Quick Answer

Use a compliance-first sequence: collect a signed Form W-8BEN before payment, then compare live quotes using the same USD amount and the same delivery route. Pick the option that shows fee, rate, and recipient peso result clearly before confirmation. For recurring contractor payments, keep one evidence set per transfer with the agreement, invoice, quote details, and final confirmation so reconciliation and tax treatment do not rely on chat history.

The Tactical Landscape: A Review of Your Standard Options#

If you need to send money to philippines from us on any regular basis, start with one number: how many Philippine pesos actually reach the recipient. The visible transfer fee matters, but it is only part of the cost. The World Bank is clear that remittance pricing is hard to compare because both fees and exchange rate margin shape the final result.

Compare the core services by what they actually disclose#

For this corridor, brand familiarity is not the right filter. What matters is whether the provider shows the fee, the rate, the payout rail, and the final PHP amount before you commit. You also need to know whether the service fits a one-off payment or a repeatable business process.

| Provider | Pricing transparency | Philippines payout rails noted here | Business use signals | Recurring workflow support |

|---|---|---|---|---|

| Wise | States it uses the live mid-market rate with a small upfront fee, and shows recipient amount | Verify current Philippines payout options in your account | Supports business customers, but verification can delay transfers by 5 to 14 working days | Standing orders supported; batch payments supported, up to 1,000 payments in one CSV or XLSX upload |

| Remitly | States it shows total cost and delivery time before you send | Cash pickup, bank deposit, mobile wallet, and more | Remitly Business exists; speed depends on payment method, delivery method, transaction review, and partner system availability | Verify current support |

| WorldRemit | States fees and exchange rates are shown upfront; Philippines page shows rate, fee, and total PHP by receive method and partner | Cash pickup, bank transfer, mobile wallet, mobile load | No business-specific feature established here | No recurring feature established here |

| Xoom | States fees vary by transaction type, payment method, and destination or currency choices | Cash pickup, bank deposit, mobile wallet, door-to-door delivery | Xoom says it is person to person and cannot be used for commercial purposes | No recurring feature established here |

| Western Union | Estimator shows fee and rate estimates, but says they are not guaranteed | Verify current Philippines payout options in estimator or app | Verify business and recurring support | No recurring feature established here |

Feature support changes by corridor, account type, and payout partner, so verify current availability before you rely on it. Based on the disclosures noted here, Wise explicitly documents repeatable workflows, Remitly and WorldRemit list multiple Philippines payout rails, and Xoom states it is not for commercial use.

Run the same true cost check every time#

The biggest comparison mistake is using the headline fee alone. Instead, run one controlled test:

- Use the same USD send amount across every provider.

- Keep the payout method identical, such as bank deposit to bank deposit or wallet to wallet.

- Record the final PHP amount shown before confirmation.

- Then separate the visible transfer fee from the exchange rate effect. A low fee with a weaker rate can still leave your recipient with less.

It takes a little longer and avoids the classic trap of chasing a "low fee" offer that quietly makes up the difference in FX spread. Save a screenshot of the quote page and the final receipt. That gives you a clean record of the promised rate, fee, payout method, and delivery estimate if you need to reconcile later.

Match speed to the payout rail and the review risk#

Speed is a tradeoff, not a promise. Remitly, WorldRemit, and Xoom say delivery can depend on payment method, delivery method, review, or partner availability. Western Union also says holds can happen while it verifies identity, confirms details, or waits on bank review.

| Payout rail | When it fits | What to confirm |

|---|---|---|

| Bank deposit | When you have the exact bank details and the recipient wants funds in an account | Exact bank details |

| Cash pickup | When banking access is limited | Required ID and reference details |

| Wallet transfers | When the exact wallet brand and registered mobile number are confirmed and the wallet is supported for the specific partner route | Exact wallet brand, registered mobile number, and partner-route support |

In practice, check speed and cost in the same quote flow for your exact funding source and payout rail. Review checks can erase an expected speed advantage. If your account needs verification, Wise says that step alone can take 5 to 14 working days.

Recipient fit matters as much as price. Bank deposit works well when you have the exact bank details and the recipient wants funds in an account. Cash pickup is useful when banking access is limited, but it may require the receiver to present the required ID and reference details. Wallet transfers are convenient, but only when you confirm the exact wallet brand, registered mobile number, and whether that wallet is supported for the specific partner route.

Before you send, check those details once, then check them again. If you catch an error right after payment, U.S. remittance rules may give you a 30 minute cancellation window, with refunds due within three business days for a valid request.

If you want a deeper dive, read Separating Business and Personal Finances: A Important Step for LLCs.

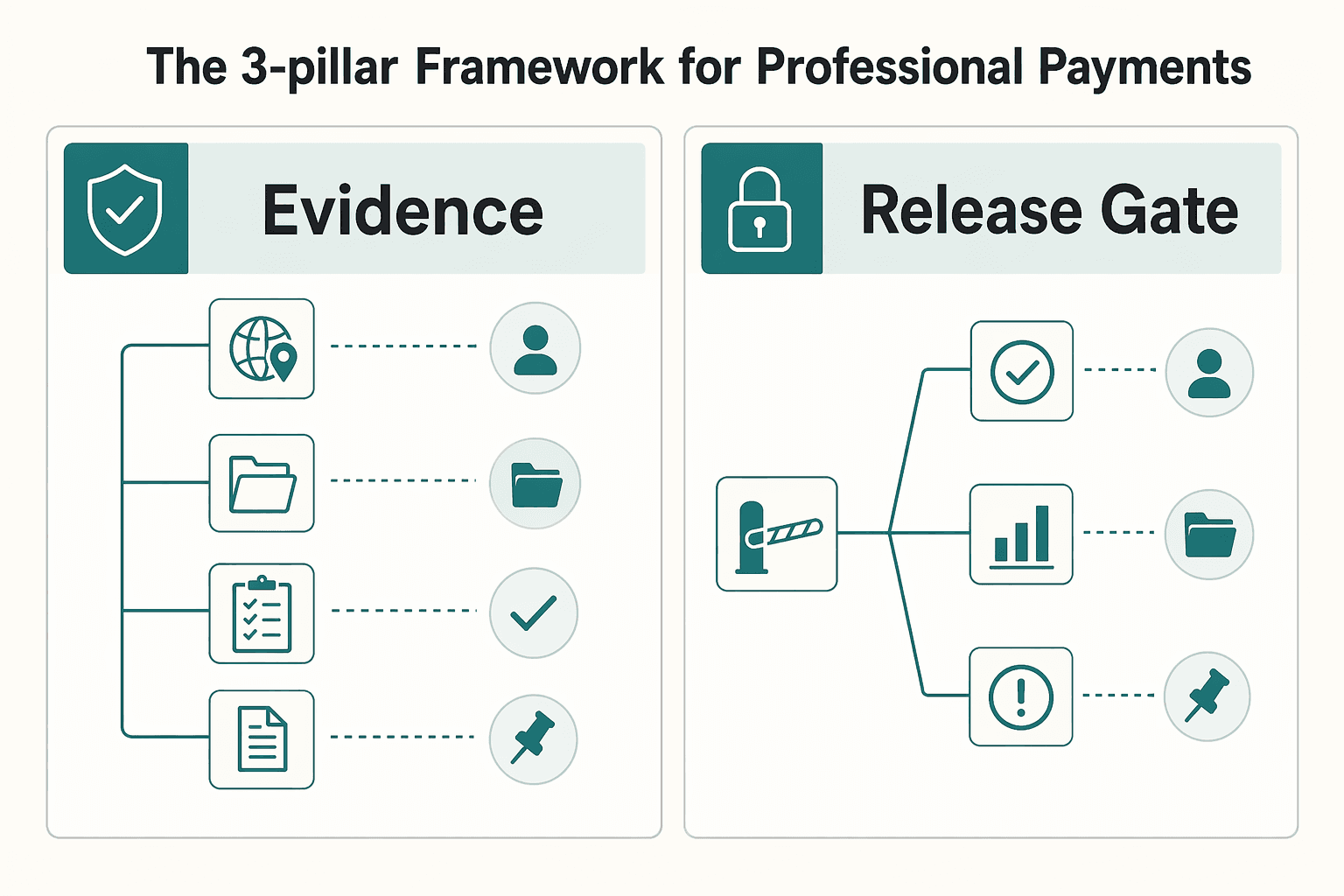

Beyond Fees: The 3-Pillar Framework for Professional Payments#

Use this framework before you choose any provider: fees and speed are inputs, but a payment workflow is only safe to repeat if it is compliant, scalable, and easy to reconcile. Run these three checks first, then decide how you send.

- Pillar 1: Compliance. If this payment is reviewed later, can you show the rule basis, the current source, and the records behind your decision? You should not be depending on memory, stale screenshots, or guidance you cannot validate.

- Pillar 2: Scalability. Will this still work cleanly when you move from one-off transfers to regular payments or multiple recipients? The process should hold up as volume grows instead of turning into manual exceptions.

- Pillar 3: Financial control. Can you reconcile each transfer from request to receipt without digging through email? You want a clean evidence pack for bookkeeping, reviews, and disputes.

| Pillar | What to check | What can go wrong | What "good" looks like |

|---|---|---|---|

| Compliance | Current source, document date, version history, saved decision record | Outdated guidance or no defensible reason for how you paid | You log the source used, when you checked it, and records tied to the payment |

| Scalability | Repeatability, approval steps, recipient data handling | A process that works once breaks at higher volume | The same steps work for the next payment without improvisation |

| Financial control | Quote proof, receipt, payout details, matching internal record | Missing audit trail, messy reconciliation, weak dispute evidence | One payment file contains quote, confirmation, and matching notes |

A practical cross-check for all three pillars is record freshness. Save the exact date or version marker for any regulatory or policy source you rely on. For example, eCFR shows when a title is up to date and last amended, and CRS products like R48150 include a PDF Version History. That habit helps you prove your process was current when you used it.

Related: The Best Way to Pay Filipino Virtual Assistants from the US. If you want a quick next step, Try the free invoice generator.

Pillar 1: How to Ensure Bulletproof Compliance#

To keep this payment process defensible, follow this order every time: collect tax status documentation first, pay second, archive records third.

| Scenario | Form or reporting path | Article note |

|---|---|---|

| U.S. person | W-9 workflow | Potentially 1099-NEC |

| Non-U.S. person | W-8BEN workflow | The contractor gives this form to you, and you keep it in your records |

| Nonemployee compensation paid to nonresident aliens | Form 1042-S | IRS guidance says this is the reporting form |

| Card and certain third-party network payments | 1099-K by the payment settlement entity | Not on 1099-NEC |

- Collect the tax form before the first payment

For a Philippines-based contractor who is a non-U.S. person, use Form W-8BEN. In plain terms, it establishes foreign status for U.S. tax handling. The contractor gives this form to you (the payer/withholding agent), and you keep it in your records.

Use this routing logic:

- U.S. person: W-9 workflow, and potentially 1099-NEC

- Non-U.S. person: W-8BEN workflow

Not every contractor payment belongs in 1099-NEC. IRS guidance says nonemployee compensation paid to nonresident aliens is reported on Form 1042-S, and foreign-source income paid to a nonresident alien is normally not required on an information return.

Operational rule: no signed W-8BEN, no payment. Also set a renewal reminder, since W-8BEN is generally effective through the last day of the third succeeding calendar year unless circumstances change.

- Keep the payment lane business-only

Keep business and personal payment activity separate. Before you release funds, confirm:

- Payment is sent from an approved business account.

- Contractor identity on the invoice matches the W-8BEN and payee profile.

- Transaction is categorized correctly in your books.

This is what turns payment history into an audit-ready record instead of scattered personal-account activity.

One routing note: card and certain third-party network payments may be reported on 1099-K by the payment settlement entity, not on 1099-NEC.

- Archive a minimum compliance file for each payment

The burden of proof is on you, so an invoice alone is not enough. Keep one folder per payment with at least the following, then confirm whether any additional jurisdiction-specific records are needed.

| File item | What to verify | Why it matters |

|---|---|---|

| Contractor invoice | Service dates, amount, scope, contractor name | Supports business purpose and deduction |

| Signed Form W-8BEN | Signed copy on file, current status, renewal date | Supports foreign-status and reporting treatment |

| Payment confirmation metadata | Transaction ID, send date, amount sent, fees, FX rate, payout method, delivery confirmation | Shows what was paid and how |

| Extra document check | Whether any jurisdiction-specific records are required | Avoids a federal-only file failing broader review |

Save this file right after each payment while details are still complete.

You might also find this useful: The Best International Money Transfer Services (Beyond Wise).

Pillar 2: Are You Making a Payment or Building a Team?#

Before you pay a contractor in the Philippines from the U.S., classify the job: one payment, or a repeat system you will run every month. If it is one invoice, optimize for a clear quote and clean proof. If it is recurring, optimize for controls and records so your process does not break as volume grows.

| Transaction type | Required workflow features | Operational risk if missing | Suitable tool category |

|---|---|---|---|

| One-off invoice or test project | Pre-funding quote, visible fee breakdown, downloadable confirmation | You cannot confirm what was paid, which FX rate applied, or whether pricing changed before funding | Consumer transfer app |

| Recurring monthly retainer (one contractor) | Saved recipient profile, repeatable payment flow, approval step, exportable payment records | Data-entry mistakes, late payments, and month-end reconciliation from screenshots and email threads | Business payments platform |

| Multiple recurring contractors | Centralized recipient data, batch-ready operations, role-based approvals, consistent accounting exports | Admin load rises with each contractor, approvals happen ad hoc, and records drift from books | Contractor management platform |

Use that matrix as a fit lens, not a provider ranking. For simple transfers, Wise or Remitly may fit when your main need is a clear quote and proof of payment. Only Wise has verified detail here: it states it uses the live mid-market rate with an upfront fee, offers a separate Wise Business path, and shows a regulator-standardized fee view. It also displays a quote window such as Rate guaranteed (20h), which you can capture with the final receipt for your records.

For Deel and Papaya Global, keep them as candidates only when your problem is recurring operations, not a one-time send. This section does not verify their pricing or feature sets. Evaluate fit by asking: can you store recipient data once, run approvals before release, and export clean records each cycle?

A practical check for recurring retainers#

If you pay the same contractor each month, your minimum workflow should include:

| Recurring control | Article detail |

|---|---|

| Scheduled payment date | Tied to the invoice or retainer cycle |

| Recipient data | Stored once and verified against each invoice |

| Approval control | At least one approval before release, especially when another person enters payment data |

| Exportable records | For bookkeeping, not only in-app confirmation screens |

Manual re-entry is the common break point: names drift, amounts change without review, and records become incomplete.

A quick readiness test#

Run this now. If you answer "no" to any two, your current setup is likely too manual:

- Can you process next month's payment without retyping recipient details?

- Can a second person review amount and destination before funds are released?

- Can you export a record that includes fee, FX rate, send date, and confirmation?

- As transfer volume changes, do you recheck route-level pricing instead of reusing old assumptions?

Wise also notes that fees vary by currency, shows examples like From 0.57% and a 6.11 USD wire fee on one screen, and says monthly discounting starts at 25,000 USD and resets on the first day of the month. It also flags that additional SWIFT fees may apply on some EUR routes outside SEPA. Same operational lesson: verify the live route each time.

We covered this in detail in The Best Way for a UK Freelancer to Get Paid by an Australian Client.

Pillar 3: Why Professional-Grade Financial Control is Non-Negotiable#

If this payment repeats, convenience is no longer the standard. The standard is whether you can document each transfer, reconcile it without cleanup drama, and retrieve records quickly. If a tool cannot do that, keep it for one-off use.

| Control area | Basic transfer app | Business-grade setup |

|---|---|---|

| Reporting depth | Receipt view or confirmation screen | Exportable records your workflow can use (for example CSV or QBO, if offered) |

| Reconciliation effort | Manual matching across invoices, bank lines, and messages | Repeatable matching from saved payee data and consistent transfer records |

| Audit defensibility | Weak when fee/rate context is fragmented | Stronger when quote and final transfer artifacts are retained together |

- Structured exports you can actually use

A receipt is proof of payment, but it is not a full bookkeeping workflow. Use a simple acceptance test: export a sample file before you commit, and confirm the fields are usable in your finance process. If you still need manual re-entry each month, the setup is not ready.

- Transfer-level records, not just "sent" status

Keep both the quote artifact and final confirmation for every transfer. Wise shows the kind of checkpoints to look for: upfront pricing, visible fee detail, the "View in the regulator's standardized format" link, and in some quotes a rate window like "Rate guaranteed (20h)." One example quote also shows "Total included fees (0.30%) 88.77 USD." Do not assume one route represents all routes. Wise also states fees vary by currency, and some paths can include extra network costs, such as additional Swift fees in certain EUR transfers outside SEPA.

- Accounting sync that behaves predictably

Treat QuickBooks, Xero, and Wise Business as examples, not guarantees. Your acceptance test is consistency: transactions land with the correct date and amount, plus enough reference detail to trace back to the invoice and transfer record. Verify current integration behavior before you lock your process around it.

Run a short monthly control routine: export activity, reconcile each transfer to invoice and bank movement, investigate exceptions, then archive the invoice, quote artifact, and final confirmation together. That turns "payment sent" into "payment provable."

For a step-by-step walkthrough, see The Best Way to Invoice a Canadian Client from a US LLC to Minimize Fees.

Conclusion: From Transactional Task to Strategic Advantage#

Once you know which payment path fits, the real job is making it repeatable. If you want fewer surprises in U.S.-to-Philippines payments, treat each transfer as part of an operating process, not a one-off click.

-

Lock down compliance first. Keep a completed Form W-8BEN on file as part of onboarding, because the IRS directs foreign individuals to provide it to the payer or withholding agent when requested. Pair it with the contractor agreement, invoice, quoted transfer terms, and final confirmation. What matters here is having one complete proof set in one place, and electronic records count under the same IRS recordkeeping rules as paper records. A common failure is having the receipt but not the form or invoice that explains why the payment was made.

-

Standardize recurring payments before you scale them. Reuse a verified recipient only after the first payout lands correctly, and keep the same naming format across the invoice, transfer, and ledger. If you repeat a transfer in Wise, the prior details can carry over, but the exchange rate will be the current mid-market rate, so you still need to review the live quote each time. The key point is that recurring does not mean hands-off. If timing or recipient details change, the error repeats just as reliably as the payment.

-

Review visibility, not just fees. Before approval, confirm any exact fee and recipient amount shown on the quote, then save the receipt and transfer history for month-end review. For remittance transfers, receipts also include a cancellation-right notice, and timing can matter because certain cancellation requests hinge on a 30-minute window after payment. The payoff is simple: a monthly reporting check catches small FX, fee, or reconciliation issues before they turn into cleanup work.

The next step is simple: confirm documentation, choose the right payment model, and run every transfer through the same checklist. That gives you fewer payment errors, lower admin friction, and more time for client work and team management.

This pairs well with our guide on The Best Way to Pay an Indian Development Agency from the US.

Frequently Asked Questions

What do you need to set up a U.S. to Philippines business payment?

Start with clean sender and recipient details: full legal names, addresses, and the purpose of the transfer. Many licensed operators also ask about your relationship to the recipient and may require a government-issued ID for verification, especially as amounts rise. If a transfer is large, including cases over $10,000 with some providers, expect extra documentation rather than assuming the first quote will go straight through.

What paperwork should you keep for each contractor payment?

Keep the contractor's agreement, invoice, quoted transfer terms, and final payment confirmation together. That set is much easier to defend later than a chat thread and a screenshot. If your provider offers exportable transfer history, save that too, because a PDF receipt alone may not be enough for month-end reconciliation.

How should you handle tax-status questions without guessing?

Do not infer status from nationality or location alone. If the contractor's tax position is unclear, check the relevant IRS classification context, including the Nonresident Alien or Resident Alien discussion in Publication 519, before you make assumptions. If facts are mixed, this is a good point to ask your tax adviser instead of improvising.

Can you rely on the cheapest advertised fee?

No. Advertised transfer fees are only part of the cost, because exchange rate margins can reduce how many pesos the recipient actually gets. A live quote might show 100 USD -> 6057.95 PHP at 60.5795 PHP, but you still need to check the fee line, the rate, and whether any receiving cost shows up elsewhere.

What is the practical way to run recurring payments without monthly cleanup?

Reuse a verified recipient profile only after the first payment lands correctly, and keep the same naming format on every invoice, transfer, and ledger entry. Before each cycle, recheck the quoted payout in PHP, because exchange rates decide the real outcome and small moves matter. One published example shows that on a $1,000 transfer, a shift from 49.50 to 50.50 PHP/USD changes the recipient result by 1,000 pesos.

Which payment path gives you the right balance of control and admin?

Use this as a screening tool, not a promise about any one provider. The deciding factor is whether the option gives you enough records and repeatability for your current team size. | Path | Control | Compliance ownership | Workflow automation | Admin burden | Total effective cost | | --- | --- | --- | --- | --- | --- | | Bank wire | High bank-level control, limited transfer UX | Requirements vary by provider and jurisdiction; verify upfront | Usually low | High | Can be hard to read because fees and FX spread are not always obvious | | Direct transfer service | High control inside the transfer tool | Requirements vary by provider; verify before relying on defaults | Varies by provider | Medium | Often clearer quotes, but still check fee, rate margin, and any receiving costs | | Contractor-management platform | Less direct control over payment mechanics | Support scope varies, so verify exact compliance/document coverage before relying on it | Varies, sometimes broader for recurring operations | Medium to lower if it fits your process | Bundled pricing varies, so judge it against time saved and error reduction |

When should you choose a direct transfer tool instead of a contractor-management platform?

Choose a direct tool when you have a small contractor roster, you are comfortable keeping payment records yourself, and you can review each payout before release. Choose a management platform when team complexity is already causing misses in contracts, approvals, or recurring payment admin. In either case, verify the export and record trail before you commit.

Should you pay extra for speed?

Only when timing matters enough to justify it. Faster delivery can cost more, while slower routes often cost less, so routine retainers are usually better handled by sending earlier rather than buying rush processing every month. If you need predictability, build a schedule buffer instead of solving every deadline with a higher fee.

What are the main security checks before you send?

Verify regulatory licensing, confirm the site uses HTTPS, and avoid public Wi-Fi when you approve transfers. Also check that recipient and destination details match your records before you confirm. If the route or recipient is new, do not approve it casually just because the app flow looks familiar.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

The Best Way to Pay Filipino Virtual Assistants from the US

There is no single best way to **pay Filipino virtual assistants**. The right choice keeps payments on time, secure, and easy to verify, not just cheap on paper.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.