Quick Answer

Diagnose the request first, then act: if it is a state coverage obligation, provide the required legal proof; if it is a client policy requirement, pursue accepted alternatives or submit a ghost policy COI. The practical flow is to review the clause, confirm worker classification and jurisdiction, then choose exemption, negotiation, or compliance. For non-standard setups, use a broker early and validate certificate holder fields, named insured details, and endorsements before submission.

You landed the contract. Negotiations are done, the scope is set, and you are ready to deliver high-value work. Then the email arrives from your new enterprise client: "Please provide your Certificate of Insurance for Workers' Compensation to complete your vendor onboarding."

For an independent consultant, a solo founder, or any Business-of-One, that request can feel like a bureaucratic hurdle built for larger companies. It can also bring an unexpected cost that threatens your margin and control.

The better move is to treat it as an operating issue, not a personal one. A reactive freelancer sees a blocker; a business owner diagnoses the requirement, picks the right path, and gets procurement what it needs without unnecessary spend. This playbook shows how to handle the request that way.

Step 1: Diagnose the Underlying "Why"#

Start by identifying what is driving the request: a legal coverage obligation or a client procurement rule. Those paths often call for different proof and different options.

If the request cites state coverage rules, worker status, or public-contract insurance terms, treat it as compliance first. If it shows up as a standard insurance clause in your MSA, vendor packet, or onboarding flow without a legal citation, treat it as a client risk-policy requirement first.

| Scenario | Trigger | Who sets it | What proof usually satisfies it | Negotiable? |

|---|---|---|---|---|

| Legal requirement | State coverage rules, worker-classification facts, or public-contract insurance terms | State workers' comp authority or contracting agency | COI after policy purchase, or a state-specific exemption document where allowed | Usually limited |

| Internal risk policy | Boilerplate insurance schedule, procurement checklist, or onboarding requirement | Client legal, risk, or procurement team | COI or other documentation the client accepts | Sometimes |

Use state-specific signals, not national assumptions. New York says virtually all employers must provide coverage for employees under WCL §2 and 3. California requires coverage even with one employee. Texas says most private employers can choose coverage, while governmental entities must carry it. Start by checking your state workers' compensation board.

Then verify your status. For employee-vs-contractor questions, use the IRS common-law categories: behavioral control, financial control, and relationship of the parties. Do not assume an "independent contractor" label alone settles the issue.

Before you reply, run this quick sequence:

- Read the exact contract clause and insurance schedule for required types, minimum amounts, and timing, including whether proof is required before work starts.

- Check your state guidance and confirm your entity and worker status.

- If you are in New York, do not treat CE-200 as a universal fix. It is for specific government-entity contexts and cannot cure past non-compliance.

- Ask procurement one precise question: "Is this workers' comp requirement being imposed by state law for my engagement, or is it your standard vendor insurance requirement? If there is an alternate document you accept, please share it."

Once you know which lane you are in, Step 2 becomes a strategy choice instead of a scramble.

Related: What is Cyber Liability Insurance and Do Freelancers Need It?.

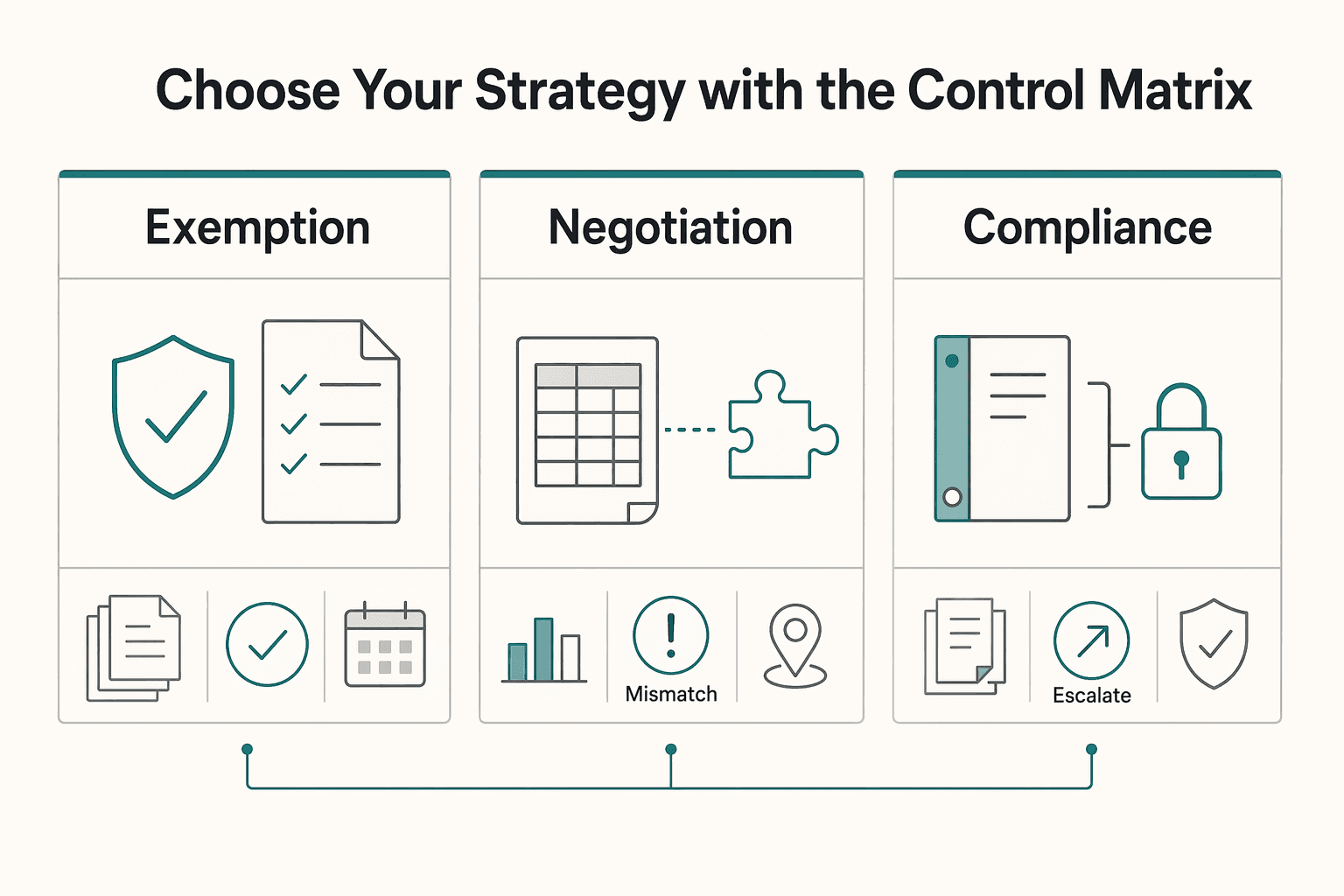

Step 2: Choose Your Strategy with the Control Matrix#

Do not default into a path. Start with a structured risk review, then choose the path your documentation can support.

Use this matrix as a control tool, not a prediction tool. It helps you check risk coverage, document readiness, and decision authority across stakeholders.

| Path | When this path fits | Required proof | Time-to-clear onboarding | Cost profile | Risk if denied |

|---|---|---|---|---|---|

| Exemption | An exception route is being considered and reviewers are open to documented support | Official records for your case, plus risk-identification artifacts (incident logs, analytics outputs, expert input, and policy/procedure audit notes) | Varies based on document completeness and reviewer queue | Primarily documentation and coordination effort | Move to another path using the same evidence file |

| Negotiation | The default requirement may not match your current risk profile and decision owners will review alternatives | Clause excerpt, operating facts, and one consistent evidence pack (incident logs, analytics outputs, expert input, and policy/procedure audit findings) | Varies by reviewer availability and escalation path | Coordination-heavy; direct spend is case-specific | Delay, then fallback to compliance if alternatives are declined |

| Compliance | Decision owners require full compliance, or other paths are not accepted in time | Complete application/certificate package and any required wording, validated against one checklist | Varies; inconsistent details can add rework | Case-specific and should be confirmed during review | Clearance may still fail if submitted details are incomplete or inconsistent |

Read the matrix in this order:

- Build a complete risk picture first, including operational, compliance, and process exposures.

- Test whether an exception path is reviewable with a documented request and clear decision owner.

- Move to full compliance only when other paths do not clear and the required artifacts are complete.

Keep one working file for all three paths: contract clause, onboarding checklist, incident reporting logs, analytics outputs, policy/procedure audit notes, and message trail. A single evidence set helps you surface process gaps before they become downstream risk.

Path 1 Exemption Checklist#

Use this path only when an exception route is actually available and reviewers will consider supporting records.

- Confirm the exact document label and status fields for your case before submission.

- Validate key fields for consistency, including entity name, dates, and scope.

- Add risk-identification artifacts: incident logs, analytics outputs, expert input, and policy/procedure audit notes.

- Send one concise submission note and ask what, if anything, is still required to close.

Path 2 Negotiation Checklist#

Negotiation works better when you present one consistent fact pattern and ask for a specific decision, not a general favor. Use a reusable message framework:

| Part | What to include |

|---|---|

| Claim | your current risk profile may not match the default requirement for this engagement |

| Supporting fact | consistent operating facts plus evidence from incident logs, analytics outputs, expert input, and policy/procedure audits |

| Acceptable alternatives | documented controls or exception paperwork you can provide now |

| Escalation request | the reviewer who owns exceptions if the first reviewer cannot approve |

Keep these touchpoints in mind:

- Start with your business contact to align context.

- Route the same fact pattern to procurement/legal without changing the core claim.

- Track responses in one thread so decisions and conditions stay clear.

Path 3 Compliance Checklist#

If you need to complete a full compliance path, accuracy matters as much as speed. Inconsistent details create rework and can introduce downstream process risk.

- Ask each stakeholder for the exact intake items needed and assign an owner for each artifact.

- Request certificate/document wording requirements in writing before submission.

- Use a field or mobile intake method to capture emerging risk factors and feed updates into your checklist.

- Verify every field on the final package, submit once, and confirm receipt and final clearance status so Step 3 stays procedural, not reactive.

You might also find this useful: How to Set Up Workers' Compensation Insurance for a Remote Team.

Step 3: Execute the Compliance Path with Precision#

If you land on the compliance path, the job is straightforward but detail-sensitive. Secure an active policy and submit a COI package procurement can approve without rework. Run this as a sequence from channel choice to final QA, and keep state-specific rules in view because workers' compensation oversight is state-level.

1. Choose the right channel before requesting quotes#

Channel choice affects both underwriting fit and how smoothly your proof gets issued. Start with fit and execution reliability, especially for owner/officer exclusion questions or other non-standard setups.

| Channel | Use when | Turnaround and COI signal | Watchout |

|---|---|---|---|

| Independent agent or broker | Your setup is non-standard, for example owner/officer exclusion questions or state-specific uncertainty | Can shop multiple insurers, which helps when one carrier is not a fit | Speed depends on responsiveness and how clearly you provide COI requirements |

| Digital platform | Your operation is straightforward and you need fast intake and proof delivery | Some platforms advertise COI delivery in about 10 minutes or instant access | Fast flow may be less flexible when contracts require custom COI handling or endorsement checks |

| Direct carrier | You already know that carrier writes your class of business in your state | Can be efficient when underwriting fit is already known | Captive/direct routes are single-carrier, so fallback options are limited if declined |

Practical rule: start with an independent agent or broker when the facts need interpretation. Use digital for clean, standard submissions on tight timelines. Go direct when carrier fit is already confirmed.

2. Build your application checklist before quote intake#

Build the intake package before you ask for quotes. That cuts down on back-and-forth and keeps the quote, bind, and certificate stages aligned.

| Item | Details to collect |

|---|---|

| Business identity | legal entity name, address, FEIN/EIN/Tax ID, primary contact |

| Work classification | clear description of duties/classification-relevant work |

| Payroll and staffing | employee count and payroll facts by role/classification |

| Owner status | flag owner/officer exclusion early if relevant and complete any exclusion forms surfaced in workflow |

| Certificate holder details | exact certificate holder name and any contract-specified details |

| Contract-specific COI requirements | required wording and any requests for additional insured, waiver of subrogation, or endorsements |

Collect each item once and use the same set for quote review, binding, and certificate checks.

3. Use a short talk track in first contact#

Your first outreach should give the broker, platform, or carrier enough to quote correctly and flag certificate issues early. Include these points:

- Business profile: your structure and staffing facts.

- Coverage format needed: workers' comp policy for contract compliance.

- Certificate requirements: exact certificate holder details and required wording.

- Delivery deadline: when proof must be sent.

4. Bind coverage, then verify the COI package#

Treat COI handling as its own step after binding. A COI is proof of coverage and, by itself, does not amend policy terms or grant rights. If the contract calls for additional insured status or waiver of subrogation, you may need endorsement support beyond certificate text.

5. Run final QA before submitting to procurement#

Before you send anything, do one final pass against the contract and the onboarding checklist:

| Check | What to confirm |

|---|---|

| Policy status | active on submission date |

| Named insured | matches the contract exactly |

| Certificate holder | correct exact name and contract-specified details |

| Endorsements | listed or confirmed/attached when applicable |

Then send one complete package: COI, any required endorsement support, and a short note requesting final clearance confirmation.

If you want a deeper dive, read Canada's Digital Nomad Stream: How to Live and Work in Canada.

For a related classification check, use Use the W-2 vs 1099 calculator.

From Compliance Anxiety to CEO Confidence#

The process is simple: diagnose the requirement, choose the right path, and submit proof that clears review the first time. Once you do that a few times, the request stops feeling personal and starts feeling operational.

Start with diagnosis. Because insurance rules vary by state, begin intake with the jurisdiction and the exact contract requirement before you request quotes. If federal contracting language applies, FAR 52.228-5 can require written confirmation that insurance is in place before work starts. For private-company and state/local contexts, treat the state workers' compensation board as a primary official contact point.

Then choose the path that fits the jurisdiction instead of forcing a default approach. Texas shows why: many private employers can choose whether to carry coverage, while Texas governmental entities must carry it. New York is stricter for most employers, and permits, licenses, or contracts may require insurer-issued Form C-105.2, not a broker-issued certificate.

Finally, keep your proof discipline tight. A database hit is not the same as legal proof: California's public coverage search states it is not verification and may miss updates from the last 60 days. Before you submit documents, verify coverage directly with the employer or insurer.

| Area | Reactive response | CEO-style response |

|---|---|---|

| Documentation readiness | Scrambles for documents after procurement requests them | Keeps clause text, entity details, state context, and required proof format ready |

| Procurement friction | Sends a generic certificate and waits for rejection | Matches proof to requirement, for example insurer-issued C-105.2 in New York |

| Repeatability | Rebuilds the process for every contract | Uses the same intake, verification, and renewal checkpoints each time |

Keep this checklist for every new contract:

- Ask four intake questions: which state rules apply, what exact clause governs, who is requesting proof, and whether the contract requires proof before work starts.

- Maintain a compliance packet: contract excerpt, legal entity details, work description, certificate/form copy, and insurer confirmation when needed.

- Route requests correctly: insurer/carrier for official coverage proof, including C-105.2 in New York, the state board as an official workers' comp contact point, and the contract owner for clause interpretation.

- Track renewals and recurring obligations: New York sample C-105.2 certificate language caps validity at one year, and Texas non-subscribers have an annual DWC-005 filing window from February 1 through April 30.

For a step-by-step walkthrough, see The Best Disability Insurance Companies for High-Earners.

If client requirements keep expanding beyond insurance paperwork, use a setup designed for compliant money movement and clearer records: Explore Gruv for freelancers.

Frequently Asked Questions

How do you tell whether this is a legal requirement or a contract requirement?

Start by verifying authority before you pick a path. In the Longshore context, OWCP handles authorization of insurance carriers and self-insured employers, and a contract may include its own proof requirements. Pull the exact contract clause, confirm the specific Act involved, then verify authority first and either negotiate or secure proof.

Who regulates Longshore insurance authorization?

OWCP is the authority for authorization of insurance carriers and self-insured employers in this program context. Authorization is not one-size-fits-all, because each carrier or employer must be separately authorized for each Act administered by that office. Before you rely on coverage, ask your broker or carrier to confirm authorization for the exact Act and keep that confirmation in your records.

Should you contact the U.S. Department of Labor about premium rates?

No. DOL states it does not regulate insurance premium rates, and authorized carriers are regulated by state insurance commissioners where they operate. If a quote looks off, gather the quote details, state, work description, and carrier name, then escalate through your broker or the relevant state regulator.

How do you verify the OWCP contact path for authorization or compliance questions?

Treat this as an execution checkpoint, not a formality. The OWCP FAQ says that to request authorization, you submit an application to write coverage, and it provides a direct contact path for authorization and compliance questions. If you are asked to submit materials, use the listed address checkpoint: Frances Perkins Building, Room S-3229, 200 Constitution Ave NW, Washington, DC 20210.

Can you self-insure instead of buying a policy?

Possibly. In this context, Form LS-271 is the application for self-insured employers. Before you prepare a full package, confirm with OWCP what supporting documents are required.

What should you prepare before you ask a broker, carrier, or OWCP for help?

Bring the exact contract language, a plain description of your work, and the state or states involved. Also say whether your question is about carrier coverage or self-insurance, and identify the specific Act if authorization is part of the issue. If you think a state-specific exception may apply, flag it for verification before you rely on it.

What happens if you skip insurance or posting requirements?

The OWCP FAQ explicitly flags consequences for failing to obtain Longshore insurance and for failing to post Form LS-241 or LS-242. Verify those obligations early and keep documentation showing your coverage and posting status. If a client asks only for proof, do not assume that request replaces any underlying compliance duty.

How much should you expect to pay?

A current range is not verified in this article. DOL is not the rate regulator, so ask your broker to show the state basis, work description used for the quote, and whether the carrier is authorized for the applicable Act. That helps you compare quotes on the same assumptions.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far/52.228-5trusted

- acquisition.gov/far/subpart-28.3trusted

- beta.dol.gov/policy-regulations/pay-benefits/workplace-in...trusted

- congress.gov/114/plaws/publ113/PLAW-114publ113.htmtrusted

- dhs.gov/sites/default/files/2023-04/HSAM%20through%2...trusted

- dir.ca.gov/dwc/employer.htmtrusted

- dol.gov/general/topic/workcomptrusted

- dol.gov/agencies/owcp/dlhwc/FAQ/InsuranceFAQtrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Canada Digital Nomad Visa Planning for Visitor Status and Work Permits

The phrase `canada digital nomad visa` is useful for search, but misleading if you treat it like a legal category. It is shorthand for existing Canadian status options, mainly visitor status and work permit rules, not a standalone visa stream with its own fixed process. That difference is not just technical. It changes how you should plan the trip, describe your purpose at entry, and organize your records before you leave.

What is Cyber Liability Insurance and Do Freelancers Need It?

**Treat cyber coverage as part of your system, not a checkout decision.**

Workers' Compensation for Remote Independent Contractors: OAI, Contracts, and Liability

The shift from anxiety to advantage starts with dismantling one dangerous assumption many remote professionals make: that in a crisis, a client's insurance will protect them. That belief creates a serious risk hiding in plain sight. To build a resilient career, you first need to understand the legal and financial wall that separates you from a traditional employee.