Quick Answer

Choose the best cap table management software by matching the tool to your stage: spreadsheet with signed founder documents at the start, then a professional platform when non-founder equity begins. Your practical selection criteria are compliance workflow depth, modeling reliability, admin burden, and budget fit. In vendor demos, verify controls like role-based access, immutable change history, and export readiness so your record holds up in diligence.

The Founder's Equity Playbook: A 3-Stage Framework for Managing Ownership#

| Stage trigger | Core risk | Required capability | Recommended tool class |

|---|---|---|---|

| Founder-only ownership, with signed legal docs and very few changes | Version confusion, informal recordkeeping, no clear change control | One current source of truth, disciplined updates, document-backed entries | Legally backed spreadsheet |

| You are preparing to grant equity beyond the founder group, or approvals and permissions tracking are starting to matter | Manual governance failure through human error, version confusion, and delayed reporting | Role-based access control, approval controls, export controls, audit trail, multi-factor authentication | Professional cap table software |

| You need to model rounds, option pools, RSUs, or convertible instruments like SAFEs or notes | Misstated dilution, reporting friction, poor auditability across more instruments and stakeholders | Scenario modeling, immutable audit logs, least-privilege access, support for rounds, pools, RSUs, and convertibles | Advanced equity management platform |

Choose your equity tool based on execution risk, not startup image. If ownership is still simple and changes are rare, a spreadsheet may be enough for a period. Once grants, approvals, permissions, or investor scenarios enter the picture, software becomes important because it formalizes ownership data, rights, and change history so the record is auditable.

The easiest way to decide is to ask one question: what goes wrong if this cap table is wrong today? The answer usually tells you whether you can stay manual, move to a basic platform, or step up to a more capable equity product.

Here is the practical read on those stages. In Stage 1, your job is not to buy software just because you can. It is to keep the ownership record clean, current, and tied back to signed documents. If two founders keep separate files, or edits happen without a dated record of what changed, you are already creating the version confusion software is supposed to prevent.

Stage 2 is where many teams wait too long. The moment equity administration extends beyond a simple founder split, the important feature is not a prettier interface. It is governance. You need to know who can view, edit, approve, or export data, whether MFA is enforced, and whether every change is captured in an immutable audit log.

Mis-timing mistakes#

- Move too early: You can end up paying for permissions, approval layers, and reporting depth you do not yet use. Another common problem is getting locked into a long-term contract with heavy termination penalties before you know whether the tool fits your real needs.

- Move too late: Migration gets harder because you now need a clean data map, a validated migration plan, and a rollback option before go-live. If a vendor cannot offer migration guidance, sample templates, and a sandbox to test permissions and approvals, treat that as a red flag.

By Stage 3, the tool is no longer just a record. It needs to help you model future ownership with confidence. The next sections walk through each stage in detail so you can see what to track, what to verify, and when to move from spreadsheet to software. Related: How to Create a Cap Table for Your Startup.

Stage 1: The Legally-Backed Spreadsheet (Founders Only)#

Use a spreadsheet only while ownership is still founder-only, changes are infrequent, and your founder split is already documented in signed formation and founder equity documents. At this stage, the spreadsheet is a tracking tool, not the enforceable record. If the file and signed documents differ, treat the signed documents as the source of truth.

Your job in Stage 1 is to keep one clean, current record that stays consistent with your legal agreements and any ownership numbers shared elsewhere.

Founder-only checklist: what to track and why it matters#

- Founder legal name: prevents identity confusion during diligence and migration.

- Exact share count: keeps ownership precise; percentage-only tracking is not enough.

- Issue date: preserves a clear timeline of ownership decisions.

- Security type: avoids confusion once additional instruments are introduced.

- Authorized share total: helps catch issued-share drift against approved capacity.

- Dated change notes tied to supporting documents: improves auditability and makes future exports easier to trust.

After each update, confirm there is only one live version and reconcile entries against signed documents.

Failure modes to avoid#

- Handshake assumptions: undocumented understandings can turn into founder disputes.

- Unsynced versions: multiple files create uncertainty about who owns what.

- Undocumented equity edits: missing change history weakens auditability and can slow diligence.

Move to Stage 2 as soon as any non-founder equity workflow starts (employee, advisor, or contractor equity). That is where manual tracking is more likely to miss vesting, conversion logic, and consistent audit-ready records.

You might also find this useful: The Best Tools for Managing a Global Equity Plan.

Stage 2: The First Hire - Your Trigger for Professional Tools#

Once you grant equity to anyone beyond the founders, move from a spreadsheet to dedicated equity management software. At that point, you are no longer just tracking ownership. You are administering option grants, vesting, fair-market-value support, approval records, and a holder-facing view of equity.

This is where spreadsheet risk becomes operational risk. Errors can lead to audit issues, incorrect tax withholding, and lower employee trust. A common failure moment is when an investor, auditor, or board member asks for your cap table and the numbers do not reconcile, or an old vesting schedule creates new uncertainty.

What breaks first in a spreadsheet#

The first breakdown is usually evidence, not arithmetic. You need one system that connects grant terms, vesting schedules, current ownership, and valuation support. If you cannot quickly show what was granted, when vesting started, what the holder can see, and what approval record supports the issuance, your process is already fragile.

Timing and maintenance break next. A spreadsheet can list grants, but it does not reliably run the workflow around them. You need accurate vesting administration, a current ownership record across instruments, and readiness for checkpoints like 409A support, Form 3921 support, and 83(b) election support where relevant. A valuation misstep can create IRS penalty risk and complicate fundraising.

After each grant, run the same control check: security type, exact share or option count, vesting start date, strike price, and employee-facing record should all match signed documents. Keep approvals and valuation support together so you can produce a clean record on request, not rebuild history from email.

Carta and Pulley as a buying decision#

At this stage, choose for compliance fit and operational reliability, not feature volume.

| Decision criterion | Choose Carta if demo evidence shows | Choose Pulley if demo evidence shows | Verify before signing |

|---|---|---|---|

| Compliance workflow depth | Strong handling of grants, vesting records, valuation-related steps, and tax checkpoints | The same core controls with workflows your team can run consistently | Current handling for 409A, Form 3921, and 83(b) support where relevant |

| Modeling usability | Scenario modeling is clear enough your team will use it regularly | Scenario modeling is easier for your day-to-day operators | Ability to model hires, option pool changes, SAFEs, and future rounds |

| Admin overhead | Setup, permissions, and ongoing updates match your team capacity | Ongoing administration feels lighter for your actual staffing level | What still requires manual entry or outside counsel/finance support |

| Employee equity visibility | Employee view reduces clarification churn | Employee portal/statements are clearer for your team | Exactly what holders can see and how records are delivered |

| Pricing and support fit | Needed plan and support level fit your budget and pace | Needed plan and support level fit your budget and pace | Current plan terms, implementation scope, and add-on fees |

Minimum capabilities checklist#

Use this as the minimum bar:

- Grant administration: issue and track grants without parallel spreadsheets.

- Vesting records: vesting is visible and tied directly to each grant record.

- Valuation support: fair-market-value workflow support, including 409A checkpoints.

- Tax workflow support: Form 3921 and related employee tax-event support.

- Employee access: each holder can view their equity without manual updates from you.

If you are still finalizing plan design, align that structure before grants accelerate. See How to Structure an Employee Stock Option Plan (ESOP) for a US Startup.

Choose the platform you can keep accurate under pressure. In Stage 3, that same system becomes your planning base for dilution, hiring, and financing decisions. If you want a deeper dive, read Value-Based Pricing: A Freelancer's Guide.

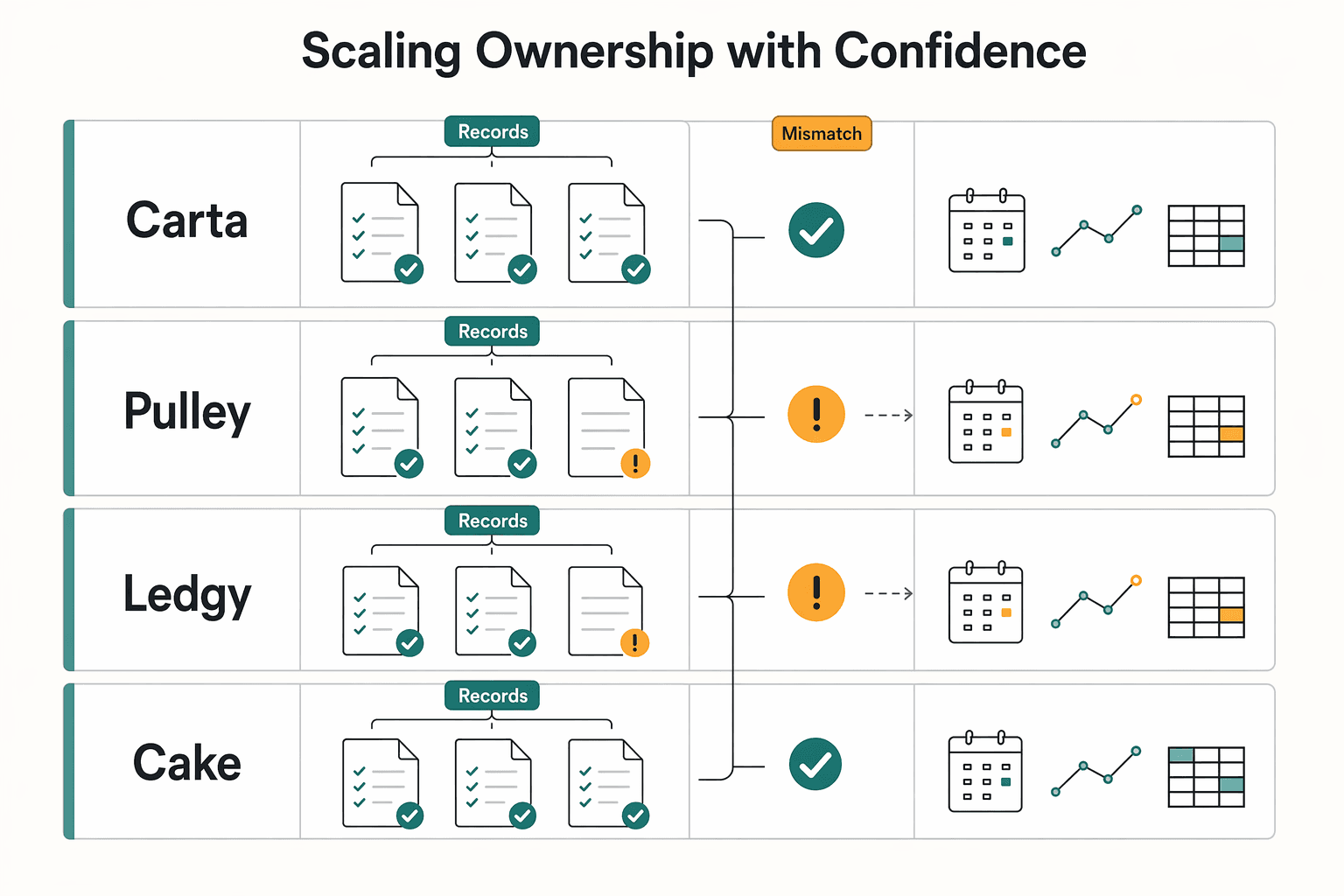

Stage 3: Scaling Ownership with Confidence#

At this stage, you should run equity as an operating system, not a one-off admin task. Your ESOP process needs one reliable record that connects governance, grant execution, employee visibility, and scenario planning before hiring or fundraising decisions are made.

Start by standardizing grant governance. Run every grant through the same sequence: compensation decision, board approval or consent, signed grant documents, cap table update, and employee delivery. After issuance, verify that the security type, share or option count, vesting start date, strike price, and approval date match across the consent record, signed grant notice, and employee-facing view. Keep 409A support or other valuation backup in the same evidence pack, because valuation mistakes can create tax risk and financing friction.

As soon as hiring and financing timelines overlap, model decisions before you make promises. Test grants against your current pool, planned hiring, and likely next round so dilution tradeoffs are visible early. If you are moving toward Series B or beyond, treat this as a precision problem: clean approvals, clear reporting, and strong auditability matter more than convenience.

Use this as a fit table, not a universal ranking.

| Platform | Typical fit signal | Global readiness | Modeling depth | Employee experience | Admin control prompt |

|---|---|---|---|---|---|

| Carta | Commonly positioned for Series A+ in 2026 comparisons | Partial support for international stakeholders | Full scenario modeling | Full employee equity app | Verify board consents, approval audit trail, and current pricing directly |

| Pulley | Commonly positioned for pre-seed to Series A with SAFE/note modeling | Not available for international stakeholders in the cited matrix | Full scenario modeling | Partial employee app | Verify what still needs manual legal/finance follow-up and current pricing |

| Ledgy | Strong fit candidate for cross-border stakeholder setups | Full support for international stakeholders | Full scenario modeling | Full employee equity app | Verify valuation workflow and document handoff, since built-in 409A is not available in the cited matrix |

| Cake | Strong fit candidate where employee clarity and onboarding speed matter | Full support for international stakeholders | Full scenario modeling | Full employee equity app | Verify governance records, board approval handling, and jurisdiction fit in your demo |

Keep employee communication explicit: tell people what the platform record confirms and what still depends on signed legal documents. Most breakdowns at this stage come from stale portal data, verbal promises, or grants approved in principle but not fully issued. If you operate across borders, confirm international stakeholder support directly instead of assuming it.

Before financing, audits, or strategic transactions, your process should already produce:

- Board approvals, consents, and audit trail for each issuance and change

- Current cap table export tied to signed grants, vesting, exercises, and cancellations

- ESOP documents and valuation support

- Related tax records where relevant

- Reporting exports ready for investors, auditors, or counsel without rebuilding history from email

If any internal policy depends on a pool-refresh target, approval threshold, or country-specific rule, document it and mark unresolved values as pending until counsel or finance confirms them.

We covered this in detail in The Best Expense Management Software for a Remote Team.

Conclusion: From Liability to Leverage#

The real win is not a prettier cap table. It is using a tool that fits your stage and keeping the underlying records accurate. That is what helps turn ownership management from recurring risk into something more manageable.

-

Stage 1: Founders only. If you are still running on a spreadsheet, treat accuracy as the primary checkpoint before you go deep on any 2026 tool comparison. Key differentiator: at this stage, the question is whether your current records are reliable enough to compare options with confidence.

-

Stage 2: New equity issuance. Once you are actively comparing software, use explicit evaluation criteria instead of brand familiarity. Start with plain-language checks: features, pricing, benefits, and whether a provider addresses decision questions like 409A valuations in its buying material. Key differentiator: the goal is to reduce spreadsheet, compliance, and stakeholder-communication burden as complexity rises.

-

Stage 3: Ongoing administration. When equity workflows overlap, move beyond a basic portal and test for operational fit. One 2026 review highlights Pulley for scenario-based equity forecasting, but your practical check is whether the system helps you manage ongoing equity work without rebuilding context each cycle. Key differentiator: this is where fit starts to matter more than feature lists.

Use this as a quick self-audit before you move on. Have you compared tools on stated evaluation criteria? Are you pressure-testing how the tool handles ongoing operational complexity? If one answer is no, that is your next task. The FAQ below covers edge cases that often surface after the basic decision is made.

Frequently Asked Questions

Can you keep using a spreadsheet if there are only founders on the cap table?

Yes, if the spreadsheet is only a record of signed founder documents and not a substitute for them. Tie share counts and vesting terms back to executed paperwork and approvals, and have counsel confirm the spreadsheet matches the legal record.

What is the real trigger to move from manual tracking into software?

A practical trigger is your first non-founder equity grant, but it is not a universal legal cutoff. If you are about to issue options, restricted stock, warrants, SAFEs, or notes, start evaluating a platform before the grant goes out. Make sure the platform can track the specific instruments you use.

Why does manual tracking fail once financing gets more complex?

It usually breaks at the edges you do not notice until diligence or a round, such as pro rata rights, vesting logic, conversion terms, and overlapping instruments. If you already have multiple SAFEs or notes, run a sample financing and see whether your current model still holds up under conversion. Your platform import should reproduce historical transactions cleanly, and you should test complex conversions before you trust any output.

Do you need a valuation before granting stock options?

This depends on your jurisdiction and facts, so treat valuation as a pre-grant legal and tax checkpoint with counsel and tax advisors. Confirm the fair market value process they want you to follow, then build that approval sequence into the platform. Do not assume a vendor label or built-in valuation feature satisfies your legal or tax requirements in every jurisdiction.

What should you check before you issue equity to a first employee or advisor?

You need more than a grant screen and an email trail. Confirm the plan materials, approvals, grant terms, and exercise or acceptance steps are present and stored in one place. If you need a refresher on plan setup, see How to Structure an Employee Stock Option Plan (ESOP) for a US Startup, and have counsel confirm the current filing window for any tax-sensitive election or notice before you act.

How should you choose the best cap table management software for your company?

Start with accuracy, auditability, and financing-workflow maturity before you worry about interface polish. Score each option on four things only: compliance depth, scenario modeling, admin workload, and budget fit. Then ask each vendor to show audit logs and diligence-ready exports, not just dashboards.

How do you compare vendors without getting stuck in brand debates?

Focus on the work your team actually has to do in the next 12 months. Use your own data to test imports, run a sample financing, model dilution, and export a diligence pack. Some 2026 buying guides mention onboarding claims like <1 week, but treat that as something to validate rather than accept.

What are the most common implementation mistakes after you buy a platform?

The biggest one is assuming migration equals cleanup. Reconcile historical transactions before launch, then compare the platform output against signed grants, vesting schedules, cancellations, and any note or SAFE terms. Run a mock audit or diligence export early, because export problems often show up long after the import looked done.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- dau.edu/sites/default/files/2025-01/DAU%20Project%20...trusted

- dep.nj.gov/wp-content/uploads/rules/rules/njac7_13.pdftrusted

- dodcio.defense.gov/Portals/0/Documents/CMMC/AssessmentGuideL2v2...trusted

- dot.ny.gov/main/business-center/contractors/constructio...trusted

- fhwa.dot.gov/bridge/pubs/hif21031.pdftrusted

- norfolk.gov/m/FAQtrusted

- cakeequity.com/guides/best-cap-table-softwareexternal

- cakeequity.com/guides/best-equity-management-softwareexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

How to Structure an Employee Stock Option Plan (ESOP) for a US Startup

If you searched for **employee stock option plan esop**, stop and sort out the label first. In startup conversations, people often say "ESOP" when they mean a stock option plan or option pool. A formal **Employee Stock Ownership Plan (ESOP)** is different. It is often discussed as a business transition option for owners, while startup stock options are commonly used to give employees a stake in the business.

How to Create a Cap Table for Your Startup

A cap table should do three jobs well: record ownership, help you model decisions, and hold up in diligence. Most founders start by treating it like an administrative file: a spreadsheet, a few signed PDFs, and a hope that everything still ties together when it matters. That view is too narrow, and it gets expensive later.