Quick Answer

Build around a three-tier setup: Foundation for one dedicated intake account, Command Center for allocation buckets, and Compliance Shield for filing and record controls. Keep invoicing fields compliant under §14 UStG, and treat aggregation apps as visibility tools rather than compliance engines. For cross-border accounts, maintain a live log and run FBAR checks as a separate task. This structure turns app selection into a weekly operating routine you can verify.

Tier 1: The Foundation - Why Your German Bank Account is Just the Starting Point#

Start with a consistent money-intake layer, then build the rest of the stack around how you actually work, not brand claims. This tier is about reliable intake and review. Allocation and compliance controls come later.

Searching for the best personal finance apps germany can surface options, but it does not solve the core setup. The first question is whether you can verify activity and work from one reliable record without friction.

1. Separate the money stream#

Set one consistent stream for client payments and business spending records, separate from day-to-day personal activity where practical. That separation gives you one intake point you can test, reconcile, and trust before you add more tools.

2. Compare accounts by operating fit, not branding#

Choose by operating fit. This is where small differences turn into daily friction. If you compare each option against the same criteria, you will learn more than from marketing pages. In one budgeting-tools survey, even after 8 options were predefined, 34.7% selected "Other." That is a useful reminder not to copy someone else's setup by default.

| Selection point | What to verify yourself | Red flag |

|---|---|---|

| Personal fit | Does this workflow match how you actually manage money? | It works in theory, but not in your day-to-day routine. |

| Fast transaction entry | Can you log routine transactions quickly enough to stay consistent? | Entry is slow enough that updates get skipped. |

| Statement sync | Can you reliably import/sync bank and card statements? | Sync or import repeatedly fails. |

| At-a-glance review | Can you review accounts and current status quickly in one place? | You cannot get a clear snapshot without extra digging. |

| Side-by-side comparison | Have you tested options against the same checklist? | The choice is based mostly on branding. |

3. Test the review layer early#

Treat any aggregation promise as a practical test, not a feature win. Test whether your setup can pull balances and transactions into one review view.

A good early checkpoint is whether your setup supports three basics without friction: fast transaction entry, statement sync, and at-a-glance account review.

4. Know what this tier cannot do#

A clean account setup is not a spending plan. One of the quickest ways to run out of money is to have no plan for spending.

So keep Tier 1 in its lane. It handles intake and storage. The next tier is where you decide what the money is for.

If you want a deeper dive, read Can Digital Nomads Claim the Home Office Deduction?.

Tier 2: The Command Center - Separating Business Revenue from Personal Reality#

Once your intake account works, stop treating the full visible balance as automatically spendable. Use a simple bucket or label system so business and personal decisions are not driven by one misleading number.

App searches can surface options, but market noise makes it hard to tell what is actually useful. Whether you track manually or with automation, set one clear review rule before you spend.

1. Allocate with a consistent check, not ad hoc#

Classify incoming money before day-to-day spending begins. Exact percentages and country-specific tax allocations are outside this section's scope and depend on your setup and local rules.

When a payment arrives, record it at your chosen checkpoint (immediately or on a fixed schedule). Consistency matters more than adding more tools.

| Bucket | Purpose | Trigger event | Common mistake to avoid |

|---|---|---|---|

| Profit or buffer | Keep a planned portion outside day-to-day operations | Each incoming payment or scheduled allocation day | Treating this as leftover instead of a planned hold |

| Owner pay | Personal draw or salary-equivalent transfer | Scheduled transfer to personal account | Paying personal expenses directly from the business account |

| Obligations hold (if applicable) | Set aside money for obligations that may come due under local rules | Each allocation cycle | Spending from this hold during a tight month and not restoring it |

| Operating costs | Pay subscriptions, contractors, software, overhead | Fund after core holds are set | Letting this bucket absorb every extra spend request |

Use a clear spend rule: personal spending comes from owner pay, business bills come from operating costs, and held buckets stay untouched until due.

2. Use working labels so the balance stops lying to you#

If you want faster decisions, label money in a way that matches your workflow. Treat labels such as "gross," "reserve," or "available" as internal planning terms, not legal or accounting definitions.

That matters more than feature lists. A high visible balance is not a spending signal if part of that money is already assigned in your plan.

After each review, you should be able to answer two questions quickly:

- How much is safe for operating spend right now?

- How much can move to personal use without touching held obligations?

If you cannot answer both quickly, tighten your command center.

3. Give each tool one job#

Too many tools create noise, not control. Give each tool one job, then judge it by whether it helps you verify balances and decide what to keep or skip.

| Layer | Job |

|---|---|

| Bank app or banking layer | Check balances and confirm current account positions |

| Tracking layer (manual or automated) | Record how incoming money is classified |

| Additional apps | Keep them only if they are clearly useful; skip them if they add noise |

If a tool looks polished but does not improve clarity, it creates work later.

4. Choose your review style, but keep the evidence pack#

Manual tracking and automation can both work. The deciding factor is whether your review layer lets you verify balances quickly and keep records clear.

Before committing to any app stack, run one live-payment test. Confirm the payment posts clearly and your updated balances still match reality. If that test is messy, skip the tool.

This tier gives each euro a job. The next one is about making sure your records, deadlines, and exceptions do not turn into avoidable risk. Related: The Best Personal Finance Apps for Freelancers.

Tier 3: The Compliance Shield - Protecting Yourself from Catastrophic Risk#

The goal here is straightforward: prevent filing misses, reduce audit friction, and avoid preventable penalties. Keep using apps for visibility, but do not mistake visibility for compliance. For every cross-border risk, assign a required record, a calendar trigger, and a specialist handoff point.

| Risk area | Recurring task | Required records | Tool owner | Failure mode if skipped |

|---|---|---|---|---|

| Cross-border reporting | Monthly account log + annual filing check | Account inventory, statements, filing notes, confirmation receipts | Spreadsheet + bank app | Filing trigger missed, late filing, incomplete filing |

| Advisor-ready documentation | Quarterly export + folder cleanup | Invoices, receipts, bank exports, reconciliation notes, open-questions log | Invoicing tool + bank app | Advisor reconstructs history, slower responses to reviews |

| Multi-currency tax planning | Per-payment FX capture + reserve transfer | Payment record, FX source, EUR conversion, reserve proof | Spreadsheet + bank app | Reserve looks adequate in foreign currency but falls short in EUR |

| PE exposure | Monthly country activity review | Contracts, travel/work-location log, invoicing trail | Spreadsheet + invoicing tool | Foreign tax exposure identified only after revenue is booked |

1. Cross-border reporting#

Treat cross-border reporting as a live tracking job, not a year-end scramble. It covers filing duties created by cross-jurisdiction accounts or activity. For U.S. persons, FBAR (FinCEN Form 114) is an annual report filed with FinCEN (not the IRS), and Form 8938 is separate and does not replace it.

| Control point | What to do |

|---|---|

| Account inventory | Keep a live inventory of every relevant non-domestic account |

| Event-based updates | If aggregate foreign account values could exceed $10,000 at any time in the year, switch to updates for new accounts, large transfers, or balance spikes |

| FBAR filing check | Run a filing check against the April 15 due date and automatic October 15 extension |

| Account information service or PSD2 third-party feed | Treat it as monitoring only; access depends on your express permission |

| Germany-based payment-services entity | Verify it in BaFin's daily updated register before relying on it |

Keep a live inventory of every relevant non-domestic account. If aggregate foreign account values could exceed $10,000 at any time in the year, switch to event-based updates for new accounts, large transfers, or balance spikes. Then run a filing check against the April 15 due date and automatic October 15 extension.

If filing is required and missed, consequences can include civil and criminal exposure. If you use an account information service or a PSD2 third-party feed, treat it as monitoring only; access depends on your express permission. Verify any Germany-based payment-services entity in BaFin's daily updated register before relying on it.

2. Advisor-ready documentation#

Your tax advisor should get a structured packet, not raw transaction noise. A Steuerberater is a regulated German tax advisor. The standard to aim for is traceability: each material bank line should map cleanly to an invoice or receipt.

| Record or step | What to keep or do |

|---|---|

| Bank data export | Export bank data as part of the quarterly routine |

| Invoice export | Export invoices as part of the quarterly routine |

| Dated folder | File both exports in a dated folder |

| Open-questions log | Keep a short open-questions log for unclear items |

| Receipts | Retain receipts with business-purpose notes |

| Correction notes | Keep correction notes where invoice amounts changed |

| OSS records | Keep them for 10 years and make them electronically available without delay on request |

| Invoice retention under UStG §14b(1) | BMF guidance states it was shortened from 10 years to 8 years |

Run a quarterly routine: export bank data, export invoices, file both in a dated folder, and keep a short open-questions log for unclear items. Retain receipts with business-purpose notes, and keep correction notes where invoice amounts changed.

Be explicit about retention scope. OSS records must be kept for 10 years and be electronically available without delay on request. BMF guidance states invoice retention under UStG §14b(1) was shortened from 10 years to 8 years. Handoff point: any mixed personal and business charges, missing receipts, or unexplained internal transfers go to your advisor immediately.

3. Multi-currency tax planning#

If you get paid in foreign currency, the control is not the app. It is whether you convert that inflow into a EUR tax reserve you can actually pay from. The rule is consistency: one approved rate source, one method, every time.

For each foreign-currency payment, record the amount, date, FX source, EUR equivalent, and reserve transfer evidence. The U.S. Treasury Fiscal Data tool explicitly notes FBAR use. For other filings, confirm your advisor's preferred source and timing method, then apply it consistently.

Document any buffer policy so your rule is repeatable. Handoff point: when FX swings start changing prepayment planning or cash availability, escalate to your tax advisor.

4. PE exposure#

Permanent establishment risk is where self-service often stops being enough. PE is a treaty concept: a fixed place of business through which business is carried on, and it can create tax exposure in another country.

Maintain a monthly country activity log showing where you worked, for which client, under which contract, and whether a recurring local presence existed. If activity moves toward a stronger local presence, longer duration, or greater economic substance, escalate before renewal or expansion.

EU materials note that SMEs can become taxable in more than one EU country once foreign activity creates a PE. Handoff point: repeated on-site work, fixed local workspace patterns, or contract terms indicating deeper local activity should be reviewed by a tax advisor or legal specialist.

For a step-by-step walkthrough, see The Best Personal Finance Apps for UK Residents.

Before you send a cross-border invoice, sanity-check the VAT treatment so your compliance process stays consistent: Use the VAT reverse-charge checker.

Ground-Level Execution: Your Questions Answered#

A single app is not enough. What works better is a stack with clear roles: one layer for money movement, one for visibility, one for invoicing, and one manual tracker for deadlines and exceptions.

| Your situation | Bank layer | Aggregation layer | Invoicing layer | Manual compliance layer |

|---|---|---|---|---|

| German freelancer, mostly domestic clients | Dedicated business account; use subaccounts if helpful (N26 states up to 10 additional Spaces) | Optional, for cash visibility | Tool that supports domestic B2B E-Rechnung workflows (structured electronic format) | VAT deadline calendar, receipt folder, quarterly export checklist |

| EU B2B clients | Dedicated account with clear client-payment tagging | Useful when you operate across multiple accounts | Tool with separate fields for Steuernummer and USt-IdNr. | VAT treatment notes, client-country log, advisor handoff list |

| Cross-border or higher-risk setup | Business-only account flow | Monitoring only, not compliance | Same invoicing controls as above | Account inventory, filing deadline tracker, exception log |

Do I need a separate business account if I am a Freiberufler?#

The sources here do not state a blanket legal requirement for a separate account, but using one as your default control step is practical. Freiberufler is a tax category under §18 EStG, so first confirm your activity classification, then route client income through one dedicated business account. Report your freelance start to the Finanzamt within one month, complete tax registration, and then build invoicing processes after your Steuernummer is assigned.

How should you handle VAT and e-invoicing in 2026?#

Start with a calendar-first process. If you are newly founded and not treated as Kleinunternehmer, plan for monthly authenticated electronic VAT pre-filings at the beginning and apply the 10th-day rule for due dates.

For domestic B2B, e-invoicing is generally mandatory from 1 January 2025, with transition rules. A valid E-Rechnung is structured electronic data rather than only a PDF. Next action: verify whether the §19 UStG thresholds (25.000 EUR and 100.000 EUR) apply to you and use an invoicing tool that can produce compliant structured output. When to escalate: if you are unsure about cross-border VAT treatment, hand it to your tax advisor before issuing invoices.

What is the difference between Steuernummer and USt-IdNr.?#

They are different identifiers with different jobs. Your Steuernummer is assigned by your local Finanzamt after tax registration, while your USt-IdNr. is a separate VAT identifier used for VAT-facing EU internal-market processes. Next action: keep both in separate fields in your invoicing setup and test one invoice template before sending any live invoice.

Can a budgeting or aggregation app replace compliance work?#

No. Use aggregation for visibility, not as a compliance engine. For example, Outbank states support for 4,500+ banks/providers, but monitoring coverage does not make invoices legally compliant or complete your filing duties. If you connect via a Kontoinformationsdienst, verify BaFin registration and plan for strong customer authentication with at least two factors. When to escalate: if your tracker shows unresolved exceptions, missing docs, unclear VAT treatment, or unusual transfers, send those items to your tax advisor immediately.

You might also find this useful: A Guide to Creating a Freelance 'Press' or 'Featured In' Page.

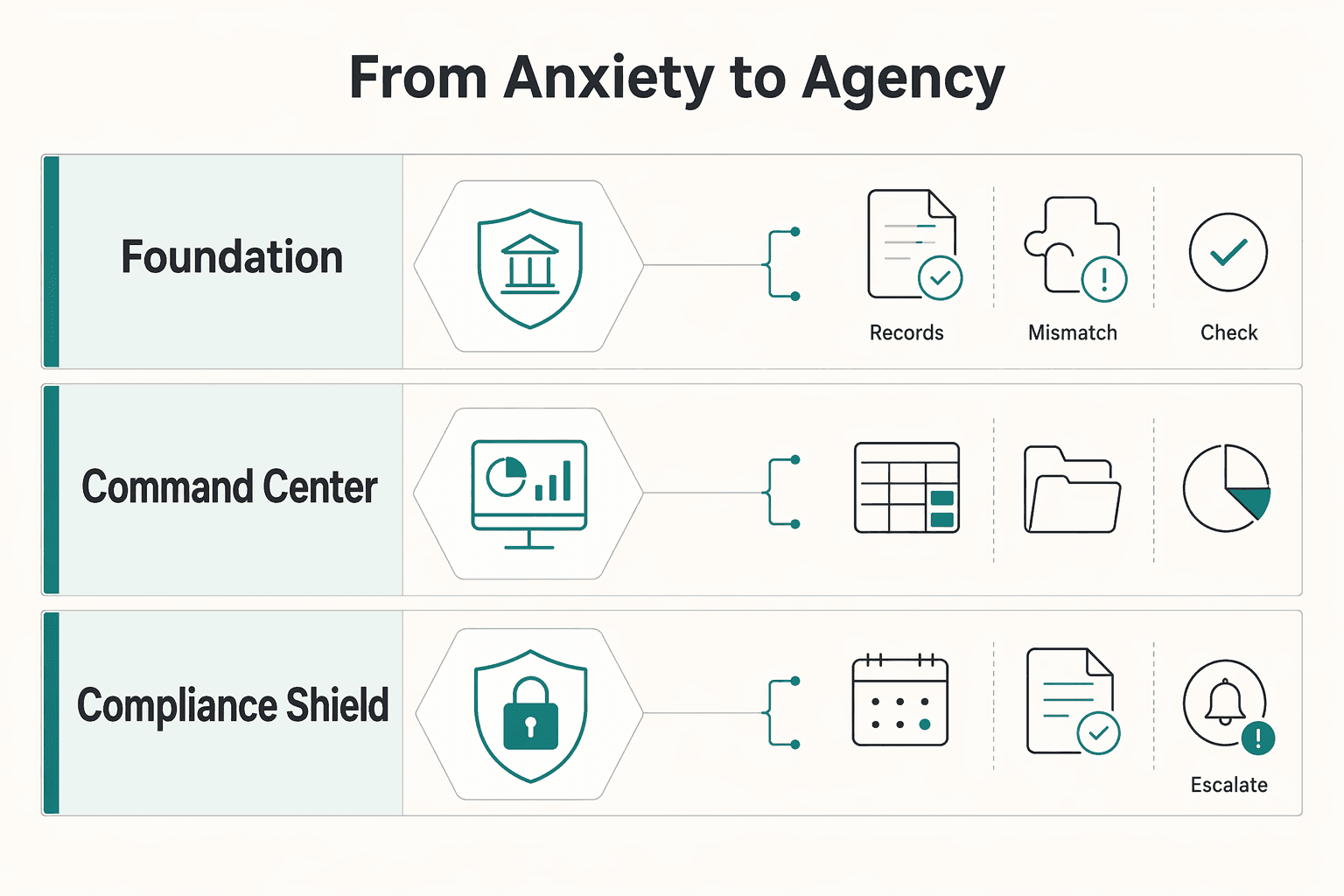

Your Financial OS: From Anxiety to Agency#

Use these three tiers as a practical operating model with clear boundaries. One tier handles where money lands, one handles how you assign it, and one handles the checks that keep small issues from becoming expensive ones.

| Tier | What you do each week | What it does not include | Main risk it controls | When this tier is working | Failure signal |

|---|---|---|---|---|---|

| Foundation | Route client payments into one dedicated intake account and reconcile inflows. | It does not decide allocations or complete compliance tasks. | Blurred money flow and poor payment visibility. | Payments arrive in one place and are easier to match to invoices. | Payments land in multiple places or reconciliation is inconsistent. |

| Command Center | Apply your allocation rules for owner pay, reserve buckets, and operating spend. | It does not make invoices compliant or close filing obligations. | Spending funds that should be reserved. | You can state what is safe to spend before spending it. | Reported balance looks fine, but planned obligations are underfunded. |

| Compliance Shield | Run document checks, deadline tracking, and exception review on a fixed cadence. | It is not "automatic" just because tools sync data. | Missed requirements and unresolved exceptions. | Required records are current and open exceptions are visible. | Missing records, unclear invoice fields, or exceptions carrying over week to week. |

Foundation. This is your intake layer. Check that client payments arrive in your dedicated intake account and match cleanly. If intake is fragmented, fix that before tuning anything else.

Command Center. This is your allocation layer. Use it to assign jobs to money, not just observe balances. A dashboard can help with visibility, but your rules are what create control.

Compliance Shield. This is your control layer. Keep one routine for records, deadlines, and exceptions, and treat unresolved items as active risk. If review steps are skipped, risk can accumulate even when cashflow looks stable.

Implement in this order: set account structure, define allocation rules, then lock a recurring compliance routine. That sequence can give you clearer cash decisions first and fewer preventable surprises later. For a related comparison, see The Best Personal Finance Apps for Australians.

If you want your invoicing, payment collection, and payout flow in one operational setup, review what Gruv offers for independent professionals: Explore freelancer workflows.

Frequently Asked Questions

Do I need a separate business account if I am a Freiberufler?

The sources here do not state a blanket legal requirement for a separate account, but using one as your default control step is practical. Freiberufler is a tax category under §18 EStG, so first confirm your activity classification, then route client income through one dedicated business account. Report your freelance start to the Finanzamt within one month, complete tax registration, and then build invoicing processes after your Steuernummer is assigned.

How should you handle VAT and e-invoicing in 2026?

Start with a calendar-first process. If you are newly founded and not treated as Kleinunternehmer, plan for monthly authenticated electronic VAT pre-filings at the beginning and apply the 10th-day rule for due dates. For domestic B2B, e-invoicing is generally mandatory from 1 January 2025, with transition rules. A valid E-Rechnung is structured electronic data rather than only a PDF. Next action: verify whether the §19 UStG thresholds (25.000 EUR and 100.000 EUR) apply to you and use an invoicing tool that can produce compliant structured output. When to escalate: if you are unsure about cross-border VAT treatment, hand it to your tax advisor before issuing invoices.

What is the difference between Steuernummer and USt-IdNr.?

They are different identifiers with different jobs. Your Steuernummer is assigned by your local Finanzamt after tax registration, while your USt-IdNr. is a separate VAT identifier used for VAT-facing EU internal-market processes. Next action: keep both in separate fields in your invoicing setup and test one invoice template before sending any live invoice.

Can a budgeting or aggregation app replace compliance work?

No. Use aggregation for visibility, not as a compliance engine. For example, Outbank states support for 4,500+ banks/providers, but monitoring coverage does not make invoices legally compliant or complete your filing duties. If you connect via a Kontoinformationsdienst, verify BaFin registration and plan for strong customer authentication with at least two factors. When to escalate: if your tracker shows unresolved exceptions, missing docs, unclear VAT treatment, or unusual transfers, send those items to your tax advisor immediately. You might also find this useful: A Guide to Creating a Freelance 'Press' or 'Featured In' Page.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- europa.eu/youreurope/business/taxation/vat/one-stop-sh...trusted

- fiscaldata.treasury.gov/currency-exchange-rates-convertertrusted

- gsa.gov/reference/geographic-locator-codestrusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- irs.gov/businesses/comparison-of-form-8938-and-fbar-...trusted

- jud.ct.gov/LegalResources/Docs/LJDocs/CTReports/FullVol...trusted

- oag.maryland.gov/resources-info/Pages/security-breach-notices...trusted

- oecd.org/content/dam/oecd/en/publications/reports/201...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Can Digital Nomads Claim the Home Office Deduction?

Claim the deduction only when your facts and records can carry it. With the home office deduction for digital nomads, the real decision is usually a three-way call: claim it, do not claim it, or pause and get help because your file is not ready.

The Best Personal Finance Apps for Freelancers

If you are choosing among the best personal finance apps freelancers can use, start with payment risk, not popularity. The goal is simple: keep cash flow visible enough to act early when income slows or bills stay fixed.

Build a Freelance Press Page Clients Can Verify

Your freelance press page should do two jobs at once: help prospects assess your credibility quickly, and keep weak, inflated, or poorly sourced claims off your site. Treat it as a short evidence archive on your website, not a brag wall.