Quick Answer

Use the lightest IRS channel that can finish the job, then keep proof of every interaction. Start with Online Account for Individuals or live chat for simple checks, use the International Taxpayer Service Call Center for narrow account questions, move to tracked mail or fax for written responses or deadline-driven submissions, and consider a tax professional with Form 2848 for audits, disputes, collections, or appeal-rights letters.

Before You Contact the IRS: Triage Your Mission Like a CEO#

Before you reach the IRS from abroad, make three decisions in order: your objective, your practical risk level, and the proof you need to keep. This is not an IRS term. It is a working method that helps you avoid repeated contacts and weak records.

1. Write your one-sentence objective#

Start with a verb: Confirm, Request, Respond, Dispute, or Authorize. If you cannot state success in one sentence, pause before you reach out.

If your need is routine account visibility, check whether Online Account for Individuals can solve it first, such as your balance, payments, tax records, or notices. If you are a new user, have photo identification ready for setup.

2. Classify the issue before choosing a channel#

Rate risk by consequence, not stress level:

| Issue type | Best first channel | Proof to retain | Escalation trigger |

|---|---|---|---|

| Simple status or account question | Online Account for Individuals, then International Taxpayer Service Call Center at 267-941-1000 (Monday-Friday, 6 a.m. to 11 p.m. Eastern). If you are outside the U.S., live chat can help with amended return questions or transcript requests. | Dated notes, screenshots, and any reference number | Issue stays unresolved or IRS says the question is too complex for telephone assistance |

| Deadline-driven response or international account issue submission | Fax 681-247-3101 (international tax account issues) or mail to International Accounts (Philadelphia for individuals outside the U.S., Ogden for businesses outside the U.S.) | Full copy of submission, fax confirmation, any mail tracking or delivery records, and the IRS notice | Deadline risk, mismatch in IRS records, or rejected or unmatched documents |

| Audit, collection, penalty dispute, or appeal-rights letter | Consider a tax professional first. Use Form 2848 if a representative will speak to IRS without you present | IRS letters, prior correspondence, return support, timeline, and signed authorization documents | Appeal rights or active collection. Written protest timing is critical, generally 30 days from the letter date, and the protest must go to the address on the letter, not directly to Appeals |

3. Set your evidence standard before outreach#

Match the proof to the mission. If you only need information, detailed notes may be enough. If you need to prove a timely response or protect your rights, build a stronger evidence file before contacting the IRS.

| Situation | Proof or form | Practical note |

|---|---|---|

| You only need information | Detailed notes | May be enough |

| You need to prove a timely response or protect your rights | Stronger evidence file | Build it before you contact the IRS |

| Someone only needs to review or receive your tax information | Tax Information Authorization | May be enough |

| Someone will represent you before IRS | Form 2848 | Use Form 2848 |

Do not use email for sensitive tax data. IRS states it will never initiate contact by email and tells taxpayers not to send sensitive personal information that way. Also plan around current centralized international channels, since foreign-post taxpayer service is no longer available.

If someone only needs to review or receive your tax information, a Tax Information Authorization may be enough. If they will represent you before IRS, use Form 2848.

4. Build a contact packet and run a 60-second check#

Prepare one packet so you can complete a call, fax, or mailing without gaps:

| Packet item | Include |

|---|---|

| Identity | Legal name, Social Security number, and verification details needed for account help |

| Case file | Relevant return, IRS notices, prior correspondence, payment records |

| Mission sheet | One-sentence objective, risk level, deadline, exact question |

| Evidence set | Documents you will send, plus your fax or mail proof method |

| Authority docs | Form 2848 or Tax Information Authorization, as needed |

Quick check before you reach out: can you state your objective in one sentence, name the exact channel or address, and show what proof you will keep if receipt is later questioned? If not, finish the packet first.

If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Step 2: Select the Right Channel for Your Mission#

Choose the channel based on what you need to accomplish. Use the lightest option that can finish the job, then escalate quickly if the issue shifts from information to documentation, deadlines, or dispute risk. Keep one operating constraint in mind: IRS taxpayer service at foreign posts of duty is no longer available.

| Channel | Best use case | Speed | Proof quality | Cost / effort | Escalate when |

|---|---|---|---|---|---|

| IRS online tools (including international live chat where available) | Quick clarification and self-service checks; live chat for amended return questions or transcript requests | Often fastest for simple requests | Medium if you save screenshots or transcripts | Low | You need correction, formal submission, or issue resolution that does not complete online |

| International phone | Specific individual or business account questions through the International Taxpayer Service Call Center | Varies by queue and issue type | Low unless you keep strong call notes or reference details | Low to medium | The issue is too complex for telephone assistance or is not resolved by phone |

| Tracked mail or fax | Written responses and submissions, including international tax account issues that fit fax scope | Usually slower to start, with a clearer written trail | Medium to high if you keep full copies plus delivery or fax confirmation | Medium | Deadline risk increases, records mismatch continues, or the issue falls outside the fax scope |

| Tax professional with Form 2848 | Higher-risk matters where representation, procedure, and correspondence control matter | Setup takes time before handoff is complete | High when authorization and records are complete | High | You need someone authorized to act and speak to the IRS for you |

IRS online account and live chat#

Start here if your goal is a quick check or a straightforward question that may be resolved without a call. For people outside the U.S., IRS lists live chat for amended return questions or transcript requests, with published availability Monday-Friday, 6 a.m. to 11 p.m. Eastern.

Switch channels if the issue requires a correction, a formal response packet, or judgment on disputed facts. Save screenshots or chat records before you move on so your file stays complete.

Phone#

Use the International Taxpayer Service Call Center for narrow, specific account questions. The published line is 267-941-1000 (not toll-free), and published hours are Monday-Friday, 6 a.m. to 11 p.m. Eastern. Have your name and SSN ready so the assistor can work the issue.

Do not rely on phone calls alone when your case turns on written evidence or complex factual resolution. IRS states some questions are too complex for telephone assistance, so move to a written channel when phone help cannot resolve your issue.

Tracked mail or fax#

Written channels are the right move when your objective is to respond, submit documents, or preserve delivery evidence. IRS lists fax 681-247-3101 for international tax account issues only, so confirm your case fits that scope before you send anything.

Send a complete packet, not partial pages. Include the IRS notice, identifying details, your objective, and the full supporting set. If a notice provides its own response address, follow that notice.

Tax professional with Form 2848#

Hand off when the downside is meaningful and you need controlled representation, not another round of self-navigation.

Use Form 2848, Power of Attorney and Declaration of Representative for that handoff path. This is the escalation lane when procedure and record control matter as much as the underlying tax facts.

You might also find this useful: How to Get a PTIN from the IRS as a Tax Preparer.

Step 3: Verify Every Interaction to Create a Bulletproof Record#

You are not finished with an IRS interaction until you can prove what happened, what you sent, and what the next step is. For each interaction, keep one clear evidence artifact, store it the same day, and set a follow-up date if confirmation does not appear.

If a contact seems unexpected, start with authenticity checks. IRS says it typically makes first contact by mail delivered by the U.S. Postal Service, so treat surprise calls, texts, or emails as a cue to verify against a mailed notice before you act.

Phone#

Use the International Taxpayer Service Call Center for overseas account questions: 267-941-1000 (not toll-free), Monday-Friday, 6 a.m. to 11 p.m. Eastern. After each call, save a short call log with date, time, number dialed, tax year or notice discussed, what you asked, and what you were told to do next.

Phone is fast, but your proof is only as strong as your notes. If the outcome is "respond in writing," link that call log to the written submission in your archive.

Mail#

Use mail when you need a documented paper trail. Keep a complete copy of the packet and never send original documents.

If timing matters, use an IRS-designated private delivery service and keep written proof of the mailing date. Then save the mailing receipt and delivered status with the exact packet copy.

Fax#

For international tax account issues only, IRS lists 681-247-3101. Your core proof is the fax transmission confirmation plus the exact PDF you sent.

Before sending, confirm packet quality and completeness, including notice pages, identifiers, and legible scans. For payment-credit issues, keep the transaction record that includes the confirmation number.

Online account and uploads#

For digital steps, capture proof before you close the page. IRS Online Account is available to taxpayers with international addresses and shows digital notices and up to 5 years of payment history.

If you use the IRS Document Upload Tool, save the receipt confirmation page. For payments, notices, and uploads, keep screenshots or PDFs that show the final confirmation state and any confirmation number.

| Channel | Evidence artifact | Where to store it | If confirmation is missing |

|---|---|---|---|

| Phone | Call log (date/time, issue, next action) | Tax-year folder, notice-specific subfolder | If written action was required, move to written follow-up tied to the notice |

| Packet copy, mailing receipt, tracking, delivered status | Same folder as response packet | Allow at least 30 days for IRS reply, then follow up | |

| Fax | Sent PDF and transmission confirmation | Same folder as notice response | Confirm scope or completeness, then resend if needed |

| Online/upload | Confirmation screenshot or PDF and confirmation number | Tax-year folder under notices or payments | Reconcile in Online Account and add a dated follow-up note |

Use a simple archive protocol so records stay usable:

- Use one naming pattern (example:

2024_CP____ Response_Faxed_2026-04-18.pdf) - Store files by tax year, then by notice, payment, filing, or correspondence

- Run a quick post-contact reconciliation: tax year, notice, amount, and next deadline

Do not treat any single artifact as complete proof by itself. Your strongest file is the artifact plus the exact related documents and the documented next action. For retention, use the applicable period of limitations framework rather than one universal timeline. 3 years is a baseline in some cases, not every case.

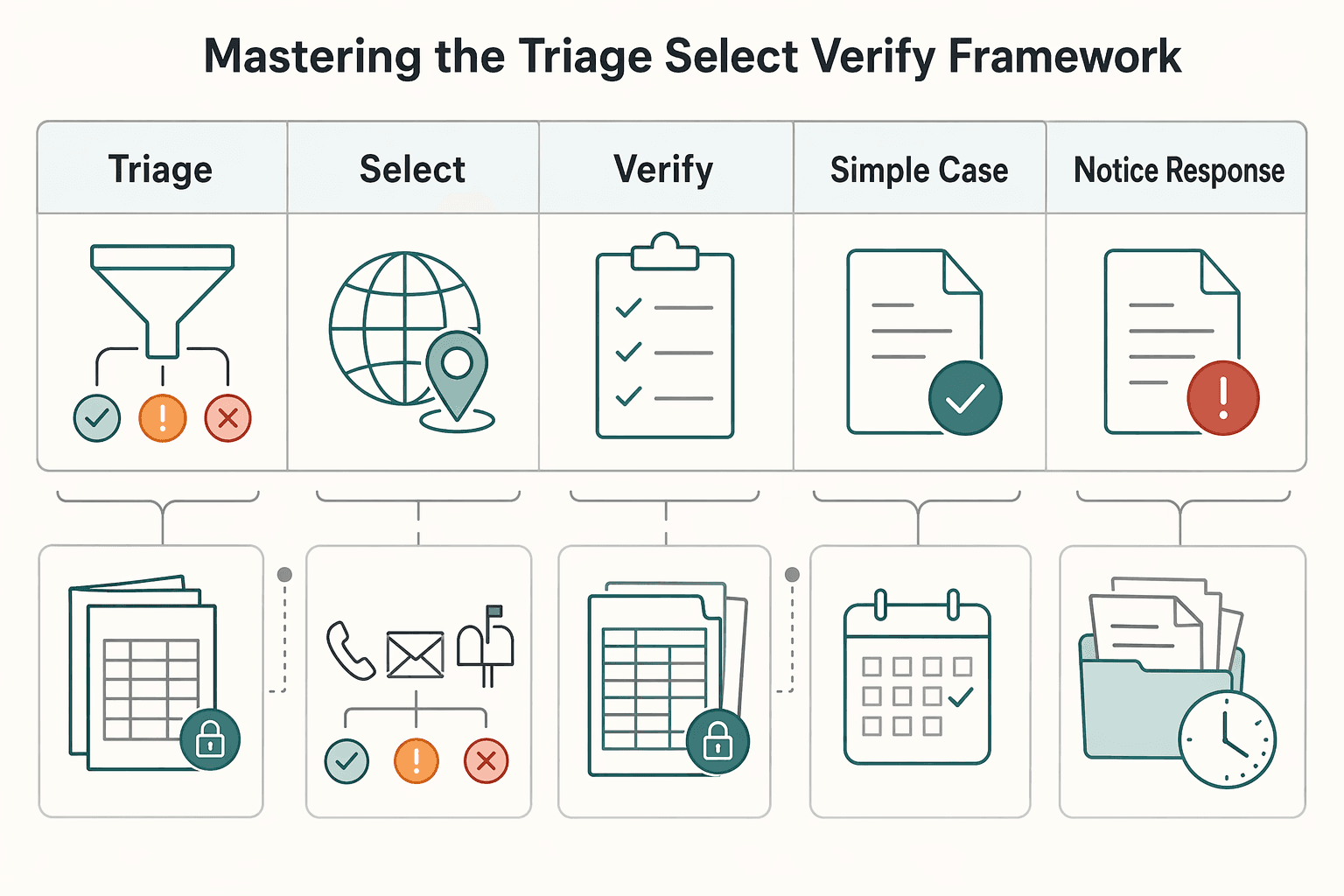

From Anxiety to Agency: Mastering the Triage, Select, Verify Framework#

Use Triage -> Select -> Verify to match the issue to the proof you need before you reach the IRS from abroad. You stay in control when your channel choice and your records are strong enough to survive delays, incomplete responses, or handoffs.

| Step | Focus | Save now |

|---|---|---|

| Triage | Write your objective in one sentence before contact | Save the notice and your one-sentence objective |

| Select | Use the lightest channel that still fits the stakes | Save the IRS page or instructions you used |

| Verify | Treat each interaction as incomplete until your file can prove what happened | Archive the call log, delivery proof, or transmission report in one folder |

Publication 2104's FY 2025 problems are a practical warning: taxpayers abroad face severe compliance burdens, telephone service quality is a known concern, and records requests can face delays or inadequate responses. Plan for follow-up, not one-and-done contact.

Use this as a working template, not an official IRS channel matrix:

| Issue profile | Working risk label | Possible starting channel (after you verify current IRS options) | Example records to keep |

|---|---|---|---|

| Simple account or status question with no filing position at stake | Low | Published phone option (or chat, where available) | Notice copy, tax year, and a call/chat log |

| Notice response, paper submission, or request where proof of receipt matters | Medium | Published mail or fax instructions | Full packet copy plus delivery/transmission evidence |

| Audit, appeal, penalty dispute, or matter affecting representation rights | High | Decision point: self-manage or hand off to a professional with authority in place | Complete case file: notices, submissions, timeline, authority record, follow-up log |

That framework carries through the whole process:

- Triage: Write your objective in one sentence before contact. IRM 4.46.1 uses "Issue-Driven Risk Analysis" and "Improving Issue Concerns," which is a useful framing cue. Decide whether you are solving an information gap, a proof problem, or a representation problem.

- Select: Use the lightest channel that still fits the stakes. If paper processing, online-account access, or notice-response confusion is part of your case, choose the route that gives you a durable trail.

- Verify: Treat each interaction as incomplete until your file can prove what happened. Save the IRS page you relied on and note procedure-currency checkpoints you can verify. For example, IRM 4.46.1 shows a manual transmittal date of August 14, 2025.

What you do now: for Triage, save the notice and your one-sentence objective; for Select, save the IRS page or instructions you used; for Verify, archive the call log, delivery proof, or transmission report in one folder. If the issue is high-stakes, repetitive, or stuck because representation is unclear, stop self-managing and hand off with authority in place. If you're at that point, start with The Best Accounting and Tax Advisors for US Expats.

Related: How to Pay the IRS from Abroad Without Misapplied Payments.

If you want a more audit-ready way to manage cross-border money records going forward, review the Gruv docs.

Frequently Asked Questions

How do you access IRS tools from abroad if online account setup stalls?

Check the current options on the IRS international contact page before you retry. If setup still stalls, use live chat in English for amended return or transcript requests, or call the International Taxpayer Service Call Center at 267-941-1000. If your issue is not covered in chat or phone support, escalate to another listed channel.

How do you confirm the IRS received your mail from overseas?

Confirm the current IRS international mailing address that matches your taxpayer type before you send anything. IRS lists International Accounts in Philadelphia for individuals outside the U.S. and Ogden for businesses outside the U.S. Keep your full packet copy and mailing proof together, and escalate if delivery cannot be confirmed or no response arrives by your follow-up date.

When should you call the international IRS line?

Call the international line for international account questions after checking current hours and converting them to your local time. The published window is Monday-Friday, 6 a.m. to 11 p.m. Eastern at 267-941-1000. If the issue is too complex to resolve by phone or repeated calls do not produce a clear next step, switch channels and escalate.

What should you have in front of you before calling?

Have your name and Social Security number ready, along with the IRS notice and tax-year details. Keep a short call log with the date, topic, and next action while you speak. If the assistor says the question is too complex for phone handling, move to a written channel.

Can you email the IRS about a tax account issue?

Do not use email for sensitive tax data. IRS says it will never initiate contact by email. Use published channels such as phone, mail, fax for international tax account issues, or live chat where offered, and verify any urgent payment or data request before acting.

When should you involve a tax professional?

Consider a tax professional early when the issue is high-stakes for money, filings, or positions you may need to defend. It is also a practical escalation point when the issue is too complex for standard phone support or you keep repeating the same facts without a clear resolution path. Use IRS international FAQs as general guidance only, not legal authority, when deciding what to do next.

When does Power of Attorney matter?

Power of Attorney matters when you want a representative to communicate with or represent you before the IRS. Use Form 2848 for representation, but confirm current authorization rules directly with the IRS because the contact materials here do not lay out the full requirements. Escalate if communication stalls and representative permissions are unclear.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Best Accounting and Tax Advisors for U.S. Expats: Pick the Right Support Level

**Pick the support level that matches your compliance surface area, then evaluate providers on written scope and form coverage.** The common failure mode for most U.S. expats is not "forgetting to file." It is hiring the wrong help model, under-scoping what you actually need, and finding the gap when IRS filings and related reporting obligations hit the critical path. You run a business-of-one, and your tax workflow is part of the system.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.