Quick Answer

Solo consultants usually do not need traditional PRM software unless they run an affiliate or reseller program. For most direct client work, the better decision framework is clients, platforms, and compliance: control scope and approvals with a detailed SOW, make invoicing and payment terms explicit, track payout costs and hold times, and keep the records needed to verify obligations when asked.

You Searched for PRM Software. Here's the Strategic Framework You Actually Need.#

You searched for best prm software, and that intent makes sense. Most 2026 PRM roundups compare tools for companies running partner programs, and at least one of those lists is presented alphabetically rather than as a true ranking. If your day-to-day friction is client handoffs, payment operations, or recordkeeping, you are making a different decision than a VP of channel sales.

A quick check helps. If you need lead and opportunity tracking, deal registration, and partner onboarding and lifecycle workflows, you are in classic PRM territory. If not, forcing a partner-network tool onto your business may add admin without fixing the bottleneck you care about most. Use this article's three-part model instead:

| Decision lens | PRM use (partner programs) | If you are not running a partner program |

|---|---|---|

| Core use case | Manage affiliates, resellers, or distributors | Manage client delivery, platform dependencies, and operating risk |

| Workflow owner | Channel or partner team | You |

| Primary risk | Slow partner response, lost leads, weak visibility across sources | Missed handoffs, payment operations friction, unclear obligations |

| Success metric | Partner alignment, revenue contribution, less manual work | Faster payment cycles, fewer surprises, cleaner operations |

- Clients

Focus on the work and paperwork that keeps projects moving. Your checkpoint is simple: can you show what was agreed, what was delivered, and what is billable without digging through scattered email?

- Platforms

Some of your revenue may depend on marketplaces, payment tools, or partner portals. The practical question is whether a platform reduces admin or adds a new point of failure when a payout, approval, or account review stalls.

- Compliance

You need enough structure to produce the right records when asked, not scramble after the fact.

If you actually run an affiliate or reseller program, this article is not your main path. Start with How to Create a Channel Partner Program. Related: How to Set Up an Affiliate Program for Your SaaS Product.

What is Traditional PRM Software (and Why It Fails You)?#

Traditional PRM software is a channel-sales system: it helps companies manage partner networks such as resellers, affiliates, and integration partners. The classic setup is a centralized portal where partners access resources, register deals, and track commissions. That model is useful when many external sellers influence the same pipeline.

| Function | Useful when | Note for direct client work |

|---|---|---|

| Deal registration and lead distribution | Multiple partners may pursue the same account and you need conflict control | If you source and close your own work, this usually does not solve your main bottlenecks |

| Content libraries and document sharing | You need to distribute partner-facing sales materials at scale | If your daily risk is scope clarity, approvals, and proof of delivery, static asset libraries are not the core fix |

| Commission and incentive management | Indirect partners are paid for sourced or closed revenue | If you deliver directly to clients, the financial risk is typically approval, invoicing flow, and payment reliability |

| Centralized partner portal and integrations | You need a single partner hub in large channel programs | Traditional PRM is often described as siloed, with integration gaps across CRM, marketing automation, finance, and BI that can create manual reconciliation work |

Your fit question is simpler: does your revenue depend on managing many selling partners, or on running clean direct client delivery yourself?

- Deal registration and lead distribution

Useful when multiple partners may pursue the same account and you need conflict control. If you source and close your own work, this usually does not solve your main bottlenecks.

- Content libraries and document sharing

Useful for distributing partner-facing sales materials at scale. If your daily risk is scope clarity, approvals, and proof of delivery, static asset libraries are not the core fix.

- Commission and incentive management

Useful when indirect partners are paid for sourced or closed revenue. If you deliver directly to clients, your financial risk is typically approval, invoicing flow, and payment reliability.

- Centralized partner portal and integrations

Useful as a single partner hub in large channel programs. Traditional PRM is also often described as siloed, with integration gaps across CRM, marketing automation, finance, and BI, which can create manual reconciliation work.

A quick fit-check:

| Check | PRM fit | Personal operations fit |

|---|---|---|

| Buyer type | You run a company selling through channel partners | You run mostly direct client engagements |

| Revenue model | Indirect revenue via partners | Direct delivery and direct payment collection |

| Operational risk owner | Channel team coordinating many partner motions | You managing contracts, delivery records, and payment follow-through |

This is not about rejecting software. It is about choosing the right operating model for how you actually work across clients, platforms, and compliance.

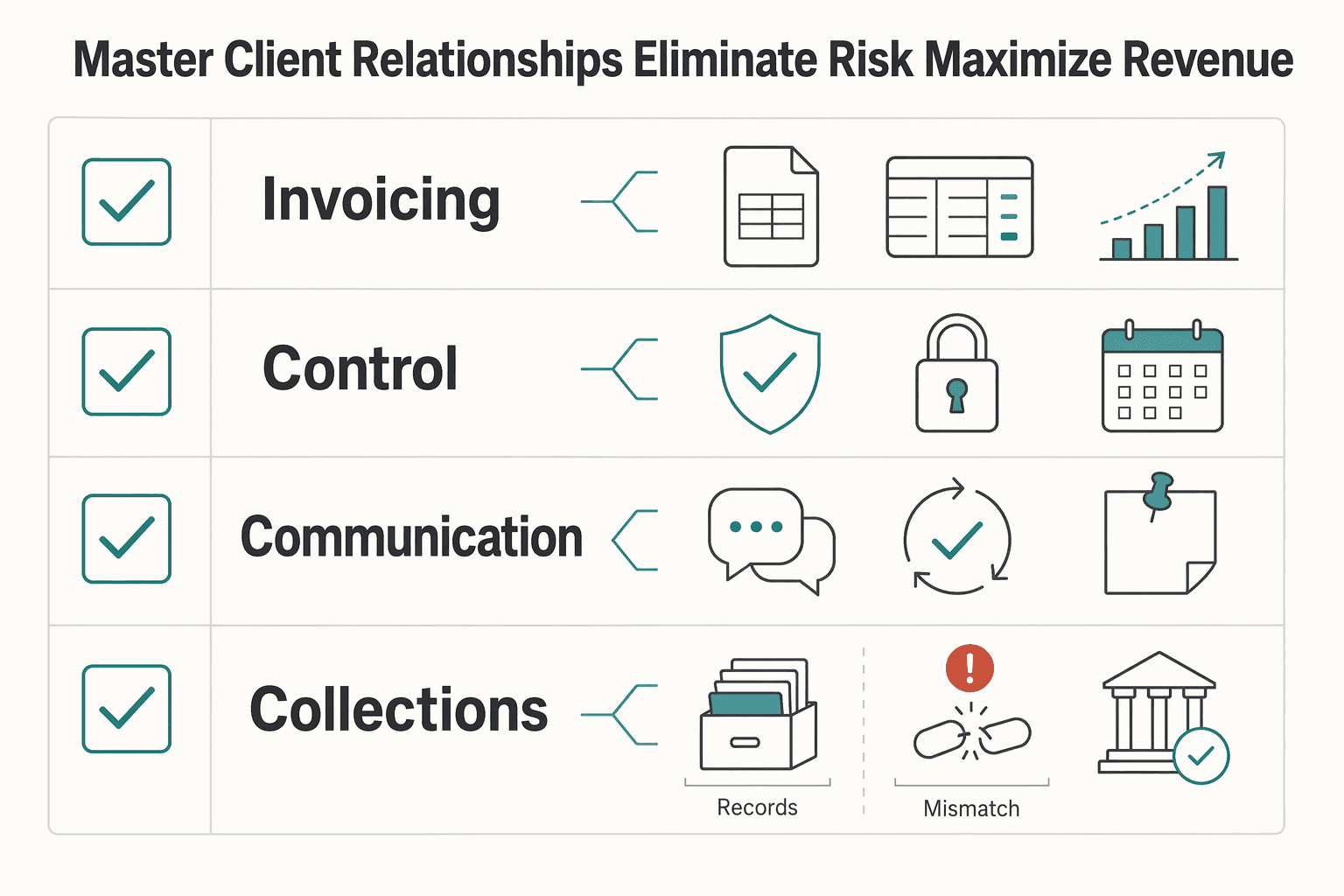

Pillar 1: Master Client Relationships to Eliminate Risk & Maximize Revenue#

Your client process should work as a risk-control system, not just admin. If you make scope, approvals, invoicing, and payment rules explicit up front, you reduce disputes and make revenue collection more reliable.

Poor communication and scattered records are common failure points. Treat a formal agreement, regular check-ins, a consistent feedback loop, and one centralized record as core controls, not optional extras.

| Area | Basic freelancer admin | Risk-managed client operations |

|---|---|---|

| Invoicing | Send a PDF after delivery | Run a pre-send checklist for client finance fields, tax treatment, legal entity details, and required wording |

| Scope control | Proposal or email summary | Signed SOW with scope, acceptance criteria, revision boundaries, and a documented change-request path |

| Communication | Updates split across email/chat | Centralized record for documents, contacts, approvals, meeting notes, and feedback |

| Collections | Follow up only after late payment | Terms confirmed at kickoff, billing structure set early, reminder cadence pre-defined, payment method approved in advance |

Run this as one system: scope drives billing, billing depends on correct finance setup, and both depend on a clear approval trail.

- Pre-send invoice checklist

Before sending, confirm the invoice matches the signed SOW and includes all required fields: client legal entity details, billing contact, any required internal reference, your legal entity details, stated tax treatment, and jurisdiction-specific wording where required. Verify jurisdiction-specific wording from official records, adviser guidance, or client source records before use.

Prioritize completeness over formatting. A polished invoice still gets rejected when required fields are missing or tax treatment is unclear. Keep a client-specific billing profile in your centralized record so each invoice uses approved details instead of memory.

- SOW control framework

Use the SOW to lock four items before work starts: scope definition, acceptance criteria, revision boundaries, and the change-request path. This is what turns extra requests into billable amendments instead of informal scope creep.

If a request changes deliverables, timing, assumptions, or review rounds, route it through the same written process every time: document the request, define impact, get written approval, and attach the amendment to the existing record.

- Payment execution flow at kickoff

Confirm payment terms at kickoff, then make sure the same terms appear in both SOW and invoice. If a client terms policy applies, verify it from the contract or source record before use. Choose billing logic early, whether deposit, milestone, or final invoice, based on project risk and delivery structure.

Set reminder cadence when issuing the invoice so collections follow a process, not a scramble. Use only pre-approved payment methods, and keep regular meetings plus a feedback loop so you have a clear record if payment slows.

Treat these as one operating unit. A formal agreement prevents avoidable disputes, centralized records keep facts visible, and disciplined billing removes common payment friction. For pricing structure depth, read Value-Based Pricing: A Freelancer's Guide.

Pillar 2: Tame Platform Partnerships to Protect Your Profit#

Your margin depends on how each platform handles payouts, not on brand reputation. Treat every marketplace, payout provider, and referral channel as a vendor relationship you actively manage, because headline fees rarely show the full cost.

| Cost or risk factor | What to verify | Why it matters |

|---|---|---|

| Platform withdrawal fees | Include them in the full payout-cost view and in the end-to-end reconciliation | Affects the final landed amount |

| Currency-exchange costs | Check the shown conversion rate and final landed amount | Affects what you keep after conversion |

| Transfer charges | Account for them before you price work | Affects the bank receipt and landed amount |

| Hold times | Check when funds are released | Adds operating risk |

| Dispute or reversal exposure | Treat uncertainty as cost until verified | Can reduce what you keep |

The practical standard is simple: if you cannot explain how funds move, when they are released, and what is deducted, you are carrying platform risk.

- Calculate true payout cost

Use a full payout-cost view before you price work. At minimum, include platform withdrawal fees and currency-exchange costs, then account for transfer charges, hold times, and dispute/reversal exposure as operating risk. Even with 5-10 high-value clients, one weak payout route can materially reduce what you keep.

Run one end-to-end reconciliation before committing to any route: platform statement, shown conversion rate, bank receipt, and final landed amount. If any step is unclear, treat that uncertainty as cost. Keep fee assumptions pending in your model until the current range is verified from platform records or provider terms.

- Compare payout options by transparency, speed, control, and retained income

Compare payout paths by how predictable and controllable they are, not by brand familiarity. That matters because pricing transparency can be incomplete in directories, making surface-level comparisons unreliable.

| Payout path | Transparency | Speed predictability | Controllability | Net retained income visibility |

|---|---|---|---|---|

| Marketplace-managed payout | Can be incomplete once FX and downstream charges apply | Tied to platform release rules and reviews | Low | Harder to forecast in advance |

| Independent payout provider | Clearer when fee logic and FX basis are explicit | More testable end to end | Medium | Easier to estimate before invoicing |

| Direct client bank transfer | Depends on bank disclosures and client AP process | Varies by corridor and approvals | Mixed: strong on terms, weaker on intermediary fees | Can be strong when total costs are known early |

In referral or channel-led deals, also review conflict handling and attribution logic. If those rules are unclear, payment risk rises even when nominal fees look acceptable.

- Build a channel mix so one platform cannot destabilize revenue

Dependency risk is concentration risk. Keep an active mix across marketplace, referral, and direct channels so a single policy or payout issue does not control your income.

Maintain one operating record per channel: current terms, payout reports, fee-page snapshots, support tickets, and attribution approvals. Then run this review checklist on a schedule:

- Have payout terms, fee logic, or FX handling changed since the last review? * Are hold times, failed payouts, or dispute resolution outcomes getting worse? * Can you still reconcile expected vs. landed amounts without guesswork? * Are account-risk signals increasing (verification friction, policy warnings, attribution conflicts)?

If multiple signals turn negative together, reduce exposure and route new work to a more controllable channel.

Pillar 3: Master Compliance, Your Most Critical Partnership#

Compliance is the operating relationship that keeps your business usable, so run it as a recurring workflow instead of a one-time setup. Most avoidable issues come from stale assumptions, missing documentation, or thresholds you planned to verify later.

| Workflow | Records to keep | Review timing |

|---|---|---|

| Presence tracking | Log where you sleep, where you work, and entry or exit dates by country; reconcile with passport stamps, flight records, and accommodation receipts | Review monthly and before visa renewals, long client projects, or any major location shift |

| Account and reporting obligations | Keep a live obligations register for tax authority, business registry, bank, payment provider, and any jurisdiction where your presence or income pattern may matter; store account confirmations, prior filings, notices, and adviser emails in one place | Review at quarter-end and before year-end |

| Client onboarding documentation | Confirm jurisdiction-compliant invoices, a detailed SOW, and the tax-form path; match legal name, tax ID details, and payee entity to your invoice setup | Decide before work starts and validate final form choice for the specific engagement |

A move does not always end prior obligations immediately. Depending on your facts, filing or reporting can still connect to where you were resident, where you are physically present, where clients pay you from, where accounts are held, or where your business is registered, so use a verification habit instead of assumptions.

- Presence tracking

Track presence continuously, then review before decisions. Keep a log of where you sleep, where you work, and entry/exit dates by country; review monthly, and do a deeper check before visa renewals, long client projects, or any major location shift.

Validate each jurisdiction rule directly instead of relying on memory. Keep the Schengen 90/180-day rule as one concrete example, and verify every other applicable country threshold from official jurisdiction records before use. Reconcile your tracker with passport stamps, flight records, and accommodation receipts so you are not reconstructing travel history when evidence is needed.

- Account and reporting obligations

Keep a live obligations register so nothing drops out of view after a move. List each place that may expect a filing, disclosure, or update: tax authority, business registry, bank, payment provider, and any jurisdiction where your presence or income pattern may matter.

Review this register at quarter-end and before year-end, with columns for status, owner, adviser needed, and current jurisdiction threshold pending official or adviser verification. Store supporting records by jurisdiction in one place, including account confirmations, prior filings, notices, and adviser emails, so you can confirm what is still active.

- Client onboarding documentation

Decide documentation before work starts, not after payment is blocked. For each engagement, confirm jurisdiction-compliant invoices, a detailed SOW, and the tax-form path early.

Use a simple onboarding decision check for W-9 and W-8BEN, then validate final form choice and withholding rules for the specific engagement against current official, adviser, or client source records. Match legal name, tax ID details, and payee entity to your invoice setup to reduce payment delays, unpaid work, and avoidable withholding issues.

Gruv: The First True "Personal Relationship Management" Platform#

If you searched for PRM software, your real operational problem is usually not partner recruitment. You are trying to keep delivery on track, get paid without friction, and avoid preventable compliance mistakes while managing about 5-10 high-value clients, not hundreds of resellers or affiliates.

Traditional PRM software is built for indirect channel sales. Your day-to-day model is different: you need one workflow that keeps your three critical relationships stable at the same time, with clients, platforms, and compliance authorities.

| Decision criterion | Traditional PRM tools | Gruv workflow |

|---|---|---|

| Compliance support | Usually centered on partner-program administration, not solo residency or filing exposure | Centered on solo risk controls, including presence tracking against rules like the Schengen 90/180-day rule and tax-form readiness at engagement start |

| Invoicing controls | Typically not the core function | Uses jurisdiction-aware invoicing plus detailed Statements of Work to reduce payment delays and unpaid work |

| Risk visibility | Focuses on channel pipeline, partner activity, and sales performance | Focuses on whether client payments, platform costs, and compliance obligations are creating friction or exposure |

| Operational fit | Best when you manage many partners in an indirect sales motion | Better fit when you run a small client book and need tighter control over delivery, money movement, and documentation |

Three practical checks keep this usable:

- Start each engagement with payment-ready documentation.

Use a detailed SOW, invoice setup that matches the engagement, and the correct tax-form path, such as W-8BEN or W-9 where relevant, before payment flow begins.

- Track presence as an ongoing compliance control.

For cross-border work, track physical presence against the exact threshold that applies, with 90/180-day as the concrete example here and other jurisdiction thresholds pending official verification before use.

- Measure what you keep, not just what you invoice.

Treat platform withdrawal fees, FX costs, and withholding risk as part of operating reality, not after-the-fact cleanup.

This approach is for you if your business runs inside the Clients-Platforms-Compliance model and you want tighter operational control over each engagement. It is not for teams primarily building reseller or affiliate channel programs; in that case, traditional partner relationship management software is the better fit.

Frequently Asked Questions

Do you actually need traditional PRM software if you work solo?

Not automatically. Traditional PRM is built for a different operating model, so first test whether the tool fits direct client work, is explainable, and keeps overhead low. If it forces process changes or presents legal-critical guidance without an official-source verification step, it is probably the wrong fit.

What should you evaluate instead of brand labels?

Start with fit. Ask whether the tool adapts to your business model or whether you must change core workflows to satisfy the software. If that creates missed handoffs or preventable admin errors, the brand label is not the important issue.

How do you tell whether a tool’s recommendations are trustworthy?

Ask for explainability. You should be able to see how the product reached a recommendation or why a status changed. If you cannot audit that logic, correcting mistakes becomes difficult.

What is a practical red flag during a trial?

Watch for unstable automation. If important statuses or recommendations swing too often, trust drops quickly. Frequent large changes during a trial are a practical warning sign.

Can you rely on legal or compliance guidance shown inside the app?

No. Treat in-app legal or compliance guidance as a starting point, then verify the current official text before you act. The app can surface an issue, but it should not be your final authority.

What capabilities matter most if your clients are international?

You need proof, not just reminders. The tool should keep billing details, supporting documents, and verification notes in one place. That makes it easier to support an invoice or decision when a client finance team or authority asks.

Are all PRM evaluation articles relevant to this decision?

No. Some articles surfaced for PRM software are actually about pricing and revenue management in multifamily operations, not partner relationship management or solo client operations. You can reuse generic checks like fit, explainability, and cost, but only after confirming you are evaluating the same category.

How do you know when a tool is too large or too expensive for your scale?

Ask what level of volume the product assumes. If the economics, setup effort, or oversight only make sense at enterprise scale, you are probably buying overhead instead of control. For a small direct-client book, a lean operations stack is usually a better fit.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cms.gov/regulations-and-guidance/guidance/manuals/do...trusted

- faa.gov/documentLibrary/media/Order/7110.65BB_Bsc_w_...trusted

- federalregister.gov/documents/2016/08/22/2016-18476/medicare-pro...trusted

- govinfo.gov/content/pkg/FR-2014-05-15/html/2014-10067.htmtrusted

- govinfo.gov/content/pkg/CHRG-117shrg51737/html/CHRG-117s...trusted

- hsr.ca.gov/wp-content/uploads/2022/02/2.-Exhibit-C-Miti...trusted

- osc.colorado.gov/sites/osc/files/FiscalProceduresManual.pdftrusted

- pmc.ncbi.nlm.nih.gov/articles/PMC12898330trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

How to Create a Channel Partner Program for a Business-of-One

You have probably reached the point where demand is real, but your capacity is still one person wide. If someone has told you to build a channel partner program, the problem may not be your ambition. Much of the advice in [channel sales for SaaS businesses](/blog/a-guide-to-channel-sales-for-saas-businesses) can feel geared toward more headcount, more process, and more admin appetite than a Business-of-One typically has.

How to Set Up an Affiliate Program for Your SaaS Product

This is not a small marketing experiment. You are taking on a sales channel that touches payouts, attribution, partner trust, and margin. If you run it solo, every vague rule and every edge case comes back to you.