Quick Answer

Build your setup in layers: keep personal spending in Monzo or Starling, run client payments through Wise Business or Revolut Business, and post records into Xero or FreeAgent. Use Open Banking aggregation only if sync quality improves your weekly review, and set one FX rule before invoices go out. Validate the stack with a live invoice cycle, a clean payment match, and a month-end export before you standardize it.

You Don't Need Another App List. You Need an Operating System.#

If you rely on client payments, one "best app" rarely solves the real problem. What you need is a financial system: a coordinated setup for your personal money, business cash flow, and compliance control.

| Your situation | What to use | Why |

|---|---|---|

| You are paid mainly in GBP, run most spending through one UK account, and admin is light | A single finance app dashboard can be enough | Apps like Emma or Snoop can aggregate accounts and cards, and Open Banking is a secure, regulated way to share data with trusted apps and services |

| You invoice across borders, hold multiple currencies, or split funds across several providers | A layered setup | A single app gives you visibility, but you also need tools to receive, hold, and move money, for example multi-currency workflows with Wise or Revolut Business |

Start simple, then add layers as complexity appears. Late payments and currency handling are operational risks, not minor annoyances. UK late payments are estimated to cost almost £11 billion per year, with around 14,000 business closures per year linked to late payment pressure.

If cash reliability matters, separate your personal layer from your payment-operations layer and check protection rules before you hold large balances. FSCS can cover eligible deposits up to £120,000 per eligible person, per bank, building society, or credit union after 30 November 2025. FCA guidance is also clear that FSCS protection does not apply to e-money accounts.

Treat compliance as a core layer, not year-end cleanup. If you are UK resident, foreign income is normally still in scope for UK tax. Self-employed records must be kept for at least 5 years after the 31 January deadline. From 6 April 2026, MTD for Income Tax starts for people with turnover above £50,000 from self-employment and property income.

This guide follows that structure. Layer 1 covers your UK personal foundation. Layer 2 covers business cash flow and cross-border payments. Layer 3 covers records and compliance checks that stop small admin gaps from turning into expensive problems. You might also find this useful: A Guide to Creating a Freelance 'Press' or 'Featured In' Page.

Layer 1: The Foundation - Mastering Your UK Personal Finances#

Keep this layer personal and practical. It is for your own UK cash clarity, not client payment operations. The easiest way to choose tools is by role, not brand. One personal hub, one visibility layer, and one reliable way to build reserves are usually enough.

Pick by role, not by brand#

Your personal setup does not need many moving parts, but each one should have a clear job.

| Role | Main job | Grounded detail |

|---|---|---|

| UK current account as your personal hub | Day-to-day spending control | Starling highlights instant payment notifications, Spending Insights, Spaces, and Bills Manager |

| Open Banking aggregator for cross-account visibility | See multiple banks and cards in one view | Emma positions itself around connected accounts, budgeting, and subscription tracking; Snoop says setup can be done in under 3 minutes |

| Savings automation for reserve-building | Create an automatic path from incoming money to savings | Prioritize reliable rules and easy pause and edit controls; you may not need a separate app if current account tools already cover bill separation and short-term buffers |

- UK current account as your personal hub

Use your personal current account for day-to-day spending control: fast alerts, clear spend visibility, and, where available, ring-fenced money for known bills. Starling highlights instant payment notifications, Spending Insights, Spaces, and Bills Manager that can hold bill money in a Regular Space and pay it on schedule. What matters most is simple: can you spot spend quickly and avoid bill surprises?

- Open Banking aggregator for cross-account visibility

Add this layer when you need to see multiple banks and cards in one view. Emma positions itself around connected accounts, budgeting, and subscription tracking. Snoop positions itself around multi-account visibility, spending and budget support, bill-cutting help, and says setup can be done in under 3 minutes. Prioritize regulated Open Banking access and expect re-consent cycles where applicable. Monzo, for example, says connected accounts use FCA-regulated Open Banking and require renewal every 90 days.

- Savings automation for reserve-building

Set up an automatic path from incoming money to savings so progress does not depend on willpower. If your current account tools already cover bill separation and short-term buffers, you may not need a separate app yet. If you add one, prioritize reliable rules and easy pause and edit controls over extra features. Consistency beats complexity here.

What to compare in practice#

Five things matter most here: budgeting depth, Open Banking coverage, rule automation, alert quality, and manual override controls. Those manual controls matter more than they seem to at first, because sometimes you need to correct categories or exclude items from spending totals.

| Tool | Daily spend control | Subscription tracking | Account aggregation | Setup friction |

|---|---|---|---|---|

| Monzo | Strong spend tracking with manual category exclusion controls | No specific sourced strength here | Yes, tied to Extra, Perks, or Max; Monzo says it supports most major UK banks | Can be higher if you need aggregation, since it sits on paid plans and renews every 90 days |

| Starling | Strong for alerts and bill separation, with instant notifications, Spending Insights, Spaces, and Bills Manager | No specific sourced strength here | Confirm with the relevant authority | Can be lower for core personal banking; Starling says you can apply online in minutes |

| Emma | Strong for budgeting across linked accounts | Yes, explicitly positioned for subscription tracking | Yes, positioned as an all-accounts dashboard | Requires linking accounts; no exact setup time provided here |

| Snoop | Strong for top-level spending and budget visibility | Not specifically sourced as a subscription tracker | Yes, connects bank accounts and credit cards in one place | Can be lower if speed matters; Snoop says setup is under 3 minutes |

Know the handoff point#

Layer 1 often stops being enough once you are invoicing clients, handling non-GBP payments, or needing business-grade records. Monzo states its personal current account is for personal payments, and GOV.UK says bank policy can vary, so you need to check your bank's rules.

That boundary matters because once business payments mix into your personal hub, your records can get weaker at exactly the point HMRC expects stronger ones. For self-employed work, you need records of all sales and income and all business expenses, kept for at least 5 years after the 31 January submission deadline. That is the handoff to Layer 2: invoicing, multi-currency handling, and business record workflows. Related: The Best Personal Finance Apps for Freelancers.

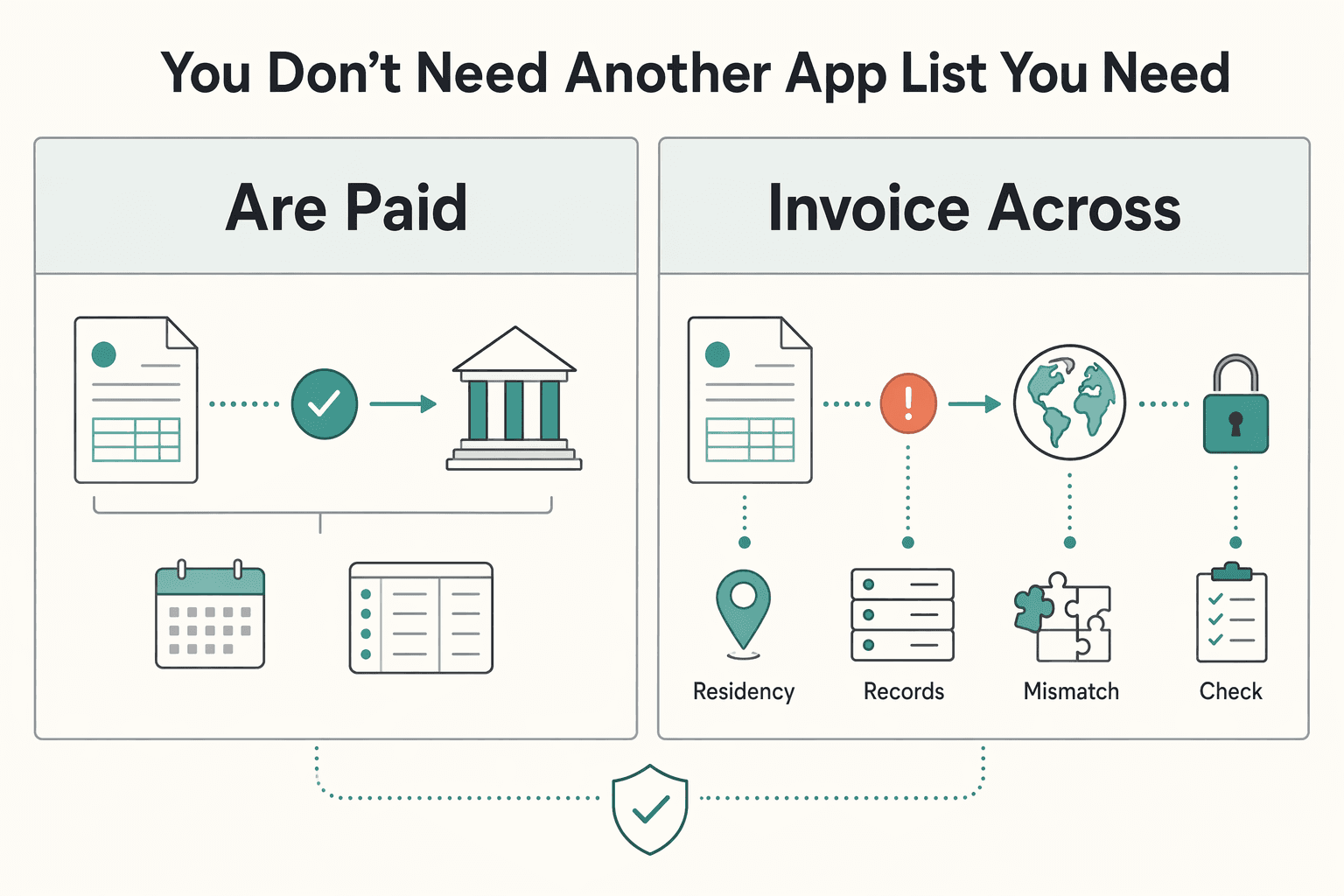

Layer 2: The Command Center - Managing Your Global Business Cash Flow#

Keep client payments out of your personal account and run a dedicated business payment layer instead. That can help protect margin, reduce avoidable fees, and make it easier for overseas clients to pay you correctly the first time.

1. Open a multi-currency business account, not another personal account#

Start with a multi-currency business account: one account structure that lets you hold and manage multiple currencies in one place. Wherever possible, use local receiving details, meaning the account details you share so clients can pay you through local rails.

This is where payment friction usually starts. Wise Business says it can hold 40+ currencies and provide receiving details for 8+ currencies. Wise Help says account details can be available in over 10 currencies depending on setup. Revolut Business says you can create many currency accounts with local and global account details, but published capacity appears as both 25+ and up to 30 currencies. Confirm your exact plan and region before rollout.

| Provider | Receiving options | Conversion controls | Payout reliability note | Invoicing and collection | Support note |

|---|---|---|---|---|---|

| Wise Business | Local receiving details for 8+ currencies on one page; help docs say over 10 currencies may be available depending on setup | Auto Conversions let you set a target rate and amount | Validate with a small test payment and check for route-specific deductions | No invoicing detail established here | Verify current support channels and response expectations on your plan |

| Revolut Business | Local and global account details; published support appears as 25+ or up to 30 currencies depending on page and plan | Limit and Stop orders for automated exchange; 0.6% fee above fair usage allowance and 1% weekend mark-up | SWIFT transfers may include intermediary and beneficiary bank fees | Invoice payments can be accepted by bank transfer, debit, credit, Apple Pay, Google Pay, and Revolut Pay across 35+ currencies | Verify current support channels and response expectations on your plan |

2. Collect through local rails first, and treat SWIFT as the fallback#

If a client can pay you like a domestic supplier, use that route first. Wise states local account details can be used so people can pay you like they would pay a local.

Two practical risk points are correspondent-bank fees and settlement timing. Correspondent-bank fees are charges taken by intermediary banks on SWIFT routes. Settlement timing is how quickly funds are credited based on the rail. Faster Payments is available 24/7/365, with stated limits up to £1 million. Bacs Direct Credit takes less than three days. CHAPS is a same-day sterling system during weekday operating hours.

Before you go live on any new corridor, run a low-value test payment. One failure mode is SWIFT being used for details intended for local collection, which can leave you paid short and make reconciliation harder.

3. Decide your conversion policy before you invoice#

Set your conversion rule before you send invoices so FX decisions stay consistent instead of becoming reactive. The FX spread is the difference between a dealer's buy and sell prices, and your practical cost is the rate shown to you plus any markup or usage fee.

The FCA expects firms to disclose the exchange rate that will be applied and the markup above a reference rate. For larger conversions, capture the quote screen. If most of your costs are in GBP, convert only what you need for near-term obligations and hold the rest in invoice currency. If you have predictable USD or EUR costs, keep part of those balances unconverted.

Pick one internal rule and stick to it: convert weekly, on receipt, or at a target rate. The key is to decide once, then apply it consistently.

4. Turn every invoice into a clear payment instruction#

Late payment problems often start with vague invoices. Use one invoice standard every time so people know exactly how to pay you.

| Invoice item | What to include | Grounded note |

|---|---|---|

| Required UK basics | Unique invoice number, your company name, address, and contact information | Included as required UK basics in this section |

| Client and service detail | Client name, service description, date of supply, total owed, and exact currency | Added to reduce disputes |

| Payment methods | Accepted payment methods clearly, including bank transfer and any integrated checkout options you offer | Use clear payment instructions every time |

| Due date | An exact due date on the invoice | If no payment date is agreed, UK guidance sets a default expectation of 30 days |

| Late-payment terms for B2B work | Your late-payment clause if you intend to enforce it | UK statutory guidance references 8% plus the Bank of England base rate for commercial debts |

Avoid vague payment text like "bank transfer preferred" without rail, currency, or due date. That wording can lead to late payment, short payment, and expensive routing.

For a step-by-step walkthrough, see The Best Personal Finance Apps for German Residents. Before you lock in your account setup, run your typical client-payment scenarios through the Payment Fee Comparison tool to see where conversion and transfer costs actually land.

Layer 3: The Compliance Shield - Eliminating Your Greatest Financial Anxieties#

Make compliance a monthly routine, not a year-end rescue. Your core control loops are straightforward: separate tax cash when revenue arrives, capture expense evidence at the point of spend, and keep your filing route ready before deadlines.

1. Tax segregation on receipt#

Move a set share of each incoming payment into a dedicated tax reserve the same day it lands. Set that share only after you verify it against your expected bill. This is a cash-control rule, not a legal-rate guess.

Keep that reserve separate from day-to-day operating money so you can see what is already committed. If you are newly self-employed, handle registration early. You must register as a sole trader if you earn more than £1,000 in a tax year, 6 April to 5 April. Late registration may lead to a penalty.

Then run one weekly check: reconcile what cleared that week against what moved into the reserve. After registering, HMRC also lets you set up monthly or weekly payments to help you budget for your bill.

2. Expense evidence capture at point of spend#

This is one of the easiest places to lose control. HMRC says you need records such as bank statements or receipts, so capture proof while each transaction is still fresh. Use this checklist every time:

- Capture the receipt as soon as you make the purchase.

- Tag the expense category immediately.

- Map it to the relevant project or client when that helps retrieval.

- Store a retrievable trail linking receipt, bank transaction, and accounting entry.

Project or client mapping is an internal control. It helps you explain expenses quickly and consistently.

3. Reporting readiness before deadlines#

Keep records and access ready so filing feels routine, not like detective work. These are the checkpoints to keep in view:

| Checkpoint | What to confirm |

|---|---|

| 5 October | Tell HMRC by this date if you need to complete a tax return for the previous year. |

| 6 April | Earliest point to file an online return after the tax year ends. |

| 31 January | Tax bill payment deadline. |

| UTR | Needed to use the online filing service. |

If you already had a Self Assessment account, reactivate it properly before filing to reduce delay risk.

4. Cross-border obligations need alerts, not memory#

If your affairs cross borders, do not rely on memory. Track obligations as monitored triggers, and for each regime record the live trigger once it is confirmed.

Use a simple decision rule: if normal activity could move you near a trigger, set an alert before you get there. Also confirm the filing route early, because the standard online Self Assessment service is not available in every case, including if you lived abroad as a non-resident. In those cases, HMRC directs users to commercial software or other forms.

5. Run the monthly auditor test#

At month-end, run one blunt test: can you produce clean income, expense, and tax-reserve records quickly, without manual reconstruction? If not, fix the broken loop that month. Do not wait for deadline pressure to find out your records only work while you can still remember the story.

If you want a deeper dive, read Understanding the UK's Statutory Residence Test (SRT).

The CEO's Dashboard: Unifying Your Financial Tech Stack#

Once the tax and record-keeping loops are stable, visibility becomes the next bottleneck. This is a gap many app roundups miss. You do not need another silo. You need one screen you trust first.

Start with the right definition#

A dashboard is a central homepage that gives you a snapshot of the finance items you act on, such as account balances, invoices owed, and bills. A single source of truth does not mean one app replaces every specialist tool. In practice, it means one screen you check first because it consolidates your current financial position well enough to make a decision without opening several more tabs.

Open Banking can support this, with limits. An Account Information Service Provider (AISP) can show data from your selected accounts in one place and analyse spending, and a Payment Initiation Service Provider (PISP) can initiate bank payments directly. Both require your explicit consent. These connections do not guarantee full UK coverage or immediate sync every time. Only the UK's nine largest banks and building societies are required to provide data through Open Banking, imports can lag online banking, and some aggregator feeds need manual refresh.

Run these four weekly checks#

A useful dashboard layer should sit on top of your Monzo, Wise, and Xero-style stack and answer the same questions every week.

| Weekly check | What your dashboard should show | Why it matters |

|---|---|---|

| Profitability check | Income, tagged expenses, and a clear monthly view to spot patterns | Supports regular reconciliation and helps you spot monthly profitability patterns, not just top-line revenue |

| Cash-position check | Current balances plus outstanding and overdue invoices and payments | Gives you a clearer go or no-go signal on spend, hiring, or a new software subscription |

| Tax set-aside visibility | Reserve balance and whether reserve transfers happened after receipts landed | Helps reduce the risk of spending money you may need for tax and makes month-end checks easier |

| Compliance monitoring | Alerts for VAT registration if taxable turnover goes above £90,000, optional VAT cancellation if it falls below £88,000, MTD for Income Tax from 6 April 2026 if qualifying self-employment and property income is over £50,000, and Self Assessment payments on account due 31 January and 31 July | Helps you track key thresholds and deadlines before they become urgent |

If you also have another trigger to monitor, add a custom alert at the confirmed threshold rather than relying on memory.

Choose the layer with five tests#

Before any dashboard becomes your first screen, put it through five tests:

| Test | What to confirm | Grounded note |

|---|---|---|

| Connection reliability | How feeds behave when data is late | Red flag: you only notice missing transactions during reconciliation |

| Category and tag consistency | One week of exports from start to finish | If those fields do not carry through, reporting drifts quickly |

| Alert quality | Alerts point to a decision or deadline | Not just activity noise |

| Reporting clarity | Balances on one page and monthly reports you can drill into | If you still need multiple logins to answer a basic cash question, the layer is not doing its job |

| Export and audit trail quality | You can export records and review an audit trail or audit log showing who changed what and when | This is your fallback when categorisation is wrong or evidence is requested |

Verify provider status and scope before you connect#

Before you connect anything, check that the provider is authorised or registered on the FCA Financial Services Register. If you use an unauthorised firm, complaint and compensation protections may not apply. Also check scope. Wise statements include transactions made through Wise currency accounts, so activity done through external payment methods may not appear in your dashboard.

That is the practical standard for a unifying layer: stronger support for reconciliation, deadline tracking, month-end review, and clearer spend decisions. We covered this in detail in The Best Personal Finance Apps for Australians.

Conclusion: From App Juggling to True Financial Autonomy#

A good setup reduces manual handoffs and helps you catch problems early. Instead of looking for one "best" app, build a connected stack that matches your payment routes, reconciliation process, and compliance checkpoints.

- Personal cash clarity

Use a personal banking layer you will actually review weekly, and add an aggregator only if it genuinely improves visibility. The real test is practical: can you check spending, reserves, and upcoming bills quickly without manual exports or heavy recategorization? If sync status is unclear or categories drift, your review loop is weaker, not stronger.

- Business cash flow control

Choose a business layer based on how you get paid, not on feature count. For mostly domestic flows, a business account plus accounting software may be enough. For multi-currency work, test tools that support those routes without adding manual reconciliation steps. Keep tools only if one live invoice, one payment match, and one month-end export flow cleanly into your accounting records and exposes errors fast.

- Compliance visibility

Your stack should make registration, record-keeping, filing readiness, and payment deadlines easy to track. If you earn more than £1,000 in a tax year, check whether you need to register as a sole trader. If you need to complete a return, HMRC says you must tell them by 5 October for the previous tax year. Keep your UTR, statements, and receipts organized, reactivate an existing Self Assessment account if required, and if you are filing for the first time, register for Self Assessment before using the online filing service. File online on or after 6 April if your case is eligible for that service, and plan for payment by 31 January.

Apply this next:

- Pick one tool per layer and define the exact weekly and month-end checks it must support.

- Run one real month and save an evidence pack: statements, receipts, exports, and filing notes.

- Keep only the tools that improve review speed, reconciliation quality, and compliance visibility.

This pairs well with our guide on The Best Personal Finance Apps for Canadians.

If you want to turn this app stack into one operational flow for invoicing, collection, and payout tracking with audit-ready records where supported, review Merchant of Record for freelancers.

Frequently Asked Questions

What is the best finance app for UK freelancers with international clients?

If you invoice overseas clients, the core need is reliable currency handling and clean records. In practice, use a multi-currency business account, one account that lets you manage several currencies in one place, plus Xero or FreeAgent for accounting. Wise Business can be a fit if holding currencies matters, but validate with one live invoice, one refund, and one month-end export before you standardize on it.

How can you manage multi-currency income as a UK resident?

The key is to control conversion timing instead of reacting to each payment. A natural hedge means matching inflows and outflows in the same currency in your normal workflow, so you convert less often. This can reduce FX pressure, but it does not remove FX risk, so keep a clear plan for what still must be converted into GBP for UK obligations.

Are there UK finance apps that help with Self Assessment tax?

If your main problem is tax discipline rather than filing alone, start with cash separation. A tax pot or space is a ring-fenced sub-balance inside your account, so Monzo Pots and Starling Spaces can help you separate future tax cash from spending cash, but they are not formal escrow accounts. For records and submissions, FreeAgent is positioned as HMRC-recognised for MTD for Income Tax and can file MTD for VAT directly to HMRC, and an MTD-compatible workflow means keeping and correcting digital records of self-employment or property income and expenses.

What is the right finance app setup for a US expat in the UK?

When your biggest risk is missing a reporting trigger, build around monitoring and evidence. Keep one account view as your compliance monitor, track aggregate non-US balances against the current filing threshold; current filing threshold pending official/source/adviser verification. Save monthly statements and exports as your evidence trail. Then run a simple routine: monthly balance check, calendar reminders for annual filing windows, and consistent record retention.

Is Monzo or Revolut better for managing finances in the UK?

Pick Monzo when your workflow is mostly GBP and you want strong spending separation plus a simple reserve habit. Pick Revolut when the decision depends more on currency handling and account-level invoicing flow, since Revolut Business supports invoice creation inside the account. In either case, compare account structure, authorised-firm status, and protection terms before you decide.

Do you need an aggregation app like Emma or Snoop if you already have a bank and accounting software?

Use one when visibility across accounts, cards, and subscriptions is the real bottleneck. Emma focuses on account connections, budgets, categories, bills, and subscriptions, and both Emma and Snoop describe broad UK bank coverage, while Snoop also states it is FCA-registered. The deciding factor is feed quality in your setup. If sync timing or category carryover is weak, your reconciliation workload can get worse, not better.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- bis.org/publ/qtrpdf/r_qt1612c.pdftrusted

- bsaefiling.fincen.gov/file/fbartrusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- makingtaxdigital.campaign.gov.uk/mtd-for-income-tax-datestrusted

- smallbusinesscommissioner.gov.uk/late-payments-research-2trusted

- wise.com/us/business/multi-currency-bankingtrusted

- emma-app.comexternal

- fca.org.uk/firms/open-banking-open-financeexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Understanding the UK's Statutory Residence Test (SRT)

Treat SRT like ops, not folklore. You want a repeatable workflow you can run monthly so your tax-year answer is boring, documented, and easy to defend.

The Best Personal Finance Apps for Freelancers

If you are choosing among the best personal finance apps freelancers can use, start with payment risk, not popularity. The goal is simple: keep cash flow visible enough to act early when income slows or bills stay fixed.

Build a Freelance Press Page Clients Can Verify

Your freelance press page should do two jobs at once: help prospects assess your credibility quickly, and keep weak, inflated, or poorly sourced claims off your site. Treat it as a short evidence archive on your website, not a brag wall.