Quick Answer

Start with a two-step screen: use Shizune’s Top 50 page (Last updated: Jan 2026) to find names, then require a second source before outreach. Move any fund to `priority now` only after you log stage fit, SaaS thesis fit, partner relevance, and decision speed in your tracker. Treat older or broad pages like Growfusely’s Aug 23, 2022 list as discovery only. This keeps your India SaaS target set practical and reduces brand-led outreach that does not convert.

Start here and use this list the right way#

If you are looking for SaaS-focused investors in India, the fastest way to waste time is to build a long list of names and call it a strategy. Start with a shortlist you can defend: each firm should have a reason to be there and one open check you still need to complete before outreach.

- Use ranked lists for discovery, not for final judgment.

Shizune is useful because it tells you exactly what it is doing. Its India SaaS page is a Top 50 list, marked Last updated: Jan 2026, and it says it ranks investors by the number of SaaS investments they made in India. That makes it a strong first-pass source when you need to move fast. The catch matters. A high rank tells you a firm has been active, not that it fits your stage, your category, or the partner you need. If you treat rank as proof of fit, you will spend time on impressive names that are simply wrong for your round.

- Cross-check any SaaS list with at least one broader market source.

A broader India VC article helps you catch firms, name changes, and context that a SaaS-only page can miss. For example, the WeWork article published on April 29, 2025 is a Top 20 venture capital list, but it is clearly cross-sector, covering startups in tech, healthcare, fintech, and more. That makes it useful for widening the search, not for ranking SaaS fit. It is also a good place to verify labels and identity shifts, such as Sequoia Capital India now shown as Peak XV Partners. Use a simple rule: if a firm looks strong in one source but vague everywhere else, move it to verify before outreach, not priority now.

- Turn noisy sources into a working shortlist with evidence attached.

Public investor lists are inputs, not answers. In your tracker, include at least the exact firm name, source URL, date checked, why it might fit, and what still needs verification before first contact. That last field is where founders usually save the most time. It forces you to catch common failure modes early: duplicate firms under slightly different names, stale list entries, and broad funds that look startup-friendly but do not actually match your SaaS story.

This guide helps you move from public-list noise to a shortlist that holds up in diligence, partner scrutiny, and your own second look.

Who this list is for and how to judge fit#

Use this list if you're building Indian SaaS with real operating discipline and want investor fit, not just familiar logos. Judge each name by round fit, category fit, and decision pace before you spend outreach time.

Treat public lists as discovery inputs, not final truth on check size, partner availability, or current deployment speed. Shizune is useful because it ranks investors by number of SaaS investments in Indian companies and shows a Jan 2026 update; that is a volume signal, not a fit signal. Growfusely is useful for widening the pool, but it is a 55-firm list published on Aug 23, 2022, so every candidate still needs a fresh validation pass.

Score each firm before you email#

| Criterion | What to check | Caution |

|---|---|---|

| Stage fit | Confirm the firm is plausible for your current round | If you cannot confirm, keep it out of priority outreach |

| SaaS thesis fit | Check for thesis match; volume is not the same as thesis match | If your story is mostly cheaper than a global giant, treat that as a weak fit signal |

| Geography fit in India | Check that the firm actively backs companies in your operating market | Not just broadly adjacent profiles |

| Partner relevance | Map the likely partner who would engage first | A firm name alone is not enough |

| Decision speed | Look for timeline clarity | If timeline clarity is missing, mark it as verify before outreach and move on |

- Stage fit

Confirm the firm is plausible for your current round. If you cannot confirm that, keep it out of priority outreach.

- SaaS thesis fit

Volume is not the same as thesis match. If your story is mostly "cheaper than a global giant," treat that as a weak fit signal for serious investors.

- Geography fit in India

Check that the firm actively backs companies in your operating market, not just broadly adjacent profiles.

- Partner relevance

Map the likely partner who would engage first. The firm name alone is not enough.

- Decision speed

If timeline clarity is missing, mark it verify before outreach and move on.

Use one hard rule: if a firm looks strong on volume but weak on thesis, rank it below a lower-volume, higher-fit option such as Blume Ventures or India Quotient. Related: A Freelancer's Guide to Angel Investing and Venture Capital.

Build your shortlist in one afternoon#

A strong shortlist comes from source order and a strict filter, not a long copy-paste list.

- Start with activity signals, then widen carefully

Open Shizune first for an activity-ranked pass; it says the list is updated monthly (snapshot: Jan 2026). Then use OpenVC to widen coverage. It is a B2B/enterprise/business-software discovery list, not a SaaS-only ranking, shows a March 22, 2026 update, and offers a downloadable dataset. If you use sources like Growfusely or Y Combinator pages, treat them as discovery inputs only and verify fit before outreach.

- Normalize names before scoring

Set up a tracker with canonical name, alias, source, and status before you evaluate fit. Keep one firm record per investor so duplicate naming does not inflate confidence.

- Use a two-pass filter

Pass one: remove obvious mismatches on stage, category, or India relevance. Pass two: check partner and portfolio relevance; if you cannot map a clear path to the right decision-maker, move that firm out of priority now.

- Bucket and contact in waves

Keep only three buckets: priority now, priority later, and watchlist. Contact the first bucket in waves, then tighten your list based on response quality and meeting conversion before you expand.

We covered this in detail in Best Accounting Firms for Startups if You Run on Client Cashflow.

Compare investor sources before you trust them#

Before first outreach, use a simple rule: do not shortlist a fund from one source alone. Require two-source confirmation, and make sure at least one source shows clear selection logic.

| Source | What it is good for | What it misses | Verification step |

|---|---|---|---|

| Shizune | Ranked SaaS activity view for India (Top 50, Last updated: Jan 2026) | Activity count is not investor fit by itself | Confirm the same fund in a second source before moving it to priority now |

Editorial roundup such as GrowthJockey (Top 30, updated 13 February 2026) | Broader market context and name discovery | The excerpt is narrative, not a transparent scoring method | Treat as discovery/context until another source confirms relevance |

Quick list such as Papermark (Top 15 in 2026) | Fast scan for missed names | Very light visible methodology | Use to widen the net, not to justify outreach on its own |

| Access-gated directory such as VC Sheet | Potentially useful later | Data is not usable while the page is stuck on browser verification | Do not count it as evidence until fund data is visible |

Shizune is the strongest first pass here because its method is explicit: it ranks by number of SaaS investments in India and states monthly updates. Use that for initial prioritization, but do not confuse rank with fit to your stage, thesis, or partner match.

Editorial and quick-list sources help with discovery and context, not proof. For example, GrowthJockey adds broad market framing, while Papermark helps with quick name capture, but neither should be your only reason to contact a fund.

Keep the workflow tight: one source finds the name, a second source confirms it, and your tracker records why it belongs on your list. If any of those are missing, hold the fund in watchlist and verify before outreach. For a step-by-step walkthrough, see The Best CRMs for a B2B SaaS Sales Team.

Best VC firms for SaaS startups in India by founder situation#

Sort your list by your current fundraising need, then qualify each name before outreach.

| Lane | Examples | When to use | Note |

|---|---|---|---|

| High-activity early pipeline | Inflection Point Ventures; Titan Capital; Blume Ventures | You need broad early conversations and a visible activity signal | Shizune Jan 2026 shows 111 India SaaS investments for Inflection Point Ventures, 102 for Titan Capital, and 99 for Blume Ventures |

| Operator-network and angel-to-VC bridge | Indian Angel Network; IAN Group; Mumbai Angels; 100X.VC | You are converting early traction into a more structured process | Shizune also maintains a separate India SaaS list of 50 angel investors and VC funds |

| Thesis-first institutional path | Accel; Peak XV Partners; 3one4 Capital; India Quotient | Your category story is already sharp and specific | In the sources reviewed for this section, the strongest count-based support is for the high-activity lane above, not this bucket |

| Platform-led discovery route | LetsVenture and LVX Ventures; Artha Venture Fund and Artha Group | You need faster top-of-funnel discovery | OpenVC's India page was last updated March 22, 2026 and is broad across investor types, stages, and sectors |

- High-activity early pipeline: Inflection Point Ventures, Titan Capital, Blume Ventures

Start here if you need a broad early pipeline and a visible activity signal. In Shizune's Top 50 SaaS VC Funds in India (last updated Jan 2026), Inflection Point Ventures shows 111 India SaaS investments, Titan Capital 102, and Blume Ventures 99. Use that as discovery input, not proof of fit: move a fund to priority now only after second-source confirmation and one clear fit reason you can defend.

- Operator-network and angel-to-VC bridge: Indian Angel Network, IAN Group, Mumbai Angels, 100X.VC

Use this lane when you are turning early traction into a more structured process. The grounded signal here is directional: Shizune also maintains a separate India SaaS list of 50 angel investors and VC funds, so discovery is not strictly split between angel and VC paths. Treat these names as candidates, then qualify the actual contact and fit before you spend meeting cycles.

- Thesis-first institutional path: Accel, Peak XV Partners, 3one4 Capital, India Quotient

Use this lane when your category story is already sharp and specific. In the sources reviewed for this section, the strongest count-based support is for the high-activity lane above, not this bucket, so rely on tighter internal readiness checks before outreach. If your narrative is still broad, keep this as a secondary lane until your positioning is clearer.

- Platform-led discovery route: LetsVenture and LVX Ventures, Artha Venture Fund and Artha Group

Choose this route when you need faster top-of-funnel discovery. OpenVC's India page (last update March 22, 2026) is explicitly broad across investor types, stages, and sectors, which is useful for sourcing but not enough for final prioritization. Build quickly, deduplicate early, and keep names in watchlist until you confirm SaaS relevance with a second source.

You might also find this useful: The Best Cloud Hosting Providers for SaaS Startups.

Use ranked lists without getting misled#

Use ranked investor lists for discovery, not final targeting. Check the source type, date, and whether a second relevant source supports the same name before you reach out.

- Check what kind of list you are reading

Not every strong-looking list is a SaaS VC shortlist. Inc42's Family Office Tracker explicitly says 200+ investors, but it is framed around family-office participation. EY's India Fintech Report 2022 and the Zinnov-Chiratae India SaaSonomics report (JUNE 2023) are useful market context, not firm-level SaaS outreach rankings.

- Treat date as a hard screening step

Log the publication date next to every source before moving any firm to priority now. A Quora page about VC focus in 2017, especially with Anonymous attribution, should not carry the same weight as a current directory-style source.

- Cross-check by source type to reduce false confidence

A name appearing in one ranked list is not enough on its own. A stronger signal is overlap across two relevant source types, such as a ranked list plus a directory-style source like Venture Intelligence's Directory of Early Stage Investors in India.

Related reading: The Best Analytics Platforms for SaaS Businesses.

Red flags that waste founder time#

Most wasted founder time comes from avoidable outreach mistakes. Filter for fit and diligence readiness before you send a deck.

- No stage thesis

If you cannot explain why a firm fits your current round, stop and tighten your case first. A discovery list can help you find names and move faster, but it does not replace your stage argument, even when the list is current (for example, updated on March 22, 2026). Write one line per firm in your tracker: what stage story you are pitching and what proof supports it.

- Brand-first shortlisting

A logo-heavy list with names like Sequoia India, Accel, or Peak XV Partners can look strong, but brand alone is not a targeting strategy. If you cannot state a concrete reason this conversation is relevant now, move that firm from priority now to verify before outreach.

- Weak compliance and governance basics

Legal and regulatory violations, or weak understanding of your legal context, are clear red flags in investor evaluation. For an India-based company, go into outreach with a clean internal position on structure, approvals, and tax questions you may face, including Angel Tax-related exposure. If this area is still fuzzy, fix it before scaling outreach; A Guide to India's Angel Tax for Startups can help you prepare.

- One deck for everyone

Sending one generic deck to every fund on your list wastes time. Keep core facts consistent, then tailor your first touch by investor type across groups like Indian Angel Network, 100X.VC, and Blume Ventures so your ask and proof points match the audience. For a broader operating setup lens, see How to Set Up a US LLC for an Australian SaaS Founder.

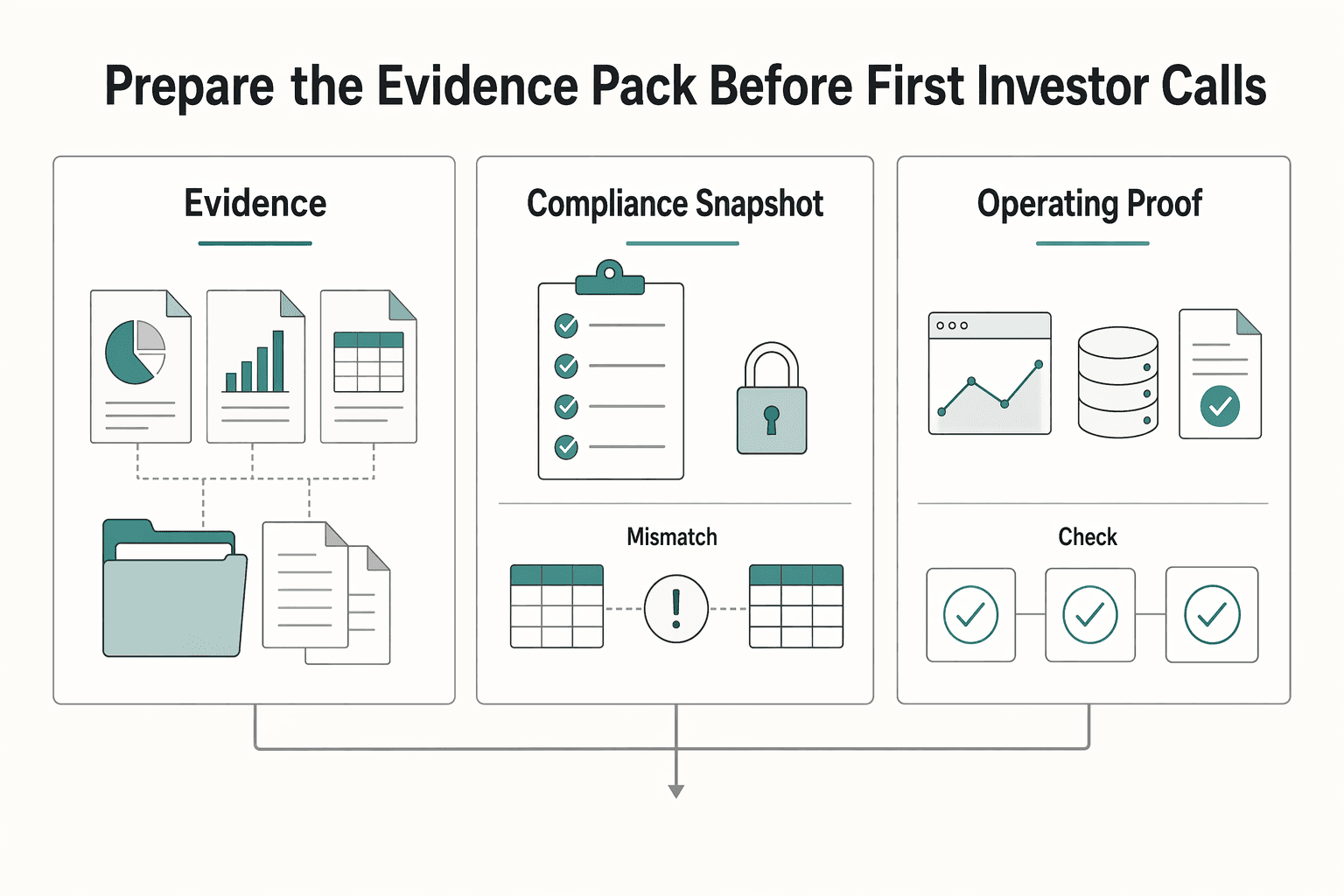

Prepare the evidence pack before first investor calls#

Before first calls, get your proof in order before adding more names. Use investor lists for discovery, not as a substitute for diligence: Shizune says its India SaaS page covers 50 funds, ranks by Indian SaaS investment count, and is updated monthly (shown as Jan 2026 on-page).

| Component | Keep ready | Check |

|---|---|---|

| Core evidence | One compact pack that your team can repeat consistently across deck, model, and supporting files | Pick three key numbers and confirm they match everywhere |

| Compliance snapshot | A one-page internal status note with each item marked ready, pending, or needs advisor input, plus owner and date | If Angel Tax is likely to come up, align the team on one concise explanation and the backing file |

| Operating proof | Records that show your reporting cadence and how issues are tracked to closure | Ask a teammate to recreate last period's key metrics from source exports without your help |

- Core evidence, one version

Keep one compact pack that your team can repeat consistently across deck, model, and supporting files. Run a quick pre-call check: pick three key numbers and confirm they match everywhere. If they do not, fix the mismatch before outreach.

- Compliance snapshot, with ownership

Keep a one-page internal status note with each item marked ready, pending, or needs advisor input, plus a clear owner and date. If Angel Tax is likely to come up, align the team on one concise explanation and the backing file; use A Guide to India's Angel Tax for Startups to prepare that discussion.

- Operating proof you can reproduce

Keep records that show your reporting cadence and how issues are tracked to closure. Stress-test them by asking a teammate to recreate last period's key metrics from source exports without your help. That matters even more when platforms advertise access to 250+ investors by industry and stage, because your story will be tested repeatedly as outreach expands; if you are scaling top-of-funnel, keep your process as tight as your targeting in Best Lead Generation Tools for B2B SaaS Operators.

Make your next move#

Your goal is a shortlist you can defend, not a longer spreadsheet: prioritize fit, then verification, then outreach.

- Build a shortlist you can defend

Start with discovery, then require a second check before any firm moves to priority now. Shizune can help you find names because it ranks investors by number of SaaS investments in India, updates monthly, and shows Last updated: Jan 2026 with 50 funds, but that activity count is not proof of partner fit or current interest in your specific segment. For each target, write one line explaining why it belongs beyond rank position. If you cannot state stage fit, India SaaS relevance, and your expected first-meeting outcome, move it to watchlist.

- Verify the signal before first outreach

Treat Y Combinator's India SaaS page as a signal source, not a full market map. It shows 31 startups and explicitly says it does not include all companies originally founded in India or by founders from there. For broader pattern checks, use YC's Startup Directory (over 5,000 companies). Add one concrete proof point per target, such as a relevant portfolio pattern, and one sentence on why your company belongs in that conversation.

- Run outreach in small waves, then iterate

Once your shortlist and evidence pack are ready, send a small first wave and review response quality before scaling. Focus on what replies reveal about fit: stage mismatch, metric questions, or proof gaps are signals to fix positioning before expanding the list. Keep your pack ready to forward: deck, cap table basics, customer or retention proof, and a short India compliance snapshot if early diligence is likely.

Frequently Asked Questions

How do I choose the best VC firm for a SaaS startup in India without relying on brand names?

Start with fit, not fame. Rank firms by stage fit, SaaS relevance, India coverage, and whether a specific partner seems credible for your category. A strong smaller fit beats a famous name you cannot map to your segment or round.

Which firms appear most active in Indian SaaS right now, and what does that activity actually prove?

Public ranking pages can highlight firms with visible deal activity, but that mostly proves recorded activity inside that source, not that the firm is right for your round. Deal volume tells you a fund has shown up in that dataset. It does not prove current thesis, partner attention, check size, or how fast the firm is moving this quarter.

Are ranked investor lists enough to build a final shortlist?

No. They are good for discovery, but a broad market list can create false confidence fast. Use ranked pages to find names, then require at least one more check before outreach: firm website, partner content, recent portfolio pattern, or a warm reference.

What should I verify before contacting firms from a public list?

Check four things: the list's publication date, whether the firm still signals interest in your stage, whether you can identify a relevant partner, and whether your evidence pack matches the story you plan to tell. One useful red flag is stale source data: Growfusely's India SaaS VC article shows a publication date of Aug 23, 2022, so treat it as a starting point, not a current shortlist. If you cannot name the partner you want and the reason they fit, you are probably not ready to send the first note.

What is the difference between a VC ranking page, an investor directory, and a startup directory?

A VC ranking page is mainly a discovery tool based on visible activity signals. An investor directory is broader and better for search, filters, and market coverage, but it still needs validation. A startup directory is more useful for spotting company and category patterns than for finalizing investor fit.

What key details are usually missing from public investor lists, and how should I fill those gaps?

The usual gaps are partner ownership, real stage behavior, present interest in India SaaS, and whether the firm is actively taking new meetings. Fill them with a short verification note for each target: source URL, date checked, named partner, one thesis clue, and one reason you belong on their radar. The common failure mode is sending broad outreach off a clean-looking list and discovering on reply that the firm was never a stage or thesis match.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 7 external sources outside the trusted-domain allowlist.

- gsb.stanford.edu/insights/masterclass-indias-venture-capital-...trusted

- bain.com/insights/india-venture-capital-report-2024external

- edzeb.com/blog/venture-capital-firms-in-indiaexternal

- eximiusvc.com/blogs/ai-saas-investors-india-what-they-real...external

- ey.com/content/dam/ey-unified-site/ey-com/en-in/ins...external

- failory.com/blog/venture-capital-firms-indiaexternal

- growfusely.com/blog/vc-firms-for-saas-indiaexternal

- growthjockey.com/blogs/top-vc-funds-of-indiaexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Health Insurance Comparison for Long-Stay Moves

Use focused time now to avoid expensive mistakes later. Start with a practical `digital nomad health insurance comparison`, then map your route in [Gruv's visa planner](/tools/visa-for-digital-nomads) so we anchor policy checks to your real plan before pricing pages pull you off course.

A Freelancer's Guide to Angel Investing and Venture Capital

**Build a decision system that protects your operating cash first, then treat angel investing as an optional use of true surplus.** If you are considering angel investing as part of broader wealth building, you need controls that keep "startup investing" from quietly raiding rent, taxes, or payroll. Knowledge feels productive, but constraints keep you solvent. As the CEO of a business-of-one, your job is to protect the operating cash that keeps the machine running.

India Angel Tax for Startups After the Cutoff

The abolition of India's "angel tax" is a major reform for startup fundraising, but the old exposure has not disappeared. The change applies only from April 1, 2025, so earlier issuances can still affect deals tied to periods before that date.