Quick Answer

Use a two-track workflow: pay the local bill with the method your tax authority accepts, then review U.S. filing treatment separately. Before releasing funds, classify the cycle as personal use, rental use, or sale-year event and confirm property ID, tax period, payee, and amount. After settlement, keep one file with the notice, bank proof, local receipt, FX record, and a reconciliation note.

You can pay foreign property taxes without creating U.S. tax surprises#

Treat local payment and U.S. reporting as two separate jobs from day one. First, get the foreign property tax bill paid on time. Then make sure your U.S. tax file can support how that payment is treated. This is an operating guide, not legal advice, because local payment rules and U.S. tax outcomes depend on the jurisdiction and your facts.

FIRPTA is a clear example of that boundary. For dispositions of U.S. real property interests by foreign persons, withholding is generally reported and paid with Forms 8288 and 8288-A. Buyers are generally the withholding agents, and Form 8288 is generally due by the 20th day after disposition. If required withholding is missed, the transferee may be held liable. Those rules apply to U.S. real property interests, so do not assume they apply to non-U.S. municipal property tax bills. The point is simple: "paid" and "reported correctly in the U.S." are different tests.

For execution, focus on traceability. Keep each payment tied to the property, period, payer, and final confirmation so you can reconcile what was billed, what was paid, and what was applied.

Also keep unrelated expat rules in their lane. The foreign housing exclusion or deduction has its own eligibility tests, including a tax home in a foreign country plus bona fide residence or physical presence. Housing expenses do not include the cost of buying property. The housing amount uses a specific formula, including 16% of the maximum exclusion amount divided by 365, or 366 in a leap year. Taking a credit or deduction for certain taxes can also cause your housing exclusion choice to be treated as revoked.

Keep the rule simple: pay locally with verifiable records, then review U.S. treatment separately before filing.

How we rank the best options and who this list is for#

We rank methods by reliability and documentation first, then price. The higher-ranked options are the ones that make on-time settlement and total cost clearer before you send money. They also leave records you can actually use later and give you a clear recovery path if something goes wrong.

| Factor | What ranks higher | Article note |

|---|---|---|

| Payment certainty | Lower chance of a missed due date and confirmation matched to the exact bill | Use options where the payment details and confirmation are clear enough to reconcile the property, period, and amount without guesswork |

| Total cost | Clear exchange rate, fees, and taxes before authorization | The article compares total landed cost, not just the transfer fee |

| Proof quality | Records that can stand on their own at filing time | The file should tie together the bill, amount, currency, payer, date sent, and final confirmation |

| Failure recovery speed | Clear references and traceable support paths | Cancellation is available only in a short 30-minute window, and certain error reports can be made up to 180 days after the disclosed availability date |

| Who it fits | Recurring payments and one repeatable control set | If you pay on a recurring cycle, consistency usually beats one-off optimization |

Payment certainty#

A method ranks higher when it lowers the chance of a missed due date and gives you confirmation you can match to the exact bill. In practice, use options where the payment details and confirmation are clear enough to reconcile the property, period, and amount without guesswork.

Total cost#

We compare total landed cost, not just the transfer fee. For remittance transfers, pre-payment disclosures are meant to show the exchange rate, fees, and taxes affecting the amount received, so options that show this clearly before authorization rank higher.

Proof quality for U.S. records#

Higher-ranked options produce records that can stand on their own at filing time. IRS recordkeeping rules require documents that support income, deductions, or credits, so your file should tie together the bill, amount, currency, payer, date sent, and final confirmation.

That same discipline also helps with FBAR and Form 8938 review. FBAR, FinCEN Form 114, is filed with FinCEN, not the IRS, and Form 8938 does not replace FBAR. FBAR can be triggered when aggregate foreign account value exceeds $10,000 during the year. Some taxpayers also face Form 8938 thresholds starting at aggregate value exceeding $50,000. Directly held foreign real estate is not itself a Form 8938 asset, but an interest in a foreign entity that holds the property can be reportable. FBAR is due April 15 with an automatic extension to October 15, and FBAR account records are generally kept for five years from the due date.

Failure recovery speed#

Recovery speed matters because errors happen. For remittance transfers, cancellation is available only in a short 30-minute window after payment. Certain error reports can be made up to 180 days after the disclosed availability date, so options with clear references and traceable support paths rank higher. Use a simple rule here. Prioritize the fastest reliable confirmation when your main risk is a missed deadline. Prioritize stronger documentation when your main risk is filing stress later.

Who this list fits best#

This list is for recurring payments and for people who want one repeatable control set for local bills while managing U.S. worldwide income reporting obligations. If you pay on a recurring cycle, consistency usually beats one-off optimization.

For a true one-time transfer, you may not need this level of structure. But once foreign account tracking, FATCA-related review, or Form 8938 review is in scope, stronger records make later reporting decisions much easier. Related: How to Handle Taxes on Rental Income from Abroad.

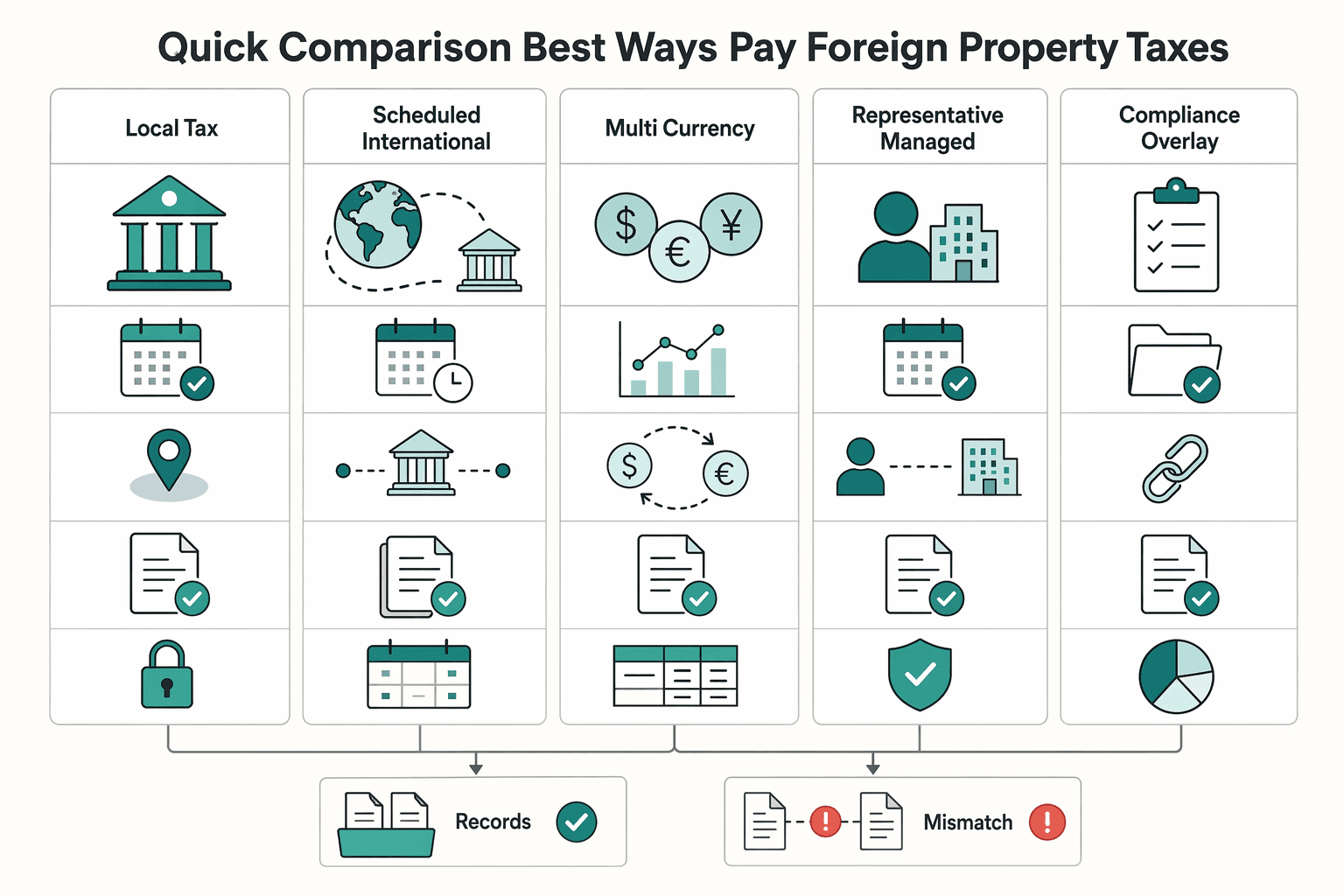

Quick comparison of the best ways to pay foreign property taxes#

Use the payment route the local authority accepts and that gives you a complete proof chain for the same property and tax period. There is no universal winner, so choose based on your main risk: missed deadline, weak records, FX timing, or dependence on a representative.

| Option | Best for | Required setup | Expected friction | Proof quality | Common failure mode | Escalation path |

|---|---|---|---|---|---|---|

| Local tax portal from dedicated account | Owners with direct portal access who want a direct path from bill to settlement | Portal credentials, dedicated paying account, correct property or taxpayer reference, receipt-download habit | Varies; often front-loaded, then lower for recurring payments | High when portal receipt, bank debit, and tax notice match | Receipt not saved, or wrong property reference used | Contact portal support, match to bank debit, request reissued receipt or posting confirmation |

| Scheduled international wire | Cases where the tax office accepts bank transfer by reference | Verified beneficiary details, exact reference format, bank template, due-date buffer | Can be higher, because one bad field may delay posting | Medium to high when wire confirmation, beneficiary instructions, and local acknowledgment are kept together | Beneficiary or reference mismatch, or incoming transfer cannot be matched | Open bank trace or recall, then contact tax office with wire reference and bill copy |

| Multi-currency balance with timed FX | Recurring bills in another currency when FX timing affects cashflow | Multi-currency account, prefunding plan, conversion record, conversion rule | Medium, because payment timing and FX timing both matter | Medium to high when conversion record, bill, and receipt are in one file | Wrong conversion amount or timing, or notice changes after prefunding | Top up or reconvert and add a reconciliation note tying notice amount, converted amount, and paid amount |

| Representative-managed payment | Owners without reliable direct access or needing local-language execution | Written authority, instruction template, approval control, required evidence checklist | Medium operations, higher oversight | Variable; depends on evidence returned | Payment made but proof is incomplete, or wrong period or property paid | Require corrected local proof and bank evidence; if repeated, change process or representative |

| Compliance overlay | Any method where you want support for foreign tax credit review, credit-or-itemized-deduction review, and worldwide income reporting | One file per property and period: notice, charge label, payer, payment date, foreign-currency amount, U.S. dollar amount, bank proof, final receipt | Moderate upfront, lower filing-time friction later | Highest when the file stands on its own | Missing tax type, mixed personal and rental records, screenshot-only records | Reconstruct from portal, bank, or representative records; if Form 1116 is relevant, keep U.S. dollar amounts, use separate forms by income category, and check one box per form |

| Caveat and confirm-before-send | Any case where local acceptance rules or income tax treaty effects are unclear | Confirm payment-route acceptance with local authority, and confirm treaty coverage for the income item | Front-loaded but necessary | Proof quality does not help if route or treaty assumption is wrong | Assuming acceptance without checking, or assuming treaty treatment applies uniformly, including state treatment | Confirm with local tax office first, then treaty position; if no treaty applies, or the treaty does not cover that income item, default U.S. rules apply |

Treat the evidence pack as part of the payment itself. Before sending, verify the property identifier, covered period, and payment reference. After settlement, confirm the final receipt matches the paid amount and period.

If you may claim a foreign tax credit, do not assume a property-related charge is automatically creditable. IRS guidance says generally only income, war profits, and excess profits taxes qualify, and you cannot claim a foreign tax credit for taxes on income you exclude. Depending on your facts, you may be able to claim either a credit or an itemized deduction for eligible foreign taxes.

For a step-by-step walkthrough, see How to Calculate Depreciation on a Foreign Rental Property.

Best for lowest operational risk: pay in the local tax portal from a dedicated account#

If you can access the local portal directly, this can be a lower operational-risk way to pay. Your notice, payment confirmation, and bank debit may be easier to match to the same property and period because there are fewer handoffs.

Why this can be a cleaner operating choice#

Direct portal payment can cut down on avoidable errors from re-entered beneficiary details, references, or tax periods. When payment happens inside the authority's own system, matching may be more straightforward than when you rely on external transfer routing.

That cleaner trail can also help when you need to support deduction review, U.S. reporting, or foreign tax credit analysis. You can keep one payer account, one receipt source, and one authority record tied to the same bill cycle.

How to keep it low risk#

Use a dedicated account as your control point, either per property or at least for foreign property expenses. Before you send payment, confirm the property identifier, covered period, and taxpayer or parcel reference exactly as shown on the notice. For one annual bill, keep one file with:

- tax notice or invoice

- portal confirmation or final receipt

- bank debit from the dedicated account

- ledger note with property name, tax year, payment date, foreign-currency amount, and U.S. dollar amount

This structure also lines up with Form 1116 recordkeeping fields, including date paid or accrued, foreign currency, U.S. dollars, and country-level separation where relevant.

Tradeoffs and red flags#

The main tradeoff is discipline. Account access, currency readiness, and receipt capture all need to be reliable. A common failure is paying successfully but saving proof that cannot later be tied back to the property or period.

Keep U.S. tax treatment separate from payment execution. A valid local payment does not automatically make the charge creditable. Generally, only income, war profits, and excess profits taxes qualify for the foreign tax credit, and you cannot take a foreign tax credit for taxes on income you exclude.

Concrete use case#

For a stable recurring cycle, keep it simple. Pay each annual bill in the municipal portal from the same dedicated account, download the final receipt, and archive it with the notice and ledger reference in one property folder.

If the paying account is foreign, remember that FBAR (FinCEN Form 114) is filed with FinCEN, not the IRS, and may apply when aggregate foreign financial accounts exceed $10,000 during the year. Form 8938 has separate thresholds and does not replace FBAR.

Use this route when you want a short path from bill to matched proof, while treating credit eligibility as a separate tax analysis step.

Best for transfer-only jurisdictions: scheduled international wire with a proof bundle#

Use a scheduled international wire when portal payment is not available, and treat documentation as part of your recordkeeping. Local payment acceptance rules and bank processing details can vary, so confirm requirements directly before sending.

Why this option works#

In practice, keep the payment instruction, account debit, and any transfer confirmation together. It makes later reconciliation easier. The tradeoff is operational: if transfer details or timing are off, matching records later may take more effort.

Order of operations to reduce rework#

- Verify payment details against the tax notice before release.

- Confirm funding account, currency, and processing timing with your bank.

- Send the transfer and save the outgoing instruction the same day.

- Capture any available confirmation that payment was received or matched.

- Archive one record bundle for your files: tax bill, transfer proof, bank debit, any local receipt, and a short ledger note with property, tax year, payment date, foreign-currency amount, and U.S. dollar amount.

If your bank only shows a generic debit after release, save the pre-submission screen or PDF instruction before sending.

U.S. reporting checkpoint to keep in view#

If your paying or holding account is a foreign financial account, keep FBAR in scope. FBAR filing is required if the maximum or aggregate maximum value of foreign financial accounts exceeds $10,000 at any point in the calendar year.

For FBAR preparation, determine each account's maximum value during the year, convert non-U.S.-currency values to U.S. dollars using the Treasury Financial Management Service rate for the last day of the calendar year, and round amounts up to the next whole dollar. If no Treasury rate is available, use another verifiable rate and document the source in your records.

This route is strongest when wire transfer is the practical channel and your records are complete enough to support later review.

Related reading: The Best Way for an Australian Agency to Pay a US-Based Contractor.

Best for recurring bills in another currency: pre-funded multi-currency balance with timed conversion#

Use this setup when the due date is predictable and you want to control FX timing instead of converting everything on deadline day. It separates conversion timing from payment timing, which can make planning easier when cash inflows are uneven.

Pros: can support steadier cashflow planning and less deadline pressure. Cons: prefunding ties up cash, and late notice changes can leave you overfunded or short.

When it helps most#

This works best when the due date is stable, you already know the payment route from prior cycles, and the current bill is usually close to prior periods. If assessed amounts or late corrections vary a lot, keep prefunding tighter and wait for the current notice before the final top-up.

How to run it cleanly#

- Set a target from the latest notice and update it when the current notice arrives.

- Log each conversion the same day: local amount, U.S. dollar amount, date, and property reference.

- Keep this balance separate from day-to-day spending so the trail stays clear.

- Before payment, match the current notice to tax year, property ID, amount due, and due date.

- Save one proof bundle: tax notice, conversion confirmations, balance statement, payment confirmation or local receipt, and a short ledger note.

If the account later shows only a generic debit, save the pre-submission conversion and payment screens.

IRS checkpoint that matters#

FX timing discipline by itself does not determine whether a tax is creditable. The IRS says the foreign tax credit is meant to reduce double taxation, and taxpayers may be able to take either a credit or an itemized deduction for foreign taxes. The IRS also says that generally only income, war profits, and excess profits taxes qualify, so do not assume a foreign property tax payment is creditable.

For potentially creditable taxes, keep Form 1116 rules in view. Individuals, estates, and trusts file Form 1116 to claim the credit. Use a separate Form 1116 for each income category, check only one category box per form, and report amounts in U.S. dollars except where Part II says otherwise. Part II tracks foreign taxes paid or accrued and includes a date paid or accrued field. The IRS also says that some foreign taxes are noncreditable even if the four tests are met. Individuals may have up to 10 years to file a refund claim for additional creditable foreign taxes.

If you exclude foreign earned income or foreign housing amounts, you cannot take a foreign tax credit for taxes on that excluded income.

If the due date is fixed but income is variable, one option is to convert in smaller tranches and stop when the current notice is covered. If cash is tight, converting closer to the due date may reduce prefunding time; prioritize a complete proof bundle.

Best for owners using local representatives: accountant-initiated payment with dual approval#

This setup can help when execution access is the bottleneck, not funding. Use a local representative to execute, but keep approval authority with you and require a complete evidence trail. The tradeoff is higher agency risk if approvals and documentation are loose.

Dual approval is a control choice, not an IRS requirement in the FIRPTA excerpts. Before any payment is sent, require the current notice and exact payment instructions, then approve only after you verify:

- property ID

- tax year or period

- amount due

- due date

- payee name and reference line, for bank-transfer jurisdictions

If any field is unclear, pause and resolve it before approval.

What to require after payment#

Ask for one complete package:

- the notice used for payment

- your written approval and the representative's execution confirmation

- payment proof with date, amount, and payee or bank reference

- local receipt, posting confirmation, or portal status evidence

- a short reconciliation note tying the payment to the exact property and reporting year

Keep this package with the property records. It does not replace FIRPTA withholding forms when a covered disposition is involved.

Where this method breaks#

The most common failure is agency risk: the wrong assessment, an outdated reference, or a generic debit that cannot be tied to the bill. A second risk appears in sale-year events, where FIRPTA withholding is a separate workflow.

For dispositions of U.S. real property interests by foreign persons, IRS guidance says:

- in most cases, the buyer (transferee) is the withholding agent

- Form 8288 and Form 8288-A are generally used to report and pay withheld tax

- both buyer and seller TINs must be included on the forms

- Form 8288 is generally due by the 20th day after the date of the disposition

- withholding is generally 15% of the amount realized (10% for dispositions before Feb. 17, 2016)

- if the transferor is a foreign person and the transferee fails to withhold, the transferee may be held liable for the tax

If your representative is involved in closing documents or withholding-related steps, separate that from recurring payment workflows and require a second reviewer.

Decide tax treatment before payment for personal use rental use or sale#

Classify each payment cycle before money moves: personal use, rental use, or sale-year event. The same local bill can lead to different U.S. record treatment, so this checkpoint should happen in writing before approval.

In the same note where you approve payment, record:

- property ID

- tax year or period

- current use classification

- whether the charge is a routine ownership bill or tied to a sale or closing step

If any of that is unclear, pause before funding.

| Classification | What to do before paying | What to archive |

|---|---|---|

| Personal use | Treat U.S. tax treatment assumptions cautiously; do not pre-label it as a tax benefit item. | Notice, payment proof, receipt or portal confirmation, and any FX conversion record used. |

| Rental use | Track as a possible rental-period item and tie it to the property's income-producing use period. | Notice, payment proof, ownership details, tax period, and a short note explaining why this cycle was treated as rental. |

| Sale-year event | Keep payment execution separate from sale-related U.S. analysis. | Closing or settlement documents, clearance or transfer-related tax records, and routine property tax records in separate folders. |

If an amount is later reviewed as a potential foreign tax credit, do not assume it qualifies automatically, and keep Form 1116 requirements in mind when you organize records. That means one income category per form, U.S.-dollar reporting, and separate country or territory lines or columns. Preserve the original currency, conversion record, and country tag in your file.

Keep FEIE and housing rules in a separate lane. U.S. citizens and resident aliens are generally taxed on worldwide income, and income excluded under FEIE is still reported on a U.S. tax return. FEIE qualification rules, including the 330 full days in 12 consecutive months physical presence test, are separate from how you classify a property tax payment cycle.

Keep the sequence simple: classify first, pay second, archive third.

Build the evidence pack before payment and close it after settlement#

The strongest control here is straightforward: build one evidence file before funds move, then close it as soon as settlement is confirmed so later U.S. reporting review is cleaner.

| Stage | What to include | Why it matters |

|---|---|---|

| Pre-payment pack | Tax notice, payee or portal confirmation, due date, FX plan, approval record, and backup payment path | Before sending funds, confirm the property ID, tax period, payee, and amount match across the notice, portal, and payment instructions |

| Post-payment pack | Confirmation ID, bank proof, local receipt or portal confirmation, and a short reconciliation note with amount paid, currency, tax period, and where the FX record is stored | Reconcile the notice against the settled amount before close so each payment can be tied to one property and one period |

| U.S. trackers | Separate references in the note for return workpapers, Form 8938 review, and FBAR tracking | The payment itself is not automatically a Form 8938-reportable asset, and filing Form 8938 does not replace FBAR |

| Consistent file structure | The same folder structure and close-out note format across properties | A practical check is whether each file quickly answers what was paid, for which property, for which tax period, and from which account |

- Pre-payment pack

Use an internal checklist, not an IRS-required format: tax notice, payee or portal confirmation, due date, FX plan, approval record, and backup payment path. Before sending funds, confirm the property ID, tax period, payee, and amount match across the notice, portal, and payment instructions.

- Post-payment pack

Close the internal file right after settlement: confirmation ID, bank proof, local receipt or portal confirmation, and a short reconciliation note with amount paid, currency, tax period, and where the FX record is stored. Reconcile the notice against the settled amount before close so each payment can be tied to one property and one period.

- Map it to the right U.S. trackers

The payment itself is not automatically a Form 8938-reportable asset. Form 8938 applies to specified foreign financial assets in which you have an interest, including certain foreign financial accounts, subject to applicable thresholds. Keep separate references in your note for return workpapers, Form 8938 review, and FBAR tracking. Filing Form 8938 does not replace FinCEN Form 114 (FBAR). If required, Form 8938 is attached to your annual return and filed by that return's due date, including extensions, and if you do not have to file an income tax return for the year, Form 8938 is not required for that year.

- Keep file structure consistent across properties

Use the same folder structure and close-out note format across properties so records are consistent at review time. A practical check is whether each file quickly answers: what was paid, for which property, for which tax period, and from which account.

Before your next due date, run a side-by-side check in the payment fee comparison so your method fits both cost and confirmation speed.

Mistakes that create cashflow strain and compliance risk#

Once the evidence pack is in place, the usual problems come from inconsistency: treating local payment as the end of the U.S. task, mixing personal and rental records, or paying at the deadline with no backup route.

Assuming local payment satisfies the United States side#

Paying a foreign property tax bill locally does not replace U.S. reporting analysis. Form 8938 and FBAR are separate tests, and you may need to file one or both. As a practical trigger, review FBAR if aggregate foreign financial accounts exceeded $10,000 at any point in the year. For some specified individuals living in the U.S., Form 8938 examples use thresholds above $50,000 at year-end or $75,000 at any time.

Operationally, tie each payment file to your annual Form 8938 and FinCEN Form 114 review, not just the property folder. Local payment can document settlement of the bill, but it does not by itself complete U.S. reporting.

Mixing personal and rental records#

Mixing records can make review harder and weaken support for return positions tied to a specific property and period. Keep notices, payment proof, rental records, and reimbursements clearly separated so the file shows what was paid and why.

This is also where documentation gaps can affect Form 1116 work. It generally requires U.S. dollar reporting, separate forms by income category, and separate country or territory lines or columns when more than one country is involved. Also, do not assume every foreign tax payment qualifies for the foreign tax credit. Generally, only income, war profits, and excess profits taxes qualify.

Paying at the deadline with no fallback route#

Deadline-day payment with no backup route can create avoidable cashflow and documentation risk. If the portal fails, details need correction, or a transfer misses cutoff, settlement evidence may not be available when you need it.

Keep a primary route and a backup route ready. Before release, confirm payee, property ID, tax period, and amount against the notice and portal, and in the final window use the route most likely to produce prompt settlement proof.

Annual U.S. and state check so paid taxes do not become surprises#

After payment, run a year-end check before return prep. Each foreign property payment should have a federal classification, a state classification, and linked records before filing.

| Review area | What to verify | Key rule mentioned |

|---|---|---|

| Federal reconciliation | Classify each paid item as personal use, rental use, or sale-year activity, and match it to the property address, local tax period, payment date, payment account, and U.S. dollar amount used on the return | For U.S. citizens and resident aliens, filing analysis starts with worldwide income; if aggregate foreign financial accounts exceeded $10,000 at any point in the year, include those accounts in FBAR review |

| California or state review | Residency status, move dates if relevant, and why the foreign property activity is included or excluded | California residents are taxed on worldwide income, part-year residents are taxed on worldwide income during the resident period, and nonresidents are taxed on California-source income; California's Other State Tax Credit is designed for taxes paid to another state |

| Treaty and Form 1116 review | Test any foreign tax credit position directly against IRS rules and Form 1116 requirements before filing | The foreign tax credit generally applies to foreign taxes paid or accrued on foreign-source income that is also subject to U.S. tax, and you cannot claim a credit for taxes on income excluded under the foreign earned income exclusion |

Reconcile every payment to one U.S. use case#

Start by classifying each paid item as personal use, rental use, or sale-year activity, then keep that label with the file through return prep.

For U.S. citizens and resident aliens, filing analysis still starts with worldwide income, and return requirements are tied to worldwide gross income thresholds, not local-country filing outcomes. Match each payment record to the property address, local tax period, payment date, payment account, and U.S. dollar amount used on the return.

Also verify that the tax receipt and bank proof match. If property references conflict, fix them now. If your aggregate foreign financial accounts exceeded $10,000 at any point in the year, include those accounts in FBAR review and keep the related account records with the same tax file.

Run a separate state review if California is anywhere in the picture#

If California is in scope, run a separate state pass because residency status drives treatment.

California residents are taxed on worldwide income, part-year residents are taxed on worldwide income during the resident period, and nonresidents are taxed on California-source income. So foreign property activity can still affect a California filing analysis depending on your status and timing.

Do not assume federal outcomes carry over automatically. Treaty treatment is not uniform at the state level, and California's Other State Tax Credit is designed for taxes paid to another state. Keep a state-only memo in your file with residency status, move dates if relevant, and why the foreign property activity is included or excluded.

Finish with treaty and Form 1116 review before you lock the return#

Before finalizing, test any foreign tax credit position directly against IRS rules and Form 1116 requirements.

The foreign tax credit generally applies to foreign taxes paid or accrued on foreign-source income that is also subject to U.S. tax, and Form 1116 is used to claim it. If income was excluded under the foreign earned income exclusion, you cannot also claim a credit for taxes on that excluded income.

If you rely on treaty treatment, review it article by article before filing. IRS guidance also warns that treaties often do not reduce U.S. tax for U.S. citizens or treaty residents, with exceptions, and states vary on treaty conformity. Finally, do not assume every foreign property-related levy qualifies for the credit. Confirm eligibility before it reaches Form 1116.

Choose the method you can execute on schedule and document end to end#

The best method is the one you can run on deadline with low failure risk and a complete evidence trail. Use the same sequence every time: classify the payment file, execute one repeatable method, verify settlement, archive proof, then complete U.S. reporting checks.

- Classify the payment file before you send money

Tag the payment to the correct tax year and keep the funding account details with the file from day one. That avoids rework later when you need to support reporting analysis.

- Use one repeatable payment path per property

Use a single method you can execute the same way each cycle. Consistency is what keeps records complete and easy to trace.

- Verify settlement, not just transmission

Keep proof that the liability was actually settled, not only that funds were sent. Match amount, tax period, payer identity, and local confirmation before you close the cycle.

- Archive one complete evidence pack

Keep the notice, payment confirmation, bank proof, local receipt, and a short reconciliation note in one place. If those pieces are split across tools and inboxes, fix that before you optimize fees.

- Close U.S. reporting checks while details are fresh

If Form 8938 applies, attach it to your annual return and file it by that return due date, including extensions. Specify the applicable calendar year or tax year. Filing Form 8938 does not replace a separate FBAR filing (FinCEN Form 114) when FBAR is otherwise required. Form 8938 threshold analysis can begin at $50,000 for certain taxpayers, and IRS states higher thresholds apply to joint filers and taxpayers residing abroad. If you do not have to file an income tax return for the tax year, you generally do not need to file Form 8938. Keep that analysis separate from the property tax payment itself.

If you want a repeatable setup with dedicated receiving details and clearer payment traceability where enabled, review Gruv Virtual Accounts.

Frequently Asked Questions

Do I still need to report in the United States if I already paid foreign property tax locally?

Yes. Paying foreign property tax locally does not by itself remove U.S. filing or reporting obligations. If the same income is taxed abroad and in the U.S., you may be able to claim a credit or an itemized deduction, and the credit is generally claimed on Form 1116. For foreign tax credit purposes, qualifying taxes are generally income, war profits, and excess profits taxes.

Is foreign property tax deductible if the home is personal use rather than rental use?

Do not assume a personal-use foreign property tax payment is automatically deductible. For foreign tax credit purposes, IRS rules are generally focused on income-based taxes, so a local property levy may not qualify for the credit. Treat this as a classification decision first, then map it to the correct U.S. filing treatment.

How does a foreign property sale change my U.S. tax exposure under capital gains tax rules?

A sale year should be reviewed as a separate tax situation, not folded into routine annual property tax handling. Recheck each sale-related payment, confirm what type of tax it is, and keep the supporting documents together for return prep. If a payment is evaluated on Form 1116, amounts are generally reported in U.S. dollars.

Do foreign housing exclusion or foreign housing deduction rules cover the cost of buying property?

Do not treat the foreign housing exclusion or deduction as covering the cost of buying property. IRS guidance also says you cannot claim a foreign tax credit for taxes on income you exclude under foreign earned income or foreign housing cost elections. Review any property-purchase-related treatment separately before filing rather than assuming it fits these elections.

What records should I keep to support foreign tax credit, FBAR, and Form 8938 reporting?

Keep records that support the tax amounts reported and the U.S. dollar amounts used in return prep. For FBAR and Form 8938, keep records that support account values and threshold testing, including highest balances during the year. FBAR can apply when aggregate foreign account value exceeds $10,000 at any point in the year, and Form 8938 has separate thresholds, for example $50,000 or $75,000 for specified unmarried or married filing separately individuals living in the U.S., and $100,000 or $150,000 for specified joint filers living in the U.S. Form 8938 does not replace FBAR, and FBAR is filed with FinCEN, not with the IRS.

How do tax treaties affect what I owe versus what I still must report?

Tax treaties do not automatically eliminate U.S. reporting. You still need to test your filing obligations form by form, including whether Form 8938, FBAR, or both apply. Keep your treaty position documented with your return records.

What details are still country-specific and must be confirmed locally before I pay?

Country-specific payment mechanics must be confirmed with the local authority before payment. For U.S. foreign tax credit analysis, verify that a tax was legally owed and not refundable, because taxes you do not legally owe, including refundable amounts, are not creditable. Keep local proof aligned with your U.S. file so each payment can be matched and reviewed later.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

How to Report Foreign Rental Income on a U.S. Tax Return

When dealing with `us tax on foreign rental income`, start conservatively: treat reportability and treatment as unresolved until primary IRS authority for your facts says otherwise.

How to Invest in Real Estate as a Digital Nomad

**Run anything with money and moving parts like an operations system (cash, docs, delegation, and controls), not a "passive income" vibe.** Real life stress-tests weak spots. You change time zones, a client pays late, and something breaks at the worst moment. As the CEO of a business-of-one, your job is to build a setup that keeps working when you are not available on demand.