Quick Answer

Australian freelancers should choose super on a like-for-like basis, then complete the deduction process correctly, and only then time contributions within the cap rules. Compare long-term net performance, total fees and insurance costs, insurance suitability, and usability. Use ATO YourSuper as a first pass for MySuper products, wait for written acknowledgment before claiming any deduction, and check current caps and fund receipt dates before contributing.

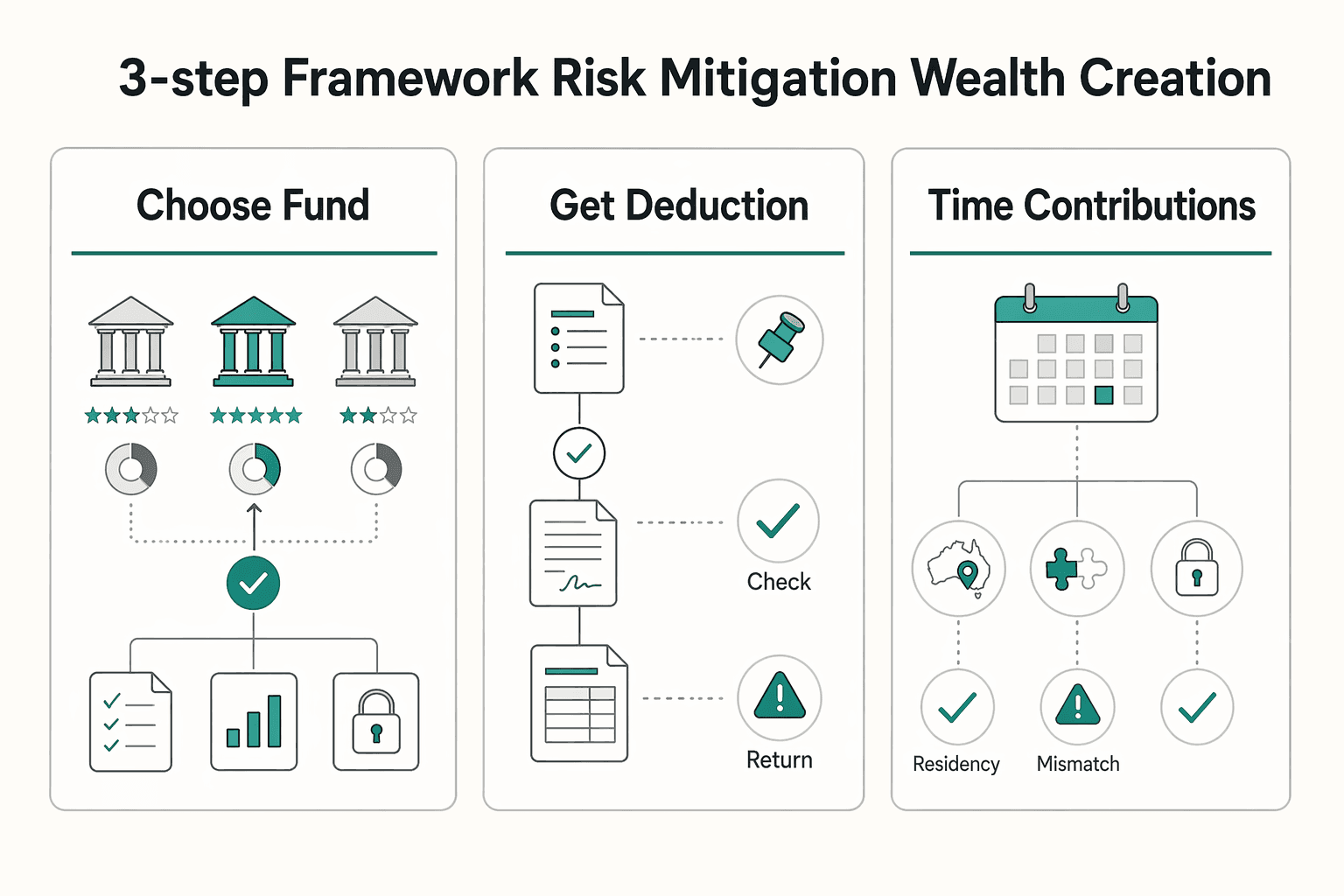

The Superannuation Playbook for the Freelance CEO: A 3-Step Framework for Risk Mitigation and Wealth Creation#

Use this playbook to make three decisions in the right order: choose a fund on a like-for-like basis, complete the deduction process correctly, and time contributions within the cap rules. The focus here is practical execution. Get the sequence right and you can reduce deduction errors, compare funds more cleanly, and time contributions with more intent.

If you are a sole trader or in a partnership, you generally do not have to pay super guarantee for yourself, but you can make personal super contributions. That means the process sits with you. Fund choice, paperwork, and timing are your job.

- Choose the fund with like-for-like criteria

Start with the same inputs across options: fees, insurance, member benefits, performance, and investment options. Use the ATO YourSuper comparison tool as a first pass, including side-by-side comparison of up to four MySuper products. Treat it as a comparison tool, not personal financial advice.

- Get deduction compliance right before lodgment

For personal super contribution deductions, the key step is a valid notice of intent and your fund's acknowledgment. Timing is strict, including the tax return lodgment point for the contribution year. Do not treat the contribution as deductible until that acknowledgment is received.

- Time contributions within current cap settings

For 2025-26, the general concessional contributions cap is $30,000. Later sections cover when carry-forward rules may apply, including the $500,000 total super balance test at 30 June of the previous financial year and the maximum 5-year window for unused amounts.

How to use this guide: first build a shortlist using comparable fund criteria, then complete the deduction sequence, then assess timing opportunities. The next sections give you the comparisons and checklists to do each step properly. For broader freelance-planning context, read Japan Digital Nomad Visa: A Guide to the New 2025 Program.

Part 1: Capital Allocation - Selecting Your Financial Partner#

Start with a like-for-like shortlist and a simple scorecard. When you compare similar options, focus on net outcomes after costs and confirm insurance fit before switching, the decision is usually much clearer. If you are self-employed, you can usually choose your own fund, so use a process rather than a hunch.

Use a four-point scorecard, then weight it to fit your priorities#

A simple scorecard is better than chasing whatever looked strongest last year. Set the weighting based on what matters most to you now.

| Criterion | What to compare | Note |

|---|---|---|

| Long-term net performance | Similar options over 5 years or more | Keep comparisons like-for-like; use short-term results as context |

| Total cost of ownership | Fees and insurance costs | Compare the net result after both |

| Insurance suitability | Cover, eligibility, and cost | Check each fund's insurance details; the ATO tool only compares MySuper products |

| Usability | Contributions, option changes, and document access | Admin drag usually continues |

- Long-term net performance

Compare similar options over 5 years or more. Keep comparisons like-for-like, for example MySuper vs MySuper, or balanced vs balanced. Use short-term results as context, not the main reason to choose.

- Total cost of ownership

Ignore headline fees on their own. Include fees and insurance costs, then compare the net result after both.

- Insurance suitability

Check whether cover, eligibility, and cost fit how you actually work. Because the ATO comparison tool only compares MySuper products, you still need each fund's insurance details before treating two options as equivalent.

- Usability

Choose a fund you can run without friction. If contributions, option changes, and document access are awkward now, that admin drag usually continues.

Build a like-for-like shortlist before you score anything#

Use the ATO YourSuper comparison tool for a first pass on MySuper products, then use APRA's MySuper product performance lookup tool as a second check. The ATO tool compares up to 4 MySuper products at a time and is updated quarterly, so note what you reviewed and the comparison date shown in the tool.

| Fund | Comparable product to check | Long-term net return | Total cost of ownership | Verification note |

|---|---|---|---|---|

| Hostplus | MySuper or balanced equivalent | Current return data pending fund documentation verification | Fee and insurance costs pending current fund disclosure verification | Confirm exact option name and insurance terms |

| AustralianSuper | MySuper or balanced equivalent | Current return data pending fund documentation verification | Fee and insurance costs pending current fund disclosure verification | Check same comparison date as other funds |

| Australian Retirement Trust | MySuper or balanced equivalent | Current return data pending fund documentation verification | Fee and insurance costs pending current fund disclosure verification | Compare like-for-like option only |

| UniSuper | Comparable default or balanced option, verify product type | Current return data pending fund documentation verification | Fee and insurance costs pending current fund disclosure verification | Verify whether you are comparing a MySuper product |

| Cbus | MySuper or balanced equivalent | Current return data pending fund documentation verification | Fee and insurance costs pending current fund disclosure verification | Check insurance availability and member fit |

Red flag for your shortlist: if a MySuper product is rated underperforming for 2 consecutive years, it can no longer accept new members.

Choose hands-off, active, or stop before SMSF#

Default-style options are usually the right starting point unless you want more involvement. If you want low maintenance, start with a MySuper option or a balanced option. MySuper is the default starting point when you do not pick an option, and balanced is a mix of growth and defensive assets aimed at steadier returns.

| Option | What it means | Note |

|---|---|---|

| MySuper option | Default starting point when you do not pick an option | Start here if you want low maintenance |

| Balanced option | Mix of growth and defensive assets | Aimed at steadier returns |

| Direct investment option | You select investments yourself | Requirements can differ by fund; Hostplus Choiceplus includes a more than $10,000 eligibility threshold and a $2,000 minimum balance in other options |

| SMSF | You manage the fund yourself | Trustee responsibility applies, and mistakes can have financial impacts |

Use a direct investment option only if you want to select investments yourself and follow product rules. Requirements can differ by fund. For example, Hostplus Choiceplus includes a more than $10,000 eligibility threshold and a $2,000 minimum balance in other options.

Treat an SMSF as a separate commitment, not a default upgrade. It means managing the fund yourself with trustee responsibility, and mistakes can have financial impacts. For broader freelancer finance context, see The Best Bank Accounts for Freelancers in Canada.

Part 2: Your Compliance Shield - Mastering Tax-Deductible Contributions#

Once you have chosen a fund, the next risk is process failure. If you want to claim a deduction for personal super contributions, sequence matters: give notice to your super fund or RSA provider, then wait for its acknowledgement before you claim.

Follow this four-step checklist in order#

If you do these steps out of order, your deduction claim may fail even when the contribution itself was made correctly. The contribution alone is not enough; your notice and the fund's acknowledgement are required parts of the claim process.

- Make the personal contribution.

This is your own after-tax contribution paid into your super account. The fund must receive it before there is anything to claim.

- Complete NAT 71121.

NAT 71121 is the ATO "Notice of intent to claim or vary a deduction for personal super contributions." You use it to tell the fund that received your contribution that you intend to claim a deduction.

- Send NAT 71121 to the receiving fund (or RSA provider).

The notice goes to the fund or RSA provider, not to the ATO. Recipient and order both matter. If the notice is misdirected, or the contribution is moved before the notice is accepted, your claim may fail.

- Wait for acknowledgement from the fund.

Only claim the deduction after the fund confirms it received a valid notice. Keep both the notice and the acknowledgement as evidence.

The deadline is an earliest-of test, not one fixed date. Lodge your notice by whichever comes first: the day you lodge your tax return for that contribution year, or the last day of the following income year. Confirm the relevant financial year and lodgment cutoff from official ATO guidance, fund records, or advisor records before using the date in a deduction claim.

Common failure points you can prevent#

These errors are preventable if you check the sequence before lodgment. Common mistakes include misdirected notices, early rollovers, and claims made before acknowledgement.

- Wrong recipient: sending NAT 71121 somewhere other than the fund or RSA provider that received the contribution.

- Missing acknowledgement: claiming before acknowledgement is received.

- Rollover too early: moving the contribution before the original fund accepts the notice.

- Wrong contribution type: trying to claim employer-related amounts through this personal notice process.

Set your cap with a simple formula#

Treat this as a calculation, not a guess. Concessional inputs count together across all your funds, including employer amounts and salary sacrifice.

Your personal deductible contribution room = current concessional cap verified from official ATO guidance - employer contributions - salary sacrifice amounts - other personal contributions you will claim as a deduction

If you have both freelance and employee income, include employer-related concessional amounts before deciding your personal amount.

| Action | Evidence to keep | Risk if skipped | Status |

|---|---|---|---|

| Make personal contribution | Transaction record from your bank/fund | No contribution available to claim | ☐ |

| Complete and send NAT 71121 to the receiving fund/RSA provider | Copy of NAT 71121 and submission record | Invalid or misdirected notice | ☐ |

| Receive acknowledgement from the fund | Acknowledgement from the fund/RSA provider | Deduction may not be accepted | ☐ |

| Confirm earliest-of deadline and claim only after acknowledgement | Dated compliance note and tax return workpapers | Late notice or premature claim | ☐ |

If you keep one rule front and center, use this: avoid rolling over the contribution or lodging your return before your notice is accepted and acknowledged.

Related: A Guide to Tax Residency in Australia for Digital Nomads. To make contribution-time recordkeeping easier, standardize what you send clients and what you store for tax season with the Free Invoice Generator.

Part 3: Your Growth Engine - Advanced Super Strategies#

Once your deduction process is solid, you can look at contribution flexibility, insurance fit, and long-term savings. These choices can change outcomes, but only if you execute them cleanly.

1. Carry-forward concessional contributions#

Carry-forward concessional contributions can be useful when your income is uneven, but start with eligibility, not contribution size. Check your total super balance at the prior 30 June first, then calculate unused cap space.

| Step | Check | Rule |

|---|---|---|

| Confirm eligibility | Total superannuation balance | Must be less than $500,000 on 30 June of the previous financial year |

| Calculate unused concessional space | General concessional cap and prior unused amounts | Cap is $30,000 for 2025-26; unused amounts expire after 5 years |

| Count concessional inputs | Employer contributions, salary sacrifice, and personal contributions you plan to claim | Count across all funds |

| Choose timing | When the fund receives the money | Contribution counts in the year the fund receives it, not when you start the transfer |

| Complete the deduction sequence | Approved notice and fund acknowledgement | Lodge the notice and wait for acknowledgement before claiming |

- Confirm eligibility first. Your total superannuation balance must be less than $500,000 on 30 June of the previous financial year. Recheck the current ATO rule before acting.

- Calculate unused concessional space. The general concessional cap is $30,000 for 2025-26, and unused amounts expire after 5 years. Count employer contributions, salary sacrifice, and personal contributions you plan to claim across all funds.

- Choose timing based on receipt date. Contributions count in the year the fund receives the money, not when you start the transfer.

- Then complete the deduction sequence. If you want to claim a deduction for a personal contribution, lodge the approved notice and wait for fund acknowledgement before claiming.

In practice, common errors include miscounting concessional inputs across multiple funds or missing the fund-received date near 30 June.

2. Insurance inside super#

Insurance inside super only works if the policy terms fit freelance income patterns and the evidence a claim is likely to require. Read the income definition, waiting period, exclusions, and evidence requirements before you assume the cover will work when you need it.

For variable income, pay close attention to how income is defined. Under an indemnity value policy, the benefit is based on a percentage of salary at claim time, and variable earners may be assessed on average annual earnings.

| What to check | Why it matters for freelancers | What to verify before you keep or change cover |

|---|---|---|

| Income definition method | Variable income can reduce benefits if the policy uses recent or averaged earnings | Read PDS wording for pre-disability income/salary/average annual earnings |

| Waiting period fit | Longer waiting periods can lower premiums, but you must fund the gap | Match waiting period to your real cash buffer and fixed costs |

| Benefit period fit | Benefit period controls how long payments can continue after acceptance | Check whether it covers likely recovery or restart timelines |

| Exclusions | Exclusions can limit payout in practice | Check PDS or insurer material for definitions and exclusions |

| Claims evidence requirements | Claims may fail or stall without required evidence | Expect claim forms, medical evidence, and possibly certified proof of identity |

If you cannot clearly explain how your policy defines income, treat that as a review trigger. Also, if cover is held through super, you cannot claim the premium as a personal tax deduction. The ATO comparison tool only covers MySuper products, so do not rely on it alone for insurance detail.

3. Non-concessional contributions#

Non-concessional contributions make sense when you want to move after-tax money into super for long-term savings and you are not claiming a deduction.

For 2025-26, the annual non-concessional cap is $120,000. The bring-forward arrangement may apply if eligible, but availability is not automatic. Balance-based rules can reduce your cap to nil, and the 2025-26 framework references $2 million in the nil-cap test.

This approach fits when you have surplus cash you do not need for near-term tax, operations, or emergency reserves. It is a poor fit in tight cashflow periods because super is generally preserved until a condition of release is met. For people born from 1 July 1964, preservation age is 60, with access still subject to release rules.

The trade-off is straightforward: money outside super keeps liquidity and flexibility. Money inside super supports long-term savings but is less accessible.

Action checklist#

Use this as a final pause point before you contribute more, change cover, or act on unused cap amounts. The goal is simple: have the numbers, policy wording, and timing details in front of you before you act.

- Review now: prior 30 June total super balance, all concessional inputs across funds, and whether your income protection definition matches variable income.

- Document now: contribution receipts, cap calculations, relevant PDS sections (income definition and exclusions), and your waiting-period cash buffer.

- Verify before acting: current ATO caps, current carry-forward balance test, non-concessional and bring-forward eligibility, and the date your fund will receive the contribution.

- Pause if unclear: do not execute large contributions or policy changes until your evidence pack is complete (acknowledgements, policy wording, and claim-document requirements).

For a step-by-step walkthrough, see The Best Pension Providers for UK Freelancers.

Conclusion: You Are the Asset - Protect and Grow It#

Your earning capacity is your core business asset, so treat your super review as a risk check first and a growth decision second. If you came looking for the best superannuation funds for freelancers, use a tighter filter: compare net outcomes on like-for-like products, follow deduction rules exactly, and do not trigger avoidable insurance or rollover losses.

- Review first: Compare like-for-like options. Use ATO YourSuper to screen MySuper products and then check fees, insurance, service, and risk fit for how you actually work. Confirm the data date shown in the tool before deciding.

- Verify before acting: For personal deductible contributions, confirm the notice timing rules for the Notice of intent to claim a deduction and the fund's written acknowledgment. Your concessional cap is counted across all funds combined. The ATO source used here shows $30,000 from 1 July 2024, so re-check the current-year cap before you contribute. If you plan to use carry-forward amounts, confirm your TSB was less than $500,000 at the prior 30 June and verify unused cap amounts from the previous 5 years.

- Defer until confirmed: Do not finalize rollovers or insurance changes until fees, cover impacts, and destination details are clear. Do not assume your highest-balance account is the right account to keep.

For your next super review, use this checklist:

- Verify the current financial-year concessional cap and TSB rule thresholds from official ATO guidance

- Keep records of your contributions and notice process

- Lodge your notice and confirm written acknowledgment is on file

- Check the latest YourSuper/APRA data date before comparing MySuper options

- Confirm with your existing fund whether any insurance entitlements could be lost before a rollover

- Pause any rollover until fees, cover loss, and destination details are verified

The standard here is simple: clear sequence, verified details, and records that support each decision. You might also find this useful: A Guide to Superannuation for Australian Freelancers.

Frequently Asked Questions

How much super should you contribute as a freelancer?

Start with cashflow, not a fixed percentage. If your income is steady, regular personal contributions can work; if it is uneven, lump sums may be easier when cashflow allows. If you want a deduction and can preserve the money, verify the current concessional cap from official ATO guidance before setting the amount. If your total super balance was under $500,000 at the prior 30 June, check whether unused concessional cap amounts from up to 5 years are available.

What is the exact order for claiming a tax deduction on a personal contribution?

Make the personal contribution first so the fund receives the money, then lodge NAT 71121 with the fund or RSA provider that received the contribution. Wait for the fund's written acknowledgment before you claim the deduction in your tax return. The deadline is the earlier of the day you lodge that year's tax return or the end of the following income year. The notice can be invalid in some cases, including if you started a super income stream from that contribution or already made a contributions-splitting application for it.

How should you compare funds and insurance?

Start with long-term net returns, then compare total fees, insurance fit, service reliability, and portability on a like-for-like basis. Use ATO YourSuper as a screening step for MySuper products, and remember a MySuper product rated underperforming for 2 consecutive years cannot accept new members. For insurance, rely on the fund's PDS and insurance guide, especially if your income varies.

Can you pay yourself super from your business account?

Yes. If you are a self-employed sole trader or partner, you can make personal contributions from business cashflow or a personal account even though you generally do not have to pay super guarantee for yourself. Make sure the fund receives the contribution, keep payment and fund records, and keep any NAT 71121 acknowledgment if you plan to claim a deduction.

Should you consolidate multiple super accounts?

Often, yes, but do a pre-transfer check first because a rollover can remove benefits you still need. Confirm the new fund accepts the rollover and check whether you will lose insurance or other features. Make sure replacement cover is active before closing an old account. Insurance on inactive accounts can be cancelled after 16 months without contributions, and default cover may not apply for new members under 25 or with balances under $6,000 unless an exception applies.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Japan Digital Nomad Visa 2026: Six-Month Planning Runbook

Treat this as your operating model: identify the right mission first, commit to one route, and keep dated records before you make irreversible plans. That is what keeps the rest of your timeline, paperwork, and decisions coherent.

Australia Tax Residency for Digital Nomads With GST and ABN Checkpoints

The goal is a defensible, low-drama position the Australian Taxation Office (ATO) can follow from your records, not a clever workaround. For a digital nomad, that usually means keeping two tracks straight: residency and GST/ABN admin. Consistency is what holds up over time: use real facts, take steps in a clear order, and keep documents that still match months later.

A Guide to Superannuation for Australian Freelancers

**Treat superannuation for freelancers australia as a repeatable operating decision, not a guess you make under invoice pressure.** As the CEO of a business-of-one, your job is to turn fuzzy compliance questions into a simple system you can run on demand. Freelance income moves, contract terms shift, and one wrong super call can squeeze cashflow or create a compliance problem you only notice later.