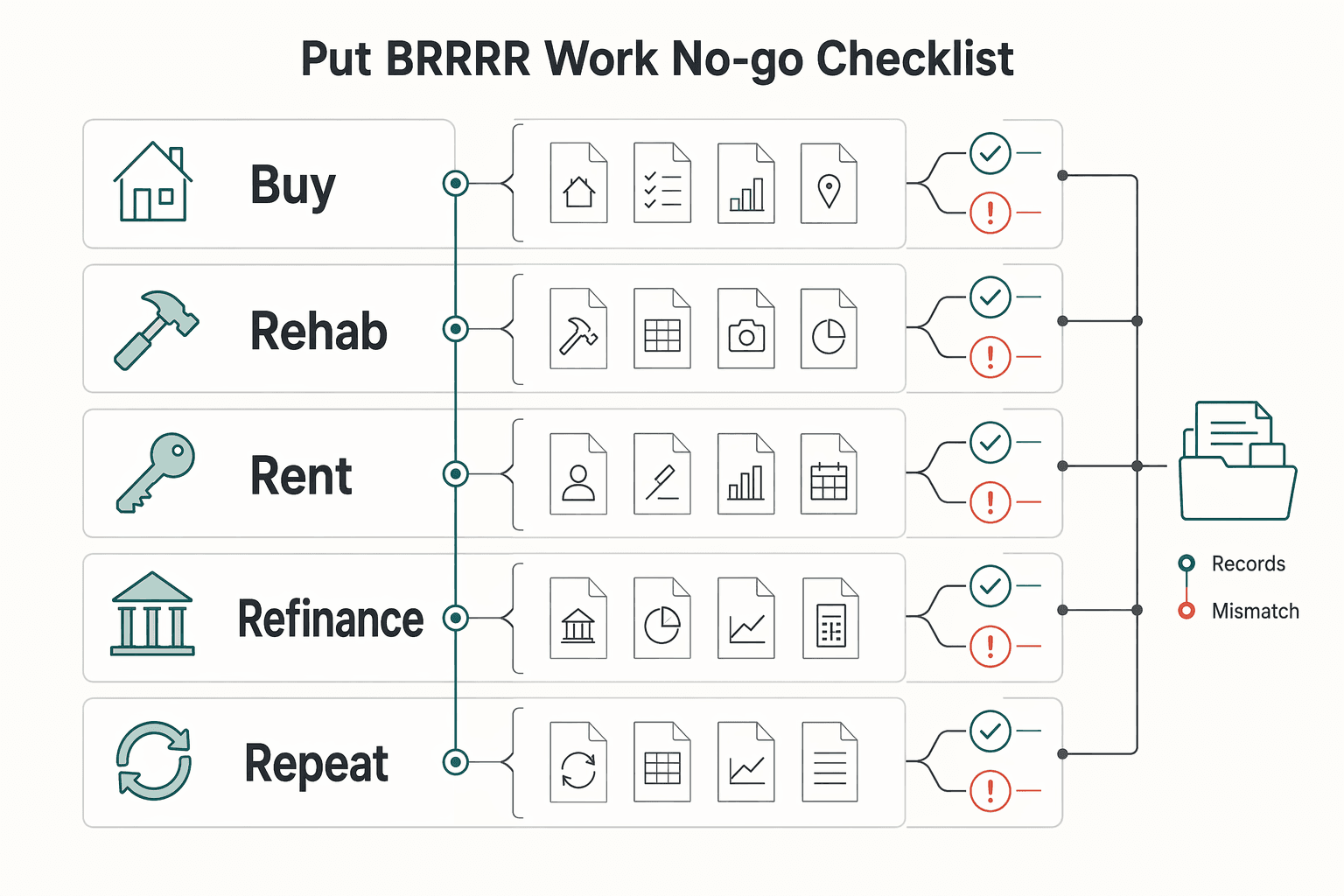

Put BRRRR to Work With a Go or No-Go Checklist#

Use BRRRR as a strict go/no-go workflow: do not advance until each stage is supported by written evidence. Start with one property, and if you cannot show proof for Buy, Rehab, Rent, Refinance, or Repeat, treat that stage as a no-go.

| Stage | Go when | No-go when |

|---|---|---|

| Buy | The deal still works under the 70% rule and your downside case is acceptable. | Your after-repair value or income assumptions are thin, or the margin disappears with a modest miss. |

| Rehab | The scope is tied to safety, leaseability, or appraised value, with room for 15-20% overruns. | Cosmetic upgrades are crowding out must-do work, or change orders are growing without a clear payoff. |

| Rent | The unit is truly lease-ready and the price target is supported by current market evidence. | Vacancy risk looks worse than expected or early tenant demand is weak. |

| Refinance | You verified lender rules before buying, including any 6-12 month seasoning period and likely 75-80% LTV limits. | You are assuming approval, ignoring appraisal risk, or missing a clean file of project and property records. |

| Repeat | The current property is occupied, financed on workable terms, and still producing durable cashflow. | You need the next deal to rescue a weak property that is not yet stable. |

The goal is not a prettier checklist. It is to stop yourself from moving forward on hope. Keep a compact evidence pack for each gate so you can defend your assumptions when timing, appraisal, or vacancy pressure shows up.

Most breakdowns come from carrying one weak assumption into the next stage. The recurring threats are renovation overruns, appraisal risk, and vacancy periods, so make your operating rule simple: when one slips, pause the cycle and fix it before you continue.

Growth pace also matters. The source material describes 1 property annually as conservative, while aggressive full-time investors may complete 4+ deals per year. Once you move beyond 2-3 properties annually, reliable contractors, property managers, lenders, and agents become essential, so scale only when that team is in place.

Frequently Asked Questions

What does BRRRR stand for in real estate investing?

BRRRR stands for Buy, Rehab, Rent, Refinance, Repeat. It is a five-step method where you improve a property, stabilize it as a rental, then try to pull equity back out through a cash-out refinance.

How is BRRRR different from house flipping?

A flip usually ends with a sale, so returns can hinge on resale timing and price. The brrrr method real estate approach depends on stable occupancy and a workable long-term loan, which makes it closer to operating a rental business than completing a one-time project.

Is BRRRR passive income or an active operating strategy?

Early on, it is active. You are managing acquisition risk, construction scope, tenant placement, vacancy, and financing, so calling it passive from day one usually hides the real workload. It can support long-term income, but it is still a serious commitment.

What are the biggest risks at each BRRRR stage?

Buy risk is overpaying or misreading after-repair value. Construction risk is cost overruns, with published guidance citing 15 to 20% average overruns as a major threat, while leasing risk is vacancy. The loan risk is a low appraisal or lender constraints, and Repeat risk is scaling before the previous property is truly stable.

What happens if you cannot refinance after rehab?

Outcomes vary by lender, timing, and deal performance. Do not assume approval is automatic just because the work is finished. A useful checkpoint is to verify lender rules before you buy, especially any 6 to 12 month seasoning period and whether the lender is likely to cap the new loan around 75 to 80% LTV.

Does the 70% rule guarantee a good BRRRR deal?

No. The 70% rule is only a screening shortcut: never pay more than 70% of after repair value minus renovation costs. It helps you reject obvious bad deals fast, but it does not protect you from bad ARV assumptions, renovation overruns, appraisal risk, or vacancy periods. If your estimate of ARV is shaky, treat the rule as a warning light, not proof.

When should you hire a property manager instead of self managing?

There is no universal trigger for every investor. In practice, as you scale, a reliable team often becomes necessary, and that team can include a property manager. That becomes especially relevant when you are trying to scale beyond 2 to 3 properties annually.

Try a related tool

A former product manager at a major fintech company, Samuel has deep expertise in the global payments landscape. He analyzes financial tools and strategies to help freelancers maximize their earnings and minimize fees.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- catawbacountync.gov/news/this-week-your-library-march-15-22-2026-1trusted

- govinfo.gov/content/pkg/GPO-CRECB-1978-pt18/pdf/GPO-CREC...trusted

- huduser.gov/portal/sites/default/files/pdf/General-Desig...trusted

- people.cs.pitt.edu/~hoffmant/java-topics/Collections/ArrayList/...trusted

- airdna.co/blog/brrrr-methodexternal

- amerisave.com/learn/the-complete-brrrr-method-guide-for-bu...external

- apexmoneylending.com/brrrr-strategy-explained-buy-rehab-rent-refi...external

- backflip.com/understand-brrrr-method-real-estate-investingexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Calculate a Freelance Rate You Can Actually Get Paid On

A workable rate is not the neat number a calculator produces. It is the number that still works after you account for real billable capacity, non-client time, scope drift, and the gap between sending an invoice and receiving cleared cash. Start with hourly math even if you do not plan to bill hourly, then turn that number into a quote with clear `payment terms`.

How to Invest in Real Estate as a Digital Nomad

**Run anything with money and moving parts like an operations system (cash, docs, delegation, and controls), not a "passive income" vibe.** Real life stress-tests weak spots. You change time zones, a client pays late, and something breaks at the worst moment. As the CEO of a business-of-one, your job is to build a setup that keeps working when you are not available on demand.

How to Calculate Cap Rate for a Rental Property

To calculate cap rate, divide **Net Operating Income (NOI)** by the property's **current market value**. That gives you an unlevered view of the asset's earning power, without mixing in loan terms or owner tax position.