Quick Answer

Yes - run a background check on a new client before signature, and do it in sequence: confirm entity and signer details, review public dispute signals, then escalate to a formal provider when downside is meaningful. If a third-party consumer report is part of the process, secure written authorization and follow FCRA-facing requirements. Use PACER for federal case context, treat OFAC name hits as items to resolve, and convert unresolved yellow flags into tighter payment cadence, milestone controls, or a pause.

Beyond 'Tools': A CEO's Protocol for Client Vetting#

A background check on a new client is not just a tool decision. It is a business decision. Before you start work, decide whether the engagement is likely to create payment friction, dispute risk, or compliance exposure while you still control the decision.

1. Treat vetting as cash-flow protection#

Start with revenue protection. The Federal Reserve's payments report (December 05, 2024) describes customer payments as the primary cash source for small businesses. It also says roughly four of every five small firms report payment-related challenges. That makes screening a pre-engagement business control, not paperwork after signing.

2. Verify identity, then corroborate details#

First confirm the business exists. Then make sure its details match the proposal, contract, and invoice instructions. Use official registry records, but do not treat one lookup as final proof. California's business search says its data is "not a complete or certified record," and Companies House states it does not check the accuracy of filed information. If the legal name, address, or filing status does not match what the client gave you, pause onboarding until you resolve the mismatch.

| Approach | Decision quality | Consistency | Defensibility |

|---|---|---|---|

| Tool-first checking | Driven by what one product happens to surface | Varies with urgency or deal size | Hard to explain why some clients got deep checks and others did not |

| Protocol-first vetting | Tied to payment exposure, scope, and risk | Same checkpoints for similar engagements | Easier to justify because each step has a defined business purpose |

3. Keep checks proportional and lawful#

Scale checks to risk, keep a clear reason for each step, and monitor higher-risk relationships over time. If your workflow uses a consumer report, FCRA legal-use limits apply because information in a consumer report can only be shared for purposes specified in the Act. If you use PACER for U.S. federal court records, plan for metered access: $0.10 per page, capped at $3.00 per document, with fees waived below $30 in a quarter.

Work in phases so you know what to verify first, what to escalate only when justified, and what to decide before you sign or onboard a new client. If you want a financial-stability angle, see How to Vet a New Client for Financial Stability.

Phase 1: The Zero-Cost Digital Due Diligence Audit#

Start with public-source checks and record what you find before paying for formal screening. That gives you a consistent first pass and helps you decide whether to proceed, pause, or escalate.

| Check | Action | What to look for |

|---|---|---|

| Review the professional profile for coherence | Compare the hiring contact's profile details against the proposal or email trail | The same name, role, employer context, and a clear connection between the person, company domain, and buying authority they claim |

| Verify the business entity details in authoritative records | Check available official or primary-source records for the stated jurisdiction | Legal name, jurisdiction, and status that align with the contract and billing party, plus a clear tie between the signatory and the entity that will pay you |

| Run a public-signal pattern scan | Do a plain-language web search on the company and key principals, then review other publicly available references that are relevant in your jurisdiction | Repeated patterns, especially recurring disputes, nonpayment complaints, or repeated conflict themes tied to the same people or entity |

| Check values and operating-style fit | Review the company's site and leadership's public-facing posts or interviews | Signals that their stated working style matches how you deliver, and early signs of likely friction around scope, collaboration, or payment behavior |

Keep simple records as you go: the URL, the date checked, what you searched, and screenshots for anything material. When you rely on a U.S. government page, confirm basic trust signals first (.gov and HTTPS).

1. Review the professional profile for coherence#

Start with the hiring contact. If the person, company, and claimed authority do not line up, the rest of the review gets shaky fast.

Action: Compare the hiring contact's profile details against the proposal or email trail. What to look for: the same name, role, employer context, and a clear connection between the person, company domain, and buying authority they claim.

2. Verify the business entity details in authoritative records#

This is a core legitimacy check. If the entity details do not align with the contract and billing party, pause and clarify before moving forward.

Action: Check available official or primary-source records for the stated jurisdiction. What to look for: legal name, jurisdiction, and status that align with the contract and billing party, plus a clear tie between the signatory and the entity that will pay you.

3. Run a public-signal pattern scan#

You are not looking for gossip or one bad review. You are looking for repeated patterns that could affect payment or delivery.

Action: Do a plain-language web search on the company and key principals, then review other publicly available references that are relevant in your jurisdiction. What to look for: repeated patterns, not one-off noise, especially recurring disputes, nonpayment complaints, or repeated conflict themes tied to the same people or entity.

4. Check values and operating-style fit#

Fit matters because many client problems start as a process mismatch, then turn into scope fights or payment friction. Review the company's site and leadership's public-facing posts or interviews.

Action: Review the company's site and leadership's public-facing posts or interviews. What to look for: signals that their stated working style matches how you deliver, and early signs of likely friction around scope, collaboration, or payment behavior.

| Signal found | Why it matters | Action |

|---|---|---|

| Identity, role, entity details, and public presence align | Core legitimacy signals are consistent | Proceed |

| Minor mismatch in names, signatory details, or entity data | May be fixable, but weakens contract and payment clarity | Pause for clarification |

| Missing or unclear entity tie to the hiring contact | Raises client-identity and enforceability risk | Escalate to formal screening |

| Repeated dispute or nonpayment patterns in public information | Elevates payment and delivery risk | Escalate to formal screening |

Use Phase 1 as your baseline filter. If material gaps remain after clarification, or the engagement carries meaningful downside for your business, move to Phase 2 before you sign. If relevant to your work, see Canada's Digital Nomad Stream: How to Live and Work in Canada.

Phase 2: Investing in a Formal Background Check#

Move to formal screening when the cost of being wrong is material to your business, not just when a project feels "big." Escalate when the client will access sensitive data, payment exposure is meaningful, delivery dependency is high, or a failed deal would be costly to unwind. If exposure is low, scope is tight, and payment protection is strong, Phase 1 may be enough.

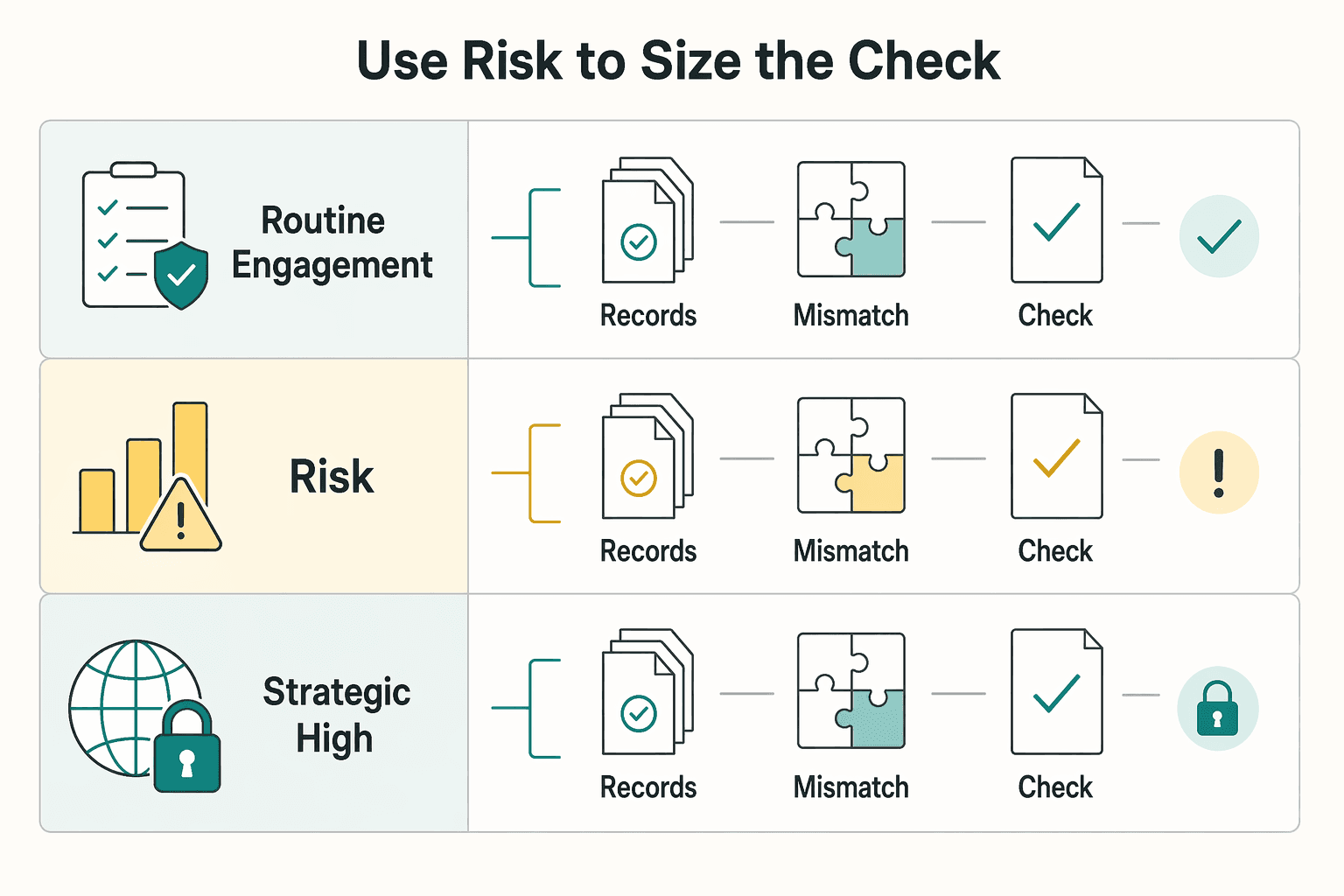

Use risk to size the check#

Use the likely downside to size the check. Ask one simple question: what happens if identity, payment capacity, or compliance posture has been misrepresented?

| Risk tier | When it fits | Appropriate check types | Decision focus |

|---|---|---|---|

| Routine engagement | Limited access, low dependency, minor unresolved questions after Phase 1 | Written authorization (stand-alone format where required), provider-based identity verification, entity and signatory confirmation, targeted litigation or bankruptcy check if payment risk is the concern | Confirm client identity and authority without over-collecting data |

| Elevated risk engagement | Meaningful unpaid exposure, internal system or data access, unresolved identity issues, higher delivery dependency | Routine checks plus broader federal litigation and bankruptcy review, stronger matching beyond name-only, and relevant public-record screening | Identify dispute patterns and financial-stress signals before contract commitment |

| Strategic or high-exposure engagement | Long-term relationship, regulated context, cross-border flow, customer-data or IP exposure, reputational sensitivity | Elevated checks plus sanctions screening, refreshed checks near signature, manual review of possible matches, and a documented escalation path for unresolved findings | Prioritize accuracy, documentation, and decision discipline |

PACER supports federal appellate, district, and bankruptcy docket searches, including nationwide party searches through the Case Locator. It is not a complete state or local court picture, and the nationwide locator updates at midnight each day.

Keep the compliance sequence clean#

If a third-party report could affect whether you accept the client, treat the process as potentially regulated screening, not casual research.

| Step | Article guidance |

|---|---|

| Get written authorization (stand-alone where required) | In employment contexts, FCRA requires a written stand-alone notice and written permission before getting a consumer report. In other contexts, use clear written instructions and confirm jurisdiction-specific requirements. |

| Use a screening provider that supports regulated use cases | When a report is used as an eligibility factor, confirm the provider can support required certifications, documents its dispute process, and follows procedures aimed at maximum possible accuracy. |

| Do not use consumer people-search tools for eligibility decisions | If a tool is marketed for casual lookup and restricts FCRA-governed uses, do not use it to accept or reject a client. |

- Get written authorization (stand-alone where required)

In employment contexts, FCRA requires a written stand-alone notice and written permission before getting a consumer report. In other contexts, use clear written instructions and confirm jurisdiction-specific requirements.

- Use a screening provider that supports regulated use cases

When a report is used as an eligibility factor, confirm the provider can support required certifications, documents its dispute process, and follows procedures aimed at maximum possible accuracy.

- Do not use consumer people-search tools for eligibility decisions

If a tool is marketed for casual lookup and restricts FCRA-governed uses, do not use it to accept or reject a client.

Choose a provider that works for solo operators#

For a solo operator, the right provider is one you can use consistently without guessing about process or documentation.

| Selection factor | What to verify | What "good" looks like |

|---|---|---|

| Compliance support | Permissible-purpose guidance, user certifications where applicable, clear regulated-use policy | You can follow a repeatable process without legal guesswork |

| Consent workflow | E-sign flow, stored timestamps, retrievable authorization records | You can prove what was authorized and when |

| Records coverage | Exact scope for federal litigation, bankruptcy, sanctions, and any add-on court coverage | Coverage is explicit, not vague "nationwide" language |

| Dispute process | How subjects challenge records and how disputed items are handled pre-decision | Clear correction and review path before final action |

| Pricing model | Per-search vs subscription terms, setup fees, hidden minimums | Verify the current price range before you commit |

Read the report for decisions, not trivia#

Start with the identity chain. If the contact identity, legal entity, signatory authority, and report identifiers do not align, pause immediately. Then look for patterns that matter to the engagement: repeated litigation, recurring collection conflict, and bankruptcy-related signals. One isolated item may be noise. Repeated themes are what should change your decision.

Treat sanctions results carefully. OFAC matching is approximate, so a potential hit is a lead to resolve, not a conclusion. Do not act on name-only similarity without additional identifiers.

From there, move to Phase 3. Proceed when findings are clean or documented and explainable. Proceed with protections for yellow flags. Pause signing when identity mismatch, unresolved sanctions exposure, meaningful litigation pattern, or financial-distress signals remain unresolved. If you want a deeper dive, read Value-Based Pricing: A Freelancer's Guide.

Phase 3: The Post-Check Playbook#

When the report arrives, make one consistent decision using the same criteria every time. Your provider gathers records; you still make the call.

Many providers return Clear or Consider. Treat those as inputs, not conclusions. Clear usually means no further review is needed, while Consider means something needs review before you decide.

1. Classify first, then act#

Start with basic consistency checks across client details and report identifiers. If key identifiers do not align, pause and resolve that first. A background check helps verify stated facts; it does not predict future behavior.

| Flag | Signal pattern | Business risk | Contract response | Escalation path |

|---|---|---|---|---|

| Green | Key identifiers align; result is Clear, or flagged items are minor and documented | Low immediate risk from misrepresentation or avoidable payment friction | Use your standard agreement and onboarding flow | Log decision and supporting records, then proceed to signature |

| Yellow | Consider result; issue is real but explainable with supporting documents | Moderate risk around payment timing, authority, scope control, or dispute handling | Proceed only with stronger commercial protections | Request written clarification, review documents, and record one final decision |

| Red | Key identifier mismatch remains unresolved, requested records are not provided, or findings materially change risk | High risk for payment, enforceability, or operational exposure | Pause signing or decline | Stop onboarding, preserve records, and follow any provider workflow notice step before ending the process |

Inconsistency is a common failure mode. If identical fact patterns get different outcomes, your process becomes hard to defend.

2. Convert yellow flags into contract controls#

A yellow flag is not automatically a no. It may mean your terms need to change. Use the report to verify the client entity, then use the contract to control the remaining risk.

| Control | Change to terms |

|---|---|

| Deposit structure | Increase upfront payment per policy |

| Payment cadence | Shorten billing intervals so exposure does not accumulate |

| Milestone gating | Release each next phase only after the prior payment clears |

| Termination protections | Define suspension rights, work-in-progress handling, and transfer conditions |

- Deposit structure

Increase upfront payment per policy.

- Payment cadence

Shorten billing intervals so exposure does not accumulate.

- Milestone gating

Release each next phase only after the prior payment clears.

- Termination protections

Define suspension rights, work-in-progress handling, and transfer conditions.

3. Decline with policy language#

For red outcomes, keep the response short and policy-based.

Standard decline: "Thank you for your time and for the opportunity. Based on our standard onboarding and due diligence process, we are not able to move forward with this engagement."

Fallback for ambiguous cases: "Thank you for the additional information. After review, we are not able to approve this engagement under our current client onboarding criteria."

4. Keep a minimal, defensible audit trail#

Keep a targeted file for each screened client, not a document dump. Record what you reviewed, what rule you applied, and what decision followed. Log these items each time:

- review date and decision date

- provider name and report date

- reported status (

Clear,Consider, or provider equivalent) - your final classification (

Green,Yellow,Red) - issue summary, if any

- supporting records relied on

- contract change, pause, or decline decision

- criteria or policy and contract version in force on that date

Store records in one access-controlled location tied to the client matter. Set a written retention approach that fits your business, and apply it consistently across engagements. We covered this in detail in The Ultimate Checklist for Onboarding a New Freelance Client.

Once you decide to proceed with safeguards, formalize scope, payment terms, and dispute handling in writing with this SOW generator.

From Anxiety to Advantage#

Vetting creates value only when it changes the next decision: proceed, proceed with safeguards, or decline. Start with the fastest high-impact checkpoint. Verify identity first so you know who you are dealing with before broader screening. Done digitally, this step can take about 90 seconds or less. If identity details do not line up, pause and resolve that before you commit time or delivery capacity. Then use a brief front-end call to confirm fit and practical next steps.

Use this triage so findings turn into action:

- Proceed

What you found: Identity checks are consistent, fit is clear, and no material issue is unresolved. What you do: Move forward on your standard terms. Risk effect: You reduce avoidable friction by validating the basics before kickoff.

- Proceed with safeguards

What you found: The client appears legitimate, but part of the review is incomplete, delayed, or mildly inconsistent. What you do: Keep the project, but add temporary safeguards and tighter checkpoints until the open item is resolved. Risk effect: You limit exposure while preserving the opportunity. If records need extra court research or verification sources are unresponsive, do not set timelines that assume instant clearance.

- Decline

What you found: Identity cannot be confirmed, fit remains unclear, or inconsistencies stay unresolved after follow-up. What you do: Walk away before work starts. Risk effect: You avoid preventable downstream risk, especially when checks can run concurrently but still be delayed independently across fragmented record systems.

Treat vetting as follow-up based on what you find, not a one-time pass-or-fail task. Document each outcome in onboarding: date checked, what you reviewed, open issues, decisions made, and any safeguards added or decline reason. That is what turns this into a repeatable operating advantage instead of a stress ritual.

For a step-by-step walkthrough, see How to Vet Contractors and Global Partners with a Tiered Background Check Process.

For related operational guidance, review Merchant of Record for freelancers.

Frequently Asked Questions

Do you always need the client’s permission?

Not always. Permission requirements vary by check type and jurisdiction. But if your provider is using a U.S. consumer-report workflow, get stand-alone disclosure and written authorization before ordering the report. If you are processing UK personal data, document your lawful basis before processing, and pause for legal review if your basis is unclear.

What should you verify first?

Verify the legal entity first, because a “clean” check does not help if the entity or signer is wrong. In practice, confirm against official registries, such as state registration databases, Companies House, or SEC filing search for public issuers. If the legal name, registration details, officers, or address do not line up, treat it as a yellow flag until resolved.

Is a sanctions search enough on its own?

No. OFAC’s search tool is useful, but OFAC states it is not a substitute for appropriate due diligence and does not provide one universal confidence threshold. If you get a potential hit, resolve identity details before proceeding. If you are a U.S. person and the match is confirmed to a listed person or entity, you generally should not transact.

How do you check litigation without overdoing it?

Use PACER to check U.S. federal cases, then focus on pattern, not noise. One isolated dispute may support stronger terms, while repeated vendor or payment disputes usually justify a decline. Keep the check lean by logging only the cases that changed your risk decision.

Can you use consumer people-search sites for a background check on a new client?

Use caution for decision-grade screening. Prefer providers that clearly define permitted use, required authorizations, and documentation expectations for your jurisdiction. If a vendor cannot explain data sources or required permissions, do not rely on it for onboarding decisions.

What should you budget, and is it deductible?

Do not lock one fixed number into policy. Verify the current price range before you set a budget, since provider scope, jurisdiction, and volume can change costs materially. For tax treatment, confirm the rule for your jurisdiction, then retain the invoice, provider terms, and your matter note for your accountant’s review.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- federalreserve.gov/frrs/regulations/joint-statement-on-the-risk...trusted

- flhealthsource.gov/background-screeningtrusted

- ftc.gov/business-guidance/resources/using-consumer-r...trusted

- ftc.gov/legal-library/browse/statutes/fair-credit-re...trusted

- hhs.gov/hipaa/for-professionals/compliance-enforceme...trusted

- hhs.gov/hipaa/for-professionals/special-topics/de-id...trusted

- irs.gov/forms-pubs/guide-to-business-expense-resourcestrusted

- irs.gov/newsroom/law-and-audit-the-due-diligence-pro...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

Canada Digital Nomad Visa Planning for Visitor Status and Work Permits

The phrase `canada digital nomad visa` is useful for search, but misleading if you treat it like a legal category. It is shorthand for existing Canadian status options, mainly visitor status and work permit rules, not a standalone visa stream with its own fixed process. That difference is not just technical. It changes how you should plan the trip, describe your purpose at entry, and organize your records before you leave.

How to Vet a New Client for Financial Stability

For independent professionals, the biggest financial risk is rarely a lack of opportunity. It is taking on a new client whose payment process is shaky, slow, or hard to verify. Time spent chasing late invoices or untangling a messy accounts payable process cuts directly into margin.