Quick Answer

Choose the best payroll software in india by matching it to your legal structure and payment trail, not by counting HR features. For this workflow, start with foreign revenue records, then recurring India compliance, then owner pay. If you run a company, use a real salary process with TDS records; if you are a proprietor, keep drawings clearly classified. Keep export documentation retrievable, and confirm LUT handling before invoicing under the export-without-IGST route.

You're Not an HR Manager. Stop Searching Like One.#

If you are a solo operator or a very small team, the best payroll software in india is usually not the one with the longest HR feature list. It is the one that helps you collect foreign revenue cleanly, keep India filings defensible, and pay yourself in a way that matches your legal structure.

That framing matters because many founder-operators buy payroll the way a larger HR team would buy payroll. They compare leave rules, employee self-service, or performance add-ons first.

For a lean setup, the real sequence usually runs the other way. Money comes in from abroad, your bank trail has to hold up, your books and tax records need to match that trail, and only then does the payroll layer become useful. If the first two layers are weak, a polished payroll dashboard does not solve the problem. It just makes a weak process look organized.

1. Collect international revenue in a way your bank can defend#

Start with money coming in, because that is where the paper trail begins. RBI directions under FEMA make it obligatory for the exporter to realise and repatriate the full value of goods or services to India. The AD bank handling your export documents is expected to ensure compliance with FEMA rules. So your first software question is not leave tracking. It is whether your collection path gives you usable proof, a clean bank trail, and purpose-code clarity for forex reporting.

| Pre-invoice check | What to confirm |

|---|---|

| Client details | Client name and address match the contract |

| Invoice sequence | Invoice number and date are sequential |

| Service description | Specific enough for your bank and your books |

| Payment terms | Currency, amount, and payment route are fixed before sending |

| Evidence pack | Invoice, contract or SOW, bank credit proof, and FIRC or FIRA if your route provides it are recoverable later |

Use that same five-point check before you invoice each cycle.

In practice, treat each invoice as the start of a file, not a one-off PDF you send and forget. Put the contract or SOW, the final invoice, and the eventual bank credit proof into the same folder or record. If your collection route gives you FIRC or FIRA, save that there too. When your bank, accountant, or tax reviewer asks what a particular inward remittance relates to, you want to answer by opening one complete packet, not by searching three inboxes and a bank statement.

The service description deserves more care than many founders give it. A vague line item may look harmless when the client is happy to pay, but it becomes a weak point when you later need to explain the remittance against your books. The goal is not to write a long invoice. It is to make the description specific enough that the contract, invoice, bank credit, and accounting entry all tell the same story. That same discipline also helps when you reconcile multiple receipts in the same month and need to match them to the right export records.

For GST, the key lever is LUT under Rule 96A, filed in FORM GST RFD-11, if you are exporting without paying IGST upfront. CBIC guidance says the bond or LUT must be furnished before export, and later guidance says no physical document needs to be submitted for LUT acceptance. If you use LUT, make sure your invoice wording and records align with current export-without-IGST requirements, and keep the ARN in your records. Verify the current filing rule before you rely on it.

Operationally, the easiest way to stay out of trouble is to build that LUT check into your invoice routine. Before the first export invoice in the relevant period, confirm that the LUT has been furnished, save the ARN where you can find it quickly, and make sure the invoice template carries the required export-without-IGST language. That is a small setup step. It prevents a much messier clean-up later if you discover after billing that the paperwork did not line up.

A common failure mode is sending a generic invoice and then scrambling when the bank asks what the remittance was for. Another is treating FIRC and FIRA as interchangeable across routes. Both are used as proof of foreign transfer to India, but the issuance flow can vary by bank or provider. Verify what your route actually gives you before you depend on it.

There is also a sequencing failure that shows up in lean teams. The person raising the invoice, the person receiving the bank alert, and the person updating the books may all be the same founder, but the work still happens on different days. That is where errors creep in. An invoice goes out with one client name format, the bank credit arrives with another reference, and the accounting entry gets posted from memory.

The fix is simple and boring. Update the record when each event happens. When the invoice is sent, save it. When the money lands, attach the bank proof. When the remittance advice or FIRC/FIRA comes through, add it to the same file. Your software does not need to be glamorous here. It needs to make retrieval easy.

When comparing tools around this part of the workflow, ask narrower questions than "Does it support global payments?" Ask whether you can recover the invoice, the payment record, and the proof document quickly. Ask whether the accounting sync keeps the trail intact, and whether your route makes it clear what evidence you will receive after settlement. Those questions are much closer to the risk you are actually managing.

2. Keep recurring India compliance narrow and disciplined#

For a lean setup, the safest approach is to keep your recurring compliance list short and specific. In practice, that usually means GST records for exports, TDS if you are paying salary from a company, and Advance Tax where applicable.

| Compliance item | When it applies | Timing or rule in the article |

|---|---|---|

| LUT under Rule 96A | Exporting without paying IGST upfront | Filed in FORM GST RFD-11; bond or LUT must be furnished before export |

| Section 192 salary TDS | You run a company and pay yourself salary | Tax on salary is to be deducted at the time of payment |

| Advance Tax | Estimated liability is Rs. 10,000 or more | Section 211 shows four instalments during the financial year; the first line shown is 15th June at 15% |

| 44AD or 44ADA advance tax | You are a 44AD or 44ADA assessee | The whole amount is due by 15th March |

One key tax lever for owner payroll is Section 192. Its text says tax on salary is to be deducted at the time of payment. So if you run a company and pay yourself salary, you need a real pay run, not ad hoc transfers to your personal account. If you operate as a proprietor, do not assume "self payroll" is the right answer. Proprietor pay and company-owner pay need different treatment.

That distinction is where many software decisions go wrong. A founder sees "payroll" and assumes it is the universal answer to getting money out of the business. It is not. If you are paying salary from a company, the software should support an actual salary process with deductions and records that match the bank payout. If you are a proprietor, forcing your withdrawals through a salary-style flow can make the records less clear rather than more clear. The right discipline is to classify the payment correctly first, then choose the workflow that fits.

Advance Tax is the other discipline to get right. The cited Section 211 structure shows payment in four instalments during the financial year, with the first line showing 15th June at 15%. The CBDT tutorial also states that advance tax applies when estimated liability is Rs. 10,000 or more. For 44AD or 44ADA assessees, the cited text shows the whole amount due by 15th March. Use the path that fits your tax treatment, and verify current applicability before filing.

In day-to-day terms, do not wait until year-end to figure out whether your owner pay, invoices, and tax reserves still line up. A simple monthly check is usually enough for a small operation: what came in, what went out as salary or drawings, what tax has already been deducted if any, and what amount you are mentally treating as your tax reserve. You do not need a giant compliance calendar to do this well. You need a short list that you actually review.

A practical way to keep this narrow is to separate recurring tasks into three buckets:

- records that prove exports and foreign receipts

- payroll records if you are paying salary from a company

- tax-payment planning records for advance tax and any TDS already applied

Once those are separated, reviews get easier. If there is a mismatch, you know where to look. If a bank credit does not tie back to an invoice, that is an export-record issue. If a salary payment hit the bank without a payslip or deduction record, that is a payroll issue. If your cash balance looks fine but you have not reserved for tax, that is a tax-planning issue. Software helps when it keeps those buckets distinct instead of blurring them.

Once those recurring obligations are under control, the next decision is how you actually pay yourself.

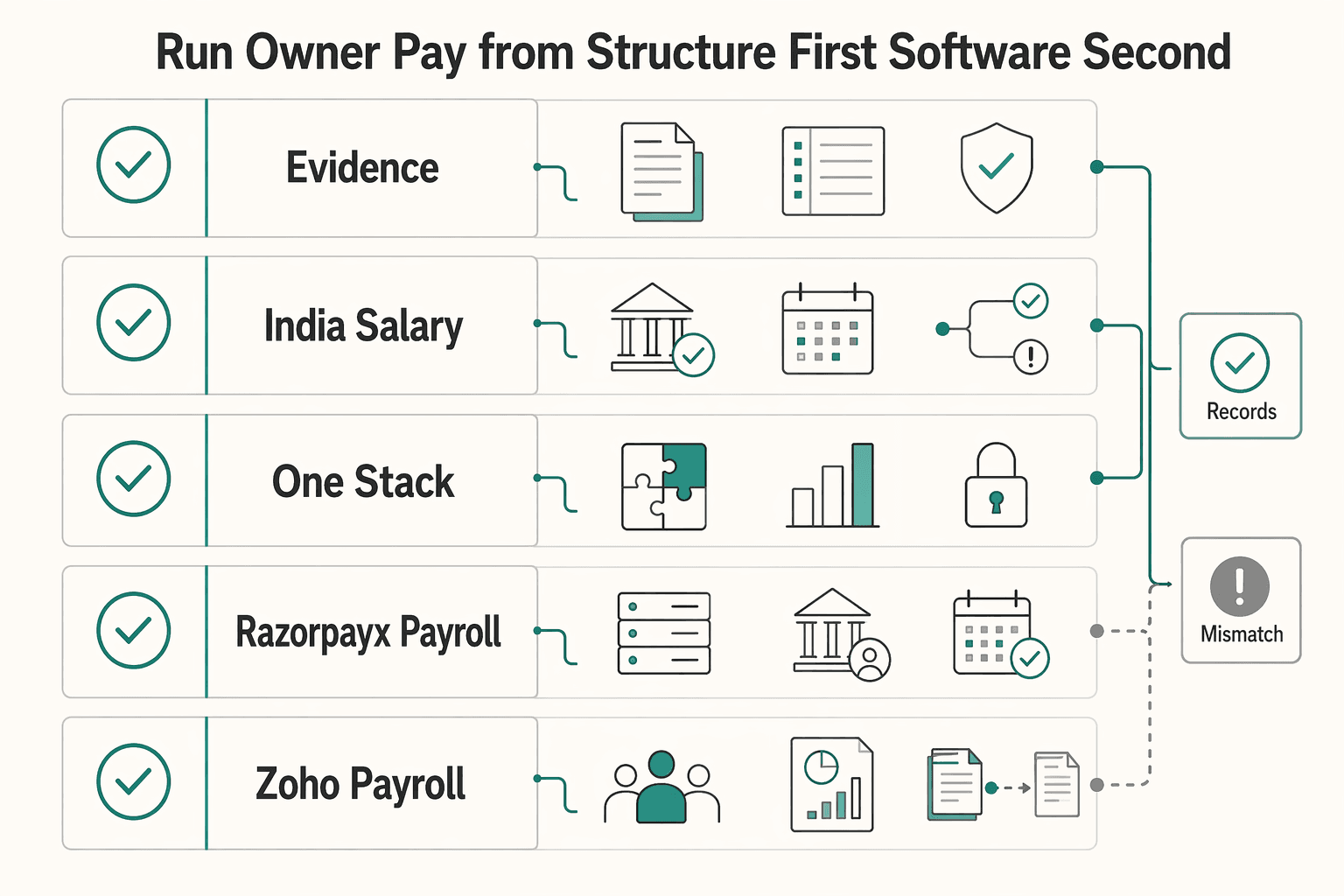

3. Run owner pay from structure first, software second#

Your pay path should follow your entity type. Only after that should you choose the tool.

| If your main risk is | Prioritize | Article guidance |

|---|---|---|

| Foreign collection evidence | Bank trail and export documents | Choose for bank trail and export documents first |

| India salary execution | Payout control versus reporting visibility | Choose RazorpayX Payroll or Zoho Payroll based on payout control versus reporting visibility |

| One stack across countries | A wider multi-country setup | Look at Deel, but do not let a global dashboard distract you from India-specific filing checks |

| Tool | Cross-border collection | Compliance artifacts | Payroll execution | Payout controls | Reporting visibility | Support fit |

|---|---|---|---|---|---|---|

| RazorpayX Payroll | Not a cross-border collection tool in the cited docs | Automates some statutory compliance, but docs say it does not file nil returns | Salary paid directly to employee bank accounts in India | Strong if you want bank-linked salary execution | Useful for India payroll ops | Best when India salary execution is the main job |

| Zoho Payroll | Not positioned here as a foreign collection rail | India tax-compliant positioning; generates statutory summaries; TDS liabilities created after pay-run approval | Good for structured India pay runs | Approval step matters because liabilities generate after approval | Good visibility for statutory summaries | Best when reporting and post-approval tax objects matter |

| Deel | Stronger fit if you also need global payroll or payment coverage | Built-in compliance and dashboard visibility are core pitch points | Designed for global payroll operations | Better for multi-country payment complexity | Strong central dashboard | Best when India payroll is only one part of a wider global stack |

These tables are most useful if you read them in the order of your own risk. If your immediate problem is paying India salaries correctly from a company account, payroll execution and payout control deserve more weight than dashboard breadth. If your immediate problem is seeing liabilities and summaries clearly before and after approval, reporting visibility matters more. If payroll in India is only one line in a broader multi-country setup, the wider stack may matter more than local convenience. The mistake is to treat every feature as equally important when your actual operation is narrow.

Before each payroll run, check four basics: entity type, salary structure, current TDS assumptions, and whether you are paying salary or taking drawings. If you are a company, keep the structure simple and documented with components that fit your actual setup. If you are a proprietor, treat owner withdrawals as drawings and keep a separate tax reserve instead of imitating payroll.

That pre-run check should happen before approval, not after money moves. If the entity type is wrong in your own head, everything downstream becomes harder: the classification in books, the deduction logic, the bank narration, and the year-end explanation. A short review before each run usually catches the issue early. Are you processing salary because salary is the correct treatment, or are you using payroll software simply because it is the easiest button to click? Those are not the same thing.

For a company-run salary flow, simplicity is a strength. A founder salary structure does not need to mimic a large employer's compensation policy to be valid and usable. It needs to be documented, repeatable, and easy to reconcile. When the pay run is approved, you should be able to point to the payslip, the deductions, and the matching bank payout without explaining away side transfers or one-off personal withdrawals mixed into the same month.

For proprietor drawings, the practical implication is simple: keep the owner withdrawal record distinct from employee salary records and keep your tax reserve logic outside the payroll engine. This makes later review easier because you are not trying to reverse-engineer which "salary" payments were actually just owner drawings.

Use this as the decision rule. If your main risk is foreign collection evidence, choose for bank trail and export documents first. If your main risk is India salary execution, choose RazorpayX Payroll or Zoho Payroll based on payout control versus reporting visibility. If you need one stack across countries, look at Deel, but do not let a global dashboard distract you from India-specific filing checks.

A good buying test is to walk one real payment cycle through the tool before you commit. Start with the way money enters the business, then ask how owner pay or employee salary would be recorded from that point forward. If the software looks strong in demo screens but leaves you unsure how you would retrieve proof documents, approve a pay run, or reconcile the bank debit to the payroll record, it is solving the wrong problem for your size.

If you want a deeper dive, read Value-Based Pricing: A Freelancer's Guide. If you want a quick next step, try the free invoice generator.

Conclusion: From Payroll Tool to Financial Command Center#

Once you separate money-in, compliance, and owner pay, the choice gets much clearer. The outcome you want is not a prettier HR dashboard. It is cleaner cashflow visibility, fewer payment delays, and lower compliance risk.

-

Implement now. Write down your operating setup on one page: entity type, how revenue comes in, whether you pay yourself salary or take drawings, and what evidence pack you keep for each payment. If you run a company, make payroll formal enough to produce payslips, deductions, and a bank trail. If you are a proprietor, do not fake payroll when drawings are the real treatment. The practical advantage here is traceability. A useful version of this one-pager is not theoretical. It should show the exact path from payroll inputs to bank credit to books to owner pay. If someone asked you next month how one specific payment moved through your system, the answer should already exist in that document pack.

-

Review monthly. Check the few records that actually move risk: statutory setup (such as TDS, PF, ESI, and professional tax), payroll approval flow, and whether approved payouts match payslips and bank entries. Verify current requirements before you act. Your software checkpoint is simple: it should automate calculations, generate compliant payslips, and integrate with attendance, leave, and accounting so compensation stays accurate and on time. For a lean team, the point of this review is not to create a long admin ritual. It is to catch mismatches while they are still easy to fix: attendance or leave data not reflected in time, a pay run approved with the wrong assumptions, or a bank payout that does not clearly match the payroll record.

-

Escalate to a tax advisor. Bring in help when the owner-pay structure changes, when you start paying salary from a company, or when statutory treatment is unclear. Also escalate if your records do not line up across payroll records, bank credits, payslips, and books. One payroll mistake can mean statutory penalties or employee dissatisfaction. The trigger for escalation is not only complexity on paper. It is also inconsistency in practice. If you keep finding that one system says one thing and your bank statement says another, that is the moment to stop improvising and get a clean answer before the mismatch compounds.

| If your main need is... | Choose software for... | Verify before buying |

|---|---|---|

| Payroll visibility | clean records and monthly clarity, not extra HR features | payslip detail and accounting sync |

| Compliance workflow | statutory updates, payslips, and approval controls | TDS/PF/ESI/professional tax coverage and audit trail |

| Payroll execution | accurate, on-time salary processing | attendance and leave sync, plus bank reconciliation |

| Reporting clarity | gross-to-net visibility and monthly summaries | deduction views and accounting exports |

If you came here looking for the best payroll software in india, use that table as your decision rule. Shortlist two options today, ask each vendor to show a live payslip plus accounting integration, and compare the output against your own entity structure.

During that comparison, do not just ask what the product can calculate. Ask what you will be able to prove later: how a pay run was approved, how a payout appears in the bank, how a statutory summary is generated, and how quickly you can recover the underlying records when someone asks.

If contractor payments are part of the picture too, read How to Manage and Pay a Global Team of Contractors Compliantly next. Then review your pricing so taxes and payment friction are covered before the next invoice cycle.

Related: What to Do If You've Been Misclassified as an Independent Contractor.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- cbic-gst.gov.in/pdf/circularno-2-gst.pdftrusted

- cbic-gst.gov.in/hindi/IGST-bill-e.htmltrusted

- grow.exim.gov/hubfs/ebook/basic-guide-to-exporting_Latest_...trusted

- incometaxindia.gov.in/_layouts/15/dit/Pages/viewer.aspxtrusted

- incometaxindia.gov.in/_layouts/15/dit/Pages/viewer.aspxtrusted

- wise.com/help/articles/2655509/whats-a-foreign-inward...trusted

- deel.com/solutions/payrollexternal

- deel.comexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

What to Do If You've Been Misclassified as an Independent Contractor

Treat this as a protection problem first, not a label debate. If your work was treated as an independent contractor arrangement even though the relationship functioned differently, your first goal is to protect pay, rights, and records while you choose the least risky escalation path. You can do that without making accusations on day one, which often keeps communication open while you document what happened.

How to Pay International Contractors With Fewer Delays and Disputes

Paying international contractors reliably starts with compliance setup before the first invoice. Missed registration or filing steps turn routine payouts into delays and penalties.