Quick Answer

Choose the best software for sales tax based on who owns compliance risk in your actual invoicing flow, not on rate calculation alone. For cross-border services, confirm place-of-supply, verify EU business IDs through VIES, and apply reverse-charge treatment only when supported. If your process still depends on manual handoffs between tools, errors and payment delays remain likely. A broader integrated setup or a Merchant of Record arrangement can reduce that risk when scope is clearly defined.

Beyond Software: A Risk Mitigation Framework for Your Global Service Business#

If you are looking for the best software for sales tax, decide on the operating model before you compare calculators. The real risk is not just getting the rate wrong. It is knowing where tax is due, who has to account for it, and whether the liability stays with you.

-

Start with VAT/GST scope, not just U.S. sales tax. If you sell services across borders, you may be dealing with VAT/GST regimes used in over 170 countries and, if you have U.S. exposure, over 12,000 U.S. jurisdictions. When those regimes are not well coordinated, the risk is not only miscalculation. It can also include double taxation or unintended non-taxation.

-

Use place-of-supply logic before pricing any tool. For services, the key question is usually which country treats the service as supplied there. That outcome can trigger registration and VAT accounting obligations in that country, not just a different tax rate.

-

Handle B2B reverse charge at the invoice level. For many B2B services, taxation follows where the customer belongs, and reverse charge can shift VAT accounting to the buyer. When the customer is liable, your invoice needs to reflect that treatment clearly under EU rules.

-

Separate automation from liability ownership. Some tools automate calculation and parts of filing or remittance workflows while filing and remittance responsibility stays with you. More outsourced setups can take on more of that work, but scope varies, and prior periods can still remain your responsibility. A Merchant of Record model is different because it can hold transaction-level legal, financial, and compliance responsibility.

-

Use a maturity lens to choose safely.

Ad hoc means manual checks and invoice fixes after the fact. Systematized means a repeatable process and cleaner records, with filing and remittance responsibility still in-house. Integrated means billing, accounting, and tax handling work together, with some outsourced models taking on more filing and remittance work.

When you compare options, score them on three things: invoice correctness by default, integration with your billing and accounting flow, and clear ownership of filing, remittance, and liability. You might also find this useful: The Best Tax Software for US Expats.

Your Real Challenge Isn't Sales Tax - It's a Global Compliance Matrix#

If you operate across borders, a sales-tax-only checklist is too narrow. The real job is managing compliance across multiple jurisdictions as rules change and administrative work grows.

That review is not a side task. Cross-border compliance means working across different tax codes, frequent regulation updates, and heavier admin overhead.

- Jurisdiction mapping first: identify which countries or jurisdictions your transactions touch and keep those records consistent across your internal systems.

- Responsibility path second: define who owns tax-compliance decisions and how your team adapts review steps as regulations shift.

- Checklist discipline as scale control: mistakes create rework, and rework slows approvals. A simple pre-send checklist helps teams stay consistent at higher volume.

| Decision point | Service business logic | Product e-commerce logic |

|---|---|---|

| What usually drives review | Multi-jurisdiction compliance duties, changing regulations, administrative burden | Checkout-oriented sales-tax workflows and transaction volume |

| What teams emphasize in setup | Clear compliance responsibilities and process coverage | Simpler setup for high-volume online sales tax workflows |

| Common tooling bias | Broader compliance process coverage and exception handling | Often optimized for simpler, high-volume checkout flows |

You can see that bias in how tools are positioned. One 2025 comparison describes TaxJar as simple, cloud-based, and e-commerce focused, with pricing listed as starting at $19/month. That may fit straightforward online retail, but it does not automatically solve every cross-border service compliance scenario.

Once you map that compliance-responsibility path, software selection gets much simpler. You can then choose the operating tier and stack that reduce corrections and compliance surprises. If you want a deeper dive, read Value-Based Pricing: A Freelancer's Guide.

Tier 1: The Ad-Hoc Operator (High Risk, High Anxiety)#

If you create invoices manually and track tax exposure in separate files, you may be carrying avoidable risk. Manual work is not the core problem. Disconnected records increase error risk and rework.

In practice, this shows up as a correction loop: CRM, contract, and invoice details do not match, required tax details are requested late, and invoices are revised after submission.

The three signals that tell you you're still in Tier 1#

1. Buyer details are incomplete at invoice time. For B2B services, buyer status affects tax treatment because place-of-supply can depend on whether the customer is a taxable person. Under EU VAT rules, invoices are generally required for most B2B supplies, and invoice content can require the customer VAT ID when the customer is liable for VAT. If buyer type or the required tax ID is missing, your tax treatment is not well supported.

| Signal | What to check | Grounded detail |

|---|---|---|

| Buyer details are incomplete at invoice time | Buyer type and required tax ID | If buyer type or the required tax ID is missing, your tax treatment is not well supported |

| Reverse-charge treatment is applied by habit, not by validated workflow | Properly validated tax ID | A common failure mode is treating a sale as no VAT before the tax ID is properly validated |

| No threshold or registration alerting | Registration triggers | TaxJar support describes dashboard visibility at 75% of a state threshold and email notification at 100% |

2. Reverse-charge treatment is applied by habit, not by validated workflow. In relevant cases, invoices must indicate reverse charge. VAT liability can also shift to the customer when services are supplied by a non-established supplier. A common failure mode is treating a sale as no VAT before the tax ID is properly validated. If validation is missing or inconclusive, pause and resolve treatment before issuing.

3. You have no threshold or registration alerting. Spreadsheets can track totals, but they can miss registration triggers unless monitored consistently. Some tools provide threshold alerts. TaxJar support describes dashboard visibility at 75% of a state threshold and email notification at 100%. If you only check at period end, you may discover triggers late. If this is your weak spot, read A Guide to Sales Tax Nexus for Remote Businesses.

Tier 1 risk checklist#

Before you send any cross-border invoice, run this checklist:

- Confirm buyer type

Mark B2B or B2C from evidence, not assumptions. If it is unclear, stop and resolve it first.

- Validate buyer tax ID where relevant

For EU VAT numbers, verify through VIES. Do not treat VIES as global coverage, and note that UK GB VAT-number validation through the old VoW service ceased on 01/01/2021.

- Apply reverse-charge wording only when supported

When applicable, include a reverse-charge reference such as "Reverse charge". If validation is null or unclear, hold the invoice and clarify.

- Store the evidence trail digitally

Keep the tax ID check result, buyer-type note, invoice version, and approval record together. Record retention is a core control, and some VAT regimes require digital records in compatible software.

Your immediate move#

The quickest Tier 1 upgrade is to make this process repeatable before you add more review. Choose tools against three criteria: validation support so tax IDs are checked before issue, template controls so required fields and reverse-charge wording stay consistent, and an audit trail so you can show what was checked, when, and on which invoice.

For a service business, those controls usually reduce risk faster than adding more manual review.

Related: How to Get a Sales Tax Permit as a Freelancer.

Tier 2: The Systematized Professional (Moderate Risk, Lingering Anxiety)#

Tier 2 often looks organized from the outside, but risk still sits in the handoffs between tools. That is why payment friction and compliance anxiety can persist even when the process feels mature.

1. E-commerce-first logic mismatch#

A product-oriented stack may calculate tax well for checkout flows, but service invoicing can strain that model. Many e-commerce platforms are built around shipping-address sales-tax logic. For cross-border services, you may still need a clear process for questions like buyer status, location evidence, and invoice treatment decisions.

The cost shows up in invoice edits, slower approvals, and uncertainty about whether the final treatment is supported. If you are evaluating the best software for sales tax, start here: can it support cross-border service decisions inside the workflow, or do you still make those decisions outside the tool?

2. Reconciliation gaps across tools#

A patchwork setup can break down when you need to explain one invoice from end to end. One tool shows the invoice, another shows the payment event, and another shows tax output, but the full decision trail can remain fragmented.

Integration breadth helps, but it does not guarantee control. Avalara states it has over 1,400 signed partner integrations and an open API for non-prebuilt systems. Treat that as connectivity, not proof of reliable handoffs. Run a trace test on one paid invoice. If you cannot clearly connect the tax decision, the amount paid, and where evidence is stored, you likely have an attribution gap.

3. Manual handoffs before invoice send#

At Tier 2, high-risk steps can still be manual. You may check key details in one place, adjust invoice wording in another, and send payment from a third.

That creates misses under deadline pressure: checks not attached to the invoice record, wording applied by habit, or payment requests sent before the invoice version is final. If your process still depends on copying decisions between tools before send, treat that as active risk.

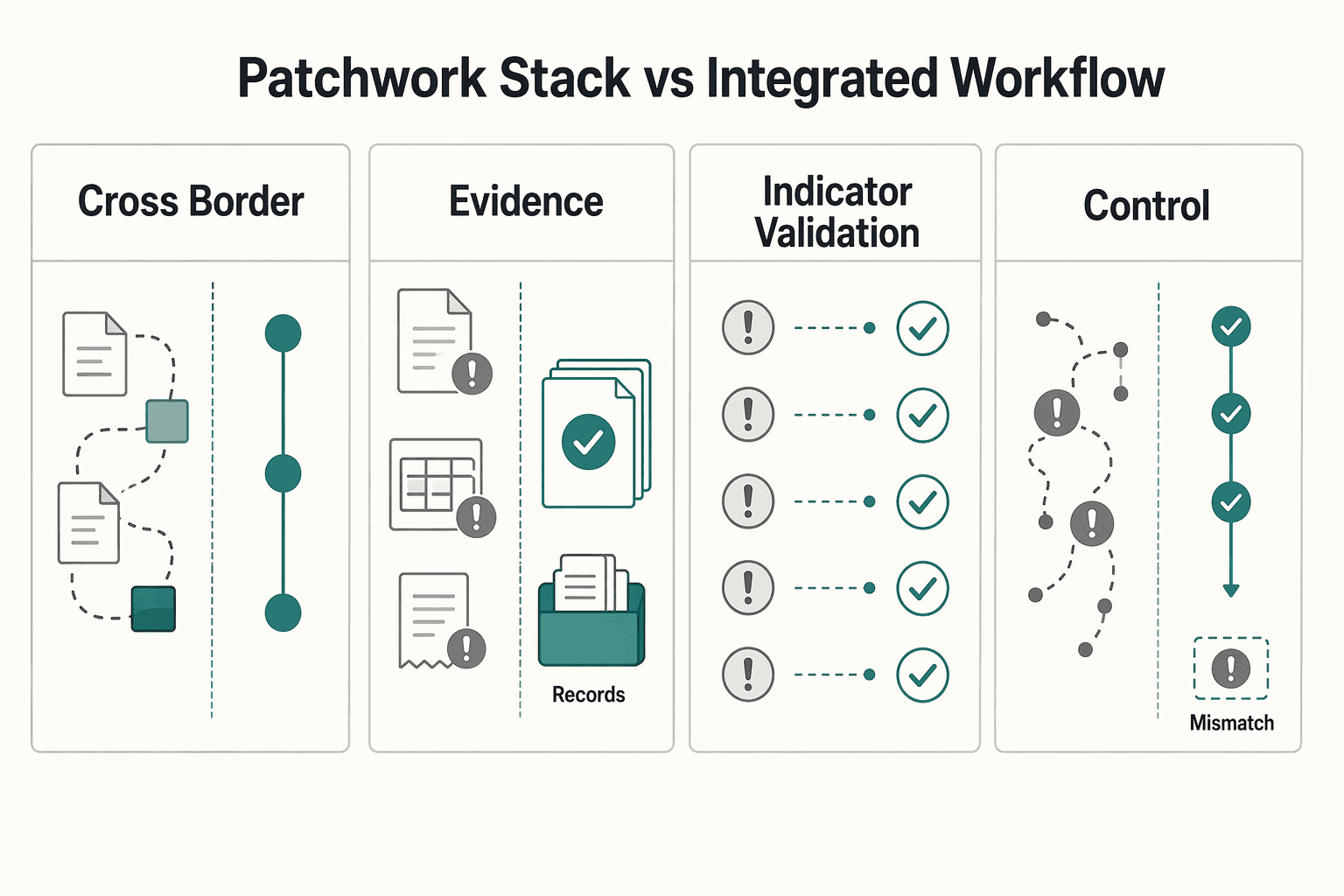

Patchwork stack vs integrated workflow#

| Decision point | Patchwork stack | Integrated workflow |

|---|---|---|

| Cross-border service support | E-commerce logic often leads | Service treatment decisions are handled in the same workflow as invoicing |

| Decision trail (attribution) | Invoice, payment, and tax decisions are split across tools | Decision, amount, and evidence trail stay linked |

| Indicator validation | Checks are ad hoc | Indicators are defined, validated, and reviewed for data quality |

| Handoff control | Reconciliation happens after issues appear | Handoffs are checked before invoice release |

| Record retrievability | Evidence is scattered across tools | Evidence is retrievable for review and reporting |

Use a simple control test. Define and validate five indicators, then check data quality for each: service-decision capture, attribution trail completeness, handoff control, invoice-payment linkage, and record retrievability.

Move to Tier 3 when you no longer own risk at the handoff points. If invoice release still depends on memory, manual copy and paste, or post-payment reconstruction, you do not need more features. You need a process that stays reliable without you acting as the last control.

For a step-by-step walkthrough, see Best Sales Compensation Software for Solo Operators in 2026.

Tier 3: The Automated Enterprise-of-One (Low Risk, Total Control)#

Tier 3 means tax handling is built into how you invoice and collect payment, not managed as a separate manual check. The outcome is straightforward: treatment is decided before send, proof stays with the transaction, and exceptions are reviewed on purpose.

1. Automation in the payment flow#

At this level, your setup determines treatment from seller configuration and customer context, then keeps that decision attached to the same transaction record. That includes inputs like business address, registrations, tax codes, customer location, and customer status.

The real gain is control, not just speed. When tax treatment, invoice behavior, payment event, and ledger entry stay connected, you can explain why an invoice was issued the way it was without reconstructing events across tools. If you are choosing software, use this filter: does it keep decisions inside the payment path, or push critical steps back onto you?

2. Calculator versus Merchant of Record#

A calculator can automate a lot without taking legal responsibility away from you. It may determine rates, validate VAT IDs in supported regions, and apply reverse-charge logic when tax ID and jurisdiction conditions are met. You still need filing and remittance coverage where you are registered.

A Merchant of Record model is different because the provider is the recognized seller in the transaction model. In that setup, responsibility can shift materially, but only within the actual contractual and operational scope. Also, "MoR" is not itself a tax-law term, and no platform removes every edge case.

Use this simple rule:

- Calculator plus filing tools: you still own the chain unless filing and remittance scope is explicitly enrolled and active.

- MoR model: confirm who is the seller for the transaction and who carries filing and remittance obligations.

3. What new client onboarding looks like in practice#

A strong Tier 3 process is predictable, and it usually follows this order:

| Step | Action | Output |

|---|---|---|

| 1 | Capture customer location and business status up front | Customer location and business status |

| 2 | For EU B2B services, apply place-of-supply based on where the customer is established | Place-of-supply decision |

| 3 | Validate VAT ID through VIES and store the result and timestamp with the transaction | VAT ID result and timestamp |

| 4 | Apply invoice treatment before send | If reverse charge applies, include the required reverse-charge reference and insert the current required wording after verification |

| 5 | Post to the ledger with treatment attached | Reporting reflects the original decision path |

Treat exceptions as the real risk surface. VIES returns valid or invalid outcomes, can lag national systems, and has an explicit accuracy caveat. Since GB VAT number validation ceased through VIES on 01/01/2021, route affected cases through exception review before invoice release.

4. Tier 2 versus Tier 3#

| Decision area | Tier 2 | Tier 3 | What it means for you |

|---|---|---|---|

| Ownership of liability | You usually retain liability unless separate filing coverage is enrolled and in scope | Liability shifts only where seller status or filing responsibility is explicitly handled by provider model or scope | You must confirm responsibility per jurisdiction, not assume it |

| System integration | Tax, invoicing, and payment records are often split | Treatment is decided and retained in one transaction path | Can reduce reconstruction work during audits |

| Exception handling | Ad hoc handling of failed checks and unusual jurisdictions | Exceptions are blocked, reviewed, and documented before send | Fewer preventable invoice mistakes |

| Finance visibility | Reconciliation mostly happens after payment | Ledger, invoice treatment, and payment event align at creation | More real-time visibility into cashflow and compliance posture |

Tier 2 helps you make fewer mistakes, but Tier 3 changes when and where mistakes can happen.

5. Operating at Tier 3#

| Control | Action | Grounded detail |

|---|---|---|

| Configuration | Configure seller details, registrations, tax codes, invoice logic, and payment flow as one system | Where local rules are needed, record the current requirement after verification |

| Proof retention | Retain proof per transaction | Customer location, business status, VAT ID result, timestamp, invoice version, and applied treatment |

| Exception review | Run exception reviews on a fixed cadence | Failed IDs, missing data, or out-of-scope jurisdictions should block send until cleared |

| Responsibility by jurisdiction | Confirm filing and remittance ownership per jurisdiction | Verify enrollment and scope for filing products and seller status in MoR arrangements |

| End-to-end trail | Keep an end-to-end proof trail accessible | Any invoice can be explained without relying on memory or multiple disconnected tools |

At this level, you want the proof trail to be routine, not heroic. Any invoice should be explainable without relying on memory or a chain of disconnected tools.

We covered this in detail in The Best Payroll Software for a Company with Employees in India.

Before you send a cross-border B2B invoice, run a quick VAT check to help reduce avoidable rework and payment delays with the VAT Number Validator.

Conclusion: Build Your Business on a Foundation of Confidence#

Choose your operating model before you choose a tool. Good software for sales tax only helps if it removes send-time guesswork, reduces compliance handoffs, and makes tax-liability ownership explicit.

-

Tier 1: You are still the final checkpoint. If you are deciding tax treatment when you send an invoice, you are still carrying most of the risk. In U.S. workflows, you may collect from the customer and still need to remit on the state schedule. Virginia shows how specific that gets: starting with the April 2025 filing period, filers use Form ST-1, and returns are due on the 20th of the following month. In EU B2B work, invoices are generally required, and when reverse charge applies after verification, your invoice needs the required indication.

-

Tier 2: Your tools are better, but the joins are still fragile. A calculator plus invoicing plus separate filing can improve tax determination, but you still own every handoff. That is where records drift across systems and correction work grows. TaxJar explicitly notes that multi-state filing is hard to manage manually, and AutoFile support depends on enrolled scope. The practical test is simple: can you keep the tax decision, customer proof, timestamps, invoice version, and filing record connected without manual stitching?

-

Tier 3: You choose a model that matches the real job. This is where you stop shopping for an app and choose clear operating ownership. A unified tax workflow for calculation, reporting, and filing, or a Merchant of Record model with contract scope you have verified, can reduce post-invoice handoffs and clarify who handles tax on each payment. That clarity matters when deadlines slip. Texas states a 5% penalty for taxes paid 1-30 days late, and 10% when paid over 30 days late.

Next step: audit your path from invoice creation to payment to filing. Flag every spreadsheet, every manual approval, and every point where liability ownership is unclear. If your system still depends on manual checks at send time, treat that as remaining risk and move toward a unified setup.

This pairs well with our guide on The Best Tax Research Software for Accountants.

If you want to replace fragmented tax and payment steps with a single compliance-first operating model, review Merchant of Record for freelancers.

Frequently Asked Questions

Do you need to worry about VAT or sales tax first?

Start with the tax system that applies to where and how you sell, because VAT and sales tax can involve different compliance workflows. In the U.S. alone, you may face thousands of tax jurisdictions, so verify jurisdiction and customer context before invoicing. That helps you avoid charging the wrong tax or missing required treatment.

If you invoice an EU business client for services, what should you verify before sending the invoice?

Confirm the client’s business status and the tax documentation required for the jurisdictions involved, then store the verification result with a timestamp in the transaction record. If treatment is unclear, verify requirements before finalizing the invoice. That reduces invoice rework and payment delays tied to missing or incomplete proof.

Does software built for physical goods usually fit a service business?

Not always. Some tools are designed around product checkout flows rather than service invoicing decisions. Test whether tax treatment is decided in your real invoice path without spreadsheet patching or manual re-entry. That matters because manual data entry creates avoidable errors.

What is the real difference between a calculator and a broader compliance platform?

Treat this as a workflow decision, not just a feature list. A calculator can determine tax, while some compliance platforms also support filing and payment steps, but you still need to verify exact scope and enrollment before relying on that coverage. | Option | Liability ownership | Workflow fit for service businesses | Payment-delay risk outcome | |---|---|---|---| | Calculator tool | You often retain filing and remittance responsibility | Good for transaction-level tax determination when integrations are strong | Lower calculation error risk, but handoffs can still delay resolution | | Compliance platform | May support filing and payment steps, depending on enrolled scope | Better when you need calculation plus compliance tasks in one flow | Fewer missed post-invoice steps and fewer handoff delays | | Merchant of Record model | Depends on who is contractually the seller and what jurisdictions are covered | Useful only when seller status and operational scope clearly match your transactions | Lower assumption risk when ownership is explicit, high risk if scope is unclear |

If a provider says it uses a Merchant of Record model, are you done?

No. You still need to verify seller status, jurisdiction coverage, and filing and remittance responsibilities in the contract and operating flow. “MoR” alone does not prove every obligation moved off your side. That prevents liability assumptions that surface later as compliance gaps.

Do you still need to watch thresholds and registrations if you automate tax?

Yes, because automation does not remove registration timing risk. Economic nexus can be triggered by thresholds such as $100,000 in sales or 200 transactions, but those are examples, not universal rules. Verify current jurisdiction requirements before invoicing at volume to reduce back-tax, penalty, and interest exposure, and review A Guide to Sales Tax Nexus for Remote Businesses if needed.

What should you check in the product before paying for it?

Check integration coverage with the systems you already use and confirm that the tool keeps a clear audit trail for each tax calculation. Integrations with platforms like QuickBooks, Shopify, WooCommerce, or Amazon can reduce manual handoffs, but depth and quality still vary by product. Pricing signals such as From $19/month, 700+ integrations, or $349 per sales tax registration per location only matter if your invoicing and reporting flow runs cleanly from end to end.

What happens if you send an invoice with the wrong tax treatment?

The immediate risk is operational. Payment can slow down while you correct and reissue documents. Before sending, keep customer context, tax decision inputs, timestamps, invoice version, and applied treatment in one record. That gives you a defensible audit trail and a faster correction path when exceptions happen.

How do you choose the best software for sales tax if you are a solo service business?

Choose the tool that matches your risk surface and workflow, not the longest feature list. For lower invoice volume, prioritize treatment accuracy and proof retention. For broader jurisdiction exposure, prioritize registration tracking, filing support, and integration coverage. Run one real invoice scenario, including an exception case, before committing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- comptroller.texas.gov/taxes/file-pay/penalties.phptrusted

- europa.eu/youreurope/business/taxation/vat/check-vat-n...trusted

- europa.eu/youreurope/business/taxation/vat/cross-borde...trusted

- irs.gov/taxtopics/tc305trusted

- legislation.gov.uk/eudr/2006/112/article/226/adoptedtrusted

- tax.virginia.gov/retail-sales-and-use-taxtrusted

- taxation-customs.ec.europa.eu/taxation/vat/vat-businesses/invoicing_entrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

How to Get a Sales Tax Permit as a Freelancer

Start with what the client actually receives, not the label you use for your work. Classify each offer by the output delivered, because that shapes taxability and whether permit follow-through may be required.

When Remote Businesses Need to Register for Sales Tax Nexus

Yes, you can trigger sales and use tax obligations in states where you have no office, warehouse, or local staff. It pays to verify early and keep clean records as you grow. One operational risk is letting your records drift out of sync. If that happens, you may not be able to show when nexus started, which sales counted, and when registration should have happened.