Quick Answer

Start by writing the money rules first: decide who fronts costs, map each expense bucket, and require approval plus documents before reimbursement. For shared expenses with freelance collaborator setups, use one split method per project phase and tie repayment to clear payment terms instead of expected cash. Keep one record system for invoices, receipts, and proof of payment, then reconcile on a fixed cadence. If funds are delayed, pause new shared spend rather than letting one partner float the project indefinitely.

Shared expenses with a freelance collaborator only work when cashflow rules are set first#

Shared expenses often run into timing issues before trust issues. If you want this arrangement to stay fair, start with cash timing, not goodwill. Decide how money comes in, who can spend it, and what proof is required before anyone treats a cost as shared.

- Set the fronting rule before the first purchase.

Problems start when one person keeps paying out of pocket and the other assumes the next client payment will square things up. That is a cashflow problem, not a trust problem. If you cannot say who fronts software, travel, ads, or contractor fees, treat the spend as the buyer's own cost until both sides approve it in writing.

- Tie spending to actual payment terms, not expected money.

An invoice is not cash in your account. Payment terms define what is owed, when it is due, and how it will be paid. Some platforms also add a delay after the client approves payment. On Upwork fixed-price work, milestone funds can stay in review for up to 14 days. They then move to a five-day security hold before withdrawal. If your collaboration depends on those funds to pay someone back, say that before kickoff so nobody spends against money that is not yet liquid.

- Classify every expense before payback is even possible.

Put written categories in your books instead of burying expense decisions in chat. A practical approach is to use buckets such as shared project costs, individual overhead, and non-reimbursable items. In that setup, only shared project costs are eligible, and only when the purchase was approved under the agreed rule. If a cost is not mapped first, treat that as a red flag. Retroactive classification creates avoidable disputes.

- Verify with documents, not memory.

The IRS standard is useful here even if your immediate concern is bookkeeping, not tax filing. You generally need documentary evidence such as receipts, canceled checks, or bills to support expenses. At minimum, each record should show the payee, amount paid, proof of payment, and date incurred. It also helps to include the purpose and project tag so your books reflect real business transactions instead of scattered screenshots.

That is why "we'll sort it out later" can get expensive, even when it sounds practical in Reddit or Quora threads. Clean shared-cost repayment starts with boring specifics: category, split rule, payment terms, and evidence. If one of those is missing, stop the expense or treat it as personal spend until the record is fixed. For more on cash timing, see Automating Freelance Finances Without Losing Cashflow Control.

How to choose the best shared-expense method for your collaboration#

Choose a method only after roles are documented and money rules are written. If responsibilities are still verbal or unclear, fix that first with a Subcontractor Agreement or a Joint Venture Agreement.

Use these four checks before you lock in a shared-expense method:

- Documented ownership before spend

Assign each expense in advance: who buys it, what project purpose it serves, and whether it is shared, personal overhead, or non-reimbursable. If ownership is unclear before purchase, the method is too loose.

- One recordkeeping source for all proof

Use one recordkeeping system for invoices, receipts, paid bills, and reimbursement entries. Your books should clearly show income and expenses and include a summary of business transactions, with supporting documents that let either collaborator verify a charge quickly.

- Pre-approval triggers in writing

Define what must be approved before money moves, and by whom. The exact trigger can vary, but the rule should be explicit enough that urgency cannot be mistaken for authorization.

- Recurring close discipline tied to tax support

Reconcile shared costs on a recurring cadence you both follow, and keep documentation that supports deductions under the ordinary-and-necessary standard, including where records may flow into Schedule C support. The IRS does not mandate one universal monthly-close schedule, but your method should still produce complete, reviewable records.

You might also find this useful: How Freelancers Can Use Accrued Expenses to Make Better Close Decisions. If you want a quick next step, Try the free invoice generator.

The 5 best ways to split shared expenses and when each wins#

Once ownership and approval rules are written, the best method is the one you can apply consistently at close with minimal judgment calls. Start with equal split for stable recurring costs, then switch to effort, usage, pass-through, or hybrid rules when contribution or benefit is no longer even.

| Model | Best when | Key detail |

|---|---|---|

| Equal split model | Contribution is similar and costs are predictable | Straight 50/50 for recurring software, shared storage, or basic admin spend; gets unfair fast if variable production costs creep in |

| Effort-based split model | Labor is uneven and one collaborator carries more delivery work | Allocation follows actual work performed; keep time records tied to tasks or deliverables |

| Usage-based split model | One collaborator drives most tool consumption, ad spend, contractor minutes, or software seats | Allocate after costs are incurred using actual usage; you need exports, seat counts, or platform reports |

| Client-funded pass-through model | Low-float teams that need to protect cashflow | Third-party project costs are billed back to the client at or near cost, with approval and payment terms set before spend |

| Hybrid cap model | Longer projects with both stable and variable costs | Use a fixed base split for recurring costs, then a month-end true-up for over-cap items based on actual effort or actual usage |

- Equal split model

This wins when contribution is similar and costs are predictable. Use a straight 50/50 rule for recurring software, shared storage, or basic admin spend. It keeps bookkeeping simple because every approved charge follows one rule, but it gets unfair fast if variable production costs creep in. Review the fixed-cost list monthly and match each charge to a receipt, proof of payment, and project purpose.

- Effort-based split model

This wins when labor is uneven and one collaborator carries more delivery work. It is usually fairer than a flat split because allocation follows actual work performed. The model fails when effort evidence is weak, so keep time records tied to tasks or deliverables. If you also have profit-sharing or revenue-sharing terms, keep expense allocation separate from payout logic to avoid compounding disputes.

- Usage-based split model

This wins when one collaborator drives most tool consumption, ad spend, contractor minutes, or software seats. It is strongest when you allocate after costs are incurred using actual usage, not estimates. The tradeoff is bookkeeping load: you need exports, seat counts, or platform reports that show who used what. If exact proportions are unclear, use a reasonable documented basis and define one unit of measure upfront.

- Client-funded pass-through model

This wins for low-float teams that need to protect cashflow. It works when third-party project costs are billed back to the client at or near cost, with approval and payment terms set before spend. Your contract should define eligible expenses, pre-approval rules, and how those costs appear on invoices. Do not treat every project expense as pass-through if some costs are your own operating overhead.

- Hybrid cap model

This wins on longer projects with both stable and variable costs. A practical version is a fixed base split for recurring costs, then a month-end true-up for over-cap items based on actual effort or actual usage. You get predictability without forcing every line into one rule. Make the cap categories, true-up timing, and reallocation basis explicit in writing so "we'll settle later" does not become a dispute.

If you want a deeper dive, read The Best Way to Manage Shared Finances in a Business Partnership.

Classify every cost before anyone spends#

Pre-spend classification prevents most reimbursement disputes and makes tax records defensible. Set your buckets before kickoff, tie each one to reimbursement eligibility, and treat any unmapped purchase as the buyer's own cost until both collaborators approve a different treatment in writing.

| Bucket | Use for | Handling note |

|---|---|---|

| Shared project costs | Expenses directly tied to a specific client deliverable | Mark each item with a project tag, purpose note, and approver so reimbursement is clear and traceable |

| Individual overhead | Costs that support one collaborator's business across multiple jobs | Supplies, platform fees, and ongoing marketing are not automatically payable by the other collaborator |

| Non-reimbursable or mixed-use costs | Personal, convenience, or mixed-use spending | If an item has both business and personal use, track the business portion separately from day one |

The reason is practical: you need records that can substantiate expenses, and those records are much easier to keep when the purpose and bucket are decided before the charge hits.

- Shared project costs

Use this only for expenses directly tied to a specific client deliverable. Mark each item with a project tag, purpose note, and approver so reimbursement is clear and traceable.

- Individual overhead

Use this for costs that support one collaborator's business across multiple jobs. Expenses like supplies, platform fees, and ongoing marketing may be ordinary and necessary for that person's business, but they are not automatically payable by the other collaborator.

- Non-reimbursable or mixed-use costs

Put personal, convenience, or mixed-use spending here until it is split correctly. If an item has both business and personal use, track the business portion separately from day one to support Schedule C reporting.

Quick stress test:

- An Airbnb stay used only for a client shoot can fit shared project costs; extra personal nights do not.

- Etsy listing fees or always-on shop marketing usually fit individual overhead.

- On TaskRabbit, keep reimbursed materials separated from platform totals so filing adjustments are easier.

Use one enforcement rule: no receipt, no project note, no pre-mapped bucket, no payback. Need the full breakdown? Read A Guide to QuickBooks Self-Employed for Freelancers.

Lock payment terms and approval gates before client kickoff#

Lock spending authority, funding order, and reimbursement timing in one signed agreement before kickoff so payment decisions stay predictable when pressure rises.

- Set approval gates before any spend

Put authorization rules in writing before an expense exists. Name who can approve routine costs, which categories need both collaborators to approve, and what happens when spend goes over the agreed plan. Treat pre-approval as the default, and treat costs without an approval record as unauthorized until reviewed.

- Sequence invoices around funded work

Use this order: funded milestone or client deposit first, then spending. This mirrors fixed-price protection models where client funds are deposited before work begins and reduces float risk for either collaborator. If funding is not in place, avoid fronting large pass-through costs.

- Define exception handling and payout timing

Decide in advance how out-of-policy spending is handled: reduced reimbursement, delayed reimbursement after client payment, or reimbursement only after written ratification by both collaborators. Require an itemized expense statement for any exception request. Set a payout window in the contract (for example, payment within 30 days after receiving the statement).

- Align internal terms with upstream agreements

If one collaborator is a subcontractor, confirm the client contract and related agreements allow that setup before kickoff. Keep your internal expense rules consistent with those documents so obligations do not conflict. If you use a Subcontractor Agreement or Joint Venture Agreement, review any incorporation clause so it does not import duties that break your agreed cost-sharing logic. If you need a deeper checklist, see Hiring Your First Subcontractor: Legal and Financial Steps.

If approval rules, funding checkpoints, and reimbursement timing are scattered across different docs or message threads, fix that before work starts.

Build the evidence pack that prevents reimbursement fights#

Reimbursement disputes usually start when an expense record is incomplete, so treat missing evidence as "not yet payable" until the record is fixed.

- Use one standard record for every expense

Require the same fields each time: receipt or paid bill, business purpose, project tag, approver, payment proof, amount, date, and who paid first. Your recordkeeping system should clearly show income and expenses, and supporting documents should back each entry. Consistent records do more than speed bookkeeping; they also support what you report on your return.

- Set verification checkpoints while details are still easy to confirm

Weekly receipt checks and monthly reconciliations are practical controls, not IRS-required cadences. Weekly, confirm new expenses include the required evidence and the listed approver matches your agreement. Monthly, reconcile the expense log against client invoice collections, collaborator reimbursements, and open balances so issues are caught before memory and documents fade.

- Keep tax-ready fields visible from day one

For Schedule C support, records should make it easy to show source, amount, and business purpose, and to explain why a cost is ordinary and necessary. Keep category, vendor, date, amount, payment status, and pass-through vs. own-business classification in the log from the start. That reduces last-minute reconstruction and lowers deduction-risk errors.

- Treat Mercury and TurboTax as support, not authority

Tools can help store entries, attach receipts, and organize bookkeeping, but they do not replace written collaborator terms on approval, split rules, and payout timing. Use them as system-of-record support, not as a substitute for your agreement. Most disputes still come down to contract logic: whether the expense was approved and how reimbursement is triggered.

A reliable red flag is any entry with only one proof point, such as a receipt without payment proof or a charge without a business purpose. That is where reimbursement fights usually begin. This pairs well with our guide on The Best Way to Pay Freelance Collaborators in Europe from the US.

Pick a reimbursement cadence that protects cashflow#

Choose the reimbursement rhythm based on how long either collaborator can safely float approved costs, then enforce the same cutoff and review process every cycle.

| Cadence | Best fit | Tradeoff |

|---|---|---|

| Weekly reimbursement | One person is regularly fronting costs and cannot carry a long float | More bookkeeping overhead, and payment can still take a few business days after approval in some systems |

| Milestone reimbursement | Shared costs map clearly to project stages that trigger invoicing and payment as work progresses | Timing exposure if release is delayed, because milestone funds can be held until client release and disputes can interrupt release timing |

| Monthly reconciliation | Records are already disciplined and collections are predictable | The person fronting costs may carry the balance for longer |

- Weekly reimbursement

Weekly is usually safer when one person is regularly fronting costs and cannot carry a long float. Weekly and monthly batching are both common operational setups, and shorter cycles reduce how long balances stay outstanding. Keep one fixed weekly cutoff for receipt, approval, business purpose, and proof of payer; otherwise you add admin work without improving control. Tradeoff: more bookkeeping overhead, and payment can still take a few business days after approval in some systems.

- Milestone reimbursement

Use milestone reimbursement when shared costs map clearly to project stages that trigger invoicing and payment as work progresses. This keeps payback aligned with the same events driving client billing. Tradeoff: timing exposure if release is delayed, because milestone funds can be held until client release and disputes can interrupt release timing. Do not reimburse large items from milestone funds that are expected but not yet released.

- Monthly reconciliation

Monthly works when records are already disciplined and collections are predictable. It fits a month-end close approach: review, reconcile, and finalize monthly activity in one cycle. Tradeoff: the person fronting costs may carry the balance for longer. Before paying out, reconcile receipts, approvals, invoice collections, and unpaid collaborator balances.

If payment timing is unstable, use weekly or milestone-based reimbursement. If collections are steady and month-end reconciliation is consistent, monthly can reduce operational noise. Related reading: Building a Portfolio Career With Multiple Freelance Income Streams.

Red flags that predict disputes and payment loss#

Most payment disputes are visible early. If any of these patterns show up, pause new shared spending and tighten your written terms before the next receipt lands.

- Shared spending with no written scope

If a cost is not tied to an agreed deliverable, owner, and split rule, you are already in dispute territory. Scope creep is a common trigger: work expands beyond the agreed scope without matching budget or responsibility updates. Fix this by documenting role splits and payment terms before work continues, and require each new cost to map to a current scope note, project tag, and approver.

- "We'll settle later" language

This usually means no one has set timelines, limits, or evidence requirements. Reimbursement rules work when they clearly define documentation and submission and approval timing. Set a repayment date, require receipt evidence plus business purpose and payer proof, and record it in bookkeeping on a set schedule.

- One person repeatedly fronts costs before client funds are in place

This is credit risk, not a durable workflow. If expenses depend on client money, require pre-funding through a deposit or milestone payment before purchase, or define a clear stop-work trigger when funds have not cleared. Without that control, the collaborator carrying the float effectively becomes the unpaid lender.

- Copy-pasted advice from Reddit, r/MiddleClassFinance, or Quora

Generic threads can give you ideas, but they do not reflect your contract or approval process. Use them as prompts only, then test each rule against your signed terms, documentation workflow, and tax setup. Public internet advice can be wrong or incomplete, so treat it as input, not policy.

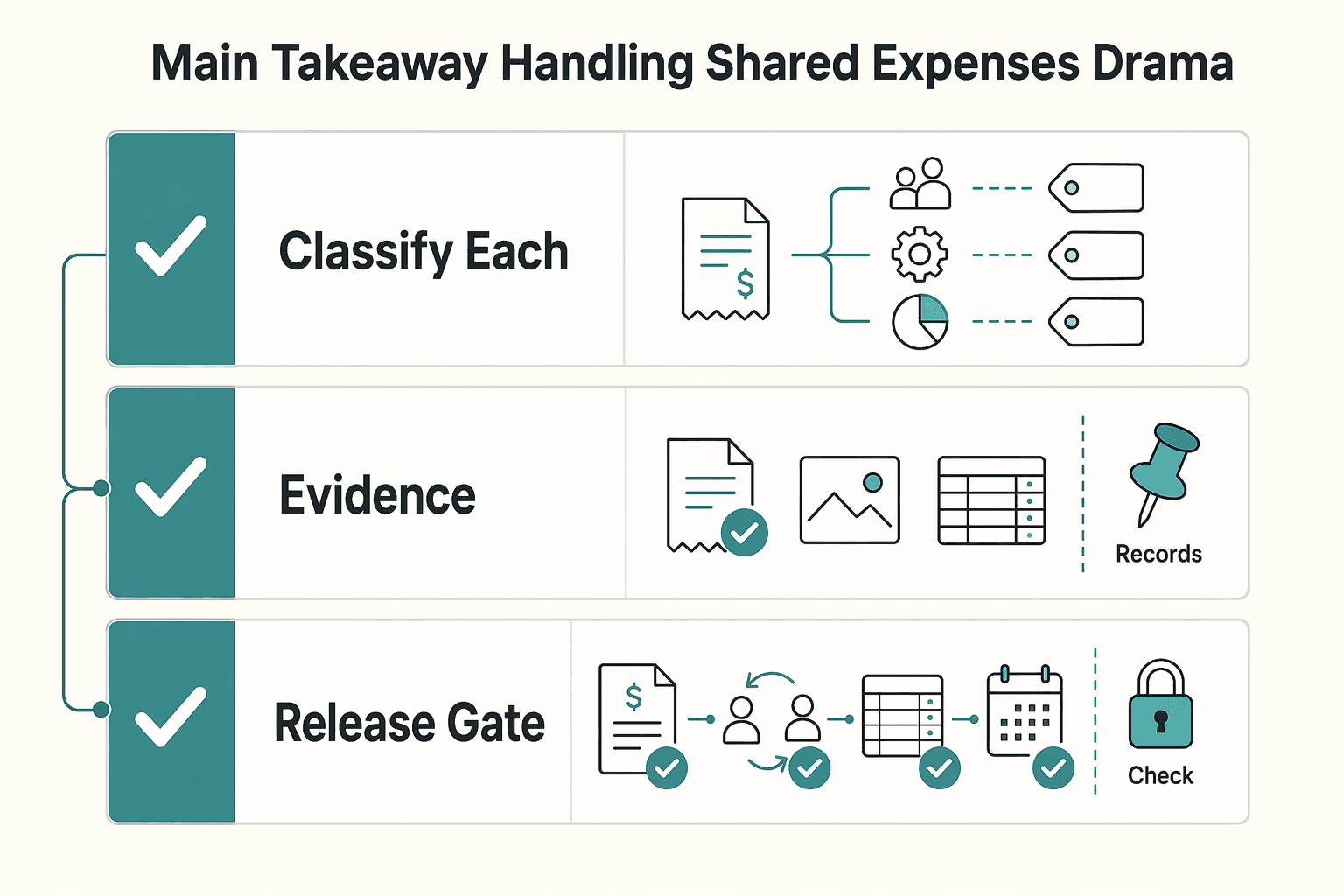

The main takeaway for handling shared expenses without drama#

The lowest-drama setup is strict and connected from the start: define cost allocation, set reimbursement rules, keep records, and keep invoice, payback, bookkeeping, and payment terms in one written system.

-

Classify each cost before anyone spends. Mark expenses as shared project cost, individual overhead, or non-reimbursable in advance. If a cost was not mapped and approved, treat it as the buyer's cost until both parties approve it in writing.

-

Use one split rule per phase and document it in the Shared Expenses clause. The point of this clause is clear financial responsibility, which helps prevent payment disputes. If the project scope changes, update the rule for the next phase instead of reworking past charges.

-

Tie reimbursement to a defined process in the Reimbursement of Shared Costs clause. State eligible cost types, how requests are submitted, and any approval limits. This gives you a clear decision path when spending falls outside the agreed process.

-

Reconcile from source documents, not memory. Keep the records that feed bookkeeping and tax entries, including items like paid bills, invoices, receipts, deposit slips, and canceled checks. Consistent documentation keeps small disagreements from turning into bigger payment and accounting problems.

That is the core takeaway: when one control is missing, disputes become predictable. Keep the rules written, specific, and connected.

For a step-by-step walkthrough, see How to Create a Business Budget for Your Freelance Business.

Frequently Asked Questions

What is the best way to split shared freelance project expenses when effort is unequal?

Use an effort-based split or a hybrid cap, not a default 50/50 rule that both sides quietly resent. The deciding factor is evidence. Tie the split to something you can verify later, such as approved hours, deliverables, or a written ownership percentage for that project phase. If the work mix changes mid-project, do a regular true-up instead of waiting for the final payback argument.

Which expenses should be shared versus treated as individual overhead?

Share costs that are clearly tied to the client job and approved in advance, like project-specific software, travel, or production spend. Treat standing business costs as individual overhead unless your agreement says otherwise, such as your baseline laptop, home internet, or general subscriptions you would pay for anyway. A useful check is whether the cost is ordinary and necessary for operating your business and clearly tied to the project work.

How often should collaborators reimburse each other to avoid cashflow strain?

There is no single required cadence, so pick the one that matches who is fronting the money and when the client invoice gets paid. Weekly payback can reduce float when cash is tight, milestone-based payback can fit projects with funded stages, and monthly reconciliation can work when neither person is carrying painful balances. If one person keeps covering material costs before client funds clear, shorten the cycle and pause new spending until the balance is settled.

How should shared expenses appear on client invoices and internal records?

On the client side, keep project expenses visible as separate invoice line items when you plan to pass them through, rather than burying them inside labor. Internally, each expense should carry a basic evidence pack: receipt, paid bill, or invoice, plus business purpose and project context. Supporting documents matter because tax and bookkeeping records are stronger when backed by invoices, receipts, deposit slips, canceled checks, or similar source documents.

How do shared expenses affect tax deductions and Schedule C reporting?

For Schedule C support, the standard is not “we both touched the project,” but whether the cost was ordinary and necessary for operating your business and whether you can substantiate it. In practice, that means your books should show the business purpose, your share of the expense, and the source documents behind it. If mileage is part of the expense, the 2025 Schedule C instructions cite a standard mileage rate of 70 cents per mile for business use.

What should a collaborator agreement include to prevent reimbursement disputes?

Your agreement should name which expenses are shareable, how each share is calculated, and the process for documenting and paying back those costs. It should also state who can approve spending, what happens when someone spends outside the agreed terms, and how disputes get resolved before they become write-offs. A written partnership or collaborator agreement is a practical control because it gives you something concrete to point to when memory and expectations no longer match.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- controller.ucsf.edu/reference/sponsored-research-post-award-admi...trusted

- ecfr.gov/current/title-2/subtitle-A/chapter-II/part-2...trusted

- ecfr.gov/current/title-13/chapter-I/part-125/section-...trusted

- finance.uw.edu/travel/files/pdf/EXP-J-03-How%2Bto%2BCreate%...trusted

- irs.gov/businesses/small-businesses-self-employed/wh...trusted

- irs.gov/businesses/small-businesses-self-employed/bu...trusted

- itap1.for.irs.gov/owda/0/resource/Commentary_Files_Redirect_IT...trusted

- law.cornell.edu/wex/subcontractortrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Hiring a Subcontractor for the First Time Without Costly Surprises

**Start with a risk-control sequence, not an ad hoc handoff.** As the Contractor, your goal is simple: deliver cleanly, control scope, and release payment only when the work and file are complete.

How to Structure a Joint Venture Agreement Between Two Freelancers

Treat the **freelance joint venture agreement** as a working document you can use day to day, not a ceremonial signature page. Put it in place before work starts so everyone involved is working from the same written terms.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.