Quick Answer

No, most freelancers do not need enterprise suites as their best tax research software. Tools like Thomson Reuters Checkpoint and CCH are built for firm-level research depth, while a business-of-one usually needs tighter controls: day-count tracking for residency, aggregate foreign-account monitoring for FBAR exposure, and invoice record discipline. Use primary IRS and Treasury materials to verify rules, then involve a cross-border CPA when treaty interpretation or conflicting jurisdiction facts drive the decision.

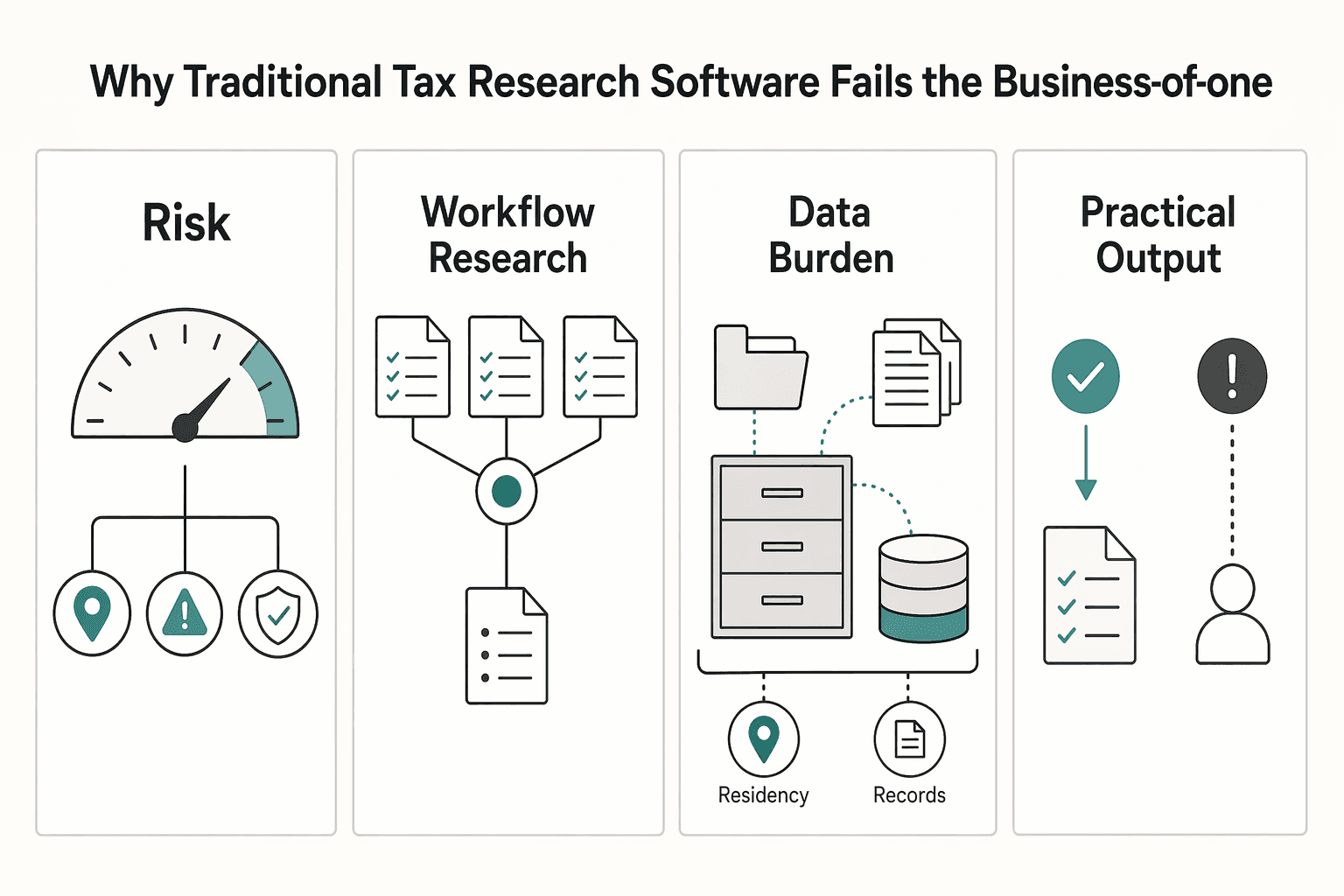

Why Traditional Tax Research Software Fails the "Business-of-One"#

If you run a solo practice, most products in the tax research category are built for a different job. Enterprise suites are often designed for firm-wide research depth and workflow needs. You need something narrower and more practical: a way to monitor your own compliance facts, plus a clear point where self-service stops and escalation starts.

- Cost mismatch

You are buying personal risk control, but these products are sold as firm infrastructure. CCH Axcess Tax is marketed as cloud software "suitable for firms of all sizes," and one independent 2026 buyer guide lists it at $9,999. That may make sense across a client portfolio. It is usually hard to justify when you only need to track your own residency exposure, foreign-account reporting risk, and invoice compliance.

- Audience mismatch

Checkpoint is positioned as a research and guidance solution for tax and accounting professionals, with integrated research, editorial, productivity, and marketing resources. Bloomberg frames its international tools around what a "global tax team" needs across more than 220 countries and jurisdictions. If you are managing one cross-border life, that is the wrong operating model. You need to know when your facts cross a filing line, not run a firm-style research process.

- Outcome mismatch

Your real questions are operational: Are you approaching the IRS substantial presence test, with 31 days in the current year and 183 days over the weighted 3-year lookback using the 1/3 and 1/6 components? If you are a U.S. person, did your foreign accounts exceed the $10,000 aggregate FBAR trigger, even if they produced no taxable income? Are your invoices compliant where you bill, including the EU rule that invoices are required for most B2B supplies? A research suite can help you read the rules, but you may still need to assemble your evidence pack: travel logs, peak account balances, and invoice and receipt records.

| Decision point | Enterprise suite | Business-of-one tooling |

|---|---|---|

| Buyer | Firm, tax team, or accounting practice | Solo operator managing personal risk |

| Workflow | Research, citation trail, preparation/compliance workflow | Monitor, verify, escalate |

| Data burden | Broad jurisdiction libraries plus client files | Your travel days, account balances, and invoices |

| Practical output | Defensible memo or researched position | Alert, checklist, and "talk to a CPA now" trigger |

Use this filter before you buy. If a tool does not help you verify travel dates, track aggregate foreign-account balances, and retain invoice support documents, it is probably the wrong fit. Once you stop shopping for an enterprise suite, the next step is simpler: identify the three compliance areas that deserve your attention first. If you want a deeper dive, read Value-Based Pricing: A Freelancer's Guide.

Tier 1: What You Should Actually Be Researching - Your 3 Core Compliance Risks#

For a solo cross-border setup, most of the real risk sits in three places: travel days, total foreign-account balances, and the cross-border invoices you issue. Track them weekly. Reconcile them monthly against source records. Escalate when you are near a rule or deadline you have verified, your facts conflict across jurisdictions, or a bank or client asks for corrections you cannot defend confidently.

| Risk | What to monitor | Failure mode | Safe default action |

|---|---|---|---|

| Residency | Country-by-country day counts, FEIE eligibility logic, and applicable local residency rules | One itinerary change breaks more than one test | Log each border crossing the same day and verify the current rule before travel |

| FBAR | One account register, aggregated balances, early-warning balance estimates | "Small" balances add up or FX movement changes your position | Review monthly and trigger alerts below your internal warning level |

| Invoicing | Client billing details on file, jurisdiction-specific invoice requirements, invoice wording/template | Rejected invoices, payment delays, correction churn | Pause sending until requirements and wording are verified |

Residency risk#

Residency usually deserves the most attention because you are managing several rule systems at once, not one. In practice, that means tracking FEIE eligibility for your U.S. return and verifying any local residency rules that apply where you spend meaningful time.

| Checkpoint | Detail | Note |

|---|---|---|

| Minimum days | 330 full days in foreign countries | Missing the 330-day minimum fails the physical presence test |

| Measurement window | 12 consecutive months | Days do not have to be consecutive |

| Full-day rule | 24 consecutive hours from midnight to midnight | Use passport and calendar evidence instead of memory |

| Tax-home link | FEIE eligibility is tied to having a foreign tax home | You still file a U.S. return reporting the income |

| Waiver path | Certain war or civil-unrest departures | IRS guidance includes a waiver path |

For FEIE physical presence, the test is explicit: 330 full days in foreign countries during 12 consecutive months. Those days do not have to be consecutive. A full day is 24 consecutive hours from midnight to midnight, so use passport and calendar evidence instead of memory.

Day counting alone is not enough. IRS guidance also ties FEIE eligibility to having a foreign tax home, and it states you still file a U.S. return reporting the income. If you need a first-pass check before calling a CPA, use the IRS Interactive Tax Assistant and save the result with your travel log.

The common miss is assuming a disrupted year still "mostly qualifies." Missing the 330-day minimum fails the physical presence test, even in common disruption scenarios. IRS guidance does include a waiver path for certain war or civil-unrest departures.

FBAR monitoring risk#

Handle FBAR like an aggregation problem, not a legal research project. Keep one tracker for every foreign financial account, its balance history, and a rough converted balance so you can spot drift early instead of discovering it at filing time.

A monthly review is the safe default. Multiple banks or payment platforms can hide risk because each account looks small on its own. The exact reporting trigger and conversion approach depend on your filing context, so set internal alerts only after you verify the rule you are using.

Keep the evidence pack simple and consistent: statements or exports, account identifiers, and notes for opened or closed accounts. For due-date timing and extension updates, check FinCEN's FBAR page directly.

Invoicing risk#

Invoice compliance is usually an operations problem before it becomes a tax problem, because errors hit cash flow first. Specific invoice-field and tax-wording requirements are jurisdiction-specific, so verify what applies before you send. As a baseline, confirm the client billing details you have on file and align your template to the requirements you have validated.

Keep one folder per client with the contract or SOW, onboarding tax details, the issued invoice, and any corrected invoice. That record matters when a client changes billing entities, asks for wording changes, or disputes format after delivery.

The usual failure pattern is delayed payment followed by rushed resubmissions. If billing-country facts change mid-engagement, re-verify before issuing the next invoice instead of reusing the old template.

Related: How to Choose a Tax Preparer for Your Freelance Business.

Tier 2: The "Business-of-One" Risk Management Toolkit#

Once you know the core risks, your tool stack should get much smaller. Use a lean setup that helps you answer four questions quickly: what data you own, what changed, what action to take now, and when to escalate.

| Risk | Minimum viable tool capability | Common failure mode | Safe-default workflow |

|---|---|---|---|

| Residency tracking | Rolling day counter for FEIE physical-presence tracking (330 full days in 12 consecutive months) and Schengen 90/180 tracking, plus notes for jurisdiction checks | Counting from memory or trusting totals without assumptions | Log each crossing the same day, review weekly, and verify current test assumptions before new travel |

| Account-reporting monitoring | Single register for all foreign accounts, aggregate balance view, and FBAR filing reminders (April 15 with automatic extension to October 15) | Looking at accounts one by one and missing the aggregate trigger | Reconcile monthly, set an alert below the $10,000 aggregate trigger, and prepare e-filing when triggered |

| Invoicing compliance | Client tax fields, VIES check capture, and templates that support reverse-charge wording | Reusing stale client details or issuing before VAT checks are complete | Validate before first invoice and again after billing-entity changes; hold invoice if treatment is unclear |

| Primary-source lookup | Direct path to IRS FEIE pages, Publication 54, Publication 901, IRS treaty index, and Treasury treaty text | Stopping at summaries instead of controlling text | Save source link + review date in your notes; escalate when treaty interpretation or conflicting country rules decide the answer |

Residency tracking#

Your day counter should help you make decisions before you create a filing problem. Keep entry and exit dates by country or travel zone in one record. For FEIE, treat eligibility as requirements-based, not automatic just because you live abroad. Watch alerts as you get close to thresholds, and use that information to decide whether to stay, leave, shorten a trip, or adjust your testing window.

Escalate when multiple residency frameworks conflict or when country-specific residency treatment matters and your tool cannot point you to controlling authority. The Schengen calculator is a helper, not legal entitlement.

Account-reporting monitoring#

For account reporting, completeness matters more than sophistication. Maintain one complete account register with status and balance history. FBAR review starts when the aggregate value of foreign accounts exceeds $10,000 at any point in the year. Track the filing window (April 15, with automatic extension to October 15) and plan for e-filing.

| FBAR item | Detail | Note |

|---|---|---|

| Trigger | Aggregate value of foreign accounts exceeds $10,000 at any point in the year | FBAR review starts when the threshold is exceeded |

| Filing window | April 15, with automatic extension to October 15 | Plan for e-filing |

| Main record | One complete account register with status and balance history | Completeness matters more than sophistication |

| Review cadence | Monthly reconciliation | Looking at accounts one by one can miss the aggregate trigger |

| Escalation | Account inclusion is unclear, balance history is incomplete, or the trigger is crossed | Escalate when you cannot defend the data trail |

Escalate when account inclusion is unclear, balance history is incomplete, or your aggregate trigger is crossed and you cannot defend the data trail.

Invoicing compliance#

Invoice tooling should protect cash flow by preventing avoidable rework. Maintain client legal and billing details plus VAT status, watch for failed or unavailable VIES checks and billing-entity changes, and decide whether to send, correct, or pause. Use VIES as a registration check for cross-border trade status, not as a full legal determination on its own.

Escalate when reverse-charge treatment is uncertain across transaction type or member-state handling, or when required invoice wording cannot be confirmed from primary rules.

Primary-source lookup#

When a tool returns "maybe," go to the primary text quickly. Keep a short bookmark stack: IRS FEIE pages, Publication 54, Publication 901, the IRS treaty index, and Treasury treaty texts. Treat phrases like "depends" or "see treaty" as a sign that summary material has done all it can do.

Escalate when treaty interaction or competing country positions determine the outcome.

Tool stack checklist#

- One live day counter updated the same day you cross a border.

- One foreign-account register with monthly reconciliation, $10,000 aggregate trigger alerts, and FBAR reminders.

- One invoicing setup that stores VIES checks and supports reverse-charge wording.

- One primary-source bookmark stack for FEIE, treaty lookup, and country-level checks.

If those tools keep producing conflicting outcomes or leave treaty and residency questions unresolved, you have reached the limit of tooling. That is where Tier 3 begins, and escalating to an advisor becomes the safer default. You might also find this useful: The Best Tax Software for US Expats.

Before you move on, set up a single source of truth for day-count tracking so your residency checks stay consistent month to month. Tax Residency Tracker.

Tier 3: The Escalation Protocol - When to Call a Cross-Border CPA#

This is the line between monitoring and interpretation. Track and retain your own records for the three core risks, then escalate when the answer depends on cross-border interpretation. Tier 2 is for monitoring tax residency, FBAR-related exposure, and invoicing data. Tier 3 starts when judgment, not data collection, becomes the bottleneck.

A practical rule is to stay self-service while you are gathering and organizing facts from your own records. Escalate when you need to decide what those facts mean across jurisdictions. That is where tools often stop at source material without giving you reliable interpretive context. Treaty issues are a common example, and even OECD material on the 183 Day Rule presents application and interpretation as the hard part. The patterns below are conservative escalation signals, not hard legal thresholds:

Consider escalating if one of these patterns appears#

| Scenario | Why self-service is risky | What to bring to advisor | How an advisor can help |

|---|---|---|---|

| Foreign entity setup | You are no longer just tracking compliance; you are choosing a structure with cross-border implications. | Proposed country, entity type you are considering, income sources, client locations, current residency log, and current invoicing setup. | Review whether the structure fits your facts and flag likely coordination and filing implications before you proceed. |

| Treaty conflict exposure | If your answer depends on treaty wording or potential double-tax outcomes, interpretation risk rises quickly. | Country-by-country date log, work-location timeline, income summary, relevant treaty text you found, and notes on where uncertainty starts. | Interpret treaty language against your facts and clarify your likely position on residency, sourcing, or double-tax exposure. |

| Multi-jurisdiction life changes | Moves, dual-base living, or major work-pattern shifts can break assumptions in your existing tracking setup. | Timeline of moves and travel, housing changes, client mix, and planned changes for the next year. | Help reassess your compliance approach and define what records to maintain going forward. |

| Official authority notices | Once a tax authority sends a notice, this is no longer just a research exercise. | Full notice, prior filings, account summary, residency log, and any prior correspondence. | Help frame a consistent response based on complete records and prior filings. |

How to vet the advisor#

Use a fit check, not just a generic credential check:

- Ask which cross-border cases they handle that match your pattern.

- Confirm they actively cover the jurisdictions in your fact pattern.

- Confirm they work from client evidence packs, including residency logs, account records, and invoicing records.

- Treat it as a warning sign if they give confident structure or treaty conclusions before reviewing your dates and documents.

What to prepare before the consult#

Bring an evidence pack so the call is about decisions, not reconstruction:

| Item | What to include | Qualifier |

|---|---|---|

| Timeline | Moves, travel, work locations, and business changes | Dated |

| Residency log | Reconciled to your own records | Evidence pack |

| Foreign-account summary | Gaps clearly marked | Evidence pack |

| Invoicing evidence | Relevant to the issue | Evidence pack |

| Decision questions | Short, prioritized list | Prioritized |

- A dated timeline of moves, travel, work locations, and business changes

- Your residency log reconciled to your own records

- A foreign-account summary with gaps clearly marked

- Invoicing evidence relevant to the issue

- A short, prioritized list of decision questions

If your records are incomplete, say that up front. A common failure mode is asking for expert judgment before the facts are clean enough for a clear recommendation.

For a step-by-step walkthrough, see The Best Accounting Software for a Freelance Bookkeeper.

Conclusion: From Compliance Anxiety to Complete Confidence#

The goal is not to buy a giant research library. It is to build a repeatable way to spot risk early, document your facts, and know when to ask for help.

- Identify your highest-risk exposures

Start with a short, specific list: tax residency, FBAR thresholds, and invoicing. That matters more than shopping for an enterprise research suite, because your decisions depend on facts you can verify.

- Monitor those risks consistently

Build an active tracking routine, not a stack of saved articles. Keep your records together, log what you checked in primary sources, and note when you checked it so issues surface earlier instead of at filing time.

- Escalate with clean records when needed

Set a clear escalation trigger for complex questions. Bring organized records and your exact open question to a specialist CPA, because research access alone does not provide the interpretation needed for action.

Safe default: verify current requirements before you file, and update your tracker after major travel, account, or invoicing changes. If you want a practical starting point, Gruv tools can support parts of that process.

For a related walkthrough, see The Best Software for Calculating and Remitting Sales Tax.

Frequently Asked Questions

What is the difference between tax research software and tax preparation software?

Research software helps you interpret tax questions. Preparation software helps you calculate and file returns. Checkpoint and CCH AnswerConnect are positioned as research tools for tax professionals, while tax software is generally positioned around managing and filing taxes. If your issue is interpretation, like treaty or residency analysis, start with research. If the treatment is already clear, use prep software.

Do I need expensive tax research software as a freelancer?

Usually not, unless your work repeatedly turns on deep interpretation across complex issues. For many business-of-one setups, the bigger need is clean fact tracking and filing execution, not a full professional research library. Also keep in mind that assistive AI research tools do not replace professional judgment, so paying for research access does not remove the need to escalate when the issue turns interpretive.

What are the best free tax research tools for U.S. expats?

Start at IRS.gov/freefile for filing options, and check partner eligibility rules before choosing a Free File provider. For tax-law questions, use the IRS Interactive Tax Assistant and verify key rules on primary IRS pages for Substantial Presence, FBAR, and treaty guidance. When treaty relief matters, verify against the actual treaty text, not only summary tables. After each check, record the page used and date viewed, the fact tested, and any unresolved question for follow-up.

How can I research my specific tax questions without being a CPA?

Use a simple 3-step loop: identify the risk, monitor it with your own records and primary sources, then escalate when interpretation risk appears. In practice, that means day logs for residency exposure, account summaries for FBAR exposure, and IRS tools or instructions for narrower filing questions, while keeping records that support items reported on your return. Escalate when treaty interpretation or competing residency positions enter the picture, and remember that you still remain responsible for return information even if you hire a preparer.

What is the single biggest tax risk for a digital nomad?

A common major risk is residency exposure driven by day count and overall fact pattern, because it can change where income is taxed. Do not assume one universal threshold across countries. For example, the U.S. Substantial Presence Test uses a 31-day current-year threshold and a 183-day threshold over a 3-year period, while other jurisdictions may require broader facts-and-ties analysis. Escalate when your facts are ambiguous, especially when country ties overlap or the outcome depends on treaty interpretation.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

Best Accounting and Tax Advisors for U.S. Expats: Pick the Right Support Level

**Pick the support level that matches your compliance surface area, then evaluate providers on written scope and form coverage.** The common failure mode for most U.S. expats is not "forgetting to file." It is hiring the wrong help model, under-scoping what you actually need, and finding the gap when IRS filings and related reporting obligations hit the critical path. You run a business-of-one, and your tax workflow is part of the system.

How to Choose a Tax Preparer for Your Freelance Business

**Choose a tax preparer for freelancers by ranking compliance controls ahead of speed and price, then shortlist only candidates who can show strong documentation habits.**