Quick Answer

Start with a stage-fit shortlist, then force proof in live demos before selecting a vendor. For this topic, the practical screen is ownership and evidence: who handles Form 3921 tasks, how 83(b) election records are tracked, and whether month-end exports are usable without spreadsheet repair. Use the article’s Native, Partner-supported, or Manual labeling for each critical row, and run the 30-day validation cycle before contract signature to catch hidden handoffs early.

How to Evaluate Global Equity Plan Tools#

This is not another skimpy roundup of the best global equity plan tools with a few logo blurbs and vague "great for startups" labels. The goal is simpler and more useful: help you choose a platform with fewer compliance surprises by focusing on the details that actually affect day-to-day administration, reporting, and rollout risk.

By the end, you should have three practical outputs you can use right away: a shortlist of vendors worth a real demo, a scorecard to compare them on the same criteria, and a 30-day rollout checklist you can pressure-test before signing. If you are the person who will own grants, vesting records, approvals, or close support, that matters more than a broad feature list.

A tool can look polished in a sales demo and still leave you chasing missing reports, unclear tax ownership, or manual fixes a month later.

The scope is intentionally tight. It focuses on platforms that show up in current comparison coverage, not on inventing a giant universe of options. That matters because vendor visibility is uneven, and comparison pages still leave important gaps.

Cake Equity's guide says it was updated for 2026, with a visible last update date of Feb 26, 2026. It also says it compares six leading platforms based on founder experiences and verified G2 data. Pulley's comparison guide is dated July 10, 2025. Those dates do not prove a tool is right for you, but they do show which names are being framed in the market right now.

You should expect some unknowns, and this guide flags them instead of smoothing them over. Current comparison pages mention criteria such as 409A valuation built in, ASC 718 or stock-based compensation reporting, and audit-ready reporting, but the operational depth is not always clear from the comparisons alone.

Pricing detail is often incomplete in these guides. "Global support" is often described broadly instead of as a clear statement of what is native, partner-supported, or still manual. Implementation depth can stay fuzzy unless you ask for migration detail, sample reports, and ownership boundaries.

That is where teams get burned. Pulley makes a fair warning here: one broken formula or outdated spreadsheet entry can stall a fundraising round. So this guide treats cap table integrity, reporting evidence, and admin clarity as decision points, not nice-to-have extras. If a vendor cannot clearly show how it handles compliance-related outputs and audit-ready records, it should not make your final shortlist, no matter how strong the demo feels.

Who This List Helps and Who Should Choose a Different Path#

Use this as a practical screening tool, not a final market verdict. The comparison material behind it is useful, but it does not support hard claims about vendor fit, enterprise readiness, or compliance depth by platform.

-

Best fit for this guide. You will get the most value if you are the person managing day-to-day equity-plan administration decisions and need a tighter shortlist and better evaluation questions.

-

When to choose a different path. If your process is driven by formal public-company governance, committee workflows, or deeply custom control design, use this article as a starting filter and run a broader, evidence-heavy evaluation before selecting a platform.

-

Non-negotiable evaluation baseline. Keep cap table integrity, audit-ready records, and compliance outputs at the center of your review, and require vendors to show concrete system output rather than giving high-level assurances. Where evidence is not shown, treat that as unresolved risk until you verify it.

The Scorecard to Choose a Global Equity Tool Without Guesswork#

Use a weighted five-lane scorecard with a separate red-flag column, and make vendors prove each claim before you score it. That is usually more reliable than comparing polished demos.

Five lanes that separate strong tools from risky ones#

Score each lane on a 1-5 scale, then weight it by your stage and risk profile.

| Lane | What good looks like | What to verify live |

|---|---|---|

| Compliance depth | Clear handling of Form 3921, 83(b) timing, and QSBS attestation scope | Ask who owns Form 3921 filing steps, how 83(b) timing and records are handled (30-day window), and whether QSBS attestation is included or an add-on |

| Global coverage realism | Country support described by jurisdiction, not generic "global" claims | Ask for your exact countries and what is native, partner-supported, or manual in each |

| Admin workload | Low manual cleanup for grants, changes, approvals, and close | Ask what your team still has to do outside the platform each month |

| Employee experience | Employees can understand grants, documents, and timelines without repeated back-and-forth | Ask to see the employee flow for accepting grants and retrieving signed records |

| Reporting quality | Audit-ready exports and usable month-end outputs | Ask for a sample month-end reporting pack and the audit trail view |

Compliance should usually carry more weight than teams expect. Form 3921 is an IRS information return tied to ISO exercises under section 422(b), so filing ownership needs to be explicit. For 83(b), timing is strict, so verify how transfer dates, reminders, and records are captured.

Treat QSBS attestation as scope and pricing to confirm, not a default feature. If it shows up in a demo, verify whether it is included in plan scope or sold as an add-on.

Red flags that should lower the score hard#

Some signals should sharply reduce a score or take a vendor out altogether:

- No clear owner for tax filings. If Form 3921 ownership is vague across platform, partner, and your team, mark it red.

- Weak audit trail language. You need a traceable record of actions, signatures, and changes, not generic "history available" wording.

- Global support without jurisdiction detail. Country-level tax, security, and reporting requirements vary, so broad claims alone are not enough.

If a vendor cites broad reach, for example "over 160 countries," ask for operating detail in your specific jurisdictions before giving credit.

Implementation evidence before you sign#

Before you choose a finalist, ask for three concrete artifacts:

- A migration plan with owners, milestones, and cutover assumptions

- A data-mapping process showing flow across HRIS, payroll, and plan administration data

- A sample month-end reporting pack (redacted is fine)

Use a simple decision rule: if you are pre-enterprise and distributed, prioritize operational clarity over feature breadth. If plan complexity is high, prioritize controls and reporting depth over setup speed.

Best Tools for Lean Remote Startups#

For lean remote teams, start with the shortlist that makes ownership explicit: who handles 409A valuation inputs, Form 3921 steps, ASC 718 outputs, and cross-border worker edge cases after you sign.

| Tool | Grounded detail | Verify |

|---|---|---|

| Carta | 409A valuations tied to the cap table; 16,000+ valuations per year across 50,000+ companies | How ISO exercise records flow into Form 3921, who owns filing steps, and what your team still handles manually |

| Pulley | Three-day 409A turnaround benchmark; exercise-date FMV data is needed to populate Form 3921 | The FMV field on exercise records and the actual Form 3921 workflow |

| Cake Equity | Built-in 409A valuation, ASC 718 reporting, QSBS attestation, and Form 3921; 20,000+ companies | Whether 83(b) election reminders, transfer-date records, and signed-document storage are handled in-product or outside it |

| Eqvista | Compliance services page lists ASC 718, Form 3921, 83(b) Election, and Rule 701 | Where product workflows end and service work begins so month-end expectations are realistic |

| Deel | States support for handling tax laws in 110+ countries; ISOs cannot be offered to contractors or employees hired through its EOR model | System boundaries early and the terms directing customers to their own tax, legal, or accounting advisors before submitting forms |

Carta is a practical first test if you want cap table and equity admin connected in one system. Carta positions 409A valuations as tied to the cap table, and reports 16,000+ valuations per year across 50,000+ companies. During your demo, confirm how ISO exercise records flow into Form 3921, who owns filing steps, and what your team still handles manually.

Pulley is a strong speed-oriented option for early-stage grant and fundraising workflows. Pulley publishes a three-day 409A turnaround benchmark and states that exercise-date FMV data is needed to populate Form 3921. Ask to see the FMV field on exercise records and the actual Form 3921 workflow, not just a feature overview.

Cake Equity is relevant when you want broad startup compliance coverage without adopting a heavier platform too early. Cake lists built-in 409A valuation, ASC 718 reporting, QSBS attestation, and Form 3921, and cites 20,000+ companies. The key check is scope: verify whether 83(b) election reminders, transfer-date records, and signed-document storage are handled in-product or outside it.

Eqvista is useful when you want compliance-service coverage stated directly. Its compliance services page lists ASC 718, Form 3921, 83(b) Election, and Rule 701. Before you decide, clarify where product workflows end and service work begins so month-end expectations stay realistic.

Deel is a fit when equity workflows need to sit alongside distributed hiring, payroll, and compliance. Deel positions equity in the same operating hub and states support for handling tax laws in 110+ countries. But validate boundaries early: Deel also states that ISOs cannot be offered to contractors or employees hired through its EOR model, and its terms direct customers to their own tax, legal, or accounting advisors before submitting forms.

After you have a shortlist, run one hard test: ask each vendor to map support by your actual jurisdictions and stakeholder mix, including direct employees, EOR employees, contractors, option holders, and leavers. That will tell you more than generic "global" positioning. Related: The Best Software for Cap Table Management.

Best Tools for Complex Cross-Border and Enterprise-Like Plans#

If you need tighter controls and audit-ready reporting across entities, choose enterprise-oriented tooling deliberately and expect a slower implementation.

Global Shares and J.P. Morgan Workplace Solutions are reasonable candidates to pressure-test when your plan is moving beyond startup-style equity admin. For both, anchor your evaluation to the core equity-management baseline from G2: cap table features, equity issuance and governance, and growth/exit scenario modeling.

For J.P. Morgan Workplace Solutions, Cake Equity's comparison, updated Feb 26, 2026, marks 409A valuation (built-in) as partial and ASC 718 / stock-based compensation reporting as full. Read that as a practical tradeoff: reporting depth may be stronger, but you should still confirm where valuation and tax-related steps are handled inside the platform versus in outside workflows.

For Morgan Stanley at Work, Charles Schwab EquiView, Fidelity, UBS, and Bank of America, the material here does not support feature-level claims, rankings, or fit conclusions. Screen them on operating model instead: implementation scope, managed-service boundaries, exception ownership, and recurring reporting outputs. Compintelligence explicitly treats Implementation & Managed Services as a core evaluation area, which is the right lens at this tier.

Decision rule: if you need high-control audit workflows and mature service layers, accept slower setup. If speed and lean execution matter more, avoid enterprise process overhead you will not use. If your team is already distributed, How to Manage a Global Equity Plan for a Remote Team goes deeper on the operating model.

Which Global Equity Tool Fits Your Stage Right Now#

Start with stage fit: pick for your current operating needs, then verify the controls before you commit.

| Stage | Starting point | Verify |

|---|---|---|

| Pre-Series and short on time | Start with startup-focused tools; Cake's guide, updated Feb 26, 2026, frames comparisons around seed to Series A | One record from issuance through scenario forecasting into an audit-ready report; if it still depends on spreadsheet cleanup, treat it as a real risk |

| Moving into multi-entity or public-company-style controls | Bring Global Shares and J.P. Morgan Workplace Solutions into evaluation earlier, even if you also compare lighter tools | Role permissions, exception handling, and a sample month-end reporting pack; if entity structure or approvals still sit outside the system, that is a red flag |

| Main pain is payout and reconciliation across regions | Set system boundaries upfront; no single platform replaces legal, tax, and finance infrastructure across jurisdictions. | Where equity tooling ends, where finance systems take over, and where the audit trail lives for payouts, reconciliations, and exceptions |

-

Pre-Series and short on time. Start with startup-focused tools and validate compliance depth before signing. Cake's guide, updated Feb 26, 2026, frames comparisons around seed to Series A, which fits teams that need grants and cap table administration live quickly. Ask each vendor to walk you through one record from issuance through scenario forecasting into an audit-ready report. If that flow still depends on spreadsheet cleanup, treat it as a real risk to fundraising, hiring, and diligence confidence.

-

Moving into multi-entity or public-company-style controls. Bring Global Shares and J.P. Morgan Workplace Solutions into evaluation earlier, even if you also compare lighter tools. At this stage, the key question is whether the platform can serve as your centralized equity system with usable approvals, governance, and reporting. Ask for role permissions, exception handling, and a sample month-end reporting pack. If entity structure or approvals still sit outside the system, that is a red flag.

-

Main pain is payout and reconciliation across regions. Set system boundaries upfront. Equity software can centralize issuance and records, but this pack does not support treating one platform as a full replacement for legal, tax, and finance infrastructure across jurisdictions. Document where equity tooling ends, where finance systems take over, and where the audit trail lives for payouts, reconciliations, and exceptions. If a vendor says "all-in-one," treat it as a claim to verify.

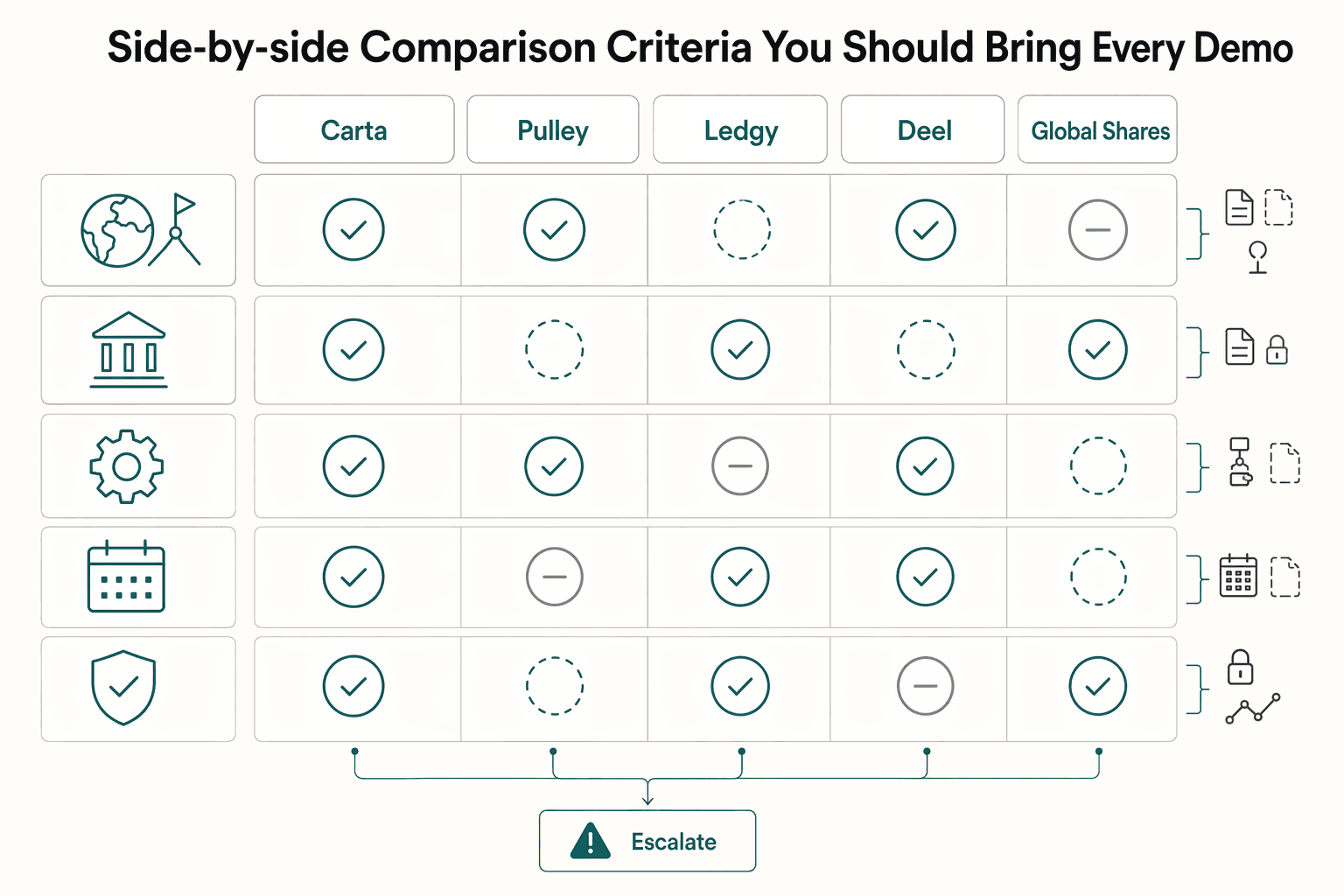

Side-by-Side Comparison Criteria You Should Bring Into Every Demo#

Take one matrix into every demo, and do not end the call with any row still vague. For each item, require the vendor to label delivery as Native, Partner-supported, or Manual so hidden handoffs do not become your team's process debt later.

| Vendor | Best for (to confirm in demo) | Core pros and cons (to confirm in demo) | Implementation burden (to confirm in demo) | Known unknowns to force clear |

|---|---|---|---|---|

| Carta | Your stage, entities, and plan design | What works out of the box vs what needs services | Data migration scope, owners, and timeline | Compliance ownership, export completeness, and exception path |

| Pulley | Your stage, entities, and plan design | What works out of the box vs what needs services | Data migration scope, owners, and timeline | Compliance ownership, export completeness, and exception path |

| Ledgy | Your stage, entities, and plan design | What works out of the box vs what needs services | Data migration scope, owners, and timeline | Compliance ownership, export completeness, and exception path |

| Deel | Your stage, entities, and plan design | What works out of the box vs what needs services | Data migration scope, owners, and timeline | Compliance ownership, export completeness, and exception path |

| Global Shares | Your stage, entities, and plan design | What works out of the box vs what needs services | Data migration scope, owners, and timeline | Compliance ownership, export completeness, and exception path |

| J.P. Morgan Workplace Solutions | Your stage, entities, and plan design | What works out of the box vs what needs services | Data migration scope, owners, and timeline | Compliance ownership, export completeness, and exception path |

Make them prove compliance and operations, row by row#

Do not accept a single "compliance" checkbox. Score each row separately, and require live evidence.

| Criteria row (required) | What to verify live | Carta | Pulley | Ledgy | Deel | Global Shares | J.P. Morgan Workplace Solutions |

|---|---|---|---|---|---|---|---|

| 409A valuation | Who owns it, where records live, what is exportable | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual |

| ASC 718 | Workflow ownership, outputs, and handoffs | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual |

| Form 3921 | For ISO exercises, who handles filing workflow, deadlines, fees, and non-compliance risk signals, plus evidence exports | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual |

| 83(b) election | What the platform supports directly vs outside process | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual |

| QSBS attestation | What is handled in-product vs external support | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual |

| Audit-ready exports | Exact report set, record-level traceability, and export format | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual |

| Migration support quality | Who maps history, validates imports, and resolves errors | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual |

| Role permissions | What each role can see, approve, and export | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual |

| Exception handling | How canceled grants, corrections, and status changes are tracked | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual |

| Month-end reconciliation workflow | What is produced in platform vs reconciled elsewhere | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual | Native / Partner / Manual |

End each demo with one final check: every row is marked Native, Partner-supported, or Manual, with a clear owner and proof.

A 30-Day Implementation Checklist to Avoid Compliance Surprises#

Use this 30-day sprint to test every demo promise against your real records before go-live. The goal is simple: confirm ownership, outputs, and controls early so compliance work does not fall back into manual cleanup at month-end.

| Week | Focus | Confirm |

|---|---|---|

| Week 1 | Lock scope and owners | Jurisdiction list, in-scope entities, ownership matrix, and required artifacts tied to 409A support, ASC 718 reporting, grant and exercise records, and Form 3921-related data trails |

| Week 2 | Run one full lifecycle in sandbox | The actual exports, timestamps, approvals, and exact output needed for compliance rows instead of summary claims |

| Week 3 | Validate migration against source records | Historical grants, employee records, document storage, exception cases such as canceled grants, status changes, and backdated corrections, plus intact document links and signed records |

| Week 4 | Run a real go-live readiness review | Failure-mode handling, support escalation paths, the documented month-end close routine, what is completed in-platform versus outside it, and a regular audit cadence |

- Week 1: lock scope and owners.

Finalize your jurisdiction list, in-scope entities, and an ownership matrix across legal, tax, finance, and equity administration. Map regulatory requirements across jurisdictions, and define required artifacts before contract signature, including records tied to 409A support, ASC 718 reporting, grant and exercise records, and Form 3921-related data trails.

- Week 2: run one full lifecycle in sandbox.

Test one grant from creation through vesting and reporting, then verify the actual exports, timestamps, and approvals your team will use. For compliance rows, validate the exact output you need instead of accepting summary claims. In one 2026 comparison, built-in 409A was shown as full for Cake, Carta, and Pulley, unavailable for Ledgy, and partial for Shareworks and J.P. Morgan, while ASC 718 was shown as full for Cake, Carta, Pulley, Shareworks, and J.P. Morgan, and partial for Ledgy.

- Week 3: validate migration against source records.

Reconcile historical grants, employee records, and document storage against your current source system before approval. Include exception cases such as canceled grants, status changes, and backdated corrections, and confirm that document links and signed records remain intact.

- Week 4: run a real go-live readiness review.

Confirm failure-mode handling, support escalation paths, and your documented month-end close routine, including what is completed in-platform versus outside it. Before launch, centralize controls, automate monitoring where supported, and set a regular audit cadence so ongoing compliance does not depend on undocumented handoffs.

Conclusion#

The best choice is usually not the platform with the longest feature sheet. It is the one that fits your stage now, holds up under cross-border scrutiny, and avoids pushing key compliance work back onto your team.

- Choose fit, not feature volume.

If you remember one thing from this guide, make it this: the right tool meets you where you are today and can still support the next stage without forcing a rebuild. A lean, distributed company should usually bias toward operational clarity and fast adoption. A multi-entity program with heavier governance pressure should bias toward controls, reporting depth, and service support, even if setup takes longer.

This is where stage fit matters more than brand gravity. Whatever your final comparison pair is, use the same rule: can this tool support your current award process, your near-term expansion, and the reporting burden you actually have, not the one the sales deck assumes?

- Use the scorecard, but make vendors prove every important claim.

A scorecard is not just a neat way to organize notes. Equity plan decisions in the real world are often assessed with scorecard logic plus qualitative judgment, not a loose feature checklist. Your version should force evidence on the points that create real downstream work: approval trails, export quality, migration mapping, month-end reporting outputs, and ownership of country-specific tasks.

The verification step that matters most is simple: ask for the exact artifact you will rely on later. That means a sample approval record with timestamps, a reporting pack you could use in close, and a jurisdiction-by-jurisdiction breakdown of what is Native, Partner-supported, or Manual. If a vendor says it supports global administration but cannot show how that works across tax and securities, exchange control, labor, and data privacy obligations that can span over 45 countries, treat that as unresolved risk, not a minor gap.

- Shortlist two tools, then block the deal on unknowns.

A shortlist is the right next move because it turns broad research into a controlled comparison. A two-finalist comparison can be enough for some teams if you use the same checklist, the same test data, and the same evidence standard on both. If your procurement is more complex, expand the pool, but do not relax the validation.

The common failure mode is committing after a strong demo and discovering later that local handoffs, changing jurisdiction rules, or missing documents still sit outside the product. Requirements move across jurisdictions, so recheck assumptions before signature and again before go-live. If a vendor cannot answer a material question clearly, leave it open in the scorecard and treat it as a decision blocker until they do.

Frequently Asked Questions

What features are truly non-negotiable in the best global equity plan tools?

Start with the baseline: cap table capability, equity issuance and governance, and scenario modeling. After that, the must-have layer is compliance automation that reduces manual filing, tax-rule, and audit-trail work rather than just giving you a nicer dashboard. If a vendor cannot show the records and audit trail you would use for review or close, treat that as a red flag.

Which tools are usually better for startups versus larger global organizations?

Stage matters more than logo recognition. For seed to Series A teams, startup-oriented equity management tools can be easier to adopt when the immediate goal is getting grants, records, and basic compliance workflows out of spreadsheets. Larger organizations often need broader plan-type support and stronger administrative controls, so evaluate enterprise-oriented providers against your entity count, award mix, and reporting requirements.

What does "global support" actually include when vendors use that term?

It should mean real coverage across compliance domains, not just that employees can log in from different countries. A serious definition includes tax and securities, exchange control, labor, and data privacy issues, and one reference point in the market talks about coverage in over 45 countries. Ask the vendor to mark each jurisdiction and each obligation as native, partner-supported, or manual, because "international" without that breakdown is mostly marketing.

Can one platform handle everything, or should I expect multiple systems?

Expect some stack reality. A platform can centralize equity administration, but you should not assume it replaces legal, tax, payroll, and entity-management tools globally. If your process depends on payroll inputs, local counsel review, or country-specific filings, plan for handoffs and document who owns each one before go-live.

What details are most often missing from vendor comparison pages?

The biggest gaps often include award and plan-type support, whether key tasks are truly automated or still manual behind the scenes, and who owns each filing step. J.P. Morgan Workplace Solutions explicitly suggests asking whether the software can manage all your existing award and plan types, plus time-saving features like automated notifications and bulk import. Also watch for small print that features, pricing, and availability may vary by jurisdiction and can change, because that is exactly how "global support" gets overstated.

How can I evaluate a tool in 30 days without creating compliance risk?

Use the 30 days to reduce risk with evidence, not promises. Put one real award type through sandbox, confirm bulk import on a sample migration, and verify the actual outputs for approvals, timestamps, and reporting rather than relying on a demo flow. A tool can look strong in the UI but still leave unsupported plan types or manual country-specific work outside the main workflow.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- irs.gov/instructions/i3921trusted

- irs.gov/pub/irs-pdf/f15620.pdftrusted

- leg.colorado.gov/initiative_files/3308/downloadtrusted

- sec.gov/Archives/edgar/data/1589025/0001534424160008...trusted

- blog.compintelligence.com/the-best-equity-management-softwareexternal

- cakeequity.com/guides/best-equity-management-softwareexternal

- cakeequity.com/features/audit-logexternal

- deel.com/blog/equity-management-platforms-startupsexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

The Best Software for Cap Table Management

Choose your equity tool based on execution risk, not startup image. If ownership is still simple and changes are rare, a spreadsheet may be enough for a period. Once grants, approvals, permissions, or investor scenarios enter the picture, software becomes important because it formalizes ownership data, rights, and change history so the record is auditable.

How to Manage a Global Equity Plan for a Remote Team

You can build a **global equity plan remote team** strategy that helps you hire and retain strong people without pretending equity will solve cashflow problems. The goal is a plan you can actually run: one that treats equity compensation as upside, keeps near-term pay dependable, and avoids promises you cannot support across countries.