Quick Answer

Expats in Germany should compare private health insurance providers only after confirming they can legally choose private cover, testing whether the premium still works in weak-income months, and checking each household member separately. The article's framework is: verify eligibility, assess reversal risk, model the exact tariff over time, and then compare providers using written proof and real support tests.

A low monthly premium from a private insurer can look like a simple buying decision. It is not. It starts a long financial commitment, and quick comparison sites often skip the part that matters most: whether private health insurance is a smart move for you at all. Before you compare providers, make a go or no-go call for your business of one. The real issue is not which insurer looks cheapest today. It is how hard this choice may be to unwind later, and whether the upside is worth the long-term business risk.

This article is built to help you make that decision in the right order. First, confirm whether private insurance is even open to you. Then test whether the numbers still hold up when income is weaker or household circumstances change. Only after that should you compare insurers, tariffs, and support quality. That sequence matters because a polished quote can distract you from the harder question: is this a durable decision for your life, or just an attractive option for this month?

Stage 1: The Go/No-Go Analysis - Should You Even Consider Private Insurance?#

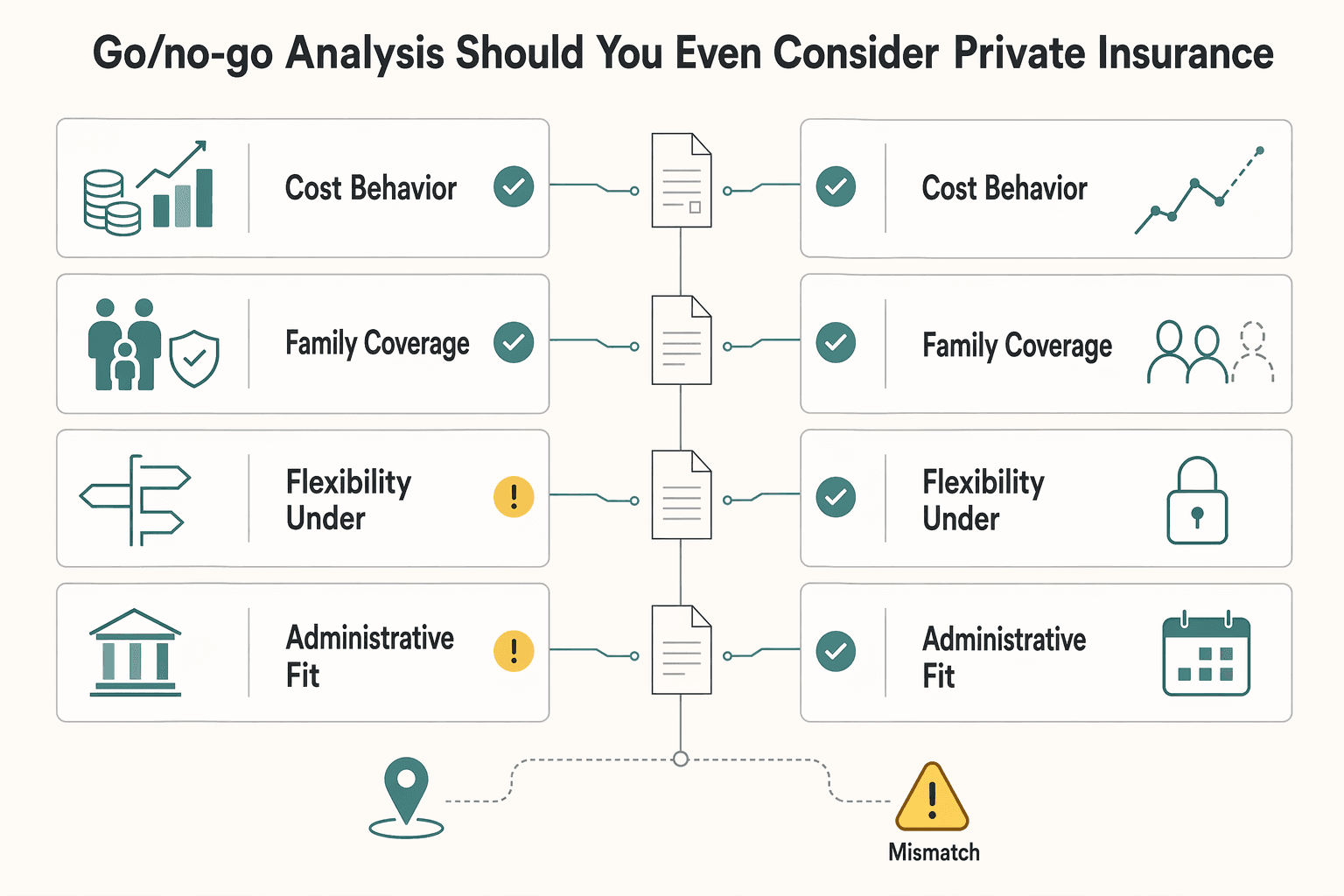

Start with a go or pause decision before you compare providers. The focus here is the public route versus the private route. The main planning risk is choosing a path before you verify whether you can choose at all, then building your timeline around assumptions about switching later.

Germany has two main health insurance systems, and health insurance is required for residents. Your first filter is status: are you pflichtversichert (must use public insurance) or freiwillig versichert (can choose public or private)?

| Decision point | Public side | Private side |

|---|---|---|

| Cost behavior | Your options depend on status and income rules. | Use a real quote for your case, not a generic starting price. |

| Family coverage model | Some family situations have specific public treatment (for example, certain students under 25 with publicly insured parents). | Do not assume the same family treatment. Check each person separately. |

| Flexibility under income swings | Context changes with status and earnings. | Your chosen contract still has to work in weak-income months. |

| Administrative fit for expats | May be mandatory or optional depending on your status. | For some expats, private may be the only option, so confirm first. |

The practical order here is simple: verify eligibility, test whether your plan depends on an easy exit later, pressure-test affordability, then check household impact. If any one of those fails, stop there. Do not move on to provider comparison as if the strategic decision is already settled.

1. Eligibility check#

This is the fastest way to decide whether to keep going. For employed people, income is the key checkpoint. The source used here, updated January 26, 2026, describes 77.400 euros per year as the line: below it, compulsory public; above it, voluntary status with a choice. Verify the current threshold before you act.

| Group | Status note | What to check |

|---|---|---|

| Employed | Income is the key checkpoint; the source describes 77.400 euros per year as the line: below it, compulsory public; above it, voluntary status with a choice | Check your contract and recent payroll records, then verify your annual gross income against the current threshold |

| Self-employed/freelance | The same source describes voluntary status with a choice between public and private | Check records showing your business status and current income pattern, then confirm how your status is being treated for insurance |

| Student/dependent | Students are also described as voluntary, with a family-coverage exception noted below | Confirm whether a public family route applies before comparing private offers |

Status and records checklist

- Employed: check your contract and recent payroll records, then verify your annual gross income against the current threshold.

- Self-employed/freelance: check records showing your business status and current income pattern, then confirm how your status is being treated for insurance.

- Student/dependent: confirm whether a public family route applies before comparing private offers.

A useful discipline here is to base your answer on documents you can save, not on memory or an estimate. If your work setup has changed recently, use the most current records you have and confirm that they support the status you are assuming. The point is not to make a best guess. It is to avoid building your whole search around a route that may not actually be available to you.

Go: you have verified that you can legally choose. Pause: you are still estimating status or using an unverified threshold.

2. Reversal-risk check#

Do not build your plan around "we can always switch later." Treat this as a planning check, not a legal assumption. Your options depend on your circumstances, so a later switch should be treated as uncertain until you verify it. Insurance affects your timeline, budget, and household setup, so this is not a side decision.

A practical way to test reversal risk is to write down the assumption in plain language: "This works because I can switch later if I need to." Then challenge it. What has to stay true for that to happen? Does your plan depend on future employment status, a different income pattern, a move, or a household change that has not happened yet? If yes, your current decision may be leaning on a future event rather than a verified present option.

You do not need a perfect long-term forecast. You do need to know whether your choice is still acceptable if a later switch is not available on the timeline you imagined.

Go: your plan still works if changing routes later is slower or more limited than you expect. Pause: your plan depends on a future switch you have not verified.

3. Affordability check#

This is where a promising quote either survives contact with reality or fails it. Use your own numbers and an actual quote. Fill this worksheet only after you verify current rules:

- Current monthly net income pending finance-record verification

- Low-month or slow-quarter income pending finance-record verification

- Current public contribution rules pending official/provider verification

- Current employee threshold pending official verification

- Actual private monthly quote pending provider verification

- Cash buffer for insurance during income dips pending finance-record verification

Then answer one question: does the private quote still work in a weak quarter, not only a strong one?

When you do this, avoid using your best recent month as the baseline if your income moves around. Use a normal month, then a weaker one. If you are self-employed or freelance, that stressed case matters more than the headline number. A tariff that feels comfortable when business is strong can feel very different when invoices are late, a contract pauses, or a slow quarter stretches longer than expected. The test is not whether you can pay it once. It is whether you can keep paying it without creating pressure elsewhere in your finances.

You should also check whether your cash buffer is real, not theoretical. If you write down several months of cushion, ask yourself where it sits today and whether it is already needed for other obligations. If the answer is "it depends," your margin may be thinner than it looks.

Go: the quote is manageable in your stressed case. Pause: the quote only works when income is consistently high.

4. Family-impact check#

A household can change the decision quickly, so do not validate only your own case. One clear checkpoint on the public side is this: if you are under 25 and your parents are publicly insured, you can be covered through your parents for free.

For everyone moving with you, verify their path separately before you compare providers. That means not only asking whether they can be covered, but also whether their route needs its own quote or confirmation. A private quote for one adult does not validate the household plan. The common failure mode is to check the main earner carefully and treat everyone else as an afterthought. That is exactly where cost and administration surprises tend to appear.

Go: you have checked status and route for each household member. Pause: you have only checked yourself and assumed the rest.

If you want a deeper dive, read The Crypto Cautionary Tale: Why Freelancers Should Be Wary of Crypto Payments.

Stage 2: The CFO's Deep Dive - Modeling the True 30-Year Cost of Your Policy#

If Stage 1 gives you a legal go, the next question is not the first quoted monthly price. It is whether the tariff stays workable over time based on documents you can verify. Treat this as a durability check: can you keep the same tariff through normal years and weaker income periods?

This stage is less about prediction and more about discipline. You are trying to avoid making a long commitment from a short snapshot. That means working from the exact tariff, documenting what you are relying on, and running more than one affordability path instead of one optimistic projection.

1. Model the exact tariff, not the brand#

Start with the exact tariff name and version shown in your offer and policy documents. Build your model from written tariff terms, the full quote, and documented inclusions, exclusions, and optional add-ons, not from headline pricing.

This matters because the brand name does not tell you enough. Your financial model should tie back to the exact product you may actually sign. Keep the quote, the tariff wording, and any add-on selections together in one file set so you can compare like with like. If you cannot match the quoted price to the written tariff terms, you are not modeling the real option yet.

2. Clarify Altersrückstellungen before you rely on it#

If your materials mention Altersrückstellungen, do not gloss over the term. This article does not provide a verified technical definition you can rely on. For decision-making, treat it as a due-diligence item. Ask the insurer or adviser to explain it in writing for the exact tariff and show where that explanation appears in the contract set.

A practical approach is to ask for three things in one message: the plain-language explanation, the contract wording tied to your exact tariff, and the specific document where that wording appears. That keeps the discussion anchored to the policy you may buy instead of a generic explanation that sounds reassuring but is hard to verify later.

3. Use a reusable 30-year scenario template#

A single neat forecast is not enough. Run multiple scenarios, then compare affordability under normal and stressed income.

| Scenario | Starting monthly premium | Annual increase assumption | Year 10 monthly premium | Year 20 monthly premium | Year 30 monthly premium | Affordability note |

|---|---|---|---|---|---|---|

| Normal case | Add your quoted premium | Add a documented assumption | Calculate | Calculate | Calculate | Fits normal income: Yes/No |

| Higher-adjustment case | Add same starting premium | Add a conservative assumption | Calculate | Calculate | Calculate | Still fits with margin: Yes/No |

| Downturn case | Add same starting premium | Add a stress assumption | Calculate | Calculate | Calculate | Fits stressed income period: Yes/No |

The point of the template is consistency. Use the same starting quote across all rows, change only the assumptions you are testing, and make yourself write a clear pass or fail note for each case. If you leave the affordability note vague, it becomes too easy to talk yourself into a weak result.

You can also use the template to compare shortlisted tariffs side by side. When each candidate is modeled the same way, you are less likely to be swayed by presentation style or sales language. A tariff that starts lower but fails your downturn case is not a better option just because the first-month price looks cleaner.

4. Stress-test low entry premiums with documents#

A very low starting price is a due-diligence trigger, not a conclusion. Request written support on:

| Written support | Use in review | Decision rule |

|---|---|---|

| The exact tariff wording and add-on terms tied to your quote | Start with the tariff-level documents, then compare them against the quote | If it is not reflected in the documents you can save, treat it as incomplete |

| How premium adjustments can occur under that contract | Check whether the projected premium path stays affordable in both your normal and downturn scenarios | Fail the option if it works only in strong-income periods |

| Any assumptions used in quote illustrations | Check whether the pricing story can be supported with contract-level documents | If the pricing story cannot be supported with contract-level documents, fail the option |

| Any unresolved items you need clarified before signing | Request clarification before signing | Proceed only if the unresolved items are clarified |

Proceed only if the projected premium path stays affordable in both your normal and downturn scenarios. Fail the option if it works only in strong-income periods or if the pricing story cannot be supported with contract-level documents.

It also helps to review the support pack in a fixed order. Start with the tariff-level documents, then compare them against the quote, then add any written explanations from the insurer or adviser. If an explanation sounds important but is not reflected in the documents you can save, treat it as incomplete. The test here is not whether the insurer can tell a convincing story. It is whether the key parts of that story are documented well enough for you to rely on them.

You might also find this useful: The Best Health Insurance for Digital Nomad Families. Before you commit to a tariff, stress-test your monthly runway and downside scenarios with the pricing calculator.

Stage 3: The Global Professional's Provider Matrix - Choosing a Partner, Not Just a Plan#

Once the tariff looks sustainable, shift from price to execution. Use one matrix across every provider. Fill it only with written proof or your own test interactions, and mark anything else as "not verified." That gives you a consistent way to choose a reliable partner, not just a plan that sounds good.

A matrix can reduce a common shopping bias: once a price looks attractive, it becomes easy to excuse missing details. Keep the standard the same for every candidate, and treat missing documentation as a decision signal.

The current source set does not verify insurer-specific rankings, policy terms, legal thresholds, or service-level outcomes, so keep this stage strictly evidence-first.

1. Verify the document trail before you compare price#

Start with documents, not marketing copy. For each provider, collect and store the exact materials you will rely on, and log where each statement came from.

Working rule: score an item only if it is available in a form you can save, date, and compare side by side. If a point is only described informally, keep it as "not verified."

The operational detail matters here. Save files in a way that lets you find them later, note the date you received them, and keep provider responses attached to the same record. That makes comparisons easier and reduces interpretation drift.

2. Compare scope claims using exact wording#

Broad coverage claims are not enough on their own. Use a table and copy exact language directly, or write "not verified."

| Provider | Scope claim (exact wording) | Limits or conditions (exact wording) | Process requirements (exact wording) | Notes |

|---|---|---|---|---|

| Candidate A | [quote exact wording] | [quote exact wording or "not verified"] | [quote exact wording or "not verified"] | [notes] |

| Candidate B | [quote exact wording] | [quote exact wording or "not verified"] | [quote exact wording or "not verified"] | [notes] |

| Candidate C | [quote exact wording] | [quote exact wording or "not verified"] | [quote exact wording or "not verified"] | [notes] |

Do not paraphrase unless you have to. Copying exact wording reduces the chance that different clauses will look equivalent when they are not. If one provider gives broad language but no usable clause, leave the cell as "not verified."

3. Test operational workflow before signing#

A provider can look fine on paper and still be difficult in practice, especially while traveling. Run a real pre-signing test for each provider:

| Pre-signing test | What to record | Score on |

|---|---|---|

| Submit one realistic support question through the actual channel | What actually happens | Clarity and repeatability |

| Ask for the exact next steps for a standard request | Whether the next step is obvious without follow-up | Clarity and repeatability |

| Send one English-language support request if that matters to you | Whether you can submit, track, and resolve without confusion | Clarity and repeatability |

| Test app or web portal steps you would actually use while traveling | Whether you can submit, track, and resolve without confusion | Clarity and repeatability |

Score each provider on clarity and repeatability. Can you submit, track, and resolve without confusion? Record what actually happens and whether the next step is obvious without follow-up.

4. Match freelancer features to your real scenarios#

Freelancer-specific features only matter if they fit situations you may actually face. Define your scenarios first, and require written answers tied to your quote or contract set.

- Income interruption: what is documented for your case?

- Relocation pause or sabbatical: what is documented for pause or dormancy handling?

- Return to Germany: what is documented for restarting, changing, or continuing cover?

If a scenario answer is not documented yet, mark it as "not verified" in your matrix. For a deeper freelancer-specific view, see A Guide to Health Insurance for Freelancers in Germany.

A useful test is to write each scenario as a short timeline. What happens first? What document would you need? Who would you contact? What written rule supports that step? If you cannot map the process from the materials you have, treat the feature as unverified.

Related: Can Digital Nomads Claim the Home Office Deduction?.

Conclusion: Make Your Decision with CEO-Level Confidence#

By this point, the decision should be documented and low on guesswork. If any key point still depends on a sales call, a summary sheet, or a verbal promise, pause and verify before signing. The goal is not to sound certain. It is to confirm what is actually true in writing.

- Risk fit

Start with a go or no-go check: is your eligibility and enrollment route clearly confirmed in writing for your situation? If your category, employment status, or switching path is unclear, treat this as not ready to sign.

- Long-term cost logic

Evaluate the plan, not just the entry price. Keep the exact plan name, quote-linked policy wording, and written reserve or adjustment terms in your file. If long-term cost wording or core policy documents are missing, your affordability check is incomplete.

- Provider operations

Confirm how the policy works in real life: who issues the contract, who supports you after purchase, what contract language applies, and what written rules apply when you need care across borders. If claims steps, support contacts, or coverage clauses are vague, treat that as a real risk.

Use this final pass or fail checklist before choosing from your shortlist, then gather your shortlisted offers and validate current policy terms and conditions for each one before you commit.

- Eligibility fit: Pass only if your category and enrollment route are confirmed in writing.

- Cost clarity indicators: Pass only if exact policy wording and long-term cost terms are documented.

- Practical support needs: Pass only if claims handling, contract language, and out-of-country care rules are clearly documented.

- If any point is unclear: Pause and verify before signing.

For a step-by-step walkthrough, see The Best Bank Accounts for Freelancers in Germany.

If your case has extra complexity, get a practical second check before you sign via contact.

Frequently Asked Questions

What are `Altersrückstellungen` in private health insurance?

Treat Altersrückstellungen as a contract term you need to verify in writing before you compare plans. This article does not provide a full technical definition, so ask the provider to show the exact tariff or policy wording tied to your quote and compare the written clauses side by side.

Can you switch back from private to public health insurance in Germany?

Do not assume switching back from private to public works the same way in every case. The article says your path depends on your circumstances and should be confirmed in writing before you sign, especially if your plan only works because you expect an easy reversal later.

How much does private health insurance increase with age?

Do not rely on a generic market estimate for how premiums change with age. This article does not provide a verified age-based increase formula, so request written tariff and policy wording on how adjustments are handled and use the scenario template to test your own quote.

Is private health insurance worth it if you are self-employed?

It can be worth considering if you are self-employed, but eligibility and fit are different questions. The article says self-employed professionals, freelancers, and business owners can choose private insurance regardless of income, with stated exceptions for artists, publicists, and farmers, and says you should then stress-test whether the plan fits your risk and income pattern.

Does German private health insurance cover you in the USA or while traveling abroad?

This article does not verify USA or travel-abroad coverage rules. Check the policy wording for travel scope, continuity limits outside Germany, authorization conditions, and exclusions for each provider, and treat anything missing as not verified.

Are your spouse or children covered under your policy?

Do not assume your spouse or children are covered just because you have a quote for yourself. The article says dependent coverage is not verified here and that you should request separate written confirmation and policy documents for each family member before deciding.

What is the difference between an insurance provider and a broker?

This article does not verify the legal duty differences between a provider and a broker. Use a practical check instead: confirm who issues the contract and who handles service after purchase, and save those details with your policy records.

Who can actually choose private insurance in Germany?

Not everyone can choose private insurance in Germany. The article says eligibility depends on your group and uses employment status as a first checkpoint, notes that people who are not eligible must enroll in public insurance, and says some international students, including those over 30 or in preparatory or language courses, may need private coverage instead of public coverage.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- eiopa.europa.eu/system/files/2020-03/methodological-principl...trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC8775800trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC12023567trusted

- sarahlawrence.edu/undergraduate/2025-2026-catalogue.pdftrusted

- ssa.gov/policy/docs/workingpapers/wp112.htmltrusted

- unc.edu/about/accessibility/well-said-transcripts-2trusted

- altmetric.comexternal

- convatecgroup.com/siteassets/convatec-ara-2024.pdfexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Freelance Crypto Payments That Protect Cashflow and Reduce Disputes

Crypto payments make sense only when they improve how reliably you get paid after you plan conversion, compliance, and recordkeeping up front. They can reduce friction in some international setups where traditional platforms add fees, restrictions, or extra steps. They also move risk onto conversion timing, exchange-fee exposure, and documentation quality, so use a simple acceptance test before you agree:

Can Digital Nomads Claim the Home Office Deduction?

Claim the deduction only when your facts and records can carry it. With the home office deduction for digital nomads, the real decision is usually a three-way call: claim it, do not claim it, or pause and get help because your file is not ready.

Choosing Between GKV and PKV as a Freelancer in Germany

Your health insurance choice is a business decision, not a paperwork task. As a freelancer in Germany, you're choosing between two legal and financial systems that affect monthly cash flow, family costs, and how easy or hard it will be to change course later.