Quick Answer

Use an accountable plan, then reimburse only documented business trips. For 2026, the standard mileage rate is 72.5 cents per mile, which is usually easier to run than full actual-expense allocation. Keep commuting separate, capture date, miles, and business purpose, and settle method rules before first reimbursement: owned vehicles need a year-one standard-mileage election for flexibility, while leased vehicles stay on standard mileage for the lease term once chosen.

Your First Strategic Decision: Who Owns the Vehicle?#

Start with ownership and deduction method together. These choices affect what you can realistically document and how much recordkeeping you will take on. In practice, most setups fall into one of two lanes: mileage-centered records, where you track business miles, or expense-centered records, where you track costs and apply a business-use percentage.

The two choices are linked. How the vehicle is held can push you toward one method or the other, and a poor method choice can change both your admin burden and your result.

1. Personally held vehicle#

When the vehicle stays in your name, choose the documentation lane you can maintain consistently. If you use the standard mileage method, you track business miles and apply the IRS mileage rate instead of collecting every receipt and allocating total costs.

The main advantage is simpler administration. If your mileage log is complete and consistent, day-to-day recordkeeping is lighter. As one grounded example, the cited source lists the 2025 rate as $0.70 per mile. Treat that as historical context, not a current-year rate.

The tradeoff is reduced flexibility. If you start with standard mileage for a vehicle, you are generally locked into that method for that vehicle.

2. Company held vehicle#

When the corporation holds the vehicle, documentation demands can rise, especially if you use actual expenses. Under actual expenses, you track the major vehicle costs, such as fuel, maintenance, insurance, registration, lease payments, and depreciation, then deduct the business-use percentage of total costs.

That means you need complete cost records and credible support for total use versus business use. If use is mixed, allocation becomes the hard part. Weak trip records or fuzzy use classification make the deduction harder to support.

Decision table#

| Path | Best fit | Compliance workload | Payroll or fringe impact | Reimbursement mechanics | Audit defensibility |

|---|---|---|---|---|---|

| Personally held + mileage-centered records | You want a simpler, miles-first approach and can keep a clean mileage log | Lower ongoing burden than full-cost tracking | Not established by the grounding for this section | Not established by the grounding for this section | Depends on documentation quality; no ownership path is established as more defensible here |

| Personally held + actual expense records | You prefer personal ownership but can track full costs and usage allocation | High (full cost tracking + business-use percentage) | Not established by the grounding for this section | Not established by the grounding for this section | Depends on complete cost and usage records |

| Company held + actual expense records | You are prepared for full documentation discipline | High (full cost tracking + business-use percentage support) | Not established by the grounding for this section | Not established by the grounding for this section | Depends on complete cost records and defensible business-use percentage support |

Boundary rules before you choose#

Be conservative. Count only miles and trips you can clearly support as business use. If the vehicle is mixed-use, expect more documentation and tighter allocation support. Commuting treatment, reimbursement mechanics, and payroll or fringe reporting details are not established by this section's grounding, so treat those as confirm-with-advisor items before you finalize the setup.

Quick decision checklist#

- Choose a mileage-centered lane if your priority is simpler recordkeeping and you can keep a strong mileage log.

- Choose an actual-expense lane only if you can track every major cost category and support business-use percentage.

- Before starting standard mileage, decide with method lock-in in mind.

- If mixed use is likely, expect more allocation work and tighter documentation standards.

Once ownership is set, the next job is to keep records consistent and confirm reimbursement or payroll treatment details with your advisor. Related: A Guide to Vehicle Expense Deductions for Freelancers.

The Non-Negotiable Foundation: Your Accountable Plan#

Put this in place before you reimburse anything. Without an accountable plan, what looks like repayment can be treated as wages instead. For an S-corp officer who performs services, that is not a paperwork issue. It is a payroll issue, and the arrangement must satisfy all three tests for reimbursed amounts.

1. Business connection (pass/fail test)#

A reimbursement works only if the expense is business-related. For vehicle use, trips reimbursed under the plan need a documented business purpose. Commuting between home and your regular business location is generally not deductible. If a trip is not business-connected, it fails here and should not be reimbursed as an accountable-plan amount.

2. Substantiation (evidence test)#

You need records that substantiate the expense within a reasonable period. If you use the standard mileage method, keep mileage records and build timely submission into your process.

Use a documented timing rule in your policy and payroll steps. Verify the exact substantiation and return cadence against current official guidance, adviser notes, and company policy before using it.

3. Return of excess (cleanup test)#

If the company advances more than the substantiated amount, the excess must be returned within a reasonable period. If it is not returned, the excess moves into nonaccountable-plan treatment and is included in wages by the first payroll period after that reasonable period ends. That is where reimbursement turns into payroll, including withholding and employment-tax consequences.

| Test | Requirement | If not met |

|---|---|---|

| Business connection | The expense must be business-related and the trip needs a documented business purpose; commuting between home and your regular business location is generally not deductible | It fails the test and should not be reimbursed as an accountable-plan amount |

| Substantiation | Records must substantiate the expense within a reasonable period; if you use the standard mileage method, keep mileage records and use a documented timing rule in the policy and payroll steps | Unsupported amounts should be routed to wages |

| Return of excess | If the company advances more than the substantiated amount, the excess must be returned within a reasonable period | The excess moves into nonaccountable-plan treatment and is included in wages by the first payroll period after that reasonable period ends |

| Policy element | Implementation choice | Record retained | Process location |

|---|---|---|---|

| Reimbursement method | Decide and document standard mileage or actual expense | Mileage records or expense support | Policy/resolution + reimbursement procedure |

| Approval workflow | Define who submits and who approves; apply it consistently | Submitted report, approval record, payment record | Reimbursement file + accounting trail |

| Timing workflow | Set submission and return cadence after verifying current official guidance, adviser notes, and company policy | Submission dates, exception notes | Policy + payroll checklist |

| Retention | Keep reimbursement and payroll support with employment-tax records for at least 4 years | Logs, reports, payroll records | Accounting/payroll archive |

The common failure modes are predictable: reimbursing commuting, paying amounts without substantiation, letting substantiation come in late, and not returning excess advances. Keep the operating cadence simple. Adopt the policy, submit on schedule, review exceptions before payroll closes, and route unsupported amounts to wages.

With that foundation in place, you can choose a reimbursement method based on what you can actually document, not what looks best in theory. You might also find this useful: Can an LLC Pay for a Member's Health Insurance?.

The CEO's Dilemma: Which Reimbursement Method Maximizes Your ROI?#

Start with the method you can support cleanly every month. For many S-corp owners, that usually means the standard mileage rate. Actual expense is worth the extra work only when the likely dollar upside is real. For 2026, the federal business standard mileage rate is 72.5 cents per mile.

| Method | What it includes | What it excludes or limits | Documentation load | Audit risk surface | Flexibility over time | Common owner mistakes |

|---|---|---|---|---|---|---|

| Standard mileage rate | Per-mile reimbursement for substantiated business miles | You do not deduct lease costs on top of mileage; for leased vehicles, you cannot deduct both lease costs and standard mileage | Lower: complete mileage log, submission record, reimbursement record | Narrower, but weak logs (late, vague, personal and business use mixed) are still easy to challenge | For owned vehicles, preserving this option generally requires choosing it in year 1 the car is available for business use; for leased vehicles, choosing it locks this method for the full lease period (including renewals) | Reimbursing nonbusiness miles, logging miles without a clear business purpose, adding lease payments on top, forgetting business parking/tolls are separate |

| Actual expense | Business-use share of gas, oil, repairs, tires, insurance, registration fees, licenses, and depreciation or lease payments | Personal-use share is not reimbursable/deductible | Higher: mileage log plus receipts/statements and allocation support across the year | Broader, because each cost category and business-use percentage can be questioned | More constrained if early depreciation choices remove standard-mileage eligibility | Missing receipts, weak business-use percentage support, no total-mile support, mixing personal and business costs |

| Parking fees and tolls | Business parking fees and tolls are separately deductible under either method | Not a replacement for either primary method | Moderate | Usually straightforward when tied to a business trip record | Available with either primary method | Folding these into mileage, or failing to tie them to specific business trips |

1. Standard mileage rate#

For most owners, this is the lower-admin option. You reimburse substantiated business miles at the IRS rate, which is 72.5 cents per mile for 2026.

The appeal is simple. You are tracking miles and trip purpose, not every operating receipt. But the log still has to hold up. It needs substantiation that ties miles to a specific business purpose and clearly separates business and personal use. A mileage app can help with capture, but it does not replace accountable-plan substantiation.

2. Actual expense#

This method can produce a better result, but only when the records are strong enough to support the allocation. You are using actual operating costs, then splitting them between business and personal use.

Use it when your cost profile and business-use pattern suggest real upside, not assumed upside. If you qualify for both methods, compute both before choosing.

3. How to decide without overthinking it#

A clean decision usually comes down to four filters:

| Filter | What to assess | Grounded direction |

|---|---|---|

| Vehicle profile | Whether costs look high enough to justify extra admin | Standard mileage is often the practical default; evaluate actual expense when costs look high enough to justify the extra admin |

| Recordkeeping tolerance | Which method you will maintain consistently | Choose the method you will maintain consistently, not the one that looks better only on paper |

| Business-use pattern | How stable and well-documented the business driving is | Stable, well-documented business driving is easier to defend; mixed use with weak logs raises challenge risk, especially under actual expense |

| Expected upside vs admin burden | Estimate both methods and compare the difference | If the difference is small, simplicity usually wins |

4. Method lock-in and switching#

Method choice matters most at the start, because early choices can limit later flexibility.

For an owned vehicle, preserving standard-mileage flexibility generally requires choosing standard mileage in the first year the automobile is available for business use. After that first-year choice, later-year switching between standard mileage and actual expenses is allowed.

For a leased vehicle, if you choose standard mileage, you must keep using it for the full lease period, including renewals. You also cannot deduct lease costs on top of mileage.

Also, standard mileage is not available for that car if you claimed a Section 179 deduction or used MACRS on it.

The practical takeaway is simple: start with mileage unless your cost profile gives you a clear reason to test actual expense, then compute both before you finalize the year. We covered some entity-choice angles in detail in The Pros and Cons of a C-Corp for a Freelance Business.

Before you lock in a reimbursement method, run a quick side-by-side estimate with the Mileage Deduction Calculator. That helps your policy choice match your real driving pattern.

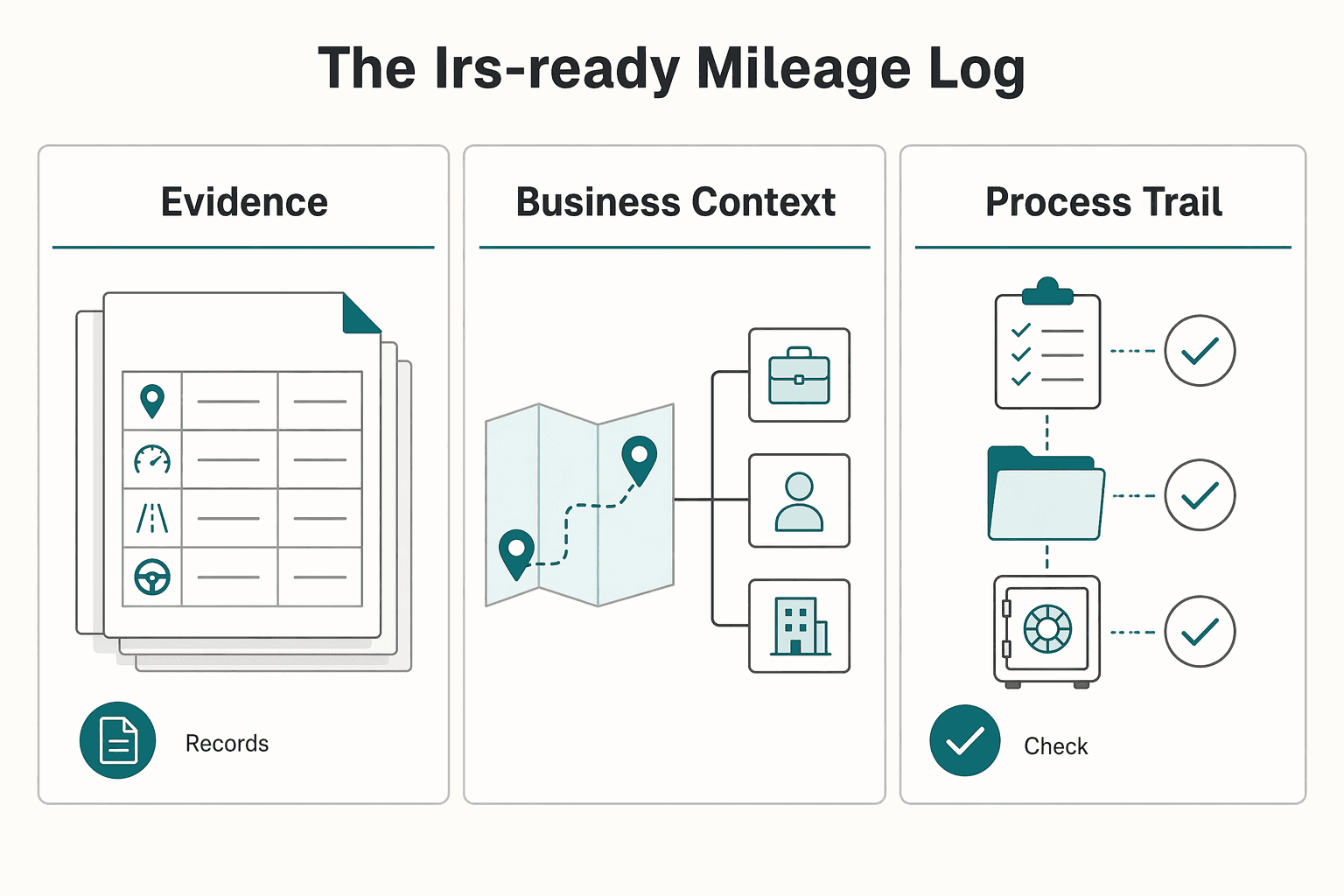

Building Your Audit-Proof System: The IRS-Ready Mileage Log#

If this ever gets reviewed, the question is not whether you meant well. It is whether your records look like a real operating process instead of a reconstruction. To track vehicle mileage for S-corp use cleanly, use a trip record standard with three layers: the trip entry, the business context, and the review-and-archive trail.

Because the provided material does not verify a full field-by-field IRS requirement list, use the table below as an internal control standard and apply it consistently.

| Record layer | What to capture | Why it matters | Common error |

|---|---|---|---|

| Trip entry | Core trip details captured consistently under your internal template | Gives you a consistent base record for reimbursement calculations and monthly review | Logging only periodic totals with no trip-level detail |

| Business context | Specific counterparty, concrete objective, and expected or actual business outcome | Distinguishes business driving from vague activity labels | Notes like "meeting," "lunch," or "admin" with no business link |

| Process trail | Created By, Created Date, review date, approver, export file, and archive location | Shows the entry moved through a real process with visible checkpoints | Silent edits to older entries with no note, timestamp, or preserved prior version |

Use a fast decision rule for business purpose#

Use a simple screen: if a one-line trip note does not identify the counterparty, the objective, and the business outcome, it is too weak.

- Weak: "Client meeting."

Stronger: "Met Sarah Kim at Northside Cafe to review scope and pricing for April website retainer."

- Weak: "Supplies."

Stronger: "Drove to printer to pick up proposal packets for Thursday pitch to Apex Dental."

Design the workflow, not just the capture#

Capture is only the first step. The real control is the review cycle:

- Review uncategorized trips and classify them on a consistent internal schedule.

- Reconcile trip records against calendar events, client meetings, invoices, or job records.

- Approve reimbursement through your accountable-plan process with a visible approver and date.

- Archive the periodic export and support file set using the same process each cycle.

Use two correction rules. First, make edits additive: keep the original, note the reason, and keep the updated timestamp. Second, keep export-ready records, not just app-resident data. A common risk pattern is letting an app auto-capture trips, skipping review, and then trying to classify everything later from memory.

For a step-by-step walkthrough, see How to Create an Accountable Plan for a Single-Member LLC.

Beyond the Basics: Navigating High-Value Vehicles, Leases, and Audit Red Flags#

This is where small mistakes can get expensive. For expensive, leased, or heavily mixed-use vehicles, use a verify-first approval process. Keep the reimbursement-method choice visible, and treat rule-dependent items as unverified until they are confirmed against the latest posted guidance before reimbursement is approved.

Working definitions (for this section)#

- High-value vehicle: a working label for vehicles where method choice or cap treatment could materially change the reimbursement outcome.

- Lease inclusion amount: a lease-related adjustment concept; apply only after you verify the current rule and table.

- Listed property: a legacy tax label that may still appear in guidance; treat it as unverified until current applicability is confirmed.

- Business-use percentage: the business share of total vehicle use in your records.

- Contemporaneous records: trip entries made at or near the time of travel, not reconstructed much later.

Use a revision-date check before applying rule-dependent decisions. Guidance changes, and a concise summary is not an all-inclusive manual.

| Scenario | Method eligibility | Admin burden | Audit risk | Escalate to a tax professional when |

|---|---|---|---|---|

| Personally owned vehicle, routine cost profile | Method options remain provisional until current guidance is verified | Moderate | Moderate if logs are incomplete | A rule-dependent decision cannot be confirmed from current materials |

| Personally owned, high-cost vehicle | Any cap-related treatment is unverified until current guidance is confirmed | High | Higher when dollar impact is large | Reasonable reviewers reach different outcomes from the same guidance |

| Leased vehicle | Lease-related method treatment remains unverified until current guidance is confirmed | High | High if method handling is inconsistent | You cannot confirm which current rule set applies |

| Mixed-use household vehicle | Approval depends on strong business-use support and documented reviewer judgment | Moderate to high | High when personal and business use overlap heavily | Claimed business-use share is not well supported by records |

Lease and method-selection flow (before first reimbursement)#

Before the first reimbursement goes out, force the file through a short review sequence:

- Identify ownership status (owned vs leased) and flag the file as advanced review.

- Select a provisional method and mark rule-dependent points as unverified until confirmed.

- Run a revision-date check against the latest posted guidance before final approval.

- Require a documentation pack before reimbursement: ownership or lease document, mileage export, business-purpose notes, method-selection memo, rule snapshot with revision date, and named approver/date.

- Route exceptions through a defined authorization path instead of ad hoc approvals, including any designated repair-authorization contact process.

Red-flag checklist and controls#

Most red flags are easy to spot if you look for them early:

| Red flag | Control |

|---|---|

| Repeated round-number trips | Review raw app captures monthly instead of relying on memory-based summaries |

| Weak business-purpose notes | Require counterparty, objective, and outcome before approval |

| Mixed-use vehicle with very high claimed business share | Reconcile against calendar and invoice records and require reviewer commentary |

| Late bulk edits before reimbursement | Use additive corrections, preserved exports, and visible timestamps |

If any of these show up, stop and review the file before reimbursement. If you want cleaner reimbursement decisions, treat high-cost or leased cases as a control event: verify current guidance first, then approve. If you want a deeper dive, read Value-Based Pricing: A Freelancer's Guide.

From Compliance Anxiety to Complete Control#

The throughline is simple: ownership drives method, method drives records, and records determine whether reimbursement stays reimbursement or turns into payroll. Control comes from making those decisions explicit and keeping the file supportable from the start.

- Ownership: Define whether the vehicle is personally owned or employer-provided.

Owner action: keep title or lease documentation and a written personal-use determination, because personal use of an employer-provided auto is wage-sensitive.

- Accountable plan: Treat reimbursements as accountable only when there is business connection, substantiation, and return of excess amounts.

Owner action: maintain a written policy plus reimbursement files that show substantiation and excess-return handling. If those conditions fail, treat it as nonaccountable and escalate for W-2 and payroll-tax handling.

- Reimbursement method: Use either standard mileage or actual expense. Standard mileage is optional when the vehicle is owned or leased.

Owner action: document your method choice and timing. For 2026, standard mileage is 72.5 cents per mile starting Jan. 1, 2026. For owned vehicles, year-one election affects flexibility, and for leased vehicles, standard mileage applies for the full lease period once chosen.

- Record-keeping: Auto expenses require strong substantiation.

Owner action: keep detailed mileage logs and supporting records for business use, and retain records at least through the general 3-year assessment window.

| Decision area | Required artifact | Review owner | Failure consequence |

|---|---|---|---|

| Ownership | Title/lease record and personal-use note | Owner; payroll/tax advisor for employer-provided auto | Personal-use wage treatment can be missed |

| Accountable plan | Written policy and reimbursement packet | Owner or CPA | Nonaccountable treatment; Form W-2 and employment-tax exposure |

| Method | Written method election and current IRS rate reference | Owner | Unsupported method changes or reimbursement position |

| Records | Mileage log export and supporting records | Owner | Substantiation failure for deductions/reimbursements |

Escalate to a CPA or payroll/tax advisor if any of these occur:

- employer-provided auto with personal use

- missing substantiation

- unclear excess-return process or timing

- attempted method change after year one for an owned vehicle or during a lease term

- a 2026 employer-provided auto first made available above $61,700 when cents-per-mile valuation is being considered

Use this closeout checklist before reimbursements are approved:

- Confirm ownership status and payroll treatment before reimbursements are approved.

- Approve reimbursements only when substantiation and excess-return documentation are complete.

- Validate the current IRS mileage and rule update from the latest notice or newsroom page before applying rates.

This pairs well with our guide on Toggl Track Project Profitability Audit for Freelancers. When your mileage process is stable, keep your broader freelance finance stack organized with the Gruv Tools library.

Frequently Asked Questions

What is an accountable plan for an S-corp?

An accountable plan is a reimbursement arrangement that must meet three tests: business connection, substantiation, and return of excess amounts. When those rules are met, accountable-plan payments generally do not need to be reported on Form W-2. Problems usually start when reimbursements are paid without substantiation or when excess amounts are not returned. Your policy should also require substantiation and excess-return steps within a reasonable period, with current timing details verified before finalizing the plan.

Which method usually fits better, standard mileage or actual expense?

Use the method you can document correctly, then compare both methods when you are eligible to do so. For 2026, the IRS business standard mileage rate is 72.5 cents per mile, and it can be simpler to administer when the trip log is strong. Actual expense requires allocating total vehicle costs between business and personal use, and it may fit better when that allocation produces a stronger supported result. For owned vehicles, you must choose standard mileage in the first business-use year if you want to use it, and for leased vehicles, standard mileage continues through the full lease period once chosen.

Can my S-corp pay for my car?

Yes, but the treatment depends on who owns the vehicle. If you own it personally, the S-corp can reimburse substantiated business use under an accountable plan, including mileage-rate reimbursement. If the company owns the vehicle, business-use value can be treated as a working-condition benefit, while personal use is generally taxable fringe compensation and may require payroll or W-2 handling.

What makes a mileage log audit-ready?

An audit-ready log is complete and specific enough to substantiate each business trip. Record the date, miles, and business purpose for each trip, and keep beginning and end-of-year odometer readings. Your records should support the amount, time, place, and business purpose of each expense.

Is commuting mileage deductible for an S-corp owner?

Usually no. Travel between home and your main place of work is commuting, and commuting expenses are not deductible. A limited exception can apply when daily round-trip travel is between home and a temporary work location in certain regular-work-location situations, so verify the facts before treating those miles as business use.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

Freelancer Vehicle Expense Deductions: Standard Mileage vs. Actual Expenses

**Handle your vehicle deduction like an operator. Choose one IRS method, document business driving as you go, and escalate before ambiguity turns into risk.**

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.