Quick Answer

Start by choosing your contribution route before choosing a provider. For best pension providers for uk freelancers, the article’s core advice is to match structure, cashflow pattern, and admin capacity: limited company directors typically test employer contributions first, while personal routes rely on provider relief handling and clear recordkeeping. Then shortlist Vanguard, PensionBee, and AJ Bell only after verifying live fees, contribution options, and statement exports. Use a percentage-of-invoice funding rule if income is irregular, and validate allowance and carry-forward position before larger payments.

Why Your Pension is Your Most Powerful Business Asset (Not Just a Retirement Pot)#

Your pension is not just a retirement pot. If you are comparing pension providers for UK freelancers, start with a simpler point. A pension can reduce tax drag now, compound over time, and keep part of your wealth away from the day-to-day cash risks of self-employment.

| Area | Grounded point | Constraint |

|---|---|---|

| Immediate tax efficiency | Limited company employer contributions may be deductible when they are incurred wholly and exclusively for the trade; personal contributions can use relief at source | The provider usually claims 20% basic-rate relief and adds it to the pension; confirm the current relief mechanics before acting |

| Long-term compounding | Pension money is invested and can compound over time | Growth is not guaranteed; the normal minimum pension age is 57 after 5 April 2028 unless protected; the standard annual allowance is £60,000 with carry forward from the previous 3 tax years |

| Risk separation from business cash | Approved pension rights are generally excluded from a bankrupt estate | That protection is not absolute; courts can review excessive contributions; confirm the scheme is registered and keep clean records |

- Immediate tax efficiency

The route matters more than the product name. If you run a limited company, employer contributions may be deductible when they are incurred wholly and exclusively for the trade, so that is often a first route to test. If you are a sole trader, or you are making personal contributions, relief at source means the provider usually claims 20% basic-rate relief and adds it to the pension. Confirm the current relief mechanics before acting. What often matters most here is your business structure, not your investment preference.

- Long-term compounding, with real constraints

Pension money is invested, which means it can go up or down. That is the point, but it also means growth is not guaranteed and the money is not there for next quarter's VAT bill. For many savers, the normal minimum pension age is 57 after 5 April 2028 unless protected. The standard annual allowance is £60,000, and it includes payments made by you and by an employer. Unused allowance may be carried forward from the previous 3 tax years. The trade-off is simple: strong for future wealth, weak for short-term liquidity.

- Risk separation from business cash

Under UK rules, approved pension rights are generally excluded from a bankrupt estate, which is why pensions can help separate long-term savings from business risk. That protection is not absolute. Courts can review excessive contributions that unfairly prejudice creditors, so check the current legal position before relying on it. Before you pay in, confirm the scheme is registered, because if it is not, you will not get tax relief. Keep clean records showing who paid, when, and by which route.

Before the next section, do a quick self-check:

- Business structure: Are you a sole trader or a limited company director?

- Cashflow stability: Can you fund contributions without starving working capital?

- Contribution method: Should the payment come from the company or from you personally?

- Allowance headroom: Are you still within your annual allowance and any carry-forward room?

The Critical Decision: Sole Trader or Limited Company Director?#

Before you compare providers, decide your contribution route first. Your structure changes who pays, when cash leaves, and what records you and your accountant need to keep clean.

1. Sole trader route#

Treat this as a personal-execution path unless you have verified a different treatment for your case. In the available sources, a sole trader is a one-owner structure, and that owner carries the responsibility for their own super obligations and any workers they employ.

Keep the workflow simple and explicit:

- You decide the contribution amount and payment timing.

- The provider processes the contribution under its standard setup.

- You and your accountant confirm what still needs to be handled in your filing.

Current relief mechanics must be verified from official HMRC guidance, provider documents, or adviser records before use.

2. Limited company route#

Keep these two flows separate:

- Company pays pension directly (employer route).

- Company pays you first, then you contribute personally (personal route after extraction).

Those are different execution paths and should be tracked as different records from day one. If you blur them, reconciliation gets harder later.

Current HMRC allowability conditions must be verified from official HMRC guidance or adviser records before company money leaves the account.

| Route | Cashflow timing | Bookkeeping complexity | Who executes key steps | Verify first |

|---|---|---|---|---|

| Sole trader personal contribution | Personal cash reduces when you pay | Low to medium | You, provider, accountant (as needed) | Current relief mechanics pending official HMRC and provider verification |

| Limited company direct contribution | Company cash reduces when company pays | Medium | You, provider, accountant, company books | Current HMRC allowability conditions pending official HMRC or adviser verification |

| Limited company personal contribution after extraction | Two-step cash movement (company to you, then you to pension) | Medium to high | You, payroll/dividend process, provider, accountant | Classification and record trail stay separate from employer payments |

3. Decide with practical filters, not a single rule#

Use four filters: profit consistency, intended contribution size, your admin tolerance, and accountant support. If those point to a simple personal path, keep it simple. If they support disciplined company-led execution, evaluate that route in detail.

Any current threshold that affects this decision must be verified from official HMRC guidance or adviser records before you use it to size a contribution.

Once you choose the structure, you can optimize contribution mix and execution cadence in the next section.

The CEO's Playbook: Maximising Tax Efficiency for Limited Companies#

If your limited company is funding your pension, run pay decisions as a compliance flow: set salary for payroll, use dividends for personal cash, and use employer pension contributions for surplus profit you want in long-term savings. Test the pension route first only when deductibility, allowance exposure, and records are all clear.

1. Use the three-part pay mix in a practical order#

- Salary: cover payroll position first

Use salary for regular taxable pay and payroll compliance. If you pay yourself salary as a director, you must register as an employer even if you are the only director or employee, and wages require Income Tax and National Insurance deductions. Confirm current allowance and rate details from official HMRC guidance or payroll adviser records before using figures in a pay plan.

- Dividends: extract personal cash after company tax

Use dividends for spendable money, not for company tax deduction. Dividends are not deductible for Corporation Tax, so this route helps cash extraction but does not reduce taxable profits. Confirm current allowance and rate details from official HMRC guidance or adviser records before using figures in a cash-extraction plan.

- Employer pension contributions: move surplus profit into pension

Use this when you do not need the cash personally now and want company-funded long-term saving. This can reduce taxable profits when deductible, but employer contributions still count toward your annual allowance and may require carry forward. Confirm current allowance and carry-forward details from official HMRC guidance, provider records, or adviser records before sizing the contribution.

| Route | Use it when | Tax step | Documentation to keep |

|---|---|---|---|

| Salary | You need regular pay and payroll record | PAYE, Income Tax, National Insurance | Payroll reports, payslips, RTI records, bank payment proof |

| Dividend | You need personal spending cash from profits | Not deductible for Corporation Tax | Approval record, dividend voucher, bank payment proof |

| Employer pension contribution | You want to move surplus company profit into pension | Deductible only if wholly and exclusively for the trade | Internal approval note, provider receipt, company bank proof, bookkeeping entry |

2. Run a wholly-and-exclusively checklist before payment#

Pass this test before money leaves the company account. HMRC looks at whether employer pension contributions are incurred wholly and exclusively for the trade, and for close/connected cases it considers the combined remuneration package (salary, benefits, and pension) rather than pension in isolation.

| Check | What the article says |

|---|---|

| Commercial rationale | Confirm total remuneration is defensible for your role and value to the business; risk increases where connected people are paid significantly more than comparable unconnected workers |

| Records | Keep an internal decision record, provider confirmation, and proof that payment came from the company account; include this decision there if your company keeps board records for director decisions |

| Consistency | Check salary, benefits, and pension together against duties, profits, and affordability |

Check the current HMRC interpretation in official HMRC manuals or adviser records before relying on this test.

3. Execute in filing order to avoid avoidable errors#

Classify first, then pay, then bookkeep. Select the correct contribution type with the provider at setup, pay employer contributions from the company bank account, and record them as employer pension contributions in your accounts and year-end filing.

Do not rely on intent or accrual alone. Corporation Tax relief depends on contributions actually being paid, and deduction timing does not automatically follow the accounting entry.

Before you submit payment, confirm timing, affordability, annual-allowance impact, and accountant sign-off. That control step prevents common failures: misclassified payments, timing mismatches, and weak evidence. Related: Understanding the UK's Statutory Residence Test (SRT).

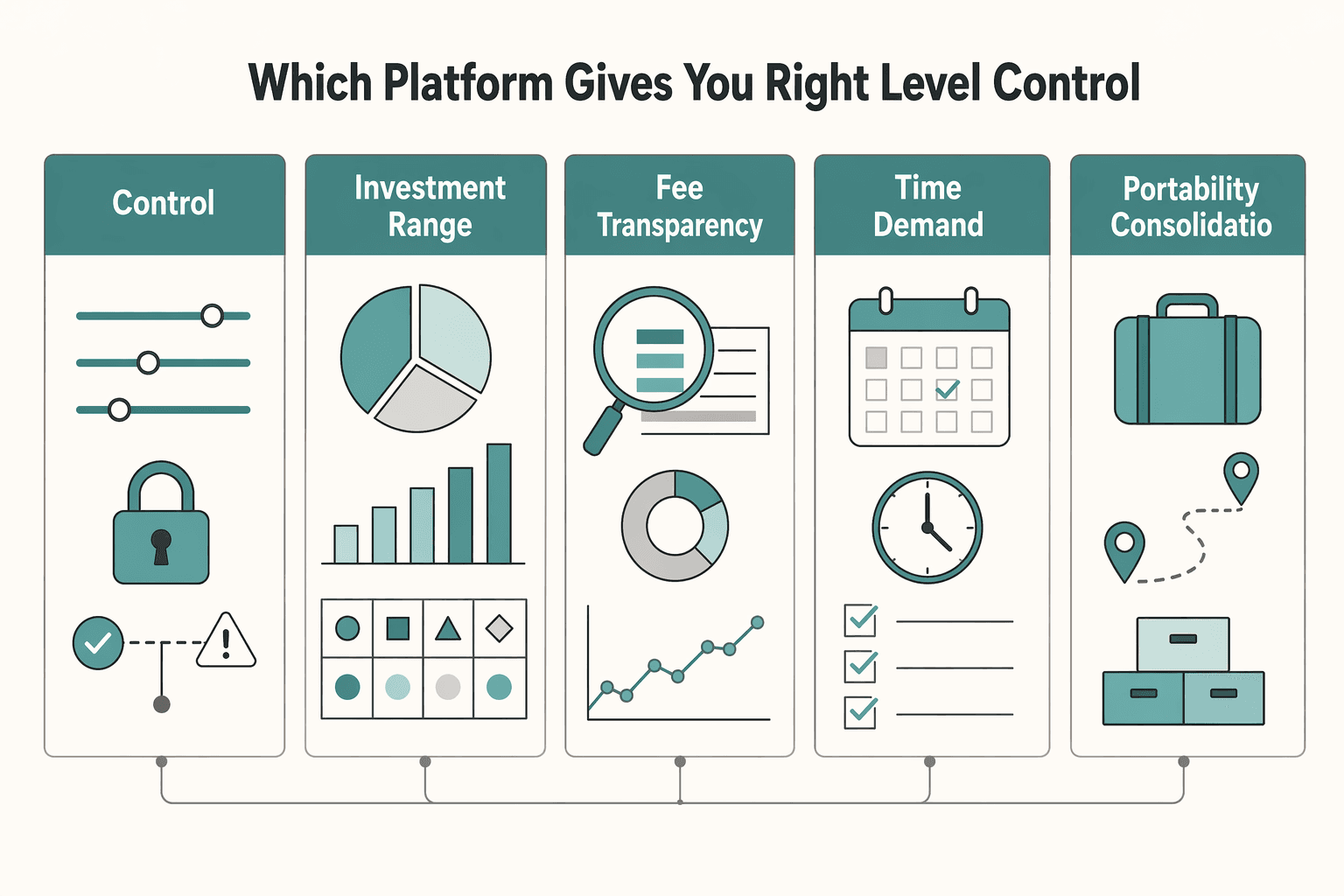

SIPP vs. Personal Pension: Which Platform Gives You the Right Level of Control?#

Pick the platform you can manage and document consistently each month, not the one with the strongest marketing.

- If you want more hands-on control, evaluate SIPP options first and verify the details

Start with three checks: can you choose investments confidently, will you review and rebalance on schedule, and are you comfortable using the platform settings without guesswork. Before funding, request the live investment menu, current charges, transfer terms, and contribution handling notes. If you cannot commit to ongoing review, do not assume a control-heavy setup will help.

- If you want fewer moving parts, evaluate personal pension options first and verify what is still on you

Keep the setup simple, but confirm exactly what is defaulted by the provider and what still needs your input. Ask what happens when contributions arrive, what you must choose, how reviews are expected to work, and how to download contribution records and statements. Simpler administration is useful only if you can still retrieve clean records at filing time.

- Compare workload and evidence requirements before comparing brands

Vanguard SIPP, AJ Bell, and PensionBee are examples only, not automatic recommendations. Confirm current platform options and charges in provider documents before shortlisting.

| Decision point | What to confirm before choosing |

|---|---|

| Control | Which decisions you make vs which are provider-set |

| Investment range | The live menu and any dealing or access limits |

| Fee transparency | Current tariff, key features, and transfer-related charges |

| Time demand | Real monthly review effort you will maintain |

| Portability/consolidation | Transfer-in/out steps, paperwork, and restrictions |

| Common pitfalls | Overestimating your follow-through or assuming "simple" means "fully automatic" |

Whichever route you choose, keep evidence ready: HMRC expects records such as bank statements or receipts, and online filing requires your UTR. If you are newly filing or re-entering Self Assessment, you must tell HMRC by the October notification deadline; missing it can lead to penalties. If you already had an account, reactivate it before filing to avoid delays. Some taxpayers cannot use online filing and must use commercial software or other forms. Self Assessment tax bills are due by 31 January.

Use this quick filter for your next step:

- Short on time: prioritise the option with the lightest ongoing review burden.

- Confident investor: shortlist options only after confirming the exact controls you will have.

- Need customization: verify it in current plan documents, not assumptions.

- Need simplicity: prioritise statement clarity and easy record retrieval.

For a step-by-step walkthrough, see The Best Superannuation Funds for Australian Freelancers.

How to Master Your Pension in a "Feast or Famine" World#

Once you have chosen the pension type, your next job is cashflow control. With irregular income, a fixed monthly promise is usually less reliable than a rule tied to money you have actually received.

| Mode | When it applies | Article guidance |

|---|---|---|

| Minimum contribution mode | Cash is tight | Stick to your base percentage |

| Catch-up mode | Surplus cash is genuinely available | Add extra only when surplus cash is genuinely available |

| Pause/restart mode | Your cash buffer drops below your floor, then reserves recover | Pause contributions when your cash buffer drops below your floor, then restart after reserves recover |

- Use a percentage trigger, not a hopeful monthly amount. Pick one percentage of each paid invoice and treat it as a standing rule. That gives you automatic scaling in strong months and lower pressure in lean months.

Keep the workflow simple and visible: - payment received into your business or personal account - allocate your pension percentage immediately into a separate holding pot - transfer to the pension on your chosen schedule (for example, weekly or monthly) - reconcile the bank payment, provider confirmation, and contribution line in your books

Keep contribution guardrails in view. For the 2025/26 tax year, the standard annual allowance is £60,000 for most people, and it resets on 6 April. For defined contribution pensions, both employer and personal payments count toward that allowance.

If you are contributing personally, tax relief is generally available on private pension contributions worth up to 100% of your annual earnings. In relief-at-source arrangements, the provider adds basic-rate relief to your pension pot. After each transfer, store the bank evidence and pension receipt together so your records are usable later.

- Use clear modes for lean and feast months. A three-mode system helps you act quickly without guessing.

- Minimum contribution mode: stick to your base percentage when cash is tight. - Catch-up mode: add extra only when surplus cash is genuinely available. - Pause/restart mode: pause contributions when your cash buffer drops below your floor, then restart after reserves recover.

Carry forward can support catch-up months, but only when conditions are met. You can use unused annual allowance from the 3 previous tax years, but not from years when you were not a member of at least one UK registered pension scheme. If MPAA applies, unused MPAA cannot be carried forward, and tax-relieved saving may be limited to £10,000 a year.

Use carry forward for real surplus periods, not by default. If core obligations and runway are not yet ring-fenced, hold cash first and contribute later.

- Check funding flexibility before choosing a provider. For irregular income, contribution mechanics often matter more than branding.

| Provider | Ad hoc contribution support | Pause or reduce | Contribution methods | Watch-out |

|---|---|---|---|---|

| PensionBee | Supports flexible contributions | States no penalty for ceasing, reducing, or altering contributions | Direct debit, standing order, bank transfer, Easy Bank Transfer | Verify how contribution history and receipts are exported before funding heavily |

| AJ Bell | Supports one-off and regular payments | Verify current pause process on your exact pension | Employer: bank transfer or direct debit; personal: debit card, instant bank transfer, or regular direct debit | Personal regular payments shown at £25 to £4,000 monthly in the cited FAQ |

| Vanguard personal pension | Supports single or monthly personal payments | Verify current pause process | Personal payments: monthly or single (from £500); company contributions: single lump sums only from a company debit card | Not a fit if you need regular company direct debits or bank transfers |

- Treat large one-off contributions as an accounting event. Big catch-up payments can help, but timing and documentation need to be checked before you send money.

Before a large one-off contribution, ask your accountant or bookkeeper to confirm contribution type, tax-year timing, and how it should be recorded. Vanguard explicitly advises accountant coordination for company contributions, and that is a useful discipline more broadly. If needed, request pension-saving details from each provider before relying on carry forward.

Once you know how you will fund, pause, and document contributions, provider choice becomes much clearer.

Choosing Your Platform: A Strategic Breakdown of Top UK Providers#

Choose the provider you can operate cleanly, not the one with the strongest marketing. If you cannot confirm current fees, contribution routes, and usable records before funding, treat that as a stop signal.

Your setup matters here. The business structure you choose affects tax and legal responsibilities, and a limited company is legally separate from its owners. If you file Self Assessment, you also need clear records (for example bank statements or receipts), your UTR to file online, and enough documentation to support your return before the 31 January payment deadline.

| Provider | Best fit | Fee structure | Investment control | Operational trade-offs | Who should avoid it |

|---|---|---|---|---|---|

| Vanguard personal pension | You want a shortlist candidate and will verify details before moving money | Confirm current platform and fund charges directly | Confirm current fund choice and dealing limits directly | Check how easily you can export contribution history, receipts, and statements for reconciliation | Avoid if you need features the provider will not confirm in writing |

| PensionBee | You want a shortlist candidate and need a clear transfer and contribution trail | Confirm current all-in costs directly | Confirm current investment choice and limits directly | Check transfer paperwork, contribution confirmations, and year-end statements before consolidating pots | Avoid if key process details are not documented up front |

| AJ Bell | You are comfortable validating setup and documentation details yourself | Confirm current custody, dealing, and other charges directly | Confirm what you can hold and how contributions are handled directly | Check how personal vs company payments appear in statements and exports | Avoid if you want a low-touch setup without reviewing fine print |

Vanguard personal pension#

If you shortlist this, run one practical test before transferring: request the current fee schedule and a sample contribution confirmation. You need to see whether bank evidence and pension records match without manual cleanup.

When this breaks down, it is usually a workflow mismatch. You assumed the current setup fit your contribution pattern, then discovered the reporting flow did not fit your books.

PensionBee#

Use this only if the transfer flow and record trail are clear for your own files. Ask what you receive per contribution, what the annual statement shows, and what documents you can produce later if your accountant asks.

This breaks down when consolidation starts before documentation is in place. Save transfer forms, provider confirmations, and bank records before you move old pots.

AJ Bell#

With AJ Bell, verify admin mechanics before you commit. Ask how contributions are labelled, how statements export, and what evidence you can pass to your accountant when payment sources vary across the year.

This breaks down when you want flexibility but do not reserve time for reconciliation. Extra control only helps if you can still close the year with clean records.

Before you act, run this quick check:

- Portfolio size band: small, growing, or substantial; confirm the current fee schedule for your band.

- Control level: minimal decisions vs regular hands-on involvement.

- Admin time budget: pick the provider whose records you will actually maintain.

- Contribution pattern: ad hoc, regular, personal, company, or mixed; match your real pattern, not an ideal one.

Conclusion: Your Next Move as CEO of 'Me, Inc.'#

Treat this as an execution checklist, but separate verified facts from open questions. The grounding available here supports Australian GST/ABN process points, and does not substantiate UK pension-specific limits, carry-forward, or provider comparisons.

- Match your setup to the correct regulatory path

Before acting, confirm which jurisdiction this decision sits in. For Australian GST process, the grounded checkpoints are clear: you generally need an ABN before standard GST registration, and once GST registration is required, you must register within 21 days (with penalties possible if you do not).

- Choose a repeatable compliance record rule

Pick a documentation habit you can keep: save the terms you relied on, the relevant confirmation notice, and the matching payment records. For GST workflows, keep the effective registration date and filing/payment cadence in your working notes.

- Use operating fit, not brand familiarity, as your filter

Where Australian non-resident GST is relevant, choose between standard and simplified registration based on operational needs. Simplified registration supports electronic registration/lodgment/payment, but it does not allow tax invoices or GST credit claims.

One last control for 2026: if your decision is UK pension-specific, verify current UK rules and provider terms from UK primary sources before acting, because that evidence is not established in the available sources.

Frequently Asked Questions

What is usually the most tax-efficient way for you to contribute if you run a limited company?

There is no single "most tax-efficient" method confirmed by the available sources. What is supported is that a limited company is legally separate from its owners, and your business structure affects tax and legal responsibilities. Next, confirm your business structure first, then verify current HMRC rules before deciding how to contribute.

SIPP vs. personal pension for a freelancer: which should you choose?

The available sources do not provide enough evidence to recommend a SIPP over a personal pension, or the reverse. Next, treat this as an open decision and verify current product terms and HMRC rules before choosing.

How much should you contribute when your income moves around?

The available sources do not set a recommended contribution amount. They do support keeping records such as bank statements or receipts for Self Assessment. Next, base contributions on income actually received and keep clear records for each payment.

Can you pause pension contributions?

The available sources do not confirm pause, restart, or direct debit rules for pension providers. Next, check your provider's current terms before building your cashflow plan around pausing contributions.

Is Vanguard or PensionBee better for you?

The available sources do not support provider comparisons or rankings. Next, request current terms directly from each provider and decide based on your own requirements.

What is the difference between an employer contribution and a personal contribution?

From these sources, the grounded point is that a limited company is legally separate from its owners, and business structure affects tax and legal responsibilities. Specific pension treatment for employer versus personal contributions is not established here. Next, verify the current rules before finalizing your bookkeeping approach.

Can you use a LISA instead of a pension?

The available sources do not provide enough evidence to decide whether a LISA should replace a pension. Next, verify current official rules before choosing between them, and if you file Self Assessment online, have your UTR ready, keep supporting records, file on or after 6 April, and plan to pay by 31 January.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- abr.gov.au/business-super-funds-charities/applying-abn/...trusted

- ato.gov.au/businesses-and-organisations/gst-excise-and-...trusted

- ato.gov.au/businesses-and-organisations/international-t...trusted

- community.ato.gov.au/s/question/a0J9s0000001Dmq/p-00029303trusted

- legislation.gov.uk/ukpga/1999/30/section/11trusted

- gov.uk/personal-pensions-your-rightsexternal

- gov.uk/guidance/director-information-hub-income-tax...external

- moneyhelper.org.uk/en/pensions-and-retirement/tax-and-pensions/...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Japan Digital Nomad Visa 2026: Six-Month Planning Runbook

Treat this as your operating model: identify the right mission first, commit to one route, and keep dated records before you make irreversible plans. That is what keeps the rest of your timeline, paperwork, and decisions coherent.

Understanding the UK's Statutory Residence Test (SRT)

Treat SRT like ops, not folklore. You want a repeatable workflow you can run monthly so your tax-year answer is boring, documented, and easy to defend.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.